In iGaming, loyalty has always been a volatile concept. Players move between operators at the tap of an app, comparing not only odds and bonuses but also how quickly winnings appear in their account. By 2026, the competitive edge is no longer defined by promotional spend or interface design; it’s defined by payout velocity. The operator that delivers verified winnings within seconds earns what no amount of advertising can buy: trust.

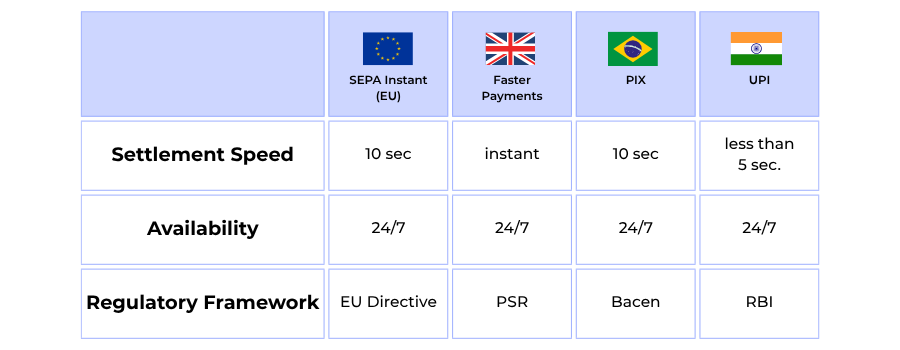

Over the past three years, real-time payment rails such as SEPA Instant in Europe, Faster Payments in the UK, PIX in Brazil and UPI in India have transformed consumer expectations.

Outside gaming, people now move funds instantly between banks, wallets, and marketplaces; inside gaming, they expect the same. A withdrawal that once took twenty-four hours now feels archaic. When operators delay payouts, even for legitimate compliance checks, players often perceive risk or instability, prompting chargebacks, duplicate disputes, and churn.

Research across high-risk verticals shows that a player’s likelihood to return for a second session rises by more than 40 % when withdrawals are instant or near-instant. Speed communicates solvency and fairness. It short-circuits the anxiety that follows a win: “Will I actually get my money?” For PSPs and acquirers supporting iGaming merchants, real-time settlement isn’t merely a technical upgrade; it’s a merchant-retention strategy. Each second shaved off a payout reinforces processing continuity, reduces support tickets, and strengthens the operator’s brand equity.

Yet speed brings scrutiny. Regulators in the EU and UK are simultaneously mandating faster payment access and tightening AML and transaction-monitoring obligations. The new EU Instant Payments Regulation, effective October 2025, demands that funds move within 10 seconds between compliant institutions, but it also holds PSPs responsible for verifying account ownership and screening each transaction in real time. For gaming operators, the challenge is balancing instant gratification with continuous due diligence.As we move through 2026, “instant” will evolve from a feature to a standard. Players will judge operators not by how quickly deposits clear but by how seamlessly withdrawals land. Those who modernise their payout infrastructure, linking open-banking APIs, tokenised credentials, and liquidity management tools, will convert payout speed into measurable loyalty. Those who don’t risk being left behind in the only race that truly matters in iGaming: the race to the player’s wallet.

- The Rise of Instant Payment Infrastructure

- Merchant Benefits: Why Instant Payouts Drive Loyalty and Reduce Losses

- Operational and Technical Considerations

- Regional Insights | LATAM and Africa Lead the Instant Payout Revolution

- Regulatory Oversight and Compliance in Instant Transfers

- 2026 Outlook | Open Banking Payout APIs and Card Network Instant Rails

- Conclusion

- FAQs

The Rise of Instant Payment Infrastructure

Until recently, “instant” payouts were marketing promises rather than a payment reality. Legacy card schemes depended on batch settlements, and wire transfers were constrained by banking hours. Between 2024 and 2026, a new generation of real-time payment rails, designed for 24/7 authorisation and settlement, has redrawn the financial map for operators in high-risk verticals such as iGaming.

Across continents, these infrastructures are now the backbone of the payout economy:

Europe: SEPA Instant Credit Transfer

The EU’s Instant Payments Regulation (European Commission, 2025) mandates that any payment between eurozone banks must reach the beneficiary within ten seconds, regardless of time or day. By October 2025, all PSPs connected to SEPA are required to offer this functionality at the same cost as a standard credit transfer. For iGaming acquirers, this removes the final friction between player verification and fund release, transactions that once settled overnight now complete before a support ticket is even logged.

United Kingdom: Faster Payments and the New Payments Architecture

In the UK, Pay.UK’s New Payments Architecture (NPA) upgrades the Faster Payments Service with richer ISO 20022 data fields and fraud-screening hooks. The Payment Systems Regulator (PSR, 2025) has signalled that PSPs must adopt Confirmation of Payee v2 for real-time account matching, a critical safeguard against Authorised Push Payment (“APP”) fraud. For licensed gaming operators, this translates to near-instant withdrawals underpinned by mandatory payee verification. Source: UK PSR Annual Plan 2025/26.

Brazil: PIX and the LATAM Ripple Effect

In LATAM, Brazil’s PIX network, managed by the Banco Central do Brasil, processed over 5 billion instant transfers in Q1 2025 alone, with adoption exceeding 150 million users nationwide (Banco Central do Brasil, 2025). PIX’s success has inspired neighbouring regulators in Chile and Colombia to fast-track similar frameworks, enabling iGaming payouts that credit player wallets within seconds, even on weekends.

India: UPI and the APAC Model

India’s Unified Payments Interface (UPI), operated by the National Payments Corporation of India (NPCI), has become the benchmark for open-API-driven instant payments, processing more than 14 billion transactions monthly as of mid-2025 (NPCI, 2025). For Asian operators and PSPs, UPI proves that real-time settlement and low interchange can coexist, setting expectations for other emerging markets such as Singapore (FAST) and Malaysia (DuitNow).

Operational Speed Meets Compliance Control

These rails deliver a dual outcome: frictionless liquidity and traceable compliance. Every transfer carries enriched data elements, payer ID, timestamp, and reference codes that feed directly into AML monitoring systems. This is vital for high-risk sectors, where each payout must be both instant and auditable. By aligning instant rails with tokenised credentials and open-banking consents, PSPs can achieve sub-ten-second settlement without forfeiting regulatory control.

Merchant Takeaway: Choosing a real-time rail is no longer about geography; it’s about finding the optimal balance between latency, liquidity, and compliance predictability. For iGaming operators, that means working with PSPs capable of orchestrating SEPA Instant, Faster Payments, PIX, and UPI under one unified API, turning payout speed into measurable loyalty and long-term player trust.

Merchant Benefits: Why Instant Payouts Drive Loyalty and Reduce Losses

For iGaming operators, the link between payout experience and player lifetime value is now quantifiable. Instant withdrawals are not just a convenience feature; they are a behavioural trigger that shapes trust, frequency, and dispute rates. Across regulated markets, “time to funds” has become one of the strongest predictors of player retention and merchant profitability.

Instant Gratification, Real Retention

Psychologically, instant gratification reinforces positive reinforcement cycles. Players who receive winnings within seconds associate that operator with fairness and control two emotions that directly drive re-engagement.

A 2025 survey by the European Gaming and Betting Association (EGBA) found that 68 percent of players cite “fast withdrawals” as their top factor in choosing a betting site, outweighing bonuses and odds quality (EGBA Consumer Behaviour Report, 2025). This finding mirrors broader fintech research showing that perceived payout reliability reduces churn by 30 – 40 per cent among digital-wallet users (FIS Global Payments Report, 2025).

In gaming, the dynamic is amplified. A delayed payout interrupts the emotional high of a win; an instant payout sustains it, encouraging the player to redeposit or replay. The result is not higher problem gambling but higher platform stickiness built on operational credibility.

Chargeback and Dispute Reduction

Instant payouts also act as a natural deterrent to chargebacks. When players receive their funds immediately, the incentive to reverse a transaction diminishes sharply. Real-time payment confirmation reduces ambiguity over settlement status, removing one of the leading causes of “friendly fraud.”

A 2024 study by Visa Europe reported that instant withdrawal merchants experienced up to 27 percent fewer post-transaction disputes versus those using batch settlements (Visa Risk Operations Report, 2024).

For high-risk acquirers managing thin margins, that reduction directly translates into lower scheme fines and better rolling-reserve terms.

Customer Support and NPS Uplift

Operational data from PSPs offering real-time payout APIs, such as Aeropay and Cross River Bank, show a measurable drop in inbound support volumes once instant settlement is introduced. Cross River’s 2025 case study on real-time gaming payouts noted a 35 percent reduction in payout-related tickets and a 17-point increase in Net Promoter Score (NPS) after migrating to an orchestration layer combining Faster Payments, PIX, and UPI (Cross River Bank Case Study, 2025).

For operators, that translates into tangible cost savings. Each avoided support interaction saves several minutes of manual reconciliation effort, labour that can be redirected to compliance oversight or player verification.

Liquidity Efficiency and Cash-Flow Stability

Traditional payout models force operators to hold excess liquidity in intermediary accounts to cover pending withdrawals. Real-time settlement allows more efficient treasury rotation: funds exit instantly but are balanced through prefunded wallets or just-in-time float management. When integrated with open-banking APIs, merchants can reconcile each payout to a verified account, lowering suspense balances and operational risk.

Merchant Takeaway: Instant payouts deliver more than player satisfaction; they recalibrate the entire risk-reward equation of high-risk processing. Faster withdrawals reduce disputes, compress support costs, and enhance liquidity management. Most importantly, they transform payout speed into a brand promise: a visible commitment to transparency and trust that no bonus code can match.

Operational and Technical Considerations

Behind every “instant payout” button lies an infrastructure of liquidity buffers, compliance checks, and synchronised APIs. For operators in regulated gaming markets, real-time settlement is not simply a technical upgrade; it’s an operational redesign touching treasury, risk, and reconciliation. Achieving true immediacy without compromising compliance requires precision in three domains: liquidity management, reconciliation accuracy, and fraud control.

Liquidity Management and Settlement Windows

Instant payouts are only as fast as the funds behind them. Operators must maintain prefunded or dynamically collateralised accounts with their PSPs to guarantee payout continuity even during peak play periods. The European Banking Authority (EBA, 2025) warns that instant payment providers must demonstrate “continuous funding capability” to mitigate settlement risk under the forthcoming Instant Payments Regulation (EBA Opinion on Settlement Risk, 2025).

High-risk merchants typically manage float through tiered liquidity pools, one per currency or jurisdiction, replenished via automated sweeps. API-based treasury tools now allow real-time monitoring of wallet balances across SEPA, Faster Payments, PIX, and UPI corridors. This visibility enables CFOs to align outgoing payouts with incoming deposits, reducing idle cash while maintaining 24/7 readiness.

Reconciliation and Data Synchronisation

Instant settlement removes the luxury of end-of-day batch reconciliation. Every transaction must reconcile automatically at the moment of confirmation. PSP orchestration platforms achieve this through ISO 20022-based messaging, embedding unique transaction identifiers (UTIs) that flow from the operator’s CRM to the acquirer’s ledger and back again.

In 2025, Pay.UK mandated richer reference fields within the New Payments Architecture (NPA) precisely to support real-time reconciliation and fraud analytics (Pay.UK NPA Data Standards Guide, 2025). For gaming operators handling thousands of micro-payouts daily, this ensures auditability and enables automated ledger posting into ERP systems without manual intervention, a key control for compliance audits under PCI DSS v4.0.1.

API Integration and Orchestration

Modern PSPs now expose unified APIs capable of routing payouts dynamically across multiple rails. When latency or cost thresholds are breached on one network, say, SEPA Instant, traffic can automatically fail over to a secondary rail, such as Visa Direct or Faster Payments. This orchestration logic is crucial for high-volume verticals like iGaming, where downtime directly equates to reputational damage.

Industry case studies from ACI Worldwide (2025) and Mambu (2024) show that PSPs adopting API-first architectures achieve a 35 – 40 % reduction in settlement errors and materially lower operational cost per payout (ACI Worldwide Real-Time Payments Benchmark, 2025).

Fraud, AML, and Continuous Monitoring

Speed cannot outrun compliance. Regulators now expect the same rigour in instant environments as in batch payments. The Financial Action Task Force (FATF, 2024) and the European Commission’s AMLD6 implementation guidelines require that sanctions screening, transaction scoring, and name matching occur within milliseconds of initiation (FATF Instant Payments Risk Note, 2024).

To achieve this, leading operators deploy AI-driven monitoring engines that flag anomalies in real time, such as payout bursts to new accounts or mismatched identities. These alerts feed directly into compliance dashboards, ensuring suspicious-activity reporting (SAR) obligations are met without slowing down the payout pipeline. Tokenised credentials and biometric re-authentications add further resilience by preventing account takeovers and synthetic-ID exploits.

Merchant Takeaway: Instant payouts compress the operational margin for error. Liquidity must be visible, ledgers must reconcile automatically, and compliance must operate at machine speed. Operators that treat these as strategic investments, not cost burdens, gain more than efficiency: they gain acquirer confidence, regulatory credibility, and the right to market “instant” as a guarantee rather than a gamble.

Regional Insights | LATAM and Africa Lead the Instant Payout Revolution

While Europe and the UK refine instant-payment regulations, it is Latin America and Africa that are redefining how real-time rails work in practice. In both regions, consumer adoption has leapfrogged legacy infrastructure. What began as domestic inclusion initiatives has evolved into a commercial framework powering real-time iGaming payouts, cross-border settlements, and micro-merchant ecosystems.

LATAM – PIX as the Continental Blueprint

Brazil’s PIX remains the world’s fastest-scaling instant-payment rail. Operated by the Banco Central do Brasil (BCB), PIX processed over 5 billion transfers in Q1 2025, up 36 % year-on-year. Unlike Europe’s gradual rollout, PIX achieved near-universal merchant adoption within four years of launch thanks to mandated interoperability across banks, fintechs, and PSPs.

For iGaming operators, PIX represents a direct-to-account payout model without card scheme intermediaries, reducing costs and chargeback exposure. According to the Federation of Brazilian Banks (FEBRABAN, 2025), merchants using PIX saw settlement costs fall by up to 60 % compared with card withdrawals, while payout times dropped from hours to seconds.

The ripple effect is continental. Chile’s 3xD and Colombia’s Transfiya networks, both modelled on PIX, are enabling regulated operators to offer near-instant withdrawals through licensed acquirers. Payment hubs such as dLocal and EBANX now aggregate these local rails into unified APIs, allowing cross-LATAM orchestration that rivals European speed but with far higher consumer penetration.

Africa: Mobile Money Meets Real-Time Infrastructure

Africa’s success is built on a different foundation: mobile money. Platforms such as M-Pesa (Kenya), Airtel Money (Nigeria) and EcoCash (Zimbabwe) have served as proto-instant networks for more than a decade. What’s new is their integration with central-bank-operated real-time systems like Tanzania Instant Payment System (TIPS) and the Pan-African Payment and Settlement System (PAPSS).

According to the African Development Bank Group (2025), over 70 % of Sub-Saharan Africa’s adult population now has access to some form of instant or mobile-linked payment rail (AfDB Digital Finance Outlook, 2025). For gaming PSPs licensed in African jurisdictions, this presents a double advantage: high reach and lower compliance friction, since most wallets already embed KYC layers approved by local regulators.

An illustrative case is Kenya, where integration between M-Pesa’s API and the Central Bank of Kenya’s IPRS verification enables real-time identity checks before funds are released—combining instant payouts with AML traceability. This approach is now influencing regulatory pilots in Ghana and South Africa, where the Rapid Payments Programme (RPP) went live in 2025 (BankServAfrica, 2025).

Cross-Regional Momentum

Both LATAM and Africa demonstrate that inclusion-driven payment innovation can outpace regulatory reform. Their instant rails are built with mobile-first architecture, API openness, and national-bank governance, elements that align closely with the EU’s 2025 Instant Payments Regulation. For iGaming operators expanding into emerging markets, these systems provide what card networks cannot: cost predictability, 24/7 availability, and near-zero failure rates.

PSPs supporting multi-region merchants are now layering LATAM and African rails into orchestration engines alongside SEPA Instant and Faster Payments. This convergence is reshaping liquidity strategies: funds can be mirrored between continents, enabling local-currency payouts to settle in seconds regardless of time zone.

Merchant Takeaway: Operators targeting LATAM and Africa should view real-time payouts not as an innovation experiment but as the new compliance baseline. Success requires regional PSP partners that combine instant connectivity (PIX, Transfiya, M-Pesa, RPP) with AML-aligned onboarding. Those who integrate these rails early gain first-mover trust in markets where payout speed equals credibility and player loyalty.

Regulatory Oversight and Compliance in Instant Transfers

As instant-payment rails move from innovation to infrastructure, regulators worldwide are closing the gap between speed and safeguard. The faster funds travel, the smaller the window becomes to detect fraud, money laundering, or sanctions breaches. For PSPs and iGaming operators, 2026 marks a decisive year in which instant settlement and instant compliance must operate in parallel.

The EU’s 2025 Instant Payments Regulation

In February 2025, the European Parliament approved the long-awaited Instant Payments Regulation, requiring all euro-area payment service providers to process transfers within ten seconds while maintaining real-time sanctions screening (European Commission, 2025).

The Regulation introduces three major compliance imperatives:

- Real-Time Sanctions Screening: PSPs must verify payer and payee data against the EU consolidated sanctions list before releasing funds. This shifts screening from batch to continuous mode, demanding advanced API orchestration and automated data feeds.

- IBAN-Name Matching: Providers must implement name-check systems comparable to the UK’s Confirmation of Payee, ensuring that transfers cannot be misdirected to unverified accounts.

For iGaming merchants, this means their acquirers and gateway partners must support both compliance-embedded rails and real-time reporting to retain licensing integrity under EU gambling directives.

United Kingdom: APP Fraud and Real-Time Accountability

The UK’s Payment Systems Regulator (PSR) has intensified oversight following the surge in Authorised Push Payment (APP) fraud, projected to exceed £700 million annually by 2026 (PSR Annual Plan 2025/26).

From October 2024, the Contingent Reimbursement Model Code became enforceable under the PSR’s Faster Payments mandate, obliging PSPs to reimburse victims of qualifying APP fraud. This liability shift has major implications for instant payouts: operators must prove that beneficiary validation and customer authentication controls were active at the time of transfer.

For gaming PSPs, compliance now requires dual confirmation: (1) that the payout account matches the verified player identity, and (2) that transaction risk scoring was executed in milliseconds. Failure to demonstrate either can expose both the PSP and merchant to reimbursement liability.

AML and KYC in a Sub-Ten-Second World

Traditional anti-money-laundering (AML) processes were designed for hours or days of latency. In an instant environment, risk assessments must compress into milliseconds. The Financial Action Task Force (FATF) issued its Instant Payments Risk Assessment Note (2024), warning that “the velocity of instant transactions may obscure the layering of illicit funds unless screening is embedded directly within payment gateways” (FATF, 2024).

To meet this requirement, PSPs are integrating AI-driven name-matching and behavioural scoring into their payment APIs. Modern orchestration engines use machine-learning models to assign transaction risk scores before settlement is approved. These results feed into Suspicious Activity Report (SAR) dashboards in real time, ensuring compliance with both FATF 40 Recommendations and local AMLD6 directives.

Data Traceability and Cross-Border Reporting

Instant payments introduce new record-keeping obligations. The European Banking Authority (EBA) stipulates that transaction data, including timestamps and confirmation references, must remain accessible for five years to enable forensic review of real-time fraud cases (EBA Opinion on Instant Payments Supervision, 2025).

Similarly, regulators in Australia and Singapore now require API-level audit logs for every instant transaction, linking payer KYC data to payment messages under ISO 20022. These digital trails provide the transparency that replaces manual investigation cycles, enabling supervisors to trace illicit flows without slowing down commerce.

Merchant Takeaway: Instant-payment compliance is no longer a post-transaction process; it’s part of the transaction itself. Every payout now carries embedded checks: sanctions screening, account matching, and dynamic AML scoring. Merchants that depend on PSPs lagging in these controls risk both licence suspension and financial penalties. The future belongs to operators who design their payout stack around regtech automation, ensuring that every ten-second payment is as compliant as it is fast.

2026 Outlook | Open Banking Payout APIs and Card Network Instant Rails

By 2026, the frontier of instant payments will extend beyond national rails. The convergence of open-banking APIs and card-network push-payment systems is creating a hybrid ecosystem where funds can move in seconds, regardless of whether the transaction travels through a banking channel or a card scheme. For iGaming operators, this convergence redefines both payout architecture and regulatory expectation.

Open Banking Payout APIs Become Mainstream

Since the introduction of PSD2, open-banking APIs have primarily supported account-to-account (A2A) collections. In 2025-2026, the evolution toward PSD3 and the Payment Services Regulation (PSR) transforms these interfaces into two-way pipelines capable of initiating withdrawals as well as deposits. The European Commission’s PSD3 draft (2025) mandates that Account-Servicing Payment Service Providers (ASPSPs) expose instant-payout endpoints to licensed third parties.

In practical terms, this allows a gaming PSP to trigger an outbound credit directly from a player’s verified bank account, secured through Strong Customer Authentication (SCA), and settle via SEPA Instant in under ten seconds. The result: reduced dependency on card schemes and lower interchange cost per payout.

The Open Banking Europe (OBE) Consortium’s 2025 roadmap predicts that A2A payout volumes will grow 40 % CAGR through 2026, largely driven by high-velocity industries such as gaming and gig-economy platforms.

Regulators view this positively: direct-to-bank rails provide traceability, explicit consent, and auditable transaction histories aligned with AMLD6.

Card Networks Go Real Time

While open banking expands laterally, card networks are modernising vertically. Visa Direct, Mastercard Send, and American Express Disbursements have all become instant-payment rails in their own right, processing push-to-card credits that land within seconds.

According to Visa Europe’s Real-Time Payments Outlook 2025, more than 10,000 financial institutions now support Visa Direct, with average payout latency under 30 seconds. Mastercard Send reports similar growth, with usage across 170 markets and a 25 % YoY increase in gaming and gig-economy disbursements (Mastercard Send Global Update, 2025).

For iGaming operators, push-to-card APIs offer instant reach to debit accounts without requiring bank-account credentials, ideal for cross-border markets where open banking is not yet standardised. The trade-off lies in higher per-transaction cost versus A2A rails, but the user experience often justifies the premium.

Orchestration Layers Unifying Rails

The PSPs leading in 2026 will not choose between rails; they will orchestrate them. Multi-rail orchestration engines dynamically route each payout based on region, compliance risk, and cost efficiency. A withdrawal initiated in Germany might execute through SEPA Instant; the same API call from Brazil could settle via PIX; a payout to a UK cardholder might flow through Visa Direct.

This approach mirrors the European Payments Council’s 2025 vision for “interoperable real-time ecosystems” under ISO 20022 messaging standards. By 2026, PSPs capable of switching rails automatically will dominate high-risk verticals, offering both compliance assurance and 24/7 liquidity resilience.

Embedded Finance and Tokenised Credentials

Another trend shaping 2026 is the tokenisation of payout credentials within embedded-finance frameworks. Payment-orchestration platforms increasingly issue merchant-controlled virtual IBANs (vIBANs) to isolate player funds and reconcile instant transactions automatically. The Bank for International Settlements (BIS) notes that tokenised account identifiers can cut reconciliation errors by over 50 % and reduce operational risk in instant-payment environments (BIS Innovation Hub Quarterly, 2025).

For regulators, this architecture satisfies dual objectives: consumer fund segregation and traceability under the EU’s forthcoming Financial Data Access Framework (FIDA). For merchants, it delivers frictionless payouts without exposing sensitive bank details, reinforcing both security and user confidence.

Merchant Takeaway: By 2026, instant payouts will transcend geography and scheme boundaries. Operators that integrate open-banking A2A APIs alongside card-network push rails will secure the most resilient payout infrastructure, one capable of meeting global compliance requirements while delighting players with true immediacy. Those waiting for regulatory mandates to force adoption risk falling behind competitors already marketing “instant” as their default standard.

Conclusion

By 2026, instant payouts will no longer be a differentiator; they will be an operational expectation across every regulated gaming market. What was once viewed as a “nice-to-have” for player experience has become a regulatory, technical, and reputational necessity. The convergence of SEPA Instant, PIX, UPI, and Faster Payments rails—combined with open-banking APIs and card-network push rails- has redrawn the boundaries of what “real-time” means for iGaming operators.

For Payment Mentors’ clients and partners, the message is clear: payout maturity equals brand maturity. Instant settlement capability now signals solvency, transparency, and compliance discipline, three pillars that underpin long-term merchant-acquirer relationships.

Why Payout Readiness Defines 2026

Real-time settlement has evolved beyond convenience. Regulators view it as a pillar of financial inclusion and risk mitigation. The European Commission (2025) considers instant payments the “default mode for euro transactions,” with equal pricing and real-time sanctions screening baked into law. In parallel, FATF and national AML bodies demand that every instant transaction be screened, logged, and auditable within milliseconds.

The implication is that speed and safety are now inseparable. Operators who can demonstrate “instant and compliant” processes will not only meet licensing thresholds but also unlock better acquisition terms, lower reserve ratios, and stronger player loyalty.

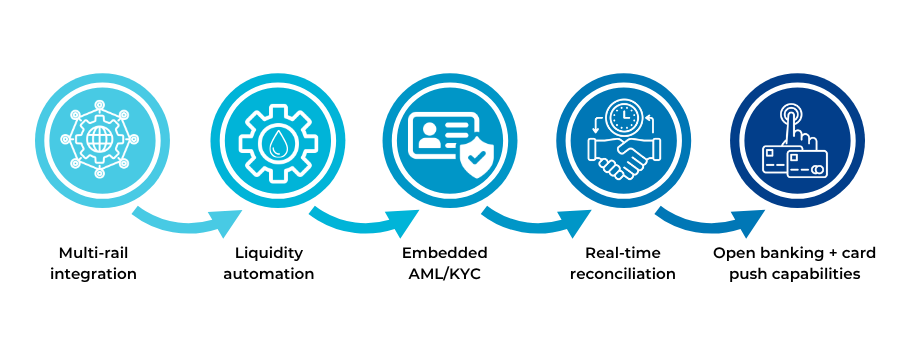

The 2026 Payout Readiness Checklist

- Multi-Rail Integration: Connect to at least two instant rails per key region (e.g., SEPA Instant + Faster Payments; PIX + Transfiya; M-Pesa + PAPSS) through a single orchestration API.

- Liquidity & Treasury Automation: Maintain prefunded wallets and real-time liquidity dashboards; automate replenishment to prevent payout interruptions.

- Embedded AML & KYC: Deploy machine-speed screening and name-matching tools integrated into each transaction flow; align with FATF and AMLD6 standards.

- Real-Time Reconciliation: Use ISO 20022 identifiers and vIBAN tokenisation to auto-reconcile every payout; maintain five-year digital audit trails as per EBA guidance (EBA, 2025).

- Open Banking and Card Push Capabilities: Offer both A2A and push-to-card options to maximise coverage, ensuring SCA and payer consent compliance under PSD3/PSR (European Commission PSD3 Proposal, 2025).

When these elements operate together, payout infrastructure transforms from a back-office function into a strategic loyalty engine, driving faster re-engagement, fewer disputes, and measurable lifetime-value uplift.

In a sector where reputation is built on trust, real-time payments are now the truest reflection of operational integrity. For 2026 and beyond, operators who align payout speed with compliance sophistication won’t just meet regulatory expectations; they’ll define the new standard of reliability in high-risk payments.

FAQs

1. What are instant payouts in iGaming?

Instant payouts are withdrawals processed via real-time payment rails such as SEPA Instant, Faster Payments, PIX, or UPI. They allow funds to reach players’ accounts within seconds, improving satisfaction and trust.

2. How do instant payouts improve player loyalty?

Instant withdrawals reduce uncertainty and create a sense of fairness. Players who receive winnings immediately are more likely to redeposit and stay loyal to the same operator. Studies by EGBA and FIS (2025) show up to a 40% increase in return sessions when payouts are instant.

3. Which payment rails support instant payouts globally?

The major instant-payment systems include SEPA Instant (EU), Faster Payments (UK), PIX (Brazil), UPI (India), and FedNow (US). Africa’s M-Pesa and PAPSS are also gaining traction for gaming payouts.

4. Are instant payouts compliant with AML and KYC rules?

Yes, but compliance must occur in real time. Regulations such as the EU’s Instant Payments Regulation (2025) and the FATF AML guidelines (2024) require live sanctions screening and name-matching before funds are released.

5. What are the main merchant benefits of instant payouts?

Faster liquidity cycles, reduced chargebacks, higher retention, and lower operational costs. Visa Europe (2024) found a 27% drop in disputes when merchants adopted instant-settlement rails.

6. What operational challenges come with instant payouts?

Key challenges include liquidity forecasting, real-time reconciliation, and ensuring API uptime. Operators must maintain prefunded accounts and automation for 24/7 payout readiness.

7. How can iGaming operators integrate instant-payment rails?

By working with PSPs offering multi-rail orchestration APIs that connect SEPA Instant, PIX, UPI, and card push systems under one compliance framework. This ensures consistent speed and AML control across regions.

8. What is the difference between open-banking payouts and card push payments?

Open-banking payouts send funds directly between bank accounts (A2A), while card push payments (like Visa Direct or Mastercard Send) route funds through card networks to debit accounts. Both are instant, but open banking offers lower costs and richer compliance data.

9. How do regulators oversee instant payments?

In Europe, the EBA and European Commission enforce real-time screening and IBAN-name matching. The UK’s Payment Systems Regulator (PSR) mandates Confirmation of Payee and liability for APP fraud reimbursement.

10. Do instant payouts reduce chargebacks and fraud?

Yes. Instant confirmation leaves little ambiguity about payment status, discouraging “friendly fraud.” Combined with name-matching and AML checks, they strengthen both merchant and acquirer defences.

11. How are LATAM and Africa leading instant-payment innovation?

Brazil’s PIX and Africa’s mobile-money integrations (e.g., M-Pesa, RPP) achieved mass adoption faster than Europe. Their mobile-first architecture allows real-time gaming payouts even in underbanked regions.

12. What future technologies will enhance instant payouts by 2026?

Open-banking payout APIs, tokenised credentials (vIBANs), and regtech-driven risk scoring. These innovations allow iGaming merchants to combine speed with continuous compliance.

13. What does Payment Mentors recommend for 2026 payout readiness?

Adopt a multi-rail payout strategy (SEPA, PIX, UPI), integrate embedded AML/KYC screening, automate liquidity management, and align with PSD3 + FATF guidance. Payment Mentors advises treating instant payouts as both a trust strategy and a compliance benchmark.