Payments now sit at the centre of how many businesses operate, even if they are not always recognised as such. Approval performance, cost, fraud exposure, cash timing, and customer experience are increasingly shaped by payment decisions that cut across teams and systems. What was once treated as a technical layer has become a source of business outcomes that are difficult to separate from core performance.

This change has been gradual, but its effects are now hard to ignore. As payment environments have fragmented and expectations around reliability and control have increased, the impact of small decisions has grown. Choices made in one area of the payment flow can influence risk posture, working capital, and customer behaviour elsewhere. Payments may still function, but without coordination, those functions can quietly work against broader business objectives.

By 2026, this has pushed many organisations to rethink how payments are managed. Rather than being set up and left to run, payments increasingly require ongoing decision-making, clear ownership, and deliberate trade-offs. This is the point at which payments stop behaving like a supporting function and begin to resemble a core business capability, one that shapes how effectively a company can operate, scale, and adapt.

- Why Payments Decisions Now Shape Core Business Outcomes

- From Integration Choice to Operating Capability

- Why Measurement Has Become Strategic

- Payments Strategy as a Resilience Function

- How Payments Strategy Changes Market Expansion

- Why This Shift Is Accelerating in 2026

- What Happens When Payments Strategy Is Missing

- Conclusion

- FAQs

Why Payments Decisions Now Shape Core Business Outcomes

For a long time, payment performance was judged narrowly. If transactions were authorised, funds settled, and obvious fraud was contained, payments were considered to be doing their job. That framing no longer holds. Today, the outcomes of payment decisions are tightly interwoven with revenue stability, risk exposure, cash flow predictability, and customer experience.

This is partly because payment components no longer operate in isolation. Approval rates influence customer behaviour and conversion. Fraud controls affect issuer confidence and dispute volumes. Settlement timing shapes working capital and forecasting accuracy. When these elements are managed independently, small optimisations in one area can create unintended consequences elsewhere.

What has changed is the scale of these second-order effects. As businesses grow across markets, channels, and payment methods, decisions that once felt local begin to compound. A retry strategy designed to recover declines can increase issuer caution. An aggressive cost optimisation can introduce reconciliation friction. Each choice has a wider footprint than before.

As a result, payments decisions now shape core business outcomes whether or not they are treated strategically. When they are left unmanaged, misalignment accumulates quietly. When they are approached deliberately, payments become a lever that supports stability rather than undermining it.

From Integration Choice to Operating Capability

There was a time when payments could reasonably be treated as a setup decision. A business selected a primary provider, integrated a small number of methods, and expected the system to behave predictably. Variation was limited, and when issues arose, they were usually contained within the payments function itself.

That model no longer holds. Payment environments are now defined by multiple rails, regional differences, and overlapping outcomes. The same transaction can be influenced by authentication rules, issuer behaviour, risk controls, and settlement mechanics, all interacting at once. As this complexity has increased, the consequences of payment decisions have spread beyond the boundaries of any single team.

What this changes is the nature of ownership. Payments can no longer be configured and left alone. They require ongoing choices about trade-offs: between approval and risk, cost and resilience, optimisation and consistency. These are not one-off decisions made at integration time, but continuous judgements that affect how the business performs over time.

This is where payments begin to resemble an operating capability rather than an integration. An operating capability implies defined ownership, shared context, and the ability to interpret outcomes across functions. It recognises that payment behaviour evolves, and that maintaining alignment requires coordination rather than configuration. By 2026, this shift has become unavoidable for organisations operating at scale.

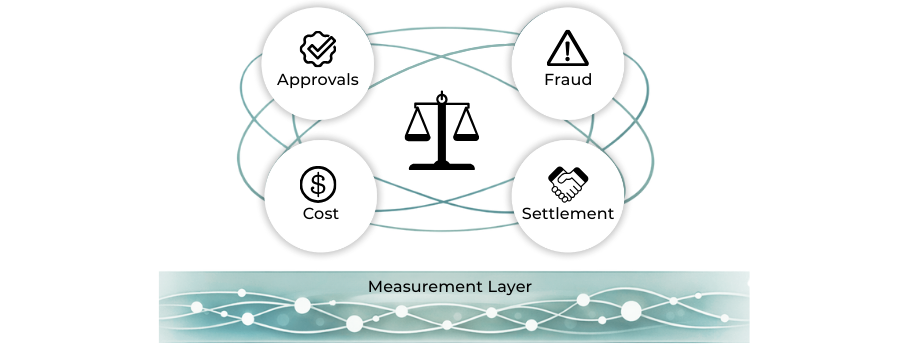

Why Measurement Has Become Strategic

As payments have become more central to business performance, the limits of traditional measurement have become more visible. Many organisations still track payment metrics in isolation, with different teams owning different numbers. Each metric may look acceptable on its own, while overall performance quietly degrades.

By 2026, this fragmented view is no longer sufficient. The value of measurement now lies less in monitoring individual outcomes and more in interpreting how those outcomes interact. Approval gains that coincide with rising dispute rates, or cost reductions that introduce settlement and reconciliation delays, are no longer secondary effects. They are signals that the system is out of balance.

Strategic measurement brings these signals together. It allows organisations to see payments as a connected set of outcomes rather than a collection of independent metrics. This shift is what enables informed trade-offs instead of reactive fixes.

In practice, the difference between operational and strategic measurement often looks like this:

- Approvals, fraud, cost, and settlement viewed together rather than owned in isolation

- Changes assessed over time, not just against short-term targets

- Performance interpreted in context, not explained away by single metrics

When measurement works at this level, it becomes a decision-making tool rather than a reporting exercise. It helps organisations identify where performance is drifting before problems become visible to customers or counterparties. This is also how silent degradation is avoided. Without joined-up measurement, payments can appear healthy while slowly eroding trust, margin, or resilience elsewhere in the business.

Payments Strategy as a Resilience Function

As payment environments become more complex, resilience has taken on a different meaning. It is no longer just about uptime or redundancy, but about the ability of payment operations to absorb change without destabilising outcomes. New rails, evolving liability expectations, market expansion, and shifting risk patterns all introduce variation that must be managed continuously rather than absorbed once.

Without strategy, this variation accumulates quietly. Local fixes are applied to address immediate issues, but their wider impact is rarely assessed. Over time, payment behaviour becomes harder to interpret, and small changes carry disproportionate risk. What appears resilient on the surface often relies on manual intervention and institutional knowledge rather than structural strength.

Payments strategy provides the counterweight to this fragility. By defining how decisions are made, how outcomes are evaluated, and where consistency matters most, strategy allows payment operations to adapt without drifting. Resilience, in this sense, is not about preventing change, but about ensuring that change does not erode trust, predictability, or control as the system evolves.

How Payments Strategy Changes Market Expansion

Market expansion used to be framed as an execution challenge. New regions were enabled by adding local payment methods, integrating additional providers, and meeting market-specific requirements. While those steps remain necessary, they are no longer sufficient on their own. As businesses expand across more markets, the cumulative impact of payment decisions becomes harder to manage without a strategic layer.

Without strategy, expansion tends to increase fragmentation. Each market develops its own payment logic, optimised for local performance but disconnected from the rest of the organisation. Over time, this creates operational drag. Reporting becomes inconsistent, settlement behaviour diverges, and teams spend more time reconciling differences than improving performance.

When a payments strategy is treated as a core capability, expansion looks different. Instead of rebuilding decisions market by market, organisations establish repeatable principles around approval handling, risk tolerance, and measurement. Local variation is expected, but it is introduced within a shared framework that keeps outcomes comparable and behaviour interpretable.

This shift reduces the cost of growth. Expansion no longer requires reinventing payment operations each time a new market is added. Strategy provides continuity, allowing businesses to scale payment activity while preserving coherence across regions. In 2026, that repeatability has become a competitive advantage in its own right.

Why This Shift Is Accelerating in 2026

The move towards payments strategy as a core capability has been building for some time, but by 2026 it has become harder to defer. Payment environments are more fragmented, outcomes are more contested, and the margin for ambiguity has narrowed. Decisions that once sat comfortably within specialist teams now have implications that senior leaders expect to understand and influence.

At the same time, expectations around predictability have increased. Businesses are under greater pressure to explain why payments perform the way they do, how risk is being managed, and how cash moves through the organisation. When answers rely on local context or informal knowledge, confidence erodes. Strategy emerges as the mechanism that restores clarity by linking decisions to outcomes in a way that can be communicated and defended.

There is also a practical driver. As complexity grows, the cost of operating without strategy rises. More time is spent reconciling inconsistencies, responding to unexpected side effects, and managing exceptions that were never designed into the system. By 2026, many organisations recognise that treating payments strategically is not about ambition, but about keeping operations intelligible as scale and variation increase.

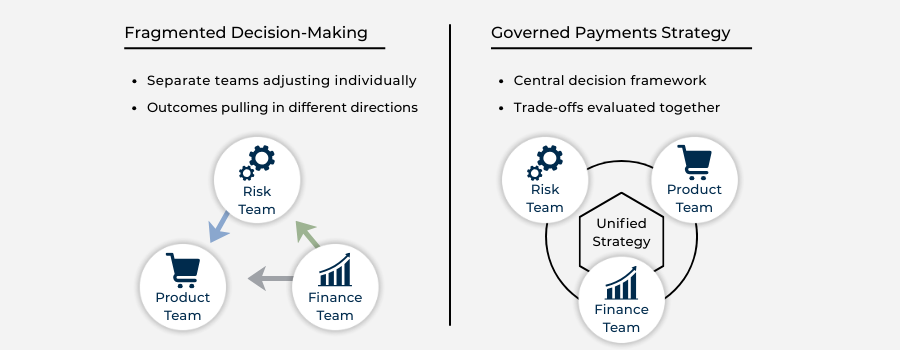

What Happens When Payments Strategy Is Missing

When payments are managed without a strategic layer, problems rarely appear all at once. Instead, friction accumulates quietly as decisions are made in isolation and optimisations pull the system in different directions. Payments may continue to function, but their behaviour becomes harder to understand and more expensive to manage over time.

In these environments, teams often respond to symptoms rather than causes. Declines trigger retries, fraud spikes trigger tighter controls, and cost pressure leads to routing changes, each addressing an immediate concern while introducing new side effects elsewhere. Without a shared framework for decision-making, these adjustments compound rather than resolve underlying misalignment.

The consequences tend to follow a familiar pattern:

Conflicting optimisation goals across payments, risk, finance, and operations

Reactive controls replacing deliberate trade-offs and long-term intent

Inconsistent behaviour across markets that erodes comparability and trust

Increasing manual effort to interpret outcomes that systems no longer explain clearly

Over time, payments shift from being a source of leverage to a source of drag. The absence of strategy does not stop growth, but it makes growth harder to sustain. By the time issues become visible at a senior level, complexity has usually become embedded, making recovery slower and more costly than it needed to be.

Conclusion

By 2026, payments strategy has moved beyond optimisation and enablement. It has become a core business capability because payment decisions now shape outcomes that matter across revenue, risk, cash flow, and customer experience. As complexity increases, the way those decisions are governed and interpreted matters as much as the technology that executes them.

Treating payments strategically allows organisations to replace reactive adjustment with deliberate control. It creates shared context across teams, makes trade-offs explicit, and prevents misalignment from accumulating quietly. Payments remain complex, but that complexity becomes manageable rather than destabilising.

This shift is unlikely to reverse. As payment environments continue to fragment and expectations around predictability rise, strategy becomes the mechanism that keeps operations intelligible at scale. Businesses that recognise this early are better positioned to compete not by moving faster, but by sustaining clarity as their payment operations evolve.

FAQs

1. What does it mean to treat payments as a core business capability?

It means recognising that payment decisions shape revenue stability, risk exposure, cash flow, and customer experience, and therefore require ongoing ownership, governance, and coordination rather than one-off setup.

2. Why is payments strategy becoming more important in 2026 specifically?

Because payment environments have become more fragmented and interdependent, making unmanaged decisions harder to contain and easier to compound into wider business issues.

3. How is payments strategy different from payments optimisation?

Optimisation focuses on improving individual metrics. Strategy focuses on managing trade-offs between competing outcomes and maintaining alignment as complexity increases.

4. Why can’t payments still be treated as a technical or operational function?

Because payment behaviour now affects multiple parts of the business simultaneously. Decisions made in isolation can undermine broader objectives even if systems appear to be functioning.

5. What kinds of decisions fall under payments strategy?

Decisions about prioritising approvals versus risk, managing cost versus resilience, handling variation across markets, and interpreting performance across interconnected outcomes.

6. How does payment strategy reduce operational risk?

By providing a shared framework for decision-making, it prevents reactive fixes from accumulating into systemic misalignment and makes outcomes easier to interpret over time.

7. Why is measurement described as strategic rather than operational?

Because the value lies in understanding how outcomes interact, not just tracking individual metrics. Strategic measurement highlights imbalance before it becomes visible as failure.

8. What happens when a payment strategy is missing?

Teams optimise locally, decisions conflict, and complexity accumulates quietly. Payments continue to function but become harder to manage, explain, and scale sustainably.

9. How does payment strategy affect market expansion?

It allows expansion to be governed by repeatable principles rather than bespoke decisions, reducing fragmentation and preserving coherence as new markets are added.

10. Who typically owns payments strategy in mature organisations?

Ownership is usually shared across functions, but responsibility is clearly defined. Strategy exists to coordinate decisions rather than sit within a single team.

11. Is payment strategy mainly about governance and control?

It is about clarity and coordination. Governance is the mechanism that allows payments to evolve deliberately rather than reactively as complexity increases.

12. Does treating payments strategically slow innovation?

It may slow unstructured experimentation, but it enables sustainable change by ensuring that innovation does not degrade outcomes elsewhere in the system.