In 2026, PSP and acquirer rejections for high-risk merchants are rising, and one of the most consistently underestimated causes is a mismatch between a merchant’s business model and the jurisdiction in which they are incorporated or licensed. Most rejections happen not because the business is illegitimate, but because of poor positioning: applying to institutions that do not support the category, or choosing a licensing jurisdiction that creates more problems than it solves for their specific vertical.

The damage compounds quickly. A failed application leaves a record. Multiple applications to institutions that were never going to approve the merchant create a pattern that later reviewers see. Application fees, legal costs and lost processing time accumulate. Merchants who skip the matching exercise and move straight to applications consistently pay more and wait longer than those who do the groundwork first.

This article is a practical pre-application guide for high-risk merchants across iGaming, adult, forex, subscription services and related verticals. Its purpose is to help merchants match their business model to the right jurisdiction before they apply, not after they have been declined.

Why Jurisdiction Matching Matters More Than Ever in 2026

The PSP and Acquirer Perspective on Licensing

PSPs and acquirers assess licensing jurisdiction as a core part of underwriting, not as a secondary consideration. A license from a credible, recognised jurisdiction signals regulatory oversight, governance standards and operational seriousness to the acquiring bank reviewing the appliccation. A license from an unrecognised jurisdiction, or no license at all in a regulated vertical, is frequently sufficient grounds for rejection regardless of the merchant’s actual compliance quality or processing history.

Acquiring banks want proof that a business is legitimate and regulated within an accepted framework. Without a credible license in the right jurisdiction, high-risk applications rarely progress past initial underwriting, particularly for iGaming, forex and adult categories where regulatory scrutiny from card schemes is already elevated. The license is not just a legal document; it is a commercial signal that determines which doors are open and which remain closed.

How Business Model and Jurisdiction Must Align

Not all jurisdictions accept all business models, and this is where many merchants lose significant time and money. A subscription-based adult platform has fundamentally different licensing requirements from a B2C iGaming operator or a forex CFD broker. Choosing a jurisdiction without mapping it against the specific business model, target markets and payment rails needed creates structural problems that no amount of documentation can resolve after the fact.

The alignment exercise matters because jurisdictions differ not only in what they license, but in how those licenses are perceived by PSPs, banking partners and card schemes.

A gaming license from Malta is read very differently by an acquiring bank than a gaming license from a jurisdiction with limited regulatory credibility, even if both are technically valid.

For high-risk merchants, that perception gap is the difference between onboarding and rejection.

Understanding Your Business Model Before Choosing a Jurisdiction

Before researching jurisdictions, merchants need precise clarity on their own business model across four dimensions. What they sell: digital goods, subscription access, gaming credits, financial instruments or adult content. How they charge: one-off transactions, recurring subscription billing, usage-based pricing or instalments. Who they serve: B2C, B2B or both, and critically, which geographies those customers are located in. What payment rails they need: card processing, A2A transfers, digital wallets, crypto or bank transfers.

Each dimension affects which jurisdictions are accessible, which PSPs will onboard the merchant and what compliance obligations will follow. A merchant who needs to process recurring subscription billing for European customers has very different licensing needs from one primarily processing one-off card payments for customers in LATAM or Asia. The geographic dimension is particularly important because some jurisdictions license operators to serve specific markets only, and processing payments from excluded markets can invalidate the license and void the PSP relationship simultaneously.

Getting this mapping wrong at the start causes delays, rejections and wasted application costs that can run into tens of thousands across multiple failed attempts. The mapping exercise takes time, but considerably less time than recovering from a series of avoidable rejections.

The Major Licensing Jurisdictions and What They Suit

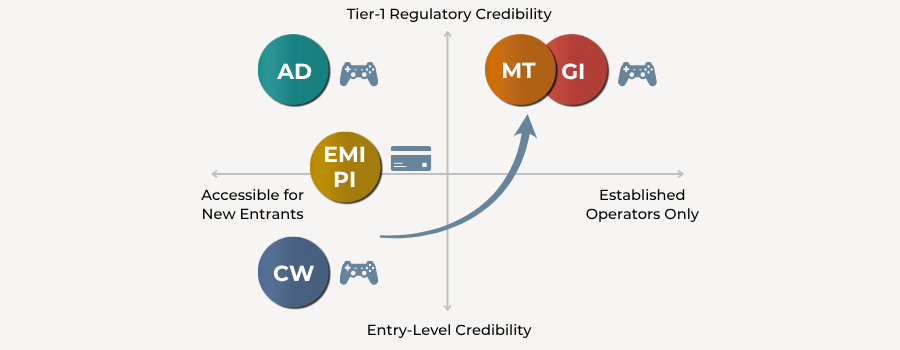

Malta (MGA): The EU Standard for iGaming and Beyond

Malta is the most widely recognised iGaming licensing jurisdiction globally, and for good reason. The Malta Gaming Authority has been issuing licenses for more than two decades, and an MGA license carries strong acceptance among European banks, PSPs and acquirers. It provides EU passporting benefits, clear regulatory guidance on AML and responsible gaming, and positions operators credibly with both payment partners and end customers.

Malta suits established or scaling iGaming operators targeting European markets, operators who need strong banking access and long-term PSP stability, and businesses that can meet robust AML, KYC, responsible gaming and audit requirements from the outset. It is not the right first choice for early-stage operators with limited processing history or those who need fast time to market. Malta’s process is thorough, its compliance expectations are high, and the ongoing audit and reporting obligations require meaningful operational investment.

Curacao: The Accessible Entry Point With Evolving Standards

Curacao has undergone significant regulatory reform, moving from a master license and sublicense system to direct licensing by the Curacao Gaming Authority, with enhanced AML requirements, mandatory UBO disclosure and clearer separation of B2C and B2B licenses. It remains lower cost and faster to obtain than Malta, and continues to accept crypto gambling where other jurisdictions do not.

Curacao suits entry-level iGaming operators, crypto-focused platforms and merchants seeking a regulated but commercially flexible entry point before transitioning to an EU jurisdiction. Many operators use Curacao as a deliberate stepping stone to Malta, building operational history and processing track record before the more demanding EU application.

The key consideration is banking access: Curacao-licensed entities face more limited PSP and banking options than MGA-licensed operators, and merchants who need broad European payment access will find this a constraint worth planning around.

Gibraltar: Prestigious but Selective

Gibraltar has been a legal gambling jurisdiction since 1998 and operates a small, high-standards licensing environment with 1% tax on income, no VAT and strong data confidentiality. Its selectivity is both its strength and its limitation: the Gibraltar regulator favours companies that already have experience in the market, and the licensing process is long and demanding.

Gibraltar suits well-established iGaming operators with existing market presence and proven governance frameworks. It is not an accessible option for new entrants and works best for operators upgrading from another jurisdiction rather than those applying for a first license. For merchants who qualify, the combination of regulatory prestige, tax efficiency and banking access makes it one of the strongest jurisdictions available.

Alderney: Tax-Efficient With Strong International Credibility

Alderney, overseen by the Alderney Gambling Control Commission, offers zero gaming tax, zero VAT and zero corporate tax on offshore profits, making it financially compelling for higher-volume operators. It suits B2C and B2B iGaming operators who need strong international credibility combined with a tax-efficient structure. Application fees start at £17,500 for local companies, with annual fees calculated on net gaming yield, and the process requires comprehensive financial, governance and AML documentation. Alderney is a credible option for operators who are not targeting EU passporting specifically but need a high-quality license that PSPs and banking partners recognise.

EMI and Payment Institution Licenses for Payment-Focused High-Risk Models

For high-risk merchants whose primary business is payment facilitation rather than gaming or content, EMI or Payment Institution licenses in EEA jurisdictions such as Lithuania, Ireland or the Netherlands offer a distinct and important licensing pathway.

EMI licenses require minimum initial capital of €350,000, robust AML and operational resilience frameworks, and provide EEA passporting rights that allow the license holder to operate across member states under a single regulatory framework.

These licenses suit fintechs, payment facilitators and high-risk platforms that need to manage their own payment flows rather than simply accepting payments through a third-party PSP. The compliance expectations are significant and ongoing, but the commercial flexibility and banking access that an EMI license provides in Europe is materially stronger than most alternatives available to high-risk businesses.

The Pre-Application Checklist, Before You Choose a Jurisdiction

The most consistent reason high-risk merchants are rejected is not illegitimacy; it is incomplete preparation. Before approaching a licensing authority or a PSP, the following questions should be answered clearly and documented. Merchants who cannot answer these questions confidently are not yet ready to apply, and proceeding anyway will typically result in a rejection that could have been avoided.

Business model clarity:

- Is your business model fully documented, including product type, pricing structure, target markets and payment flows?

- Have you identified which payment rails you need and confirmed they are available in your target jurisdiction?

- Have you mapped your MCC code and confirmed which PSPs and acquirers explicitly support it?

Corporate and ownership structure:

- Is your corporate structure clean, with clearly documented beneficial ownership and directorship across all entities?

- Are all directors and UBOs able to pass fit-and-proper tests including source-of-funds documentation?

- Is your registered entity in the jurisdiction you intend to license in, or do you need to establish a local entity first?

Compliance readiness:

- Do you have AML and KYC policies documented and ready to present?

- Do you have a responsible gaming or consumer protection framework in place if required by the target jurisdiction?

- Have you reviewed data protection obligations in the target jurisdiction and across your customer-facing markets?

Financial readiness:

- Do you have six months of business bank statements available and reconciled?

- Do you have financial projections for the next twelve months prepared and defensible?

- Have you confirmed the capital requirements for your target license and verified those funds are available?

PSP and banking alignment:

- Have you identified PSPs and acquirers who explicitly support your MCC in your target jurisdiction?

- Have you confirmed that your chosen jurisdiction is accepted by those PSPs as a credible licensing base?

- Have you checked whether your target customer markets have any restrictions on processing from your chosen jurisdiction?

Common Mismatches That Cause Applications to Fail

Vertical-Jurisdiction Mismatches

The most damaging mismatches in 2026 tend to follow recognisable patterns. A forex CFD broker applying through a gaming license jurisdiction that has no regulatory framework for financial instruments creates an immediate credibility problem with any acquiring bank reviewing the file. An adult subscription platform incorporating in a jurisdiction whose domestic banking sector will not service adult MCCs, regardless of license status, discovers too late that the license and the banking access do not arrive together. A subscription SaaS business applying to a payment institution that treats all recurring billing models as inherently high-risk, without recognising that a compliant license in the right jurisdiction changes the risk assessment, loses weeks to a process that was never going to succeed.

Each of these mismatches is avoidable with pre-application research, but each requires the merchant to understand not just where they can get a license, but where that license will actually be recognised by the payment partners they need.

Documentation and Positioning Failures

Even when the jurisdiction is correct, applications fail because of positioning rather than legitimacy. Most rejections at the PSP and acquirer level happen due to incomplete documentation, inconsistent ownership disclosures across different filings, or websites with visible compliance gaps: missing terms and conditions, unclear pricing disclosures, absent responsible use or age verification policies, and marketing claims that contradict the risk controls a PSP expects to see in place.

Merchants who treat compliance documentation as something to assemble during the application process, rather than as an operational foundation that already exists, consistently take longer to get approved and face more follow-up requests than those who arrive with a complete, consistent file. Preparation is not just about having the right documents; it is about presenting a business that already operates as if it were regulated, before the regulator formally confirms that it is.

Conclusion

In 2026, licensing jurisdiction is not a legal formality. It is a commercial and operational decision that affects which PSPs will onboard a merchant, which banking relationships are accessible, which markets can be served and how every stage of underwriting is assessed. High-risk merchants who treat it as an afterthought, choosing the cheapest or fastest option and discovering the mismatch only when PSP applications begin failing, pay significantly more in time, cost and lost revenue than those who do the matching exercise first.

The checklist in this article is designed to be completed before the first licensing conversation, not after the first rejection. Matching the business model to the right jurisdiction is not the most exciting part of building a high-risk payment stack, but in 2026 it is one of the most consequential.

FAQ

1. Why do so many high-risk merchants apply to the wrong jurisdiction first?

Because most merchants research where they can get a license quickly and affordably rather than where their specific business model, target markets and payment rails will be recognised by PSPs and acquiring banks. The matching exercise is skipped, and the mismatch only becomes visible when applications start failing.

2. How does licensing jurisdiction affect PSP and acquirer approvals?

PSPs and acquirers treat licensing jurisdiction as a core underwriting signal. A license from a credible, recognised jurisdiction indicates regulatory oversight and governance. A license from an unrecognised jurisdiction, or no license at all in a regulated vertical, is frequently sufficient grounds for rejection regardless of how compliant the merchant actually is.

3. What are the four dimensions a merchant should map before choosing a jurisdiction?

What they sell, how they charge, who they serve and what payment rails they need. Each dimension affects which jurisdictions are accessible, which PSPs will onboard the merchant and what compliance obligations will follow. Getting clarity on all four before researching jurisdictions saves significant time and application cost.

4. What type of high-risk merchant is Malta best suited for?

Malta suits established or scaling iGaming operators targeting European markets who need strong banking access, EU passporting benefits and long-term PSP stability. It is not the right first choice for early-stage operators with limited processing history or those who need fast time to market, as the compliance expectations and audit obligations require meaningful operational investment from the outset.

5. Is Curacao still a credible licensing jurisdiction in 2026?

Yes, but it has changed significantly. Curacao has moved to direct licensing by the Curacao Gaming Authority with enhanced AML requirements, mandatory UBO disclosure and clearer B2C and B2B license separation. It remains a credible entry-level option for iGaming and crypto-focused operators, and many merchants use it deliberately as a stepping stone before transitioning to an EU jurisdiction like Malta.

6. What makes Gibraltar different from Malta for iGaming licensing?

Gibraltar is smaller, more selective and better suited to well-established operators upgrading from another jurisdiction. It offers 1% tax on income, no VAT and strong data confidentiality, but requires existing licensing experience and has a long and demanding application process. New entrants are unlikely to be approved, making it a destination for experienced operators rather than a starting point.

7. What is an EMI license and which high-risk merchants need one?

An Electronic Money Institution license allows a business to manage its own payment flows rather than processing through a third-party PSP. It requires minimum initial capital of €350,000 and strong AML and operational resilience frameworks, but provides EEA passporting rights and materially stronger banking access than most alternatives. It suits fintechs, payment facilitators and high-risk platforms that need direct control over payment infrastructure.

8. What are the most common documentation failures that cause high-risk applications to be rejected?

Incomplete corporate documentation, inconsistent beneficial ownership disclosures across filings, websites with missing terms and conditions, unclear pricing disclosures, absent responsible use or age verification policies, and marketing claims that contradict the risk controls a PSP expects to see already in place. Preparation before applying is what separates approvals from rejections.

9. What is a vertical-jurisdiction mismatch and why is it so costly?

It happens when a merchant chooses a licensing jurisdiction that has no regulatory framework for their specific business model, or where domestic banking will not service their MCC regardless of license status. A forex broker applying through a gaming license jurisdiction, or an adult platform incorporating in a banking-unfriendly environment for their category, are classic examples. The mismatch costs application fees, legal time and processing delays that compound across multiple failed attempts.

10. Why is Alderney an attractive jurisdiction for higher-volume iGaming operators?

Because it offers zero gaming tax, zero VAT and zero corporate tax on offshore profits, combined with strong international regulatory credibility through the Alderney Gambling Control Commission. It suits B2C and B2B operators who need a tax-efficient structure alongside a license that PSPs and banking partners recognise, particularly those not specifically targeting EU passporting.

11. How should a high-risk merchant confirm PSP alignment before choosing a jurisdiction?

By identifying PSPs and acquirers who explicitly support their MCC, confirming those PSPs accept the target jurisdiction as a credible licensing base, and checking whether their customer-facing markets have any restrictions on processing from that jurisdiction. PSP and banking alignment should be confirmed before the licensing application is submitted, not after.

12. What is the single most important principle from this checklist?

Match first, apply second. Choosing a jurisdiction before mapping it against the business model, target markets, payment rails and PSP requirements consistently leads to avoidable rejections, wasted costs and lost processing time. The matching exercise takes time but far less than recovering from a pattern of failed applications that could have been prevented.