")

Chargebacks remain one of the most critical operational and financial threats to merchants. Each dispute not only reverses revenue but also incurs fees ranging from £15 to £100, damages credibility with acquirers, and consumes staff resources. For high-risk sectors such as iGaming, CBD, Forex, and subscriptions, sustained chargeback ratios can trigger account termination and complete loss of processing access.

The true cost extends far beyond the transaction value; merchants lose the product or service, the payment, and face additional penalties. Mastercard’s 2024 guidelines warn that exceeding chargeback thresholds leads to escalating fines and mandatory remediation programmes costing thousands.This guide outlines 15 actionable strategies to minimise chargebacks, safeguard revenue, and preserve strong relationships with payment providers. Each includes practical steps, effort and impact ratings, and supporting tools, providing a clear, structured framework for effective chargeback prevention in both mainstream and high-risk environments.

- Understanding Chargebacks: The Core Problem

- 15 Proven Ways to Reduce Chargebacks

- Quick Reference Table: Prioritising Your Chargeback Strategy

- Card Scheme Monitoring Programmes: What Merchants Must Know

- Technology and Tools for Chargeback Prevention

- Building a Long-Term Chargeback Management Strategy

- Conclusion

- FAQs

Chargebacks remain one of the most critical operational and financial threats to merchants. Each dispute not only reverses revenue but also incurs fees ranging from £15 to £100, damages credibility with acquirers, and consumes staff resources. For high-risk sectors such as iGaming, CBD, Forex, and subscriptions, sustained chargeback ratios can trigger account termination and complete loss of processing access.

The true cost extends far beyond the transaction value; merchants lose the product or service, the payment, and face additional penalties. Mastercard’s 2024 guidelines warn that exceeding chargeback thresholds leads to escalating fines and mandatory remediation programmes costing thousands.

This guide outlines 15 actionable strategies to minimise chargebacks, safeguard revenue, and preserve strong relationships with payment providers. Each includes practical steps, effort and impact ratings, and supporting tools, providing a clear, structured framework for effective chargeback prevention in both mainstream and high-risk environments.

Understanding Chargebacks: The Core Problem

What Is a Chargeback?

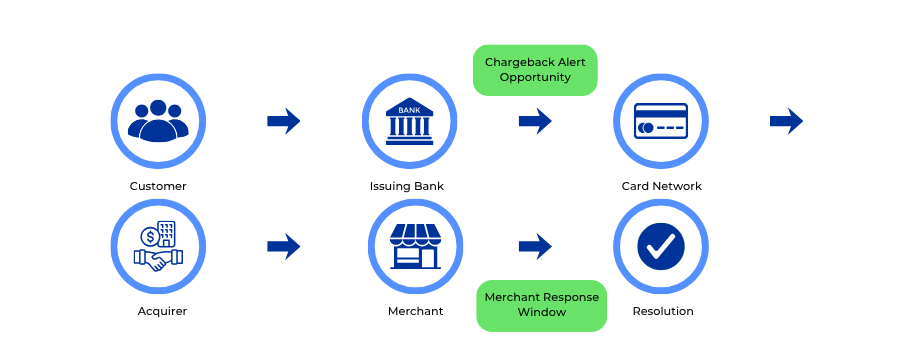

A chargeback occurs when a cardholder disputes a transaction with their issuing bank, triggering an involuntary reversal of funds from the merchant’s account to the customer. Unlike voluntary refunds, chargebacks are enforced through card network dispute systems (Visa, Mastercard, etc.).

The chargeback lifecycle follows a standard path: a customer disputes a charge, the issuing bank investigates and credits the customer, the acquiring bank debits the merchant, and a reason code is issued explaining the dispute. Merchants then have 7–21 days, depending on the network, to submit evidence defending the transaction through representation.

Why Chargebacks Happen

Chargebacks typically originate from four sources, each demanding targeted mitigation:

- Friendly Fraud (60-80%): Legitimate customers dispute valid charges, often after losing or forgetting the transaction.

- True Fraud: Criminal use of stolen cards, common in card-not-present transactions.

- Merchant Error: Incorrect billing descriptors, double charges, or fulfilment delays create legitimate disputes but are preventable through stronger operations.

- Product or Service Dissatisfaction: Customers who feel misled or disappointed often bypass refund requests and go directly to their banks.

The True Cost of Chargebacks

Every chargeback costs more than the transaction value. Direct losses include refunds and processor fees (£15-£100 per case). Indirect costs include staff time, investigation resources, unrecoverable products, shipping expenses, and elevated processing fees when ratios rise.

Exceeding network thresholds carries severe risk. Under Visa’s Dispute Monitoring Programme (VDMP), merchants surpassing a 0.9% chargeback ratio with over 100 monthly disputes are flagged for penalties and may face fines up to $50,000 or even termination of processing privileges. Mastercard’s ECMP enforces similar sanctions for persistent offenders.

Merchant Takeaway: Understanding the root causes of chargebacks is essential for designing preventive controls, maintaining compliance, and safeguarding long-term relationships with acquiring banks and payment service providers. Effective management protects not just revenue, but your business’s operational continuity.

15 Proven Ways to Reduce Chargebacks

1. Use Clear and Recognisable Billing Descriptors

One of the simplest yet most effective chargeback prevention tactics is ensuring customers recognise your billing descriptor on their statements. Confusing or generic identifiers like “XYZ Holdings 12345” often lead to unnecessary disputes. Instead, include your trading name, website, and customer service number, for example, “ACME Ltd 020-1234-5678 acme.co.uk.” Regularly test how the descriptor appears across banks and card networks, ensuring it matches the name customers see on your website and receipts.

Clear descriptors alone can reduce “unrecognised transaction” disputes by up to 25%, improving transparency and reinforcing trust before confusion escalates into a formal chargeback (Visa, 2024).

2. Implement Robust Fraud Prevention Tools

Fraudulent transactions are a major cause of chargebacks, especially for card-not-present merchants. Combining multiple fraud checks significantly reduces exposure. CVV and AVS verification confirm card authenticity and address accuracy (Mastercard, 2024), while Strong Customer Authentication (SCA) under PSD2 adds two-factor protection through 3D Secure 2.0 (European Banking Authority, 2023). Modern AI-driven systems such as Sift, Ravelin, or Riskified analyse device fingerprints, behavioural signals, and transaction velocity to block suspicious activity in real time.

3. Maintain Transparent Product Descriptions

Misleading or incomplete product details often trigger “item not as described” disputes. Customers who receive goods that differ from expectations may bypass support channels and go directly to their banks. Prevent this by providing accurate, detailed descriptions with high-resolution images, specifications, and realistic delivery times. Include usage instructions and compatibility notes where relevant. Transparent communication before purchase reduces post-delivery disappointment (Chargebacks911, 2024).

4. Provide Exceptional Customer Service

Inaccessible or slow customer support drives countless preventable chargebacks. When customers can’t reach a business or face poor communication, they contact their bank instead. Make support visible on every page, offer live chat or messaging, and respond promptly to complaints. Empowering staff to issue goodwill refunds is often cheaper than absorbing chargeback penalties. Fast, empathetic resolution builds loyalty and resolves issues before disputes reach an issuing bank (Ravelin Fraud Report, 2024).

5. Offer a Clear and Fair Refund Policy

A transparent refund policy gives customers a legitimate path for resolution, reducing reliance on chargebacks. The policy should outline return eligibility, timeframes, and processing steps, easily accessible from the website header, checkout, and confirmation emails. Overly restrictive refund terms frustrate buyers and push them toward disputes. According to Mastercard’s Chargeback Guidelines (2024), clear refund options reduce disputes and demonstrate fair merchant conduct.

6. Send Timely Order Confirmations and Shipping Updates

Lack of post-purchase communication often fuels “item not received” disputes. Automated order confirmations, tracking links, and proactive updates build customer confidence. When issues or delays arise, transparency prevents escalation. Merchants who implement proactive fulfilment communications reduce confusion-based chargebacks by 20–25% (Chargebacks911 Report, 2024).

7. Require Strong Customer Authentication (SCA)

Under PSD2, Strong Customer Authentication is mandatory for most electronic transactions and provides vital protection against fraud-related chargebacks. Implementing 3D Secure 2.0 ensures that once a transaction is authenticated, liability shifts from merchant to issuer (European Banking Authority, 2023). For online casinos and high-risk sectors, this not only ensures compliance but significantly reduces fraud exposure.

8. Keep Detailed Transaction Records

Comprehensive transaction documentation is critical for winning disputes. Maintain metadata such as IP addresses, timestamps, and delivery confirmation alongside customer communication logs. According to Mastercard’s Dispute Resolution Guide (2024), merchants should retain evidence for at least 18–24 months. Organised records enable faster representation, boosting win rates and deterring fraudulent claims.

9. Use AVS and CVV Verification

Address Verification Service (AVS) and Card Verification Value (CVV) are essential tools that verify cardholder identity and prevent unauthorised transactions. While not infallible, they significantly filter fraudulent activity when combined with other methods. Merchants failing to enforce AVS or CVV checks face higher fraud-related dispute ratios, according to Visa’s Chargeback Best Practices (2024).

10. Monitor and Respond to Chargeback Alerts

Chargeback alert services such as Visa Rapid Dispute Resolution (RDR) and Ethoca Alerts (Mastercard) notify merchants before disputes become official. Refunds within the alert window prevent chargeback registration, saving fees and protecting ratios. Visa notes that RDR participants prevent up to 40% of disputes pre-emptively (Visa, 2024).

11. Set Realistic Delivery Timeframes

Overpromising delivery times creates dissatisfaction that leads to chargebacks. Merchants should publish conservative, region-specific delivery estimates and notify customers proactively about delays. The European Payments Council (2025) recommends transparent fulfilment communication as a core trust factor in online commerce.

12. Verify High-Value or High-Risk Orders

High-ticket or suspicious transactions, especially those with mismatched billing and shipping data, should undergo manual review. Contacting customers directly validates legitimacy and deters fraudsters. This approach, combined with fraud scoring tools like Sift or Signifyd, can reduce fraudulent chargebacks by over 50% (Ravelin Fraud Trends, 2024).

13. Train Staff on Chargeback Prevention

Educating frontline teams about chargeback triggers and response protocols empowers them to resolve disputes early. According to Chargebacks911’s Merchant Education Index (2024), merchants with formal training programmes report up to 30% fewer chargebacks. Regular updates, KPI tracking, and recognition programmes reinforce a prevention-first culture.

14. Analyse Chargeback Data and Identify Patterns

Continuous chargeback data analysis reveals systemic issues. Tracking dispute reason codes, transaction origins, and product categories highlights vulnerabilities. Visa and Mastercard both recommend monthly analysis to maintain compliance and reduce exposure (Visa, 2024; Mastercard, 2024). Data-led improvement can reduce overall chargeback volumes by 20–40% within six months.

15. Partner with a Payment Provider That Supports Dispute Management

Selecting a PSP with robust chargeback tools and dedicated support can dramatically reduce risk. Providers like Adyen, Checkout.com, and high-risk specialists offer integrated alert systems, automated representation, and transparent reporting. The UK Payment Systems Regulator (2025) emphasises PSP accountability in helping merchants manage disputes effectively. For high-risk industries such as iGaming, CBD, and Forex, working with experienced providers ensures sustainable chargeback ratios and long-term processing stability.

Quick Reference Table: Prioritising Your Chargeback Strategy

| Strategy | Implementation Difficulty | Expected Impact | Time to Results |

| Clear billing descriptors | Easy | Medium-High | Immediate |

| Fraud prevention tools | Medium | High | 1-2 weeks |

| Transparent product descriptions | Easy | Medium | Immediate |

| Exceptional customer service | Medium | High | 2-4 weeks |

| Clear refund policy | Easy | Medium-High | Immediate |

| Order confirmations and updates | Easy | Medium | Immediate |

| Strong Customer Authentication | Medium | High | 1-2 weeks |

| Detailed transaction records | Medium | High | Ongoing |

| AVS and CVV verification | Easy | Medium-High | Immediate |

| Chargeback alert systems | Medium | Very High | 1 week |

| Realistic delivery timeframes | Easy | Medium | Immediate |

| High-value order verification | Medium | High | Immediate |

| Staff training | Medium | Medium-High | 4-8 weeks |

| Data analysis | Medium | High | Ongoing |

| Specialist PSP partnership | Hard | High | 4-12 weeks |

Card Scheme Monitoring Programmes: What Merchants Must Know

Visa Dispute Monitoring Programme (VDMP)

Visa’s VDMP identifies merchants with excessive chargeback ratios and imposes escalating interventions designed to force operational improvements. The programme operates across three tiers: Early Warning (0.65% ratio or 75 disputes monthly), Standard (0.9% ratio or 100 disputes monthly), and Excessive (1.8% ratio or 1,000 disputes monthly).

Merchants entering Standard monitoring face £50 monthly compliance case management fees plus £25 per additional chargeback. Excessive tier penalties increase dramatically, with fees reaching £100 per chargeback and potential processing termination.

According to Visa’s compliance framework, merchants must submit remediation plans demonstrating specific prevention measures and timeline for ratio reduction.

Mastercard Excessive Chargeback Merchant (ECMP) Programme

Mastercard’s ECMP operates similarly with slightly different thresholds: Standard programmes apply at 1.5% ratio with 100+ disputes monthly, whilst Excessive classification occurs at 3% ratio with 300+ monthly disputes. The Excessive Chargeback Program for Fraud (ECP-F) specifically addresses fraud-related chargebacks with lower 0.5% threshold.

Penalties include £25-£100 per chargeback depending on programme tier, monthly compliance review fees, and mandatory remediation plans. Mastercard provides 120-day performance improvement windows, though failure to achieve compliance results in processing termination.

Merchant Takeaway: Staying below card scheme thresholds requires continuous monitoring and proactive prevention. Once enrolled in monitoring programmes, exiting requires sustained compliance over multiple months, making prevention far easier than remediation.

Technology and Tools for Chargeback Prevention

Chargeback Alert Systems

Verifi and Ethoca alert systems notify merchants of pending disputes 24-72 hours before formal chargeback filing, creating intervention windows that prevent chargebacks from recording. Integration with payment systems enables automated refund issuance, though some merchants prefer manual review to verify refund justification before processing.

Return on investment calculations consistently favour alert participation: preventing a single £100 chargeback through £105 refund saves £15-£100 in chargeback fees, preserves chargeback ratio, and maintains better payment processor relationships. Alert coverage varies by issuing bank participation, typically reaching 30-60% of potential chargebacks depending on merchant industry and geography.

AI and Machine Learning for Fraud Detection

Modern fraud prevention platforms analyse hundreds of data points across device characteristics, browsing behaviour, transaction patterns, historical fraud indicators, and global fraud networks. Machine learning algorithms adapt to emerging fraud techniques whilst reducing false declines that damage legitimate customer conversion.

Advanced systems employ velocity checking to identify suspicious order patterns, device fingerprinting to track fraudsters across transactions, behavioural analysis comparing current sessions to historical patterns, and network effects learning from fraud attempts across all platform merchants. According to industry benchmarking, AI-driven fraud prevention reduces fraud losses 40-70% whilst improving customer experience through fewer false declines.

Order Insight and Consumer Clarity

Visa Order Insight and Mastercard Consumer Clarity programmes allow merchants to share transaction details directly with issuing banks during customer dispute inquiries. When cardholders contact banks questioning charges, issuers access merchant-provided information including logos, product descriptions, delivery status, and contact details.

This real-time data sharing resolves customer confusion before formal disputes initiate, reducing friendly fraud chargebacks by 20-30% for participating merchants. Implementation requires integration with chargeback management platforms that connect to card scheme APIs and populate transaction details automatically.

Merchant Takeaway: Technology investment delivers measurable returns through reduced chargeback fees, preserved merchant accounts, and operational efficiency gains. Comprehensive prevention platforms cost less than manual processes whilst providing superior protection.

Building a Long-Term Chargeback Management Strategy

Establish a Dedicated Dispute Response Team

As transaction volumes grow, ad-hoc chargeback handling becomes insufficient. Designating specific staff responsible for dispute monitoring, representment, and prevention ensures consistent attention to chargeback management. Team responsibilities should include daily chargeback monitoring, evidence compilation and representation submission, alert system management and refund processing, data analysis and trend reporting, and cross-functional collaboration with customer service, operations, and fraud prevention teams.

Clear workflows documenting each step from chargeback receipt through resolution create consistency and ensure compliance with tight response deadlines. Standard operating procedures should specify evidence requirements for common reason codes, approval processes for representation decisions, and escalation protocols for complex situations.

Continuous Improvement Through Data Analysis

Monthly chargeback review meetings examining trends, reason codes, affected products, and prevention effectiveness drive continuous improvement. Comparing month-over-month performance identifies whether implemented strategies deliver expected results, whilst benchmarking against industry averages provides context for performance assessment.

A/B testing policy changes, such as extended refund windows, revised shipping options, or modified customer communications, enables data-driven decision making about operational adjustments. Collaboration between payments, customer service, and operations teams ensures chargeback insights inform broader business decisions affecting dispute risk.

Stay Updated on Regulatory and Scheme Rule Changes

Payment industry regulations and card scheme rules evolve continuously, requiring ongoing monitoring to maintain compliance. The Financial Conduct Authority regularly updates payment services guidance, PSD2 technical standards undergo periodic revision, and Visa and Mastercard publish quarterly rule updates affecting dispute procedures, liability frameworks, and merchant requirements.

Subscribe to card scheme merchant newsletters, monitor regulatory announcements from UK and European authorities, and participate in payment industry associations providing compliance updates. Payment Mentors offers specialised guidance helping high-risk merchants navigate complex regulatory requirements whilst maintaining operational flexibility.

Merchant Takeaway: Chargeback management requires sustained organisational commitment rather than one-time intervention. Building prevention into business operations, empowering teams with appropriate tools and training, and continuously refining strategies based on performance data creates long-term resilience against dispute-related losses.

Conclusion

Chargebacks represent significant financial and operational challenges, but they remain largely preventable through strategic combinations of technology, transparency, and customer-focused practices. The 15 strategies outlined in this guide provide immediate and long-term impact when implemented systematically.

Begin with quick-win strategies offering easy implementation and immediate results: update billing descriptors, enable CVV and AVS verification, and enrol in chargeback alert systems. These foundational improvements typically reduce chargebacks 20-30% within the first month.

Progress to medium-difficulty implementations including fraud prevention platform deployment, staff training programmes, and data analysis workflows. These initiatives require greater investment but deliver substantial returns through comprehensive protection and continuous improvement capabilities.

For merchants operating in high-risk sectors or facing persistent chargeback challenges, specialist payment service provider partnerships and advanced technology platforms provide sophisticated tools and expertise supporting compliance with card scheme monitoring programmes whilst maintaining payment processing continuity.

Payment Mentors specialises in helping high-risk merchants build compliant, fraud-resilient payment ecosystems that balance regulatory requirements with commercial performance. Our consultancy services provide tailored guidance addressing the unique chargeback challenges facing businesses in iGaming, CBD, Forex, adult services, and subscription models.

Review your current chargeback processes against the strategies outlined above, identify immediate implementation opportunities, and develop a phased roadmap for comprehensive prevention infrastructure. The investment in chargeback reduction delivers direct returns through reduced fees, preserved merchant accounts, and protected customer relationships that support sustainable growth.

FAQs

1. What are the most common reasons merchants get chargebacks?

Chargebacks usually stem from four sources, friendly fraud (customers disputing valid payments), true fraud (stolen cards or unauthorised use), merchant error (incorrect billing or delays), and product dissatisfaction. Understanding which type dominates your disputes is key to applying the right prevention tactics, from improving product transparency to deploying real-time fraud detection tools.

2. How can merchants reduce chargebacks quickly?

Start with three quick wins:

- Use clear billing descriptors customers recognise.

- Enable CVV and AVS verification on every transaction.

- Enrol in chargeback alert programmes such as Visa RDR or Ethoca.

These low-effort steps can reduce preventable chargebacks by 20-30% within one month.

3. What tools help prevent chargebacks before they occur?

Modern PSPs integrate layered fraud tools including 3D Secure 2.0 (SCA), AI-driven behavioural analysis, and device fingerprinting. Platforms like Sift, Riskified, and Ravelin analyse transaction patterns and block suspicious payments before they trigger disputes, an essential safeguard for high-risk sectors like iGaming, Forex, and CBD.

4. What’s the difference between a refund and a chargeback?

A refund is initiated voluntarily by the merchant as part of customer service. A chargeback, however, is forced by the issuing bank when a cardholder disputes the charge. Refunds protect your ratios; chargebacks harm them and incur fees, penalties, and risk of being placed under Visa VDMP or Mastercard ECMP monitoring programmes.

5. What is a “good” chargeback ratio for merchants?

To stay compliant, merchants should maintain ratios below 0.9% (Visa) and 1.5% (Mastercard). Exceeding these thresholds can trigger fines, remediation plans, or even loss of processing privileges. Regular ratio tracking via your PSP dashboard helps you stay within safe operating limits.

6. How does Strong Customer Authentication (SCA) help reduce chargebacks?

Under the PSD2 regulation, SCA requires two-factor verification for online transactions.

When 3D Secure 2.0 is successfully applied, liability shifts from the merchant to the issuer, meaning the merchant is no longer responsible for fraud-related chargebacks.

This makes SCA both a compliance and risk-reduction advantage.

7. How can customer service impact chargeback levels?

Many disputes begin as unresolved customer complaints. Providing fast, visible, and empathetic support, via live chat, email, or phone, prevents customers from escalating to their banks. Payment Mentors’ research shows responsive service can lower chargebacks by up to 25%, particularly in subscription and high-risk retail models.

8. What’s the role of chargeback alert systems like Ethoca and Verifi?

Ethoca Alerts (Mastercard) and Verifi Rapid Dispute Resolution (Visa) notify merchants 24-72 hours before an official dispute is filed. By issuing a voluntary refund within that window, merchants can prevent the chargeback from registering, preserving both revenue and chargeback ratios.

9. How can data analysis help reduce chargebacks long term?

Analysing reason codes, product categories, and customer behaviour helps identify recurring triggers. Patterns such as “item not received” or “unrecognised descriptor” highlight where operational or communication improvements are needed. Data-led decisions typically reduce chargeback volumes by 20-40% within six months.

10. Why should merchants partner with specialist PSPs for chargeback management?

High-risk merchants (iGaming, CBD, Forex, Adult, Subscription models) need PSPs with dedicated dispute management tools, automated representation, and expert support teams. Specialist providers like Checkout.com, Adyen, or Payment Mentors’ partner PSPs offer integrated alerts, data feeds, and compliance-ready monitoring, ensuring sustainable chargeback ratios and uninterrupted processing access.