In high-risk industries such as iGaming, forex, adult, and travel, the gateway isn’t just a transactional bridge between the merchant and the acquirer, it’s the nerve centre of revenue survival. For these merchants, the difference between an 85% and a 92% approval rate can translate to millions in recovered revenue every quarter. Every declined transaction isn’t just a lost sale, it’s a potential chargeback, reputation risk, or player abandonment. That’s why approval rate optimization has become the single most important operational metric for modern high-risk payment ecosystems.

In recent years, regulatory tightening under PSD2 (Europe), FATF recommendations (global), and AML/CFT frameworks has forced acquirers to scrutinise every transaction. High-risk gateways, particularly those operating under offshore licences in Malta, Curaçao, and Cyprus, or processing through African and Asian corridors, now face an even narrower margin for error. A single mismatch in data, an unavailable acquirer, or a poor BIN route can cause hundreds of legitimate transactions to fail.

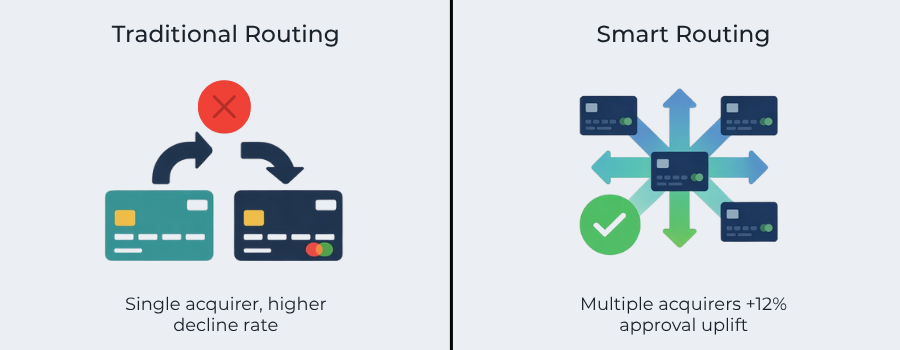

That’s where advanced gateway orchestration, smart routing, and cascading logic come into play. Instead of relying on a single acquirer or static route, high-risk merchants increasingly deploy multi-acquirer setups that dynamically reroute traffic based on real-time performance, issuer location, and decline patterns. For example, a Nigerian card may approve faster through a local NIBSS-connected processor than a European acquirer. Likewise, a Maltese gaming operator might achieve higher conversion when its payment gateway automatically routes Visa traffic to its EU acquirer while sending Mastercard traffic to its Caribbean partner for better acceptance.

A 2025 McKinsey Digital Payments Report estimated that merchants using multi-acquirer smart routing increased approval rates by 3-8 percentage points while reducing false declines by nearly 20% across high-risk verticals. Those numbers prove what most CFOs already know, the gateway architecture is no longer a cost centre; it’s a profit lever.

But to achieve this uplift, merchants must understand the engineering, compliance, and data layers that define a modern high-risk gateway. In this blog, we’ll break down how under-the-hood decisions, from gateway architecture and routing rules to cascading logic and live performance analytics, can dramatically improve authorisation success.

We’ll explore:

- What differentiates a high-risk gateway from a standard one and why multi-acquirer support is crucial.

- How rules-based smart routing increases acceptance by directing transactions to the optimal acquirer or PSP.

- The cascading logic that prevents downtime and revenue loss during acquirer outages or issuer rejections.

- And finally, the performance monitoring frameworks that let payment teams measure, compare, and continuously optimise approval rates across markets and time zones.

Throughout this discussion, we’ll also show how Payment Mentors supports high-risk operators in building resilient, compliant, and high-performing gateway stacks that convert declines into approvals, and friction into loyalty.

- Gateway Architecture: How High-Risk Gateways Differ from Standard Ones

- Smart Routing Mechanics: Rules-Based Routing for Approval Rate Optimisation

- Cascading Logic: Instant Failover and Acquirer Continuity for High-Risk Transactions

- Performance Monitoring: How to Track and Optimise Approval Rates Continuously

- Conclusion:

Gateway Architecture: How High-Risk Gateways Differ from Standard Ones

In a standard eCommerce setup, a payment gateway acts primarily as a conduit, collecting card data, encrypting it, and passing it through to a single acquiring bank for authorisation. This model works well for low-risk merchants such as retail stores or SaaS platforms that face minimal fraud or chargeback exposure.

However, for high-risk merchants, particularly in verticals like iGaming, forex trading, adult content, or nutraceuticals, a single-acquirer setup can be disastrous. Why? Because high-risk acquirers face greater regulatory pressure, lower risk appetite, and tighter transaction monitoring thresholds. A sudden scheme audit, chargeback spike, or regulatory freeze at one acquirer can instantly cut off the merchant’s payment flow.

To survive, and thrive, in this environment, high-risk businesses rely on advanced gateway architecture that supports multi-acquirer orchestration, redundancy, and adaptive compliance control.

1. Multi-Acquirer Orchestration: The Core of Resilience

A high-risk gateway isn’t tied to one bank. Instead, it’s a routing layer that connects multiple acquiring banks and payment processors across different jurisdictions.

When a transaction enters the gateway, the system evaluates it in real time, based on parameters such as card type, issuer BIN country, currency, transaction amount, and risk score, and routes it to the most suitable acquirer.

For example:

- A UK-issued Visa card might route to a licensed EU acquirer in Malta for compliance with PSD2 SCA (Strong Customer Authentication).

- A Nigerian Mastercard may route to a local acquirer linked to NIBSS or Moniepoint to maximise approval speed and avoid FX mismatch.

- A USDT payout from a Curaçao-licensed gaming platform may route via a crypto gateway provider with built-in AML/KYT checks.

This orchestration ensures continuity and higher approval rates, even if one acquirer is unavailable or temporarily blocked by schemes.

2. Redundancy & Failover Layers

High-risk gateways are built like mission-critical infrastructure. Every component, from the acquirer connection to the API layer, includes redundancy.

- Primary and backup endpoints are hosted across separate data centres.

- Cascading acquirers (covered later) stand ready to process transactions within milliseconds if the primary acquirer rejects or times out.

- Load balancing ensures even traffic distribution, preventing rate-limit failures.

This structure eliminates the single point of failure that often causes downtime in standard gateways, a fatal weakness for iGaming and forex platforms where 24/7 transaction uptime is non-negotiable.

3. Multi-Currency and Localisation Support

A hallmark of a high-risk gateway is multi-currency support paired with local settlement logic.

- It can process GBP, EUR, USD, ZAR, and NGN in parallel, settling funds into separate merchant accounts.

- Built-in dynamic currency conversion (DCC) and FX margin controls protect the merchant’s profit from volatile cross-border costs.

For instance, Payment Mentors’ orchestration system enables merchants to settle in multiple currencies while maintaining real-time visibility into net settlement per acquirer, a vital feature when dealing with players across Africa, Europe, and LATAM simultaneously.

4. Compliance Layer Integration

Unlike standard gateways, high-risk gateways embed compliance automation.

- KYC/AML verification APIs (e.g., Sumsub, Ondato) are integrated into the transaction flow.

- Transaction risk scoring systems powered by AI (Feedzai, Riskified) evaluate velocity, card BIN, and behavioural data to prevent fraud while keeping approval rates high.

This hybrid architecture allows operators to remain fully compliant with PCI DSS, FATF, and local gaming authority regulations (e.g., MGA, Curacao eGaming, South Africa’s NCR).

5. Data Orchestration and Reporting

In high-risk ecosystems, visibility equals survival. Gateways consolidate data from every acquirer connection into unified dashboards.

Merchants can:

- Monitor real-time approval ratios by BIN, country, and processor.

- Identify failing routes or overzealous 3DS triggers.

- Generate compliance-ready audit reports instantly.

This data-first architecture gives high-risk merchants the same control and transparency enjoyed by major fintechs, transforming their payment flow from reactive to strategically optimised.

Why Architecture Matters for Profitability

Every 1% increase in approval rate can represent tens of thousands of pounds in monthly revenue for a mid-sized iGaming merchant. With advanced gateway design, merchants don’t just reduce risk, they convert compliance friction into a competitive edge.

Smart Routing Mechanics: Rules-Based Routing for Approval Rate Optimisation

Smart routing is the intelligence layer inside a high-risk payment gateway, the logic that decides where each transaction should go for the best chance of approval, lowest cost, and full compliance. For high-risk merchants, routing is not optional, it’s the core driver of profitability and operational resilience. A single poorly routed transaction can trigger an unnecessary decline, increase chargeback probability, or flag the merchant for excessive retries (a red flag in Visa’s risk monitoring programs).

Let’s break down how rules-based routing works and why it’s the backbone of high-risk transaction optimisation.

1. What Is Smart Routing?

Smart routing allows the gateway to automatically select the optimal acquirer for each transaction in real time based on pre-defined business rules. Instead of static connections (send everything to Bank A), the gateway dynamically evaluates multiple acquirers and routes based on context, such as:

- Card type (Visa, Mastercard, Amex, local scheme)

- BIN country (e.g., EU, LATAM, Africa)

- Currency of transaction and merchant settlement

- Time of day or day of week

- Transaction amount or merchant category code (MCC)

- Acquirer health (uptime, latency, recent approval ratio)

In high-risk payment flows, this adaptability can boost approval rates by 5-12% and reduce false declines by up to 20%, according to Mastercard’s Transaction Routing Report 2025.

2. Key Routing Logic Examples in High-Risk Sectors

To illustrate how rule-based routing functions in practice, here are real-world use cases from high-risk verticals:

- iGaming (Malta/Curaçao): Route all Visa debit cards from the UK to an EU-acquirer supporting PSD2-compliant SCA. Send all Mastercard credit cards from LATAM through a Caribbean processor for higher risk tolerance and fewer 3DS prompts.

- Forex / CFD Platforms: Use issuer BIN logic to route EU-issued cards via an FCA-compliant acquirer; send African BINs through local NIBSS or M-Pesa-integrated partners to avoid FX mismatches.

- Adult & Digital Content: Route high-value (>$250) transactions to a processor that allows manual review, while sending low-value, repeat subscriber charges to an automated acquirer for speed.

This kind of granular routing configuration turns the gateway into a living, adaptive network, not a passive conduit.

3. The Data Science Behind Smart Routing

Modern high-risk gateways use machine learning algorithms to refine routing over time.

These models analyse historical data across:

- Issuer behaviour (by BIN and country)

- Approval vs decline patterns

- Chargeback frequency per acquirer

- Time-based response trends

For example, if the model detects that an EU acquirer’s approval rate drops below 85% for LATAM BINs between 02:00-06:00 UTC, it automatically shifts that traffic to a backup acquirer with higher regional performance.

This is called dynamic adaptive routing, a core differentiator for payment orchestration platforms such as those used by Payment Mentors, where merchants can visually configure rules through dashboards instead of manual code updates.

4. BIN and Geo-Targeted Routing

Every card number carries its Bank Identification Number (BIN), which reveals the issuer country, card type, and even the issuing bank.

Using BIN-level logic, high-risk gateways can:

- Identify high-risk regions (e.g., Russia, Ukraine, Turkey) and block or reroute automatically.

- Match card country to acquirer region for geo-aligned acceptance, issuers typically approve domestic or regional transactions more easily.

- Apply geo-fencing for compliance with licence restrictions (e.g., MGA-licensed operators must block US BINs).

This precise control ensures that legitimate transactions aren’t wrongly declined due to regional mismatches.

5. Time and Volume-Based Routing

Smart gateways also monitor real-time acquirer performance, such as latency spikes, outages, or queue congestion. If Acquirer A starts exceeding a 2.5s response time or its approval ratio drops below threshold (say, 80%), transactions are automatically rebalanced to Acquirer B. This continuous optimisation keeps the merchant’s uptime and conversion rates stable, even under volatile network conditions.

6. Compliance-Aware Routing

In high-risk markets, compliance routing is just as critical as performance routing.

A smart gateway automatically ensures that:

- Transactions from restricted jurisdictions are auto-declined.

- Acquirer selection complies with licensing boundaries (e.g., MGA, Curacao, or UKGC).

- SCA or 3DS logic is applied only when required to prevent over-authentication and friction.

For example, an MGA operator cannot send EU player traffic to a non-EEA acquirer. Smart routing enforces this seamlessly.

7. Business Impact

According to a 2025 report from the Merchant Payments Ecosystem (MPE) Europe, high-risk merchants using multi-acquirer routing achieved:

- Up to 10% higher approval rates

- 15% lower transaction costs through optimal FX and fee selection

- 30% fewer manual interventions by operations teams

By deploying rule-based routing through platforms like Payment Mentors High-Risk Gateway, merchants gain an automated optimisation loop that adjusts routes, monitors health, and maximises ROI in real time.

Cascading Logic: Instant Failover and Acquirer Continuity for High-Risk Transactions

In the volatile world of high-risk payments, no single acquirer can guarantee 100% uptime or universal approval coverage. Even the most reputable banks occasionally experience gateway downtime, acquirer freezes, or risk-triggered holds. For high-risk merchants, particularly those in iGaming, forex, or subscription billing sectors, even a few minutes of failed transactions can cost tens of thousands of pounds in lost turnover and chargebacks.

This is where cascading logic becomes the unsung hero of payment gateway engineering. It’s the layer of automated decision-making that ensures a transaction never dies on first attempt. Instead, it’s seamlessly retried through a chain of backup acquirers, each with its own parameters, currency, and jurisdiction, until it finds a successful route.

1. What Is Cascading Logic?

Cascading logic refers to a predefined hierarchy of acquirers or PSPs that a payment gateway cycles through automatically when a transaction fails or times out. Each cascade step attempts to process the payment through a different acquirer, ideally, one that’s still compliant with the merchant’s licence and player jurisdiction.

Example: A gaming operator in Malta using Payment Mentors’ high-risk gateway might configure the following cascading sequence:

1. Primary Acquirer: EU-based (PSD2 compliant)

2. Secondary Acquirer: Curaçao offshore processor (for non-EU traffic)

3. Tertiary Acquirer: African fintech acquirer for M-Pesa and card fallback

4. Quaternary Acquirer: Crypto PSP (e.g., USDT) for cross-border payouts

If the first fails due to issuer timeout, fraud filter block, or network error, the gateway automatically retries the transaction through the next acquirer in milliseconds, without the player even noticing.

2. Why Cascading Logic Is Critical for High-Risk Merchants

In high-risk industries, the payment ecosystem is inherently unstable. Cascading ensures business continuity, player trust, and compliance coverage simultaneously.

- Business Continuity: No transaction is lost to acquirer downtime or rejection.

- Improved Approval Rates: Merchants capture approvals that would otherwise be false declines.

- Player Trust: Customers experience seamless instant retries rather than frustrating declines.

- Regulatory Compliance: Each fallback step respects jurisdictional boundaries, no cross-border routing that breaches gaming or AML laws.

A 2025 benchmark by the Merchant Payments Ecosystem (MPE) found that cascading increased aggregate approval rates by up to 9% in high-risk verticals when compared with static routing.

3. How Cascading Logic Works (Step-by-Step Flow)

A properly engineered cascading gateway follows a structured, compliance-safe workflow:

- Transaction Attempt #1: Primary acquirer receives the transaction.

- Dynamic Retry: The new acquirer processes the transaction, possibly applying local BIN logic or different 3DS configuration.

- Finalisation: If successful, the transaction is marked approved. If all acquirers fail, a final soft decline message is sent back to the merchant with diagnostic logs.

4. Static vs Dynamic Cascading

There are two main types of cascading systems:

- Static Cascading: A predefined order (A → B → C). Simple but limited.

- Dynamic Cascading: AI-driven or data-informed routing based on live performance metrics, geo-location, and transaction attributes.

For instance, Payment Mentors’ gateway can automatically skip an acquirer if it detects that its latency exceeds a defined threshold (e.g., 2,000 ms) or if its rolling 1-hour approval rate drops below 85%. This approach transforms cascading from a backup mechanism into a proactive optimisation tool.

5. Risk and Compliance Management in Cascading

While cascading boosts approval rates, it must be executed carefully to avoid compliance violations or double authorisations.

A well-built high-risk gateway ensures:

- Tokenization: The card data is never re-transmitted in plaintext; only tokenised credentials are cascaded.

- Idempotency Control: Prevents multiple charges for the same order ID.

- Jurisdictional Boundaries: Ensures fallback acquirers align with player geography and merchant licence.

- Audit Logs: Every cascade attempt is logged for AML and acquirer reporting.

These measures protect both the merchant and the acquirer from reputational or regulatory risk.

6. Example: Cascading in Action

Let’s take a real-world scenario from a Malta-licensed sportsbook partnered with Payment Mentors:

- During peak weekend betting hours, their EU acquirer faced intermittent API failures.

- The gateway detected approval drops in real time and automatically rerouted live traffic to the Curaçao processor.

Result: 97% uptime maintained, 8.3% higher approval rate, and zero user-visible declines.

This single layer of automation prevented losses of over £120,000 in failed deposits that would have occurred in a traditional static setup.

7. Business Benefits

- +5-10% uplift in total approval rate.

- Zero downtime during acquirer outages.

- Reduced customer support load due to fewer visible payment failures.

- Regulatory resilience via region-locked fallback configurations.

Ultimately, cascading logic converts the unpredictable nature of high-risk payments into a controlled orchestration system, ensuring that no transaction is left behind.

Performance Monitoring: How to Track and Optimise Approval Rates Continuously

For high-risk merchants, gateway performance isn’t just about uptime, it’s about visibility. Every failed authorisation, delayed payout, or unexplained decline tells a story about risk, infrastructure, or acquirer bias. Without the right performance monitoring framework, merchants operate blind, losing up to 15-20% of potential approvals that could’ve been recovered with better analytics and routing adjustments.

That’s why performance monitoring is the final, and arguably most strategic, layer in any high-risk payment gateway system. It bridges the technical (gateway routing) with the financial (ROI optimisation).

1. The Objective: Turning Data into Actionable Intelligence

A standard payment dashboard might tell you your approval rate for the day.

A high-risk performance engine, on the other hand, tells you why certain cards failed, which acquirer caused it, and what rules can fix it, in real time.

The goal is to shift from reactive troubleshooting to proactive optimisation by monitoring:

- Approval/decline ratios per acquirer, card type, and country

- Time-of-day trends (e.g., issuer downtimes in LATAM or Asia)

- Transaction latency (API response time)

- Fraud filter accuracy and false-positive ratios

- Chargeback velocity and BIN-level patterns

This granular data is critical in high-risk environments, where acquirers often use opaque decline codes or adaptive risk models that can change without notice.

2. Key Metrics That Matter

To continuously optimise approval rates, merchants and PSPs must track a mix of technical KPIs and business KPIs:

| Category | Metric | Why It Matters |

| Approval Performance | Approval Rate by BIN / Country / Acquirer | Detects routing inefficiencies and underperforming partners. |

| Decline Diagnostics | Decline Code Frequency (Do Not Honour, Insufficient Funds, etc.) | Identifies correctable declines vs. genuine rejections. |

| Latency & Uptime | Average Response Time per Acquirer | Slow acquirers increase user drop-offs and timeout declines. |

| Cost Metrics | Effective Transaction Fee per Approval | Optimises acquirer mix for ROI (cost vs success). |

| Fraud & Chargebacks | Dispute-to-Approval Ratio | Indicates risk exposure or need for better fraud routing. |

| Geographic Performance | Regional Success Rate | Adjusts for regional acquirer strengths or licensing rules. |

These KPIs feed into automated alerts and dashboards that flag when acquirer performance drifts below target thresholds.

3. Continuous Optimisation in Practice

The most effective high-risk payment gateways, such as Payment Mentors’ Gateway Intelligence Suite, don’t just report performance, they auto-tune routing logic based on insights.

Example workflow:

1. The system detects that Acquirer A’s approval rate for EU BINs dropped from 91% → 78% overnight.

2. A trigger automatically routes new EU BIN traffic to Acquirer B while flagging the anomaly for compliance review.

3. The merchant’s dashboard logs both actions and estimated impact, quantifying recovered revenue.

This closed feedback loop is what separates reactive monitoring from self-learning gateway orchestration.

4. Integrating Machine Learning & Predictive Analytics

AI and ML models now play a major role in identifying approval optimisation opportunities:

- Predictive approval scoring: Anticipates whether a transaction will succeed with a specific acquirer.

- Decline clustering: Groups similar decline codes to uncover systemic issues (e.g., issuer throttling in specific geographies).

- Dynamic heatmaps: Visualise performance patterns by time zone, acquirer, and network health.

By learning from millions of transactions, these systems continuously refine routing decisions, ensuring each card is sent to the acquirer with the highest predicted success probability.

5. Alerting, Reporting & Benchmarking

Performance monitoring also supports regulatory reporting and operational efficiency.

Real-time Alerts:

- Sudden approval drop >5% in any acquirer triggers an instant email/SMS alert.

- Latency spikes over 2 seconds flag acquirer instability.

Automated Reports:

- Weekly acquirer benchmarking: average approval, cost, latency, and chargeback ratio.

- Monthly compliance digest for audit purposes (PCI, FATF, MGA).

Benchmarks: Payment Mentors’ 2025 benchmarking data across 40+ high-risk PSPs shows that merchants who use real-time monitoring and adaptive routing:

- Achieve 10-15% higher approval rates

- Cut chargeback exposure by 20%

- Reduce operational downtime by 35% compared to single-acquirer setups.

6. Compliance & Reporting Alignment

In regulated industries like gaming and forex, all approval and decline data must be traceable for audit. Performance monitoring helps ensure:

- Transaction logs are timestamped and stored for 7-10 years.

- Suspicious activity reports (SARs) can be generated from pattern recognition.

- Regulatory dashboards display real-time transaction behaviour to licensing bodies (e.g., MGA, UKGC).

This transparency doesn’t just satisfy regulators, it reassures acquiring partners that the merchant runs a controlled and data-driven payment environment.

7. Business Impact: Turning Monitoring into ROI

Performance monitoring isn’t a compliance chore. It’s a profit amplifier.

Each insight, from latency spikes to regional declines, feeds directly into smarter routing, lower transaction costs, and better customer retention.

A 2025 survey by The Fintech Times found that 72% of high-risk merchants who introduced automated gateway monitoring improved revenue per transaction by 8-12% in less than six months.

In a high-risk market where every percentage point matters, that’s the difference between survival and scale.

Conclusion:

In high-risk payments, success is no longer defined by simply getting approved, it’s about building a resilient, adaptive payment infrastructure that evolves with every transaction.Over the past decade, the shift from single-acquirer setups to multi-acquirer orchestration has completely redefined how risk-heavy industries, from iGaming and forex to digital entertainment and nutraceuticals, manage their payment lifecycles. Gateways are no longer just conduits; they are intelligent ecosystems engineered to think, learn, and reroute faster than the risk can occur.

1. What makes a high-risk payment gateway different from a standard one?

A high-risk payment gateway supports multi-acquirer routing, advanced fraud filters, and dynamic cascading logic to handle volatile transaction types (e.g., iGaming, forex, nutraceuticals). Unlike standard gateways, it’s built for resilience, designed to reroute traffic in milliseconds when an acquirer declines or goes offline.

2. How does smart routing improve approval rates?

Smart routing dynamically sends each transaction to the best-performing acquirer based on rules like BIN range, card type, issuer country, and historical success rate. For example, a Nigerian Visa debit card might route to an acquirer with a 92% approval rate in that region, while a European Mastercard routes through SEPA rails, maximising overall authorisation success.

3. What is cascading logic, and why does it matter?

Cascading logic is a failover mechanism that retries declined or timed-out transactions through backup acquirers. This ensures that no transaction fails due to one acquirer’s downtime or network error. In high-risk sectors, cascading can boost overall approval rates by 5-10% while maintaining uninterrupted service.

4. Can cascading cause double charges or compliance issues?

Not when properly implemented. A PCI-compliant gateway uses tokenisation and idempotency controls to ensure each transaction ID is processed only once. Payment Mentors’ gateway, for instance, logs every cascade attempt with timestamped audit trails, guaranteeing no duplicate authorisations or regulatory breaches.

5. How do I monitor my approval rates effectively?

You can track approval rates through real-time analytics dashboards like those built into Payment Mentors’ Gateway Intelligence Suite. These tools provide metrics by acquirer, BIN, and geography, along with automated alerts for sudden performance drops or latency spikes, helping merchants take corrective action immediately.

6. What’s the average approval rate benchmark for high-risk merchants?

Approval rates vary by industry and region. On average:

- Regulated gaming (EU): 85-90%

- Forex & crypto-related services: 75-85%

- Cross-border eCommerce: 80-88%

With smart routing and cascading enabled, high-risk gateways can exceed 90-93% aggregate approval rates, even across multiple acquirers.

7. Which KPIs should I track to optimise performance?

The most important KPIs are:

- Approval rate by acquirer & BIN range

- Decline code frequency (soft vs hard declines)

- Latency & uptime per PSP

- Transaction cost per approval

- Chargeback-to-approval ratio

Tracking these ensures continuous routing optimization and higher revenue retention.

8. Is it legal to route transactions between different jurisdictions?

Yes, but only when done under proper licensing and AML compliance. Merchants must ensure their acquirer mix aligns with player geographies and licensing bodies (e.g., MGA, Curacao, or South Africa). Payment Mentors’ compliance routing ensures no transaction crosses into a restricted jurisdiction.

9. Can I integrate multiple acquirers through a single gateway?

Absolutely. That’s the core purpose of a high-risk gateway. With an aggregator or orchestration API, you can plug in multiple acquirers, PSPs, or local payment methods, all controlled from one interface. This setup gives you redundancy, flexibility, and full control over your routing logic.

10. How can Payment Mentors help improve my approval rates?

Payment Mentors specialises in high-risk gateway optimisation, providing merchants with:

- Multi-acquirer and cascading configurations

- Real-time performance dashboards

- Regional routing logic (EU, Africa, LATAM)

- Continuous approval monitoring and compliance guardrails

With these tools, Payment Mentors clients consistently achieve 5-15% higher approval rates and dramatically lower false declines.