Payment stability has become one of the defining operational challenges for forex and crypto businesses heading into 2026. In an environment where regulatory scrutiny is tightening and payment providers are increasingly selective, the ability to process deposits and withdrawals consistently is no longer assumed. For many firms, stability is now something that must be earned, demonstrated, and continuously maintained.

This shift matters because payment disruptions no longer sit quietly in the background. Delayed settlements, withdrawn payment methods, or sudden PSP exits directly affect client confidence, liquidity management and regulatory standing. In forex and crypto especially, where customers expect fast access to funds and real-time execution, even short-lived payment friction can trigger reputational damage that is difficult to reverse.

Licensing has emerged as a critical stabilising factor in this landscape. Not because regulation magically removes risk, but because it changes how that risk is perceived and managed by banks, PSPs and counterparties. Licensed businesses operate within defined frameworks for governance, safeguarding and oversight, allowing payment partners to assess exposure with far greater precision.

For high-risk merchants and PSP-facing teams, this distinction is increasingly decisive. In 2026, licensed forex and crypto firms are not just more compliant, they are structurally better positioned to build resilient, predictable payment operations in a market that no longer tolerates ambiguity.

- What Payment Instability Looked Like in Unlicensed or Lightly Regulated Models

- Why Licensing Changes the Payment Risk Profile Fundamentally

- Structural Improvements Licensed Forex & Crypto Firms Bring to Payment Stability

- How Regulation Enables Better PSP Risk Modelling in 2026

- Crypto-Specific Shifts After MiCA: Stability Through Standardisation

- Forex Brokers: How Mature Licensing Improves Client Fund Flows

- Conclusion

- FAQ

What Payment Instability Looked Like in Unlicensed or Lightly Regulated Models

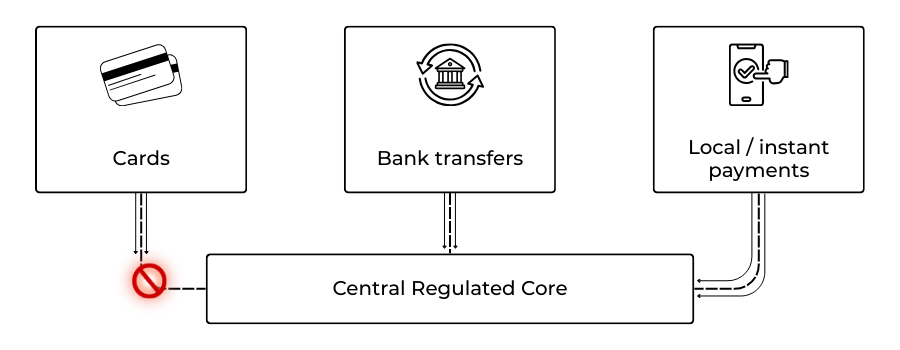

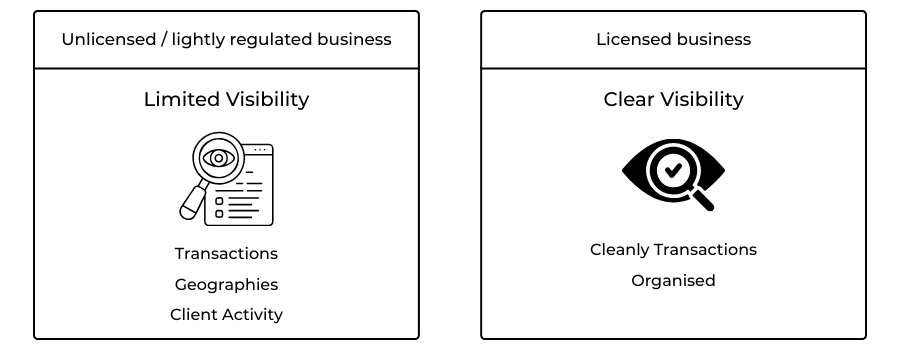

In unlicensed or lightly regulated forex and crypto businesses, payment instability was rarely caused by a single failure. It was the outcome of cumulative uncertainty. PSPs were not reacting to one bad transaction or one compliance miss; they were responding to an environment where too many critical questions could not be answered with confidence.

From a payment provider’s perspective, these businesses operated with blurred boundaries. Client activity, geographic exposure and transaction purpose were often technically disclosed but operationally unclear. When volumes increased or behaviour shifted, risk teams struggled to distinguish between normal market dynamics and emerging exposure. In the absence of regulatory anchoring, uncertainty itself became the risk.

This uncertainty shaped how PSPs behaved internally:

- Defensive Buffers: Rather than investing in granular monitoring, providers defaulted to protective actions.

- Extended Settlement Windows: Windows were stretched to buy time for secondary reviews.

- Aggressive Reserves: Capital was locked in rolling holds to absorb unknowns.

- Abrupt Exits: Accounts were frozen simply because the risk could not be modelled quickly enough.

For merchants, the experience felt arbitrary. Payment methods disappeared without warning, and operational teams spent more time managing PSP fires than improving their core trading infrastructure.

Why Licensing Changes the Payment Risk Profile Fundamentally

Licensing does not make a firm safe. What it does is change how payment partners can understand and control the risk. In 2026, most PSP decisions are driven less by what a business says, and more by whether its risk can be defended internally to compliance committees and banking partners.

Licensing turns uncertainty into something measurable

In lightly regulated models, a PSP often ends up pricing unknowns. Licensing reduces the size of that unknown bucket. A licensed firm operates with clearer rules around governance and safeguarding, giving providers fixed reference points. Even when the sector remains high-risk, the risk becomes legible.

How PSPs and banks evaluate licensed businesses differently

Payment stability is mostly a trust problem disguised as an operational problem. A licence changes the risk conversation because it supports more defensible partner decisions:

- Recognised Supervision: The business operates within a formal framework.

- Ownership Transparency: UBO (Ultimate Beneficial Owner) checks are harder to disguise.

- Safeguarding Evidence: Client fund handling is easier to reconcile.

- Structured Cycles: Compliance reviews follow regular beats rather than emergency escalations.

The key distinction: Licensing doesn’t remove risk; it changes how it’s managed. When risk teams can explain what they see, they apply proportionate controls rather than blunt restrictions.

Structural Improvements Licensed Forex & Crypto Firms Bring to Payment Stability

Stability does not improve just because a licence exists on paper. It improves because licensing forces structural discipline into areas where payments previously failed under pressure.

From Provisional Access to Relationship Continuity

Unlicensed businesses are often processed on tolerance. Licensed businesses are processed on expectation. When risk indicators move, PSPs are now more willing to pause, question, and recalibrate instead of exiting immediately.

Settlement Stops Being a Defensive Control

In fragile models, settlement delays are a risk buffer. Licensing changes that dynamic. Clearer transaction purposes and auditable reporting make it easier for PSPs to justify releasing funds on predictable timelines. Settlement becomes an operational process again, not a risk hedge.

Disputes Become Manageable Instead of Destabilising

What destabilises payments is not dispute volume, but dispute unpredictability. Licensed firms present fewer grey areas; transaction flows are easier to trace, allowing PSP risk teams to contextualise spikes instead of reacting to them as signals of systemic failure.

Payment Architecture Shifts from Survival to Resilience

Licensed businesses in 2026 are more likely to operate diversified, regulator-aligned payment stacks. This provides:

- Reduced dependency on any single rail.

- Greater tolerance during corridor reviews.

- Controlled rerouting of flows under pressure.

How Regulation Enables Better PSP Risk Modelling in 2026

By 2026, most payment stability decisions are made long before a transaction is processed. They happen inside PSP risk teams, where exposure is modelled, defended, and priced internally. Regulation matters here because it changes how those models are built, not just the conclusions they reach.

How unregulated risk was previously modelled

In lightly regulated environments, PSPs often relied on indirect indicators. Volume spikes, geographic shifts, or behavioural anomalies were treated as warning signs because there was no reliable framework to interpret them against. Risk models leaned conservative, and controls were applied broadly to compensate for uncertainty.

This approach protected the PSP, but it created instability for merchants.

What regulation changes inside PSP decision frameworks

Licensing gives risk teams fixed reference points. Instead of modelling worst-case scenarios by default, PSPs can assess behaviour against known regulatory obligations, capital buffers, and safeguarding rules. That enables more granular decision-making.

Risk reviews become less reactive because exposure can be justified internally without escalating every anomaly to a potential exit event.

What PSPs can now model with greater confidence

Regulated environments allow PSPs to move from defensive assumptions to evidence-based controls:

Transaction behaviour can be assessed against permitted licensed activity

Client fund flows can be reconciled within safeguarding frameworks

Geographic exposure can be evaluated alongside regulatory reporting obligations

Dispute trends can be contextualised rather than treated as binary risk signals

Why this directly improves payment stability

When PSPs can explain why risk remains acceptable, they are less likely to rely on blunt tools such as sudden reserves, delayed settlements, or account freezes. Stability emerges not because scrutiny is lighter, but because scrutiny is structured.

For licensed forex and crypto firms, this is one of the most underappreciated advantages of regulation in 2026.

Crypto-Specific Shifts After MiCA: Stability Through Standardisation

For crypto businesses operating in Europe, payment stability in 2026 is inseparable from the post-MiCA environment. What MiCA ultimately changed was not just authorisation requirements, but the way crypto activity is interpreted by banks and PSPs. The sector moved from being assessed through fragmented national lenses to being evaluated against a common regulatory language.

Before MiCA, payment providers struggled with inconsistency. The same exchange could appear compliant in one jurisdiction and opaque in another. That ambiguity translated directly into conservative payment decisions: limited payment methods, higher reserves, and a reluctance to support scale. Stability was fragile because confidence was conditional.

MiCA replaced that ambiguity with standardisation. Clear CASP classifications, defined activity scopes, and harmonised supervision made it easier for PSPs to understand what a crypto business is allowed to do and just as importantly, what it is not. This reduced the need for defensive assumptions when onboarding or reviewing accounts.

In practice, this has stabilised fiat-crypto payment flows. PSPs are more willing to support local bank transfers, instant payment schemes, and higher transaction volumes when activity sits within a recognised framework. Reviews still occur, but they are framed around compliance alignment rather than existential risk.

For crypto firms, the effect is subtle but material. Payment access in 2026 is less about finding tolerance and more about demonstrating consistency within standardised rules, a shift that has quietly reshaped stability across the sector.

Forex Brokers: How Mature Licensing Improves Client Fund Flows

For licensed forex brokers, payment stability in 2026 is most visible at the client fund level. The way deposits and withdrawals move especially during volatile market periods has become a direct test of operational maturity.

Mature licensing frameworks impose clearer separation between operating capital and client funds. For PSPs, this separation is not theoretical. It makes reconciliation simpler, reduces uncertainty during reviews, and lowers the perceived risk of funds being trapped if a broker faces stress or enforcement action.

This clarity changes how payment partners behave when pressure increases. Withdrawal queues are less likely to trigger defensive delays, and temporary volume spikes are easier to accommodate because fund flows can be traced and justified. The result is not faster payments by default, but fewer disruptive slowdowns when conditions deteriorate.

In 2026, brokers that demonstrate disciplined fund handling are significantly better positioned to maintain continuity when it matters most.

Conclusion

Payment stability in forex and crypto has shifted from being an operational bonus to a structural requirement. In 2026, firms are no longer judged on their ability to access payment rails once, but on their ability to retain them under scrutiny, volatility, and regulatory pressure.

Licensing has become central to that shift. Not because it removes risk, but because it reshapes how risk is understood, monitored, and tolerated by PSPs and banks. For businesses operating in high-risk sectors, stability now comes from predictability, transparency, and resilience rather than workarounds.

As payment providers continue to narrow their risk appetite, licensed forex and crypto firms are increasingly the ones able to build durable, scalable payment operations not by avoiding oversight, but by operating confidently within it.

FAQ

1. Why is payment stability such a critical issue for forex and crypto businesses in 2026?

Payment providers are operating with tighter risk thresholds, stronger regulatory oversight, and less tolerance for ambiguity. Even short disruptions now have direct commercial and regulatory consequences.

2. Does licensing guarantee uninterrupted payment processing?

No. Licensing does not remove risk, but it significantly reduces unpredictable interruptions caused by uncertainty, poor transparency, or defensive PSP behaviour.

3. Why do PSPs prefer licensed forex and crypto firms?

Licensed firms operate within recognised supervisory frameworks, making their risk easier to model, justify internally, and manage over time.

4. How does licensing reduce sudden PSP exits?

It provides clearer governance, defined activity scopes, and accountability, which allows PSPs to adjust controls rather than terminate relationships abruptly.

5. Are licensed crypto businesses treated as low risk by PSPs?

No. Crypto remains high risk, but licensed firms are assessed as manageable risk rather than unknown exposure.

6. What role does MiCA play in payment stability for crypto firms?

MiCA standardises how crypto activity is classified and supervised across the EU, reducing fragmentation and improving PSP confidence in fiat-crypto flows.

7. Why do settlement delays occur more often in unlicensed models?

Delays are frequently used as defensive controls when PSPs lack confidence in transaction purpose, fund handling, or downstream risk.

8. How does licensing improve dispute and chargeback management?

Stronger KYC, clearer client agreements, and better transaction traceability make disputes more predictable and defensible.

9. Do licensed firms still face reserves and rolling holds?

Yes, but these are more likely to be proportionate, review-based, and transparent rather than sudden or indefinite.

10. Why is multi-rail payment architecture more common in licensed firms?

PSPs are more willing to support additional payment methods when regulatory foundations are clear and risk exposure is structured.

11. How does licensing affect withdrawal reliability for forex brokers?

Clear segregation and safeguarding of client funds reduce PSP hesitation during withdrawal spikes or market volatility.

12. Is licensing now a competitive advantage in payments?

Yes. In 2026, licensing increasingly determines which firms can maintain stable, scalable payment access over time.