Latin America’s online payments market is projected to exceed $300 billion by 2026, and high-risk verticals including iGaming, adult, forex and subscription services are among the fastest-growing segments driving that number. Digital adoption is accelerating, smartphone penetration is high, and a payment-native population is spending online at rates outpacing most other regions.

The most common mistake high-risk merchants make is assuming Brazil’s playbook transfers directly to Mexico, Colombia, Argentina or Peru. PIX proved what is possible in Brazil, but each market has its own rails, wallet ecosystem, regulatory environment and fraud profile. This article is a practical 2026 guide covering the right rails, wallets and operational approach for high-risk merchants operating across LATAM beyond Brazil.

- Why PIX Changed Everything And What It Means Beyond Brazil

- Mexico – SPEI, CoDi and the Local Acquiring Imperative

- Colombia – Bre-B, Nequi and a Fast-Maturing Digital Market

- Peru and Argentina – Local Wallets, FX Complexity and What Merchants Must Know

- Instant Payouts – The Operational Challenge High-Risk Merchants Underestimate

- Fraud in LATAM’s Instant Payment Environment

- Building a High-Risk Payment Stack Across LATAM – The 2026 Approach

- Conclusion

- FAQ

Why PIX Changed Everything And What It Means Beyond Brazil

What PIX Actually Delivered for High-Risk Merchants in Brazil

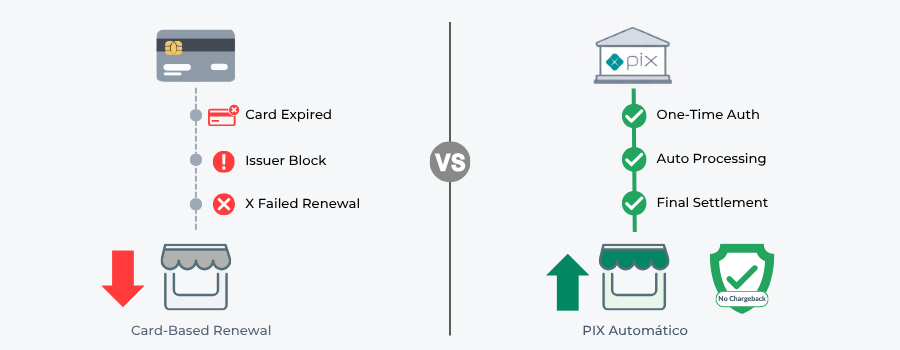

PIX’s impact on high-risk merchants goes well beyond lower processing costs. PIX transactions carry no chargeback risk; once settled, payment is final. For verticals like adult, iGaming and high-value subscription services, this removes an entire category of revenue leakage embedded in the card model.

For merchants fighting elevated card decline rates, PIX removes most authentication friction by moving it to the bank level before funds move, bypassing issuer, network and acquirer risk checkpoints simultaneously.

PIX Automático, launched in June 2025, changed subscription economics further still. Before its introduction, monthly churn from failed card renewals in high-risk subscription categories ran at 15–25%.

PIX Automático allows users to authorise recurring payments once through their bank, with payments processing automatically on scheduled dates. Renewal rates moved closer to what low-risk card categories achieve in mature markets.

Brazil’s iGaming regulation, Law 14.790/2023, made PIX mandatory for licensed operators from January 2026. Credit cards are explicitly banned for betting deposits, and payments must originate from accounts registered to the player’s verified CPF. Every PIX key must be verified against the depositor’s CPF before funds are credited. PIX is now the primary deposit and payout rail for regulated iGaming in Brazil, and operating without a compliant integration is not viable.

PIX’s Regional Spread and What It Signals

Colombia launched Bre-B in October 2025, modelled directly on PIX’s architecture: QR code payments, identification via keys, mandatory interoperability and 24/7 settlement. Brazil expanded PIX into Argentina in March 2026. The instant payment model PIX validated is becoming the regional standard.

However, each implementation has materially different feature sets and compliance frameworks. Bre-B currently handles P2P and P2M only, with recurring payments and bulk payouts still in the pipeline. That single gap changes the operational reality for subscription businesses and iGaming operators compared to what Brazil offers today. The direction is consistent across the region, but operational readiness varies significantly by market.

Mexico – SPEI, CoDi and the Local Acquiring Imperative

Mexico is the second largest digital commerce market in LATAM and one where high-risk merchants consistently underperform by arriving with an offshore card-only approach. SPEI is Mexico’s foundational instant payment system, settling transactions in seconds around the clock with full traceability through the Electronic Payment Receipt system. CoDi sits on top of SPEI enabling QR-based collections. Mexico’s real-time payments market is growing at 31.4% compound annually, with near-zero merchant fees compared to the 2–3% interchange cost of card processing.

For high-risk merchants, SPEI transactions are irrevocable once completed, creating the same dispute gap present across A2A rails: no card scheme framework, no standardised chargeback process and no defined resolution timeline. The adult industry alone is estimated to lose 45% of its LATAM sales by not offering local payment methods, and Mexico is a major contributor to that figure.

Local acquiring is non-negotiable. Local cards processed through local acquirers achieve approval rates of 60–80% in Mexico. Offshore processing typically achieves 20–45% on the same transactions. Mexican banks apply stricter controls to gambling, forex and recurring billing, and cross-border card payments frequently trigger enhanced fraud screening.

Chargeback rates in Mexico can reach 3–6%, roughly triple the global average, and regional PSPs with localised anti-fraud systems are significantly better equipped to manage that exposure than generic international tooling.

Colombia – Bre-B, Nequi and a Fast-Maturing Digital Market

Bre-B and Its Current Limitations for High-Risk Merchants

Bre-B launched at full national scale in October 2025, incorporating lessons from five years of PIX’s operational experience. Colombia’s digital economy surpassed USD 52 billion in 2025 and is projected to reach USD 73 billion by 2028 as Bre-B accelerates digital commerce adoption.

The critical operational reality for high-risk merchants is what Bre-B does not yet support. Recurring payments and bulk payouts are in the pipeline but not yet live. For iGaming operators running player withdrawals, adult platforms running subscription renewals or forex brokers running affiliate payouts, this is a meaningful gap. PSE remains the primary route for ecommerce transaction traceability in the interim, requiring strong identifier management to avoid manual reconciliation complexity.

The Wallet Layer and Colombia’s High-Risk Opportunity

Colombia’s wallet adoption is one of the most striking stories in LATAM payments. Digital wallet ownership has grown from 27 million active users in 2021 to approximately 55 million, with Nequi and DaviPlata dominating alongside Nubank. PSE accounts for 32% of all Colombian ecommerce transactions. For high-risk merchants, wallet acceptance is not an enhancement to a working payment stack; it is a prerequisite for building one.

Peru and Argentina – Local Wallets, FX Complexity and What Merchants Must Know

Peru demonstrates how central bank-mandated interoperability can transform a digital payments market quickly. Yape and PLIN each have around 14 million users, and when Peru’s Central Reserve Bank mandated interoperability in April 2023, daily cross-app transactions surged to 1.6 million transfers almost immediately. Yape processes six times more transactions than PLIN by volume and is expanding into B2B merchant acceptance through Yape Empresas. For high-risk merchants entering Peru, QR acceptance and integration with both wallets are standard consumer expectations, not differentiators.

Argentina requires a specifically calibrated approach. Mercado Pago QR codes are standard across retail and ecommerce, and offering interest-free instalments alongside QR wallet payments is often decisive for conversion. FX volatility, regulatory changes around currency controls and higher rates of issuer rejection on international card transactions mean that high-risk merchants need local payment partners with genuine Argentina expertise. The regulatory and competitive tension between Mercado Pago and the bank-backed MODO wallet adds further uncertainty that merchants operating in this market need to monitor actively.

Instant Payouts – The Operational Challenge High-Risk Merchants Underestimate

Pay-in infrastructure has matured significantly across LATAM. Payout infrastructure is a different story, and high-risk merchants with recurring payout obligations discover this quickly. iGaming operators, adult platforms, forex brokers and affiliate-heavy businesses all face the same fragmented reality: banking infrastructure differs significantly across countries, regulatory frameworks governing outbound payments are country-specific, and processing speeds range from near-real-time to batch processing with limited operating hours.

Data quality is the most immediate operational risk. A failed payout caused by a CPF mismatch in Brazil, an incorrect CLABE in Mexico or an incomplete national ID reference in Colombia are not edge cases; they are routine occurrences for merchants who have not built payout data validation into their workflows. Each failure generates customer support load, reconciliation work and in some cases compliance flags that delay resolution further.

The core payout risks high-risk merchants must plan around across LATAM include:

- Data quality failures: incorrect local identifiers causing failed transfers and manual intervention.

- Settlement fragmentation: different timing, batch limitations and operating hours creating reconciliation complexity.

- KYC on payout recipients: varying requirements by country increasing compliance overhead on outbound flows.

- AML monitoring obligations: outbound transactions requiring jurisdiction-specific thresholds and reporting that differ materially across markets.

Fraud in LATAM’s Instant Payment Environment

Why Instant and Irreversible Is a Double-Edged Sword

Instant payments now drive 60% of consumer spending in LATAM, and the fraud environment has adapted accordingly. The speed that makes PIX, SPEI and Bre-B attractive also makes fraud harder to prevent and impossible to reverse. APP scams and social engineering are rising alongside instant payment adoption. In high-risk verticals, friendly fraud in subscription services, promotional abuse in iGaming and trading, and account sharing and identity reuse are all elevated typologies.

Brazil’s Central Bank introduced mandatory security rules for PIX device registrations including per-transaction and daily limits for unregistered devices. Colombia built time-based transaction limits into Bre-B from day one. These controls operate at the infrastructure level; the fraud management burden above that level falls directly on merchants and their PSP partners.

What a LATAM-Specific Fraud Stack Looks Like

Generic fraud tools fail in LATAM because they lack local behavioural context. International scoring models trained on European or North American data consistently either block too many legitimate transactions or approve too much fraud. Neither outcome is workable for high-risk merchants in markets where margins are already compressed.

A LATAM-specific fraud stack needs CPF and local ID verification at checkout, device fingerprinting calibrated to local user patterns, local fraud scoring built on regional transaction data, and multi-acquirer routing that reduces concentration risk by market and corridor. Because instant payments are irreversible, every element must operate in real time. Batch-based monitoring is structurally inadequate in an environment where funds disperse across institutions within seconds.

Building a High-Risk Payment Stack Across LATAM – The 2026 Approach

Pillar 1 – Local Acquiring as the Foundation

Local acquiring is the single most impactful lever for high-risk merchants in LATAM. The approval rate difference is not marginal: local cards through local acquirers achieve 60–80% authorisation rates versus 20–45% through offshore processing. Local acquirers understand issuer behaviour, domestic fraud patterns and regulatory expectations in ways that global processors cannot replicate remotely. For high-risk MCCs, they are also better positioned to maintain processing relationships when scheme or regulatory scrutiny increases.

Pillar 2 – Market-Specific Rail and Wallet Mix

A single payment integration across all LATAM markets will consistently underperform against a market-specific build. In Brazil, PIX and PIX Automático are essential. In Mexico, SPEI and CoDi sit alongside cards. In Colombia, Bre-B combined with Nequi, DaviPlata and PSE defines the current payment foundation. In Peru, Yape and PLIN are standard consumer expectations. In Argentina, Mercado Pago and instalment culture shape conversion more than any other factor. High-risk merchants who build the right mix for each market outperform those who apply a uniform regional approach consistently and measurably.

Pillar 3 – Compliance Built Per Jurisdiction, Not Copied Across

Compliance in LATAM is a collection of jurisdiction-specific obligations, not a single regional framework. Brazil bans credit cards for iGaming and requires CPF matching on every PIX transaction. Colombia’s Bre-B compliance framework is still maturing. Argentina’s FX controls can change with limited notice. High-risk merchants need PSP partners with genuine local regulatory depth in each market. The consequence of getting compliance wrong is not just a fine; it is the loss of processing access, frozen settlement funds or a terminated local banking relationship that may take months to rebuild.

Conclusion

LATAM is one of the highest-growth opportunities for high-risk merchants globally in 2026, with non-cash transaction volumes projected to grow at more than 20% compound annually through 2028. The infrastructure improvements across the region are making that opportunity more accessible than ever, and the PIX model has shown what is possible when instant, interoperable payment infrastructure operates at national scale.

The merchants who will unlock LATAM beyond Brazil are those who go deep in each market: local acquiring relationships, market-specific rail and wallet integrations, real-time fraud controls calibrated to local behaviour, and compliance built per jurisdiction. Breadth without operational depth consistently underperforms in this region. Depth in each market, built systematically, is what turns LATAM’s growth trajectory into sustainable revenue.

FAQ

1. Why is LATAM considered a high-risk merchant battleground in 2026?

Because high-risk verticals including iGaming, adult, forex and subscription services are among the fastest-growing segments in a market projected to exceed $300 billion, but fragmented regulations, conservative issuer risk models, FX volatility and country-specific payment preferences make it structurally complex to operate across the region.

2. Can high-risk merchants use the same Brazil payment playbook in other LATAM markets?

No. Brazil’s PIX-dominated environment is unique. Each market has its own instant payment rails, wallet ecosystem, regulatory framework and fraud profile. Applying Brazil’s approach directly to Mexico, Colombia, Argentina or Peru consistently underperforms against a market-specific strategy.

3. What specific advantages does PIX offer high-risk merchants that cards do not?

PIX transactions carry no chargeback risk and are final once settled, removing a major source of revenue leakage for fraud-prone categories. PIX Automático also resolved the subscription renewal problem by allowing recurring authorisations at the bank level, reducing monthly churn from failed payments from 15–25% down to rates closer to low-risk card categories.

4. How did Brazil’s iGaming regulation change PIX’s role for operators in 2026?

Law 14.790/2023 explicitly banned credit cards for betting deposits from January 2026, making PIX the mandatory deposit and payout rail for licensed iGaming operators. Every PIX payment must be verified against the depositor’s CPF before funds are credited, and third-party deposits are strictly prohibited.

5. What is Bre-B and why does it matter for high-risk merchants in Colombia?

Bre-B is Colombia’s instant payment system, launched at full national scale in October 2025 and modelled directly on PIX. It offers QR code payments, key-based identification, mandatory interoperability and 24/7 settlement. However, recurring payments and bulk payouts are not yet live, which is a meaningful operational gap for subscription businesses and iGaming operators.

6. Why is local acquiring so important for high-risk merchants in Mexico?

Because local cards processed through local acquirers achieve approval rates of 60–80% in Mexico, while offshore processing typically achieves only 20–45% on the same transactions. Mexican banks apply stricter controls to gambling, forex and recurring billing, and chargeback rates can reach 3–6%, making local acquirers with region-specific fraud tooling essential for sustainable processing.

7. Which digital wallets should high-risk merchants prioritise in Colombia and Peru?

In Colombia, Nequi and DaviPlata are dominant alongside Nubank, with PSE accounting for 32% of all ecommerce transactions. In Peru, Yape and PLIN are the standard consumer expectation, each with around 14 million users and central bank-mandated interoperability enabling seamless cross-app transfers between them.

8. What makes Argentina particularly challenging for high-risk payment processing?

FX volatility, currency controls, higher rates of issuer rejection on international card transactions and the competitive tension between Mercado Pago and bank-backed MODO all add complexity unique to Argentina. Offering interest-free instalments alongside Mercado Pago QR payments is often decisive for conversion, and local payment expertise is essential rather than optional.

9. Why are instant payouts harder than pay-ins for high-risk merchants in LATAM?

Because payout infrastructure is less mature than pay-in rails across the region. Settlement timing, batch processing limitations, KYC requirements on payout recipients and AML reporting obligations all differ by jurisdiction. Data quality failures such as incorrect CLABE numbers in Mexico or CPF mismatches in Brazil are routine causes of failed transfers that generate support load and reconciliation complexity.

10. How does the fraud environment in LATAM differ from other regions for high-risk merchants?

Instant payments are irreversible, so fraud must be prevented before funds move rather than detected after. APP scams, social engineering, friendly fraud in subscriptions and promotional abuse in iGaming are all elevated typologies. Generic international fraud models fail because they lack local behavioural context, making LATAM-specific fraud scoring, local ID verification and real-time controls essential.

11. What does a LATAM-specific fraud stack need to include for high-risk merchants?

CPF and local national ID verification at checkout, device fingerprinting calibrated to local user patterns, fraud scoring built on regional transaction data and known vertical typologies, and multi-acquirer routing that reduces fraud concentration by market and corridor. All controls must operate in real time because batch-based monitoring is structurally inadequate when payments settle in seconds.

12. What is the single most important principle for high-risk merchants building a LATAM payment stack?

Depth over breadth. Local acquiring relationships, market-specific rail and wallet integrations, real-time fraud controls and jurisdiction-specific compliance all require genuine investment in each market. Merchants who apply a uniform regional approach consistently underperform those who build the right operational depth in each individual market.