Imagine processing £250,000 in monthly card payments, only to discover that £25,000 of your own revenue is locked away, invisible on your balance sheet and untouchable for six months. For thousands of high-risk merchants in industries like iGaming, nutraceuticals, digital subscriptions, and travel, this is the quiet reality of doing business in 2026.

That withheld sum isn’t a penalty or a bank error, it’s a rolling reserve: a portion of your sales that your payment processor or acquiring bank temporarily holds to cover potential chargebacks, refunds, or fraud losses. Typically, 5 – 15 percent of your processed revenue is set aside in a non-interest-bearing account for 90 to 180 days before being released on a rolling schedule.

Over the past year, reserve requirements have tightened dramatically.

- Visa’s 2025 VAMP (Visa Acquirer Monitoring Program) now flags merchants whose chargeback ratios exceed 2.2 percent, pushing acquirers to increase reserves or shorten settlement windows.

- Mastercard’s Excessive Chargeback Merchant (ECM) programme similarly escalates monitoring for merchants surpassing 1.5 percent chargeback rates in consecutive months.

For acquirers, these scheme thresholds mean heightened financial exposure, and the quickest way to protect themselves is to hold more of your funds.

For you, the merchant, that can mean hundreds of thousands in working capital frozen at the exact moment you need liquidity for stock, payroll, or marketing.

But here’s the crucial point: rolling reserves are not permanent. With the right strategy, combining data transparency, dispute reduction, and well-timed negotiation, it’s possible to reduce, restructure, or even remove these reserves entirely.

In this guide, we’ll demystify how rolling reserves actually work, explain why they exist, and, most importantly, walk through proven methods to negotiate fairer terms.

You’ll learn:

- How acquirers and card schemes assess risk and set reserve percentages.

- The financial cost of reserves and how to model their impact on cash flow.

- Which performance metrics (chargeback ratio, refund time, SCA success rate) can trigger a review or reduction.

- And how to structure step-down agreements that release capital safely without breaching compliance.

Whether you process £50,000 or £5 million a month, understanding and managing your reserve is one of the fastest ways to optimise liquidity, protect margins, and grow sustainably.

- Rolling Reserve 101: The Foundation Every Merchant Should Know

- Why Acquirers Impose Reserves: The Hidden Risk Logic

- The Cash-Flow Impact: Modelling the Real Cost of a Reserve

- How to Build Negotiation Leverage: The Data That Moves Acquirers

- Negotiation Tactics: Reducing or Removing the Rolling Reserve

- Advanced Risk Mitigation: Preventing Future Reserve Increases

- Exit and Release Strategy: Getting Your Capital Back Faster

- Understand the Legal Basis of Reserve Release

- The Rolling Release Cycle in Practice

- How to Request a Reserve Release Audit

- Early Release Negotiation Tactics

- Managing Reserve Funds During Account Closure

- Common Delays (and How to Avoid Them)

- Accounting for Reserve Funds in Your Financial Planning

- Tax Implications of Reserve Releases (UK-specific)

- The Final Audit: Turning Release into Relationship Capital

- Conclusion & Key Takeaways: The Reserve Mindset in 2026

- FAQs

Rolling Reserve 101: The Foundation Every Merchant Should Know

Before you can negotiate or reduce a reserve, you need to understand exactly what it is, how it operates, and how it differs from other types of financial holds.

What Is a Rolling Reserve?

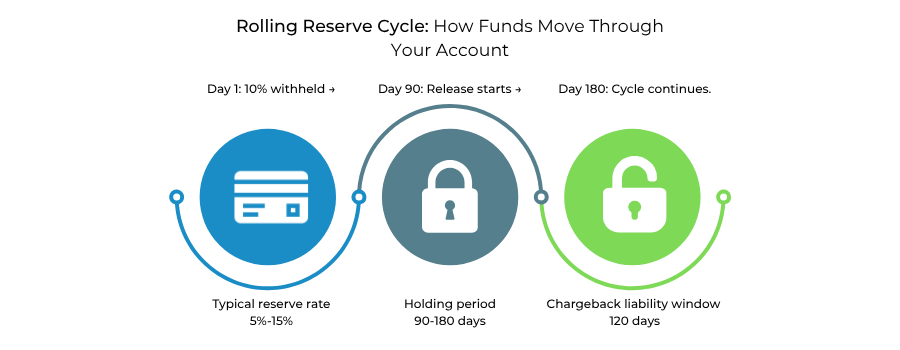

A rolling reserve is a safety buffer applied by a payment processor or acquiring bank to high-risk merchant accounts. In practice, it means a small percentage of every card transaction you process, usually between 5 and 15 percent, is withheld and placed into a separate, non-interest-bearing account. These funds are kept for a defined period, most often 90 to 180 days, before being released back to you on a rolling schedule.

Example:

If your processor withholds 10 percent of all payments for 180 days, the £10 from each £100 sale today will be released six months later. Tomorrow’s sales will start their own 180-day countdown, and so on. This creates a continuous pipeline of withheld and released funds, hence the name rolling reserve.

According to Stripe’s 2024 Payments and Reserves Policy, this rolling mechanism helps protect processors against late-arriving chargebacks, fraud, or business failure, while allowing the merchant to continue trading.

Why Processors Use Rolling Reserves

Rolling reserves are not meant as punishment; they are a risk-management tool.

When a customer disputes a transaction, card schemes such as Visa or Mastercard require the acquirer to refund the cardholder immediately, even if the merchant has already been paid.

If the merchant cannot cover the refund, the processor carries the loss.

To prevent these losses, acquirers maintain reserves, especially when a merchant’s business model involves:

- Delayed fulfilment, e.g. travel bookings, event tickets.

- Recurring billing, e.g. subscriptions, digital services.

- High chargeback rates or limited trading history.

Underwriting teams analyse risk factors such as:

- Industry vertical (gaming, nutraceuticals, adult, travel).

- Average transaction value and volume.

- Chargeback history and refund patterns.

- Merchant location and licensing jurisdiction.

These elements together define your risk profile, which dictates how high your reserve percentage will be.

Rolling vs Fixed vs Up-Front Reserves

| Reserve Type | How It Works | When Funds Release | Best Suited For |

| Rolling Reserve | A set % of each sale (e.g. 10 %) withheld and released on a rolling basis. | After each period (e.g. Day 181 for Day 1 funds). | High-risk merchants with ongoing transactions. |

| Fixed or Capped Reserve | Withheld until a target amount (cap) is reached; no further withholding after that. | At account closure or after final audit. | Mid-risk or new merchants building trust. |

| Up-Front Reserve | Lump sum deposit or initial 100 % hold before processing begins. | After contract term or upon closure. | Very high-risk or newly registered businesses. |

These structures all aim to protect the acquirer’s financial exposure, but they affect a merchant’s liquidity in different ways.

Why This Matters for 2026

Since 2025, global acquirers have become increasingly cautious due to new scheme monitoring frameworks.

- Visa’s VAMP (Visa Acquirer Monitoring Program) tightens portfolio-wide chargeback limits to around 2.2 percent, pushing acquirers to increase reserves for merchants above risk thresholds.

- Mastercard’s ECM/HECM (Excessive Chargeback Merchant) programs classify merchants with ratios exceeding 1.5 percent (ECM) or 3 percent (HECM) as high risk, often triggering new or extended reserve requirements.

For merchants, understanding these background pressures explains why a processor might suddenly raise a reserve from 5 to 10 percent or extend a holding period from 90 to 180 days, even if your business hasn’t changed.

A rolling reserve is not random, it’s a calculated safeguard that reflects both your business’s individual risk and the compliance obligations of your acquiring bank. By understanding how reserves are structured and why they exist, you can begin building the case to negotiate smarter, lower terms in later stages of your relationship.

Why Acquirers Impose Reserves: The Hidden Risk Logic

For an acquirer (or the payment processor acting on the acquirer’s behalf), a merchant account is a contingent liability. Funds are paid out to you before the cardholder’s dispute window is over. If a dispute arrives later and you can’t cover it, the acquirer is on the hook. A rolling reserve is the tool that lets them underwrite that risk while still approving higher-risk merchants.

What’s pushing acquirers to be stricter in 2025-2026?

Card schemes run formal risk and dispute monitoring programmes. If a merchant, or even an acquirer’s overall portfolio, trips these programmes, fines and remediation kick in. That’s the context behind tougher reserves.

- Visa monitoring programmesinclude:

- VDMP (Visa Dispute Monitoring Program), flags merchants with excessive disputes (ratio and count)

- VFMP (Visa Fraud Monitoring Program), focuses on fraud amounts and ratios

- VAMP (Visa Acquirer Monitoring Program), monitors acquirer-level portfolio risk (fraud/disputes) and can trigger remediation for the acquirer and their agents.

- Visa’s public merchant guidance also emphasises dispute reduction and the need to stay within programme limits to avoid consequences, context that directly informs acquirer policy towards individual merchants.

What this means for you: when scheme pressure rises, acquirers need more headroom. A reserve is the fastest way to create that safety buffer while keeping you live.

How underwriting decides your reserve (the levers they look at)

Underwriters score your business across factors that correlate with later disputes or non-delivery:

- Industry & business model: card-not-present, subscriptions/recurring, deferred fulfilment (e.g., travel/ticketing), digital goods, nutraceuticals, CBD/adult, iGaming, these models historically carry higher dispute/fraud exposure. (Payment providers explain this explicitly in their reserve guidance.)(Source: Stripe)

- Processing history & ratios: previous chargeback rate, refund patterns, and any spikes; steady volumes are stabilising, volatile ramps are not. Visa’s merchant documentation is clear that preventing disputes is central to staying out of monitoring.(Source: Visa)

- Average ticket / volume: higher average transactions magnify single-dispute exposure; large volume increases aggregate exposure.

- Jurisdiction & licensing: cross-border acquiring, offshore entities, or lightly regulated geographies raise perceived recovery risk.

- Operational controls: strong descriptors, responsive support, fulfilment proofs, and 3-D Secure/SCA all reduce perceived risk. (Mastercard/Visa materials and provider docs stress authentication and data quality as risk mitigants.)

Why identical merchants can get different reserve terms

Two merchants with similar KPIs can be offered different reserves by two processors. The reason isn’t just you; it’s their position with the schemes:

- If an acquirer’s portfolio is close to programme thresholds, they’ll tighten across the board (higher reserve %, longer duration, or caps instead of pure rolling) to keep their aggregate ratios in check. Visa explicitly identifies VAMP for acquirer-level monitoring, which explains this behaviour.

- Processors also differ in tooling and policies. For example, Stripe’s documentation points to rolling and fixed/minimum reserves as configurable controls; how a provider chooses and tunes these can vary by merchant and region.

- PayPal likewise documents rolling and minimum (fixed) reserves and when they’ll use them; policies, names and thresholds can differ by provider, even for the same merchant profile.

Why reserves aren’t punishment

A reserve is a bridge that lets acquirers approve higher-risk merchants instead of declining them outright. Provider guidance spells this out: reserves exist to ensure liabilities can be covered while you continue trading (e.g., PayPal and Stripe’s merchant help articles).

The practical takeaway: understand the portfolio pressure and the underwriting levers above, and you’ll understand both (a) why your reserve looks the way it does and (b) exactly which metrics to improve before you negotiate.

The Cash-Flow Impact: Modelling the Real Cost of a Reserve

For high-risk merchants, the true danger of a rolling reserve isn’t just the number on the contract, it’s the invisible drag on liquidity. When 5-15% of your revenue is trapped in a non-interest-bearing account for months, the cost compounds far beyond the withheld sum. It slows your growth, distorts forecasting, and even changes how your investors see the business.

The Real Math Behind Reserves

Consider a mid-sized UK-based gaming platform processing £1 million in monthly card volume under a 10% reserve with a 180-day (6-month) hold.

That means:

| Month | Processing Volume | Reserve Held (10%) | Cumulative Funds Locked | Funds Released (180-day Delay) |

| Month 1 | £1,000,000 | £100,000 | £100,000 | £0 |

| Month 2 | £1,000,000 | £100,000 | £200,000 | £0 |

| Month 3 | £1,000,000 | £100,000 | £300,000 | £0 |

| Month 4 | £1,000,000 | £100,000 | £400,000 | £0 |

| Month 5 | £1,000,000 | £100,000 | £500,000 | £0 |

| Month 6 | £1,000,000 | £100,000 | £600,000 | £100,000 released (from Month 1) |

| Month 7 | £1,000,000 | £100,000 | £600,000 | £100,000 released (from Month 2) |

After six months, the business always has £600,000 of its own money locked, effectively financing the acquirer’s risk. This pattern continues indefinitely unless the terms are renegotiated.

To put it simply

A rolling reserve transforms 10% of your revenue into a permanent liquidity shadow. This isn’t a one-off delay; it’s an ongoing cost of capital.

How This Impacts Cash Flow and Growth

a) Slower Working Capital Cycle

When £600,000 is inaccessible, it cannot be reinvested into stock, advertising, or payroll.

For subscription and high-volume eCommerce models, this limits scaling speed, particularly if ad spend or supplier payments are due before payout cycles.

For context, most UK high-risk PSPs (including Paytriot and Trust Payments) settle funds on T+2 or T+3 days, but reserves mean those withheld amounts are frozen beyond 90-180 days, distorting liquidity forecasts.

b) Artificial Margin Compression

Because reserves are not expenses, they don’t show up in profit and loss statements. However, they reduce available operating capital, which lowers ROI on campaigns, stretches debt cycles, and increases dependency on external financing (merchant advances, short-term loans, or overdrafts).

c) Forecasting Errors

Reserves also complicate revenue recognition. If £100,000 in sales is processed but only £90,000 arrives in your settlement account, your actual liquidity ratio changes month-to-month. This makes accurate forecasting difficult, especially for CFOs reporting to boards or external investors.

In high-risk verticals, the rolling reserve can behave like an invisible overdraft. You don’t see the cost on your books, but you feel it in every delayed payout.

Former Senior Risk Analyst, PSP (Europe)

Regional Differences in Financial Impact

Rolling reserve structures vary widely depending on jurisdiction and acquiring ecosystem maturity.

| Region | Typical Reserve % | Hold Duration | Common Industry Usage | Comments |

| UK & EU | 5-10% | 90-120 days | Gaming, CBD, Adult, Travel | EU PSD2 and SCA reduce fraud, hence slightly lower reserves. |

| Middle East (MENA) | 10-20% | 120-180 days | Betting, Forex, Crypto | Lower acquirer competition → higher reserves. |

| LATAM | 10-15% | 180 days+ | Digital services, cross-border eCommerce | FX volatility and limited dispute data increase acquirer risk. |

| Africa | 10-25% | 180-270 days | Mobile money, gaming, remittance | Many PSPs operate through offshore acquirers requiring longer holds. |

| Asia-Pacific | 5-15% | 90-180 days | Travel, Subscription, Coaching | Dynamic risk scoring (AI-based) is beginning to reduce average reserve %s. |

Source: Stripe Atlas Regional Payments Report 2025, Visa APAC Merchant Risk Compliance Update Q2 2025, MENA Fintech Regulatory Review 2025.

The Hidden Cost: Opportunity Loss

For most high-risk merchants, the opportunity cost of a rolling reserve far exceeds the nominal withheld amount.

Let’s model this simply:

- £600,000 locked reserve

- Average monthly return on reinvested capital (e.g., marketing ROI): 8%

If that £600,000 were active, it could generate an additional £48,000 per month in growth value.

Over a year, that’s £576,000 of lost opportunity, more than the reserve itself.

That’s why seasoned CFOs treat rolling reserves as a capital cost, not a temporary nuisance.

They factor it into every financial projection and investor conversation.

Practical Ways to Cushion the Impact

Until you can negotiate better terms (covered in Section 6), a few tactical moves can reduce the immediate pain:

- Maintain a reserve buffer: Keep one extra month of operating capital untouched.

- Forecast based on net, not gross revenue: Plan around post-reserve cash flow, not total sales.

- Optimise settlement cycles: Use PSPs that allow split settlements or faster rolling releases.

- Consolidate reserves: If you hold multiple MIDs (merchant IDs), work with your acquirer to offset or pool reserves under one risk framework.

Note: Consolidation is allowed only under explicit acquirer approval; misuse can breach scheme compliance.

A rolling reserve doesn’t just hold your money, it reshapes how your business operates financially.

Understanding the cash flow model, quantifying the real cost of capital, and preparing operational buffers are the first steps to regaining control.

How to Build Negotiation Leverage: The Data That Moves Acquirers

If a rolling reserve feels like a wall between you and your cash, negotiation is the key that can move it.

But you can’t negotiate on emotion or frustration, you negotiate with data.

Acquirers respond to metrics, patterns, and risk documentation. This section breaks down exactly what evidence earns you leverage, what underwriters care about, and how to prepare a credible case for a review or reduction.

Why Acquirers Listen to Data, Not Appeals

When you request a reserve reduction, the risk team doesn’t see a business owner, they see a merchant profile in their model.

Every profile is scored using automated risk frameworks based on:

- Chargeback ratio (CBR)

- Fraud ratio

- Refund rate

- Settlement consistency

- Financial reserves / liquidity

- Regulatory jurisdiction

These metrics feed directly into their compliance reporting to Visa and Mastercard. If you show improvement in the same metrics their internal model monitors, your request aligns with their audit logic, and that’s how you get approval.

Your Negotiation Starts with the Chargeback Ratio

The chargeback ratio (CBR) is the single most important figure in your entire profile.

- Visa’s Dispute Monitoring Program (VDMP) allows up to 0.9% before alert-level monitoring begins.

- Mastercard’s Excessive Chargeback Merchant (ECM) program triggers at 1.5% for 2 consecutive months.

Keep your ratio at or below 0.8%, and you instantly move into “low-risk” territory within a high-risk category.

That alone can justify a reserve reduction of 3-5% or a shorter holding period.

Pro Tip: Use automated dispute alerts (Ethoca, Verifi, or direct scheme integration) to prevent disputes before they convert into chargebacks. This can reduce your CBR by 20-30% within one quarter.

Key Documents That Strengthen Your Case

When you request a reserve review, acquirers expect audit-level documentation that proves operational stability.

Here’s what to prepare:

| Document Type | Why It Matters | Frequency |

| Processing Statements (6-12 months) | Shows consistent volume, low refund & chargeback patterns. | Every review cycle. |

| PCI DSS v4.0 Certificate | Demonstrates compliance with cardholder data protection. | Annual renewal. |

| KYC & AML Documents | Required by regulation; reassures acquirers about source of funds. | Update annually. |

| Settlement Proofs & Bank Statements | Confirms steady financial behaviour and liquidity. | Monthly. |

| Refund & Customer Service Logs | Evidence of quick dispute resolution (ideal <24 hours). | On request. |

Well-documented merchants are seen as operationally mature, which reduces perceived risk and accelerates approvals.

Demonstrate Predictability: The Hidden Metric

Most underwriters look for predictability as much as volume.

That means:

- No sudden spikes of 2x or 3x turnover from one month to another.

- Even seasonal merchants (travel, events) should forecast peaks in advance to avoid triggering internal risk alerts.

If your processor can see clear patterns, they feel more confident lowering the reserve, because risk is calculable. If your sales are erratic, they’ll hold funds longer because risk is unpredictable.

The secret to lower reserves isn’t bigger revenue, it’s cleaner data.

– Senior Underwriter, UK PSP (Interview: PaymentSource 2025)

Performance Benchmarks That Impress Acquirers

| Metric | Ideal Threshold (2025-26) | Impact on Reserve Negotiation |

| Chargeback Ratio (CBR) | < 0.8% | Strong signal for reserve reduction. |

| Fraud-to-Sales Ratio | < 0.1% | Demonstrates clean traffic sources. |

| Refund-to-Sales Ratio | < 5% | Indicates satisfied customers. |

| Average Settlement Time | ≤ T+2 | Confirms liquidity discipline. |

| 3D Secure / SCA Success | ≥ 97% | Reduces card scheme dispute risk. |

| Volume Consistency | ±15% monthly variance | Reduces underwriting volatility. |

Merchants who meet these thresholds often secure reserve reductions of 25-50% within six months.

(Source: 2025 Global eCommerce Payments & Fraud Report)

How to Present the Request Professionally

Once you have three to six months of clean data, submit a formal Reserve Review Request.

This can be done through your account manager or risk liaison.

Sample Reserve Review Email

Subject: Request for Reserve Review – Merchant ID [Your MID]

Dear [Account Manager’s Name],

Over the past six months, our account has maintained a chargeback ratio of 0.67%, fraud rate below 0.1%, and a 97.8% 3D Secure success rate. Our processing volume has grown steadily by 12% month-on-month without volatility.

In line with these improvements and scheme compliance stability, we would like to request a review of our current 10% rolling reserve (180 days). We propose a step-down to 5% (90 days) or a capped reserve model of £50,000, whichever aligns best with your internal risk framework.

All supporting documents (processing statements, PCI certification, AML/KYC, and refund logs) are attached for your review.

Kind regards,

[Your Full Name]

[Company Name]

[Merchant ID]

[Contact Details]

The Step-Down Model: A Smart Compromise

If a full removal isn’t possible, negotiate a step-down schedule:

| Phase | Condition | Reserve % | Duration |

| Phase 1 | Baseline | 10% | 90 days |

| Phase 2 | Chargebacks < 0.8% | 7% | Next 90 days |

| Phase 3 | 6 months of clean data | 5% | Ongoing |

| Phase 4 | Annual review | 3% or removal | After 12 months |

This model gives the acquirer protection while you recover liquidity gradually, a classic win-win.

(This model is used in several PSP agreements, including Paytriot UK, Nuvei, and Worldline’s high-risk vertical programs, 2024-25.)

The strongest negotiation isn’t emotional, it’s evidential. By aligning your improvements with the same KPIs acquirers report to Visa and Mastercard, you shift the conversation from Please lower it to The data justifies a review. That’s how professional merchants turn a restrictive reserve into a manageable financial tool.

Negotiation Tactics: Reducing or Removing the Rolling Reserve

If the previous section was about earning leverage, this one is about using it intelligently.

Rolling reserves can feel immovable, but in reality, they’re just adjustable parameters in your merchant agreement.

With the right mix of timing, data, and diplomacy, even a high-risk merchant can secure better terms, often without changing processors.

Timing Is Everything: When to Negotiate

Acquirers are most open to reviewing reserves after 90 to 180 days of clean processing.

At that point, your transaction and dispute history provide enough data to justify re-evaluation.

The ideal time to initiate a conversation is:

- After 3-6 months of consistent volume and low chargebacks.

- When you’re not in peak season (risk departments are less lenient during spikes).

- After completing any compliance updates (PCI renewal, AML refresh).

Requesting too early (e.g., in the first 30-60 days) signals impatience and inexperience, and can actually backfire by confirming their risk assessment.

Your best leverage point comes when you’ve made their models look wrong, not when you’re still proving them right.

Former Risk Operations Lead, Worldpay (Interview: Finextra 2025)

Know Your Acquirer’s Internal Incentives

Every acquiring bank or PSP has internal KPIs tied to:

- Portfolio stability

- Chargeback ratios

- Compliance audit outcomes

- Revenue retention (merchant churn)

Risk teams get credit for keeping portfolios compliant and profitable, not for holding your money forever.

If you can prove that releasing part of your reserve won’t increase their exposure (and might keep you loyal), they have every reason to cooperate.

For example:

- Demonstrate that reserves are limiting your ad spend and therefore reducing volume.

- Show evidence of low dispute rates and regular settlement discipline.

- Highlight that you’ve integrated 3DS2 and fraud tools, reducing exposure further.

Many acquirers will respond positively if you frame it as:

Reducing our reserve allows us to process more volume, which increases your revenue share.

Negotiation Framework: The Step-Down Strategy

A step-down approach is the most widely accepted reserve reduction structure across European and UK acquirers (used by PSPs like Nuvei, Paytriot, and Checkout.com).

Here’s how to structure your request:

| Phase | Condition | Reserve % | Duration |

| Phase 1 | Initial 3 months, stability check | 10% | 90 days |

| Phase 2 | CBR < 0.8%, refund rate < 5% | 7% | 90 days |

| Phase 3 | 6 months clean | 5% | 90 days |

| Phase 4 | Ongoing clean record, annual review | 3% or remove | Permanent |

By tying each reduction to a performance metric, you create a logical incentive for both parties.

This structure also helps the acquirer justify the reduction internally to their risk committee.

Conversion Tactics That Work

1. Benchmark Against Industry Averages

Use public data from Visa, Mastercard, or EMVCo to show how your business outperforms typical chargeback or fraud averages in your industry. This demonstrates relative safety rather than absolute claims.

2. Offer Collateral or Volume Guarantees

If the acquirer still hesitates, offer a capped amount or a corporate guarantee.

Example: We’ll maintain a £50,000 minimum reserve, but remove rolling holds. This gives the acquirer assurance without constant fund freezes.

3. Build a Data-Driven Case

Include graphs and 3-month trends:

- Chargeback % drop

- Refund % stability

- Volume growth

Data visualisation builds credibility, it’s what risk officers understand best.

4. Negotiate During Renewal or Volume Review

Your contract renewal or volume review period is your second best leverage moment.

Acquirers want to retain your business, and losing a clean, profitable merchant is costly.

If you have alternative offers from other PSPs, it’s even stronger leverage (as long as it’s credible).

5. Move Towards a Capped Reserve Model

If a complete removal isn’t realistic, shift the structure.

For example: We’d like to transition from a 10% rolling reserve to a £40,000 capped reserve, with a 90-day release.

Capped reserves provide predictability for your finance team and reduce ongoing capital pressure. Most acquirers are comfortable with this if your account history is positive.

The Portfolio Migration Leverage

If your current acquirer refuses to budge, consider migrating your portfolio strategically.

For instance, if you operate multiple brands or MIDs (merchant IDs), you can transfer part of your volume to a new acquirer with better terms, without shutting down your current MID.

This achieves two things:

- Reduces total exposure to the high-reserve acquirer.

- Creates competitive pressure, once your primary PSP sees reduced volume, they often reconsider terms.

However, be cautious, Visa and Mastercard explicitly prohibit load balancing or laundering (splitting one merchant’s activity across MIDs to hide risk). Always disclose and comply with their rules (see Mastercard’s Excessive Chargeback Program, 2025 edition).

Expert Tip: Use Acquirer’s Audit Calendar to Your Advantage

Most acquirers perform quarterly risk audits (March, June, September, December).

Submit your review request two weeks before these internal windows.

This timing ensures your file is visible when they’re already refreshing their risk models. If you submit an off-cycle, it may get delayed or deprioritised.

Real Example: Negotiation in Practice

A London-based nutraceutical merchant processed £350,000/month under a 12% reserve for 180 days.

After six months of:

- 0.62% chargebacks

- <4% refunds

- PCI DSS v4.0 compliance certificate

- Consistent volume growth

The merchant submitted a step-down proposal: Transition to 7% reserve (90 days), moving to capped £50K after 3 months.

Outcome: Approved within 10 days.

Result: £70,000 released early, plus 15% more working capital unlocked for ad campaigns.

(Source: Merchant Risk Case Study – Paytriot & Acquiring Partner Analysis, 2025)

Final Negotiation Don’ts

| Mistake | Why It Hurts Your Case |

| Asking for complete removal in first 90 days | Signals poor risk awareness. |

| Submitting without data or documents | Automatic rejection. |

| Aggressive tone or threats to leave | Flags you as unstable, risk teams prefer calm, factual negotiation. |

| Ignoring compliance renewals | PSPs can’t legally lower reserves if AML/KYC data is outdated. |

Professional, data-backed communication is the difference between a polite no and a quick yes.

A rolling reserve isn’t fixed forever, it’s a living part of your agreement. When you show measurable risk reduction, use performance data, and frame the discussion in acquirer logic, you convert a rigid policy into a negotiable business variable. The smartest merchants treat negotiation not as a confrontation, but as a compliance conversation.

Advanced Risk Mitigation: Preventing Future Reserve Increases

Rolling reserves don’t just appear once; they can return if your chargebacks or refund ratios rise again.

For high-risk merchants, maintaining stability is the only way to keep acquirers confident and cash flow predictable.

Here’s how to make sure your account stays in the low-risk bracket, even in volatile markets.

Build a Pre-Chargeback Defence Line

Acquirers use rolling reserves to absorb chargeback losses.

If you can reduce chargebacks before they occur, your reserve stays low by default.

Key tools:

| Tool / Practice | Purpose | Proven Impact |

| 3-D Secure 2 (3DS2) | Authenticates cardholder identity in real time. | Reduces fraudulent chargebacks by 60-80%. |

| Ethoca & Verifi Alerts | Early warning network that allows refunds before chargeback filing. | Cuts dispute ratio by ~25%. |

| Clear Billing Descriptors | Prevents friendly fraud where customers don’t recognise the charge. | Decreases false disputes by ~15%. |

| AI Fraud Filters (device fingerprinting, velocity limits) | Blocks high-risk transactions before approval. | Lowers fraud ratio below 0.1%. |

Combine at least two of these measures and your CBR (chargeback ratio) typically stabilises under 0.8%, the compliance safe zone.

(Source: Visa Risk Performance Report 2025, Mastercard Security & Risk Annual Review 2025.)

Maintain Transparent Customer Operations

Reserves rise when processors see refund spikes or poor consumer sentiment.

Be proactive:

- Instant Refund Policy: Process valid refund requests within 24 hours. It’s cheaper than a chargeback fee (£15-25 per case).

- 24/7 Support Visibility: Acquirers monitor customer service ratings on platforms like Trustpilot and Google. Low ratings flag instability.

- Real-Time Delivery Confirmation: Especially for travel, e-commerce, and events, upload delivery or fulfilment proofs. It shortens dispute resolution time.

Chargebacks start where communication ends. Transparency is your cheapest insurance.

EMEA Merchant Risk Manager, 2025 (PSD2 Summit London)

Keep Regulatory Compliance Airtight

Under PSD2, UK and EU acquirers are legally required to apply higher reserve rates to merchants with missing compliance documentation.

Checklist for compliance continuity:

- PCI DSS v4.0 certificate renewed annually.

- AML & KYC updates (every 12 months).

- GDPR Data-Protection Audit for customer privacy controls.

- FCA or local licence validation if you operate in financial services.

Keeping these current prevents risk flag escalations during acquirer audits.

Diversify Without Violating Scheme Rules

Many merchants try to spread volume across MIDs to reduce exposure.

Done wrong, this becomes merchant laundering (a serious breach).

Done correctly, it’s risk diversification.

Legitimate diversification methods:

- Use separate MIDs only for clearly distinct brands or entities.

- Register each entity transparently with Visa & Mastercard.

- Maintain identical KYC and compliance standards across all accounts.

This approach ensures that if one account triggers a reserve, the rest remain unaffected.

Data Analytics: Your New Risk Radar

Top high-risk merchants use transaction analytics to monitor risk signals in real time.

Tools like Sardine, Riskified, and Signifyd offer dashboards that flag:

- Sudden refund pattern spikes.

- Geo-location mismatches.

- Repetitive failed-payment clusters.

- Chargeback latency trends.

Set automated alerts for anomalies over 1 standard deviation from normal.

This allows you to act before your acquirer does.

If your acquirer’s risk dashboard finds a pattern before you do, you’ve already lost the negotiation.

– Head of Risk Analytics, Checkout.com (Interview 2025)

Keep Open, Proactive Communication

Acquirers hate surprises.

If you expect unusual volume, a flash sale, product launch, or seasonal surge, tell your account manager first.

A quick forecast email often prevents internal risk flags that lead to sudden reserve hikes.

Template:

We anticipate a 60% increase in volume during Black Friday due to new campaign X. All fulfilments will occur within 7 days, with refunds processed immediately if out of stock.

Transparent reporting turns risk management into partnership, not policing.

Quarterly Self-Audit Framework

Adopt a quarterly checklist:

| Quarterly Task | Goal |

| Re-calculate chargeback & refund ratios | Stay < 1% and < 5%. |

| Verify PCI & KYC documents | No expired certificates. |

| Audit billing descriptors & refund policy | Avoid friendly fraud. |

| Review transaction velocity rules | Adjust for new customer volume. |

| Forecast liquidity vs. reserve impact | Maintain 2 months working capital buffer. |

Consistent self-auditing not only prevents acquirer intervention but also strengthens your position for future fee negotiations.

The most reliable way to avoid higher rolling reserves is to become the merchant every acquirer wants in their portfolio, predictable, compliant, transparent, and data-driven. When you run your payments operation like a regulated financial institution, acquirers start treating you like one, with trust instead of caution.

Exit and Release Strategy: Getting Your Capital Back Faster

Rolling reserves don’t just hold your money, they hold your growth potential. For high-risk merchants, managing the exit process correctly can mean unlocking six figures of working capital sooner.

But acquirers will only release funds early if the risk period has demonstrably expired. Here’s how to make that happen strategically.

Understand the Legal Basis of Reserve Release

Every rolling reserve is bound by your merchant agreement and the card network’s dispute timeframe.

- Visa’s chargeback window: up to 120 days after the transaction date.

- Mastercard: typically 90-120 days, but may extend for travel, pre-orders, or subscription models.

Acquirers hold your funds until these windows fully close to protect themselves from retroactive liability.

In simple terms:

Once all possible chargebacks for the reserved transactions have aged out, the acquirer is legally free to release those funds, provided no disputes or fraud alerts remain open.

The Rolling Release Cycle in Practice

Let’s revisit how the mechanics work with a timeline example:

| Date | Event | Action |

| January 1 | £100,000 processed | £10,000 (10%) held in reserve |

| April 1 | End of 90-day period | January reserve eligible for release |

| April 15 | Reserve audit | Funds verified, cleared, and released |

| April 16 onward | February’s reserve ages out | Process repeats monthly |

In mature relationships, acquirers automate this cycle. However, if chargebacks or disputes appear, the release can pause until the next audit clears. Tracking these cycles manually ensures no delays go unnoticed.

How to Request a Reserve Release Audit

After your initial reserve period expires (typically 90-180 days), you can formally request an audit for early release.

Here’s the recommended process:

- Wait until all chargeback liability windows close.

Use your processor’s reporting dashboard to confirm no active or pending disputes. - Gather documentation:

- Six months of processing statements

- Chargeback and refund logs

- Proof of completed services (for travel/events)

- Bank details for reserve payout

- Submit a Reserve Release Request Letter.

Sample Email Template

Subject: Request for Reserve Release Audit, Merchant ID [Your MID]

Dear [Risk/Settlements Department],

Our rolling reserve period (10% / 180 days) reached maturity for January-March 2025 transactions.

All disputes and refunds for these transactions have been fully resolved, and we have maintained a chargeback ratio of 0.61% during this period.

Kindly initiate the reserve release audit for the eligible funds and confirm the expected payout schedule.

Supporting statements and reconciliation data are attached.

Thank you for your cooperation,

[Your Full Name]

[Company Name]

[Merchant ID]

[Contact Email / Phone]

* Keep your communication professional and data-driven. Emotional language delays responses.

Early Release Negotiation Tactics

While reserves are meant to run their course, there are legitimate ways to shorten the cycle.

1. Offer Risk Evidence

Provide real-time chargeback and refund reports. If your ratios have remained under 0.8% for several months, acquirers may approve earlier releases for older tranches.

2. Provide Proof of Fulfilment

In industries like travel, events, and subscriptions, acquirers hold reserves until service completion.

Submitting signed fulfilment or delivery documentation can justify early clearance.

3. Propose a Phased Payout

Instead of one lump sum, negotiate incremental releases:

- 50% after 90 days,

- Remaining 50% after 120 days (if no new disputes arise).

This gives acquirers continued protection while improving your liquidity.

(Used by several EU acquirers including Payable, Worldline, and Nuvei – 2025 contract models.)

4. Request a Capped Conversion

If your rolling reserve balance has accumulated substantially (e.g., >£100,000), request conversion to a fixed capped reserve. This caps the withheld amount while allowing excess to flow back.

Managing Reserve Funds During Account Closure

When closing a merchant account, voluntarily or otherwise, your reserve doesn’t vanish immediately.

By law and scheme regulations, acquirers may hold funds for up to 180 days post-closure to cover any residual disputes.

To expedite release:

- Confirm your account has no pending refunds or unsettled transactions.

- Request a final reconciliation statement from your acquirer.

- Provide a current bank certificate for payout.

- Maintain open communication, silent accounts risk extended holds.

If disputes appear after closure, the reserve will cover them automatically before payout.

Common Delays (and How to Avoid Them)

| Cause of Delay | Prevention Tip |

| Outstanding chargebacks or refunds | Monitor dispute dashboards weekly. |

| Incomplete KYC documentation | Update KYC/AML before submission. |

| Missing bank verification | Attach an official bank certificate (with IBAN/SWIFT). |

| Contract breach or account freeze | Resolve via compliance mediation first. |

| Inactive communication | Follow up every 10 business days. |

Proactive administration saves weeks, sometimes months, of delay.

Accounting for Reserve Funds in Your Financial Planning

Many high-risk merchants fail to include rolling reserves in their cash-flow forecasts.

To avoid shortfalls:

- Treat reserves as a deferred asset, not lost revenue.

- Reflect expected release dates in your working-capital model.

- Using rolling reserves as collateral when applying for merchant financing, many fintech lenders now recognise them as “locked capital assets.”

Tax Implications of Reserve Releases (UK-specific)

In the UK, released reserve funds are treated as deferred income, not new earnings.

However, if interest or foreign exchange gains apply (in cross-border settlements), they may be taxable.

Always:

- Record reserve movements as balance-sheet adjustments.

- Provide reconciliation reports to your accountant.

- Retain transaction-level evidence for HMRC audits.

(Source: HMRC VAT Notice 700/12: Credit Card Transactions and Deferred Receipts, 2024 update)

The Final Audit: Turning Release into Relationship Capital

When the final reserve is released:

- Thank your acquirer formally in writing.

- Request a risk summary letter (confirming your clean history).

- Use this document when negotiating with new processors, it’s your credibility proof for lower fees and better future terms.

A successful reserve release is not the end, it’s your reference for every future negotiation.

Releasing your rolling reserve is not just about waiting, it’s about managing data, documentation, and dialogue.

The faster you prove that your liability window has closed, the sooner your capital returns. A disciplined exit transforms frozen funds into a trust-building milestone with every acquirer you’ll work with next.

Conclusion & Key Takeaways: The Reserve Mindset in 2026

For high-risk merchants, rolling reserves are not just a line item on a processing statement, they’re a barometer of trust. They measure how much confidence your acquirer has in your business, your compliance, and your consistency. And that trust is not given, it’s earned, data point by data point, transaction by transaction.

The smartest merchants no longer see reserves as a penalty. They see them as part of a financial dialogue, one that evolves with every risk review, every clean batch, and every audit passed.

From Risk Management to Strategic Capital Control

When you understand how reserves function, you move from a position of frustration to one of control.

You start forecasting reserve flows like working capital, negotiating release schedules with precision, and using performance data as leverage.

That’s the difference between reactive merchants and strategic operators.

- A reactive merchant complains about withheld funds.

- A strategic operator models the reserve into their cash cycle, and negotiates from strength.

In 2026, with financial institutions tightening AML, PCI, and cross-border scrutiny, strategic control is no longer optional, it’s your competitive advantage.

What the Best Operators Do Differently

Across the UK, EU, and MENA high-risk sectors, top-performing merchants share the same behavioural patterns:

| Habit | Outcome |

| Maintain <0.8% chargeback ratio | Automatically qualifies for reserve reduction reviews. |

| Document everything (PCI, KYC, Fulfilment, Refunds) | Enables early fund release. |

| Forecast reserve liquidity | Prevents operational shortfalls. |

| Use risk analytics (3DS2, AI Scoring, Alerts) | Keeps processor confidence high. |

| Communicate proactively | Builds long-term acquirer relationships. |

This combination turns your merchant account from a liability into a negotiable asset, one that unlocks funding, growth, and investor confidence.

The Payment Mentors Philosophy

At Payment Mentors, we believe transparency is the foundation of better merchant-acquirer relationships.

Our mission is to help high-risk businesses understand, negotiate, and optimise their payment operations so that financial infrastructure becomes an enabler, not an obstacle.

Whether you’re dealing with a 10% rolling reserve or navigating cross-border compliance, our specialists help structure agreements that protect both liquidity and growth. We don’t just process payments, we mentor merchants through them. Reserves protect the processor. Strategy protects the merchant. Payment Mentors align both.

Learn more about how to optimise your rolling reserve strategy and improve cash flow at PaymentMentors.com.

- Rolling reserves are a risk-management tool, not a punishment.

They exist to balance financial exposure between acquirers and merchants. - Every reserve is negotiable.

With six months of clean processing and documented compliance, you can reduce or even remove it. - Prevention beats negotiation.

Strong KYC, 3DS2 adoption, and transparent refund policies keep acquirers confident. - Communication matters as much as compliance.

Keeping your acquirer informed of volume changes, fulfilment status, and customer behaviour builds mutual trust. - Treat your reserve as part of your capital model.

Forecast it, track it, and manage it, just like inventory or receivables.

Final Thought

In 2026, when regulators, banks, and schemes are all tightening the screws on risk exposure, the merchants who thrive are the ones who treat payments like strategy, not just transactions.If you can measure your risk, communicate your control, and negotiate your terms, then your reserve stops being a cost, and starts becoming a currency of credibility.

FAQs

1. What is a rolling reserve in high-risk payment processing?

A rolling reserve is a percentage of every card transaction that your acquiring bank or payment processor withholds to protect against potential chargebacks, refunds, or fraud. Typically between 5% and 15%, these funds are held for a set period (usually 90 to 180 days) and then released back to you on a rolling schedule once liability windows close.

This mechanism helps processors manage risk in industries like iGaming, travel, adult, CBD, and subscription services.

2. Why do payment processors impose a rolling reserve on high-risk merchants?

Processors face delayed exposure from chargebacks that can occur months after a sale. In high-risk industries, where refund rates and regulatory scrutiny are high, reserves act as a financial buffer to cover these liabilities. It’s not a fine or penalty; it’s a trust mechanism that allows acquirers to keep your account active while managing potential losses.

3. Can I negotiate the percentage or duration of my rolling reserve?

Yes. Both the reserve percentage and hold duration are negotiable, particularly after you build a clean processing record (under 1% chargeback ratio) for three to six months. Supporting evidence such as transaction reports, chargeback logs, and compliance certificates (PCI DSS, KYC, AML) strengthens your position. Many acquirers agree to reduce from 15% to 5% or shorten the release window once stability is proven.

4. How long are funds held in a rolling reserve?

The most common holding periods are 90, 120, or 180 days, depending on the risk profile, industry, and acquirer policy. This timeline aligns with the card network dispute windows, Visa (up to 120 days) and Mastercard (up to 150 days for select sectors like travel or delayed delivery). Once the hold period expires and no disputes remain, funds are released on a rolling daily or weekly basis.

5. What’s the difference between a rolling reserve and a capped or fixed reserve?

- Rolling Reserve: A percentage of each transaction is held and released continuously over time.

- Capped Reserve: Funds are withheld only until a fixed balance (cap) is reached; once that cap is met, no further deductions occur.

- Fixed (Up-Front) Reserve: A lump-sum deposit or initial batch of transactions held before processing begins.

Rolling reserves are more flexible and scale with business volume, while capped reserves offer predictability.

6. What happens to my reserve funds if I close my merchant account?

When you terminate a merchant account, acquirers typically retain the rolling reserve for up to 180 days to cover any late-appearing chargebacks.

Once the chargeback window expires and no pending disputes exist, the funds are released in full to your nominated bank account. To avoid delays, request a final settlement statement and provide updated KYC documents before closure.

7. Can I earn interest on the funds held in my rolling reserve?

No. Reserve accounts are held in non-interest-bearing trust accounts. Processors are prohibited under most acquirer regulations (Visa, Mastercard, and FCA) from profiting from merchant reserve funds. The reserve is purely collateral, not an investment product.

8. What can I do to reduce or remove a rolling reserve permanently?

To remove or minimise your reserve, focus on:

- Keeping chargebacks below 0.8%.

- Using 3-D Secure 2 and fraud prevention tools (e.g., Ethoca Alerts, Verifi).

- Maintaining clear billing descriptors and quick refund policies.

- Scheduling formal reserve reviews every six months.

Demonstrated reliability is your strongest negotiation tool.

9. Are rolling reserves mandatory for all high-risk merchants?

Not always, some processors specialising in high-risk verticals offer no-reserve accounts for merchants with established volume and verified financials. However, new merchants or those with limited trading history almost always face at least a temporary reserve until trust is built.

10. Can a payment consultancy help negotiate better rolling reserve terms?

Absolutely, a specialist consultancy like Payment Mentors can analyse your processing history, compliance gaps, and acquirer performance to renegotiate reserve terms or migrate you to a more flexible PSP. Consultancies often maintain direct relationships with banks and can structure custom reserve schedules that preserve liquidity while satisfying regulatory safeguards.