Travel merchants rarely lose customer confidence at the moment of payment. They lose it after the payment, when plans change. A booking can be approved and confirmed, yet still leave the customer uncertain about what happens next: whether a change will be charged fairly, whether an ancillary add-on will process cleanly, or whether a refund will return in a predictable way if disruption occurs.

That post-booking uncertainty has become more commercially important in 2026 because travel is not a single checkout event. It is a payment journey that spans booking, changes, partial fulfilment, cancellations, and refunds, often across borders and involving multiple parties. Industry analysis from IATA has repeatedly highlighted that payments in travel have historically been treated as a back-office cost centre, despite shaping customer experience and operational outcomes across the entire journey.

This is why modernising payment flows is no longer just about adding methods or improving authorisation rates. It is about building payment experiences that remain reliable when travel becomes messy: clear payment states, predictable post-booking handling, and refund visibility that prevents uncertainty from turning into disputes.

- What Makes Travel Payments Different from Standard eCommerce

- Where Customer Confidence Breaks in 2026 Travel Checkouts

- The Modernisation Shift: From Pay and Confirm to Payment Journey Design

- How Airlines and OTAs Are Rebuilding Payment Architecture in 2026

- Refunds, Chargebacks and Disruption: The Confidence Layer Most Merchants Underbuild

- Fraud Controls That Don’t Destroy Bookings

- Airline Payment Systems: Why Distribution Modernisation Changes Payments Too

- Merchant Checklist: Signals Your Payment Flow Builds Customer Confidence

- Conclusion

- FAQs

What Makes Travel Payments Different from Standard eCommerce

Travel payments behave differently from standard eCommerce because the transaction does not end when the customer clicks pay. In most retail scenarios, payment and fulfilment are tightly coupled. In travel, payment initiates a chain of future events that may change, split, or reverse over time.

A single booking can involve multiple payment moments: the initial ticket purchase, ancillary add-ons such as seat upgrades or baggage fees, fare changes, reissues, and eventual refunds. These events may be processed days or weeks apart, often across borders and currencies. Each step introduces a new point of potential friction or uncertainty, particularly when issuers, acquirers, and travel intermediaries are involved.

From an ecosystem perspective, these characteristics are structural rather than operational failures. IATA has consistently noted that they stem from how travel is delivered, settled, and fulfilled across multiple parties, not from poor merchant execution.

From the customer’s perspective, confidence depends on continuity. When payments behave inconsistently between booking and post-booking changes, trust erodes quickly. Modern travel payment design therefore needs to support the full lifecycle, not just checkout.

Where Customer Confidence Breaks in 2026 Travel Checkouts

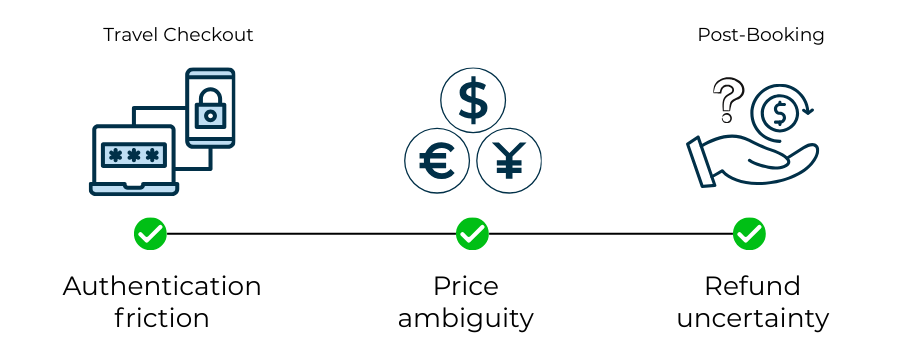

Customer confidence in travel payments rarely breaks because a card is declined. It breaks when the payment experience feels unpredictable or inconsistent with what the customer expects from a high-value booking.

High-friction authentication at the wrong moment

Strong Customer Authentication and issuer step-ups are now normal in travel payments. Problems arise when authentication is applied without context. Blanket challenges at checkout or during low-risk post-booking actions, such as adding a meal or selecting a seat, can signal unnecessary risk to the customer. In travel, that perception often leads to abandonment rather than reassurance.

Price and currency ambiguity

Travel customers are particularly sensitive to price clarity. Additional fees, FX mark-ups, or unclear currency presentation at the point of payment can undermine confidence immediately. Even small discrepancies between the advertised fare and the final charged amount create doubt, especially when customers anticipate future changes or refunds.

Refund uncertainty rather than refund denial

In 2026, many customer disputes still stem from uncertainty rather than refusal. When refund timelines, methods, or conditions are unclear, customers often assume the worst. That uncertainty frequently turns into chargebacks long before a realistic refund window has elapsed.

Confidence tends to break at the same pressure points:

Authentication that feels excessive or poorly timed

Unclear currency conversion or additional charges at checkout

Lack of visibility into refund timing and method

Confusing handling of changes or cancellations

The Modernisation Shift: From Pay and Confirm to Payment Journey Design

For many years, travel payments were designed around a single assumption: once the booking was paid and confirmed, the payment task was largely complete. Any subsequent changes, refunds, or disputes were treated as exceptions to be handled later by operations or customer support.

That assumption no longer holds in 2026. Modern travel payments are increasingly designed as journeys rather than moments. The payment experience now extends well beyond checkout, covering how changes are priced, how additional services are charged, how cancellations are processed, and how refunds are communicated.

This shift reflects how customers now judge reliability. A smooth initial checkout means little if a fare change triggers confusion or a refund feels opaque weeks later. As a result, travel merchants are rethinking payment flows as part of the overall experience. Payment states are made explicit, confirmations are clearer, and post-booking interactions receive the same attention as the original purchase.

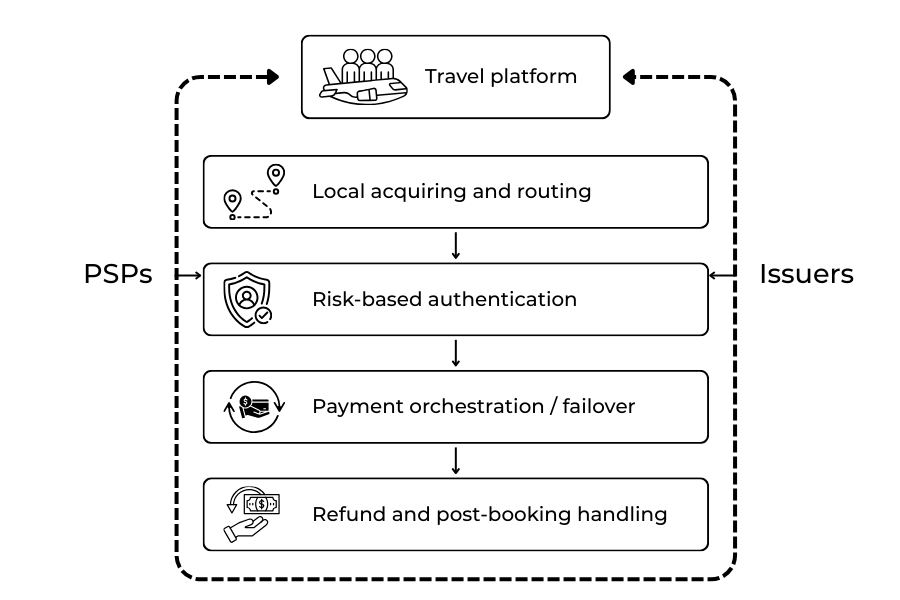

How Airlines and OTAs Are Rebuilding Payment Architecture in 2026

Airlines and online travel agencies (OTAs) are modernising payment architecture to reduce fragility across increasingly complex booking journeys. In 2026, the focus has shifted from optimising a single checkout to ensuring payments remain reliable across pricing changes, ancillaries, and disruption.

Local acceptance to reduce cross-border friction

Travel bookings frequently involve mismatches between the customer’s location, the point of sale, and the merchant’s acquiring setup. These mismatches increase issuer caution and decline rates. Airlines and OTAs are addressing this by routing transactions through local or regional acquiring paths, improving authorisation rates without changing the customer experience.

Authentication that balances fraud control and conversion

Leading merchants increasingly rely on risk-based authentication that considers booking value, route, device signals, and customer history. This allows higher-risk transactions to be challenged while lower-risk ones proceed with minimal interruption, preserving confidence at checkout.

Payment orchestration built for volatility

Travel demand is inherently volatile. System outages, issuer downtime, or sudden traffic spikes can quickly disrupt payments. To manage this, airlines and OTAs rely on orchestration layers that can reroute transactions, adjust retry logic, or switch payment rails when failures occur.

Architectural priorities in 2026 include:

- Local routing and acceptance optimisation

- Context-aware authentication strategies

- Failover and retry logic designed for disruption

- Payment handling integrated with post-booking changes

Refunds, Chargebacks and Disruption: The Confidence Layer Most Merchants Underbuild

In travel, customer confidence is tested most severely when things go wrong. Delays, cancellations, and missed connections are expected realities. What customers judge is not the disruption itself, but how payments behave once disruption occurs.

Many chargebacks in travel are driven not by fraud, but by uncertainty. When customers do not know whether a refund has been initiated or how long it will take, they seek control through their bank. From their perspective, a chargeback becomes a way to force clarity.

This is why refund handling is increasingly recognised as a confidence layer rather than a back-office function. Clear refund states and consistent communication reduce the emotional gap between a cancelled trip and the return of funds. Systems that handle initial bookings well but struggle with partial refunds or reissues quickly lose credibility. In 2026, improving confidence is less about promising faster refunds and more about making outcomes predictable.

Fraud Controls That Don’t Destroy Bookings

Fraud risk in travel is real, but heavy-handed controls often do more damage than the fraud they prevent. Applying blunt measures at checkout can undermine confidence at the exact moment customers are making a considered purchase.

High-performing travel merchants have moved away from binary decisions toward layered risk assessment. Rather than treating every booking as equally suspicious, controls account for context: route patterns, device consistency, and booking behaviour over time.

Industry analysis from IATA has repeatedly highlighted that false positives legitimate customers incorrectly challenged or declined represent a significant cost driver in travel payments. This has pushed merchants to design controls that are proportionate and adaptive. Confidence is preserved not by eliminating fraud entirely, which is unrealistic, but by ensuring security measures protect the booking without becoming the booking’s defining experience.

Airline Payment Systems: Why Distribution Modernisation Changes Payments Too

Airline payment systems are being reshaped by changes in how airlines sell, price, and manage offers. Modern airline retailing increasingly treats the booking as an order that can evolve over time rather than a static ticket.

That shift has direct payment implications. Payments must support partial fulfilment, re-pricing, reissues, and ancillaries added after purchase. Systems designed only for pay and issue struggle to support this flexibility. As airlines gain more control over offers through initiatives such as NDC, payments become part of the retail infrastructure rather than a downstream service. Merchants that modernise distribution without modernising payments create gaps that customers experience as confusion or delay.

Merchant Checklist: Signals Your Payment Flow Builds Customer Confidence

- Checkout pricing is fully transparent

Total amount, currency, and any conversion fees are visible before payment, with no surprises post-confirmation. - Authentication is applied selectively

Strong authentication is risk-based and context-aware, not triggered uniformly across all actions. - Refund handling is explicit and trackable

Customers are informed of refund eligibility, method, and realistic timelines, with visible status updates. - Post-booking changes have clear payment states

Fare changes and cancellations result in understandable payment outcomes that match what the customer sees. - Payment resilience is built in

Outing and failover mechanisms prevent isolated issuer or provider issues from breaking the experience.

Conclusion

In travel, customer confidence is shaped less by how quickly a payment is approved and more by how reliably it behaves when plans change. Bookings, ancillaries, reissues, and refunds all test whether the payment flow has been designed for real travel conditions rather than ideal ones.

In 2026, travel merchants improving confidence are those modernising payments as part of the full journey. By reducing friction at the right moments, maintaining transparency, and ensuring stability during disruption, they remove the uncertainty that drives complaints and disputes. Modern payment flows do not eliminate disruption, but they make outcomes predictable. When customers understand what will happen to their money, trust holds even when travel plans do not.

FAQs

1. Why do travel payments create more customer confidence issues than other industries?

Because travel payments extend beyond checkout. Bookings often involve changes, ancillaries, cancellations, and refunds, which introduce uncertainty long after the initial payment is approved.

2. What does modernising payment flows mean for travel merchants in 2026?

It means designing payments to support the full travel journey, not just checkout. This includes predictable handling of post-booking changes, transparent pricing, and clear refund outcomes.

3. Why do customers lose trust even when payments are successfully authorised?

Authorisation confirms a payment can proceed, but it does not reassure customers about what happens if plans change. Confidence erodes when refunds, changes, or additional charges feel unclear or inconsistent.

4. How do refunds influence chargeback rates in travel?

Many chargebacks are driven by uncertainty rather than fraud. When refund timelines or methods are unclear, customers often turn to their bank to regain control.

5. Why is Strong Customer Authentication a risk for conversion in travel?

When applied without context, authentication can signal unnecessary risk to customers. Poorly timed challenges increase abandonment, especially during high-value bookings or low-risk post-booking actions.

6. What makes cross-border travel payments more fragile?

Differences between the customer’s location, point of sale, and acquiring setup increase issuer caution. This leads to higher decline rates, authentication requests, and settlement delays.

7. How are airlines and OTAs improving payment reliability?

They are focusing on local acceptance, risk-based authentication, and payment orchestration that can reroute or recover transactions during disruption.

8. Why are false fraud declines such a problem in travel?

False positives block legitimate customers during considered purchases. Industry analysis has shown that these declines reduce revenue and damage trust more than fraud losses themselves.

9. How does distribution modernisation affect airline payments?

As airlines move toward order-based retailing models, payments must support ongoing changes, re-pricing, and ancillaries. Static pay and issue systems struggle to keep up.

10. What role do payment systems play during travel disruption?

They determine whether refunds, reissues, and adjustments are handled clearly and predictably. Well-designed payment flows maintain trust even when operations are under stress.

11. Can payment design really influence repeat bookings?

Yes. Customers are more likely to return when past payments behaved predictably, especially during refunds or cancellations. Confidence is built through experience, not messaging.

12. What is the biggest payment mistake travel merchants still make?

Treating payments as a one-time checkout event rather than a journey that continues through the entire travel lifecycle.