For a long time, merchant KYC meant filling out forms, uploading corporate documents and answering a handful of questions about ownership and business activity. Once the onboarding file was complete, it might sit untouched until a periodic review or a problem. In 2026, that model is disappearing fast. PSPs and acquirers are under pressure from regulators and banking partners to show that their KYC and AML controls are effective in practice, not just complete on paper.

For high‑risk merchants, that shift changes the texture of the relationship. PSPs still need documents, but that is the starting point rather than the finished product. They are now expected to understand how merchants behave over time, how transaction patterns evolve, and how each merchant sits inside a wider network of counterparties, related entities and potential risks. Many providers talk about perpetual KYC or event‑driven KYC, where certain triggers can generate fresh questions, even if nothing is obviously wrong at the transaction level.

This article is written for high‑risk merchants and platforms. It explains what deep KYC looks like from the PSP’s side in 2026, the behavioural and graph data they are likely to use, and how you can prepare so that enhanced checks become part of a stable relationship, not a constant series of surprises.

From Basic KYC to Deep, Behavioural KYC

What “Basic” KYC Used to Look Like

Traditionally, merchant KYC was front‑loaded when onboarding. PSPs and acquirers collected corporate registration certificates, director and beneficial‑owner documents, proof of address, sometimes bank statements, and a short description of business activity. Screening routines checked names against sanctions and PEP lists and occasionally adverse media, and once those checks were passed, the file was often treated as complete.

Periodic reviews did exist, but in many cases they were infrequent and driven by internal schedules rather than by changes in the merchant’s business. For high‑risk verticals, that meant the KYC file did not always keep pace with new products, jurisdictions or counterparties.

Why That Is Not Enough in 2026

Regulators and banks now expect payment institutions to treat KYC as dynamic, not static. Guidance and supervisory commentary highlight the need for ongoing monitoring, event‑driven reviews and a clear understanding of how customer risk changes over time. PSPs are being asked not just Did you collect the right documents at the start? but Can you explain why this merchant still fits your risk appetite today?

This expectation is feeding directly into high‑risk merchant onboarding and monitoring. Rather than relying only on static information, PSPs are combining traditional KYC artefacts with behavioural and relationship data about how you actually transact, with whom, and how that map changes as you grow. That combination is what this article calls deep KYC.

Behavioural Data: How PSPs Look at “How You Really Operate”

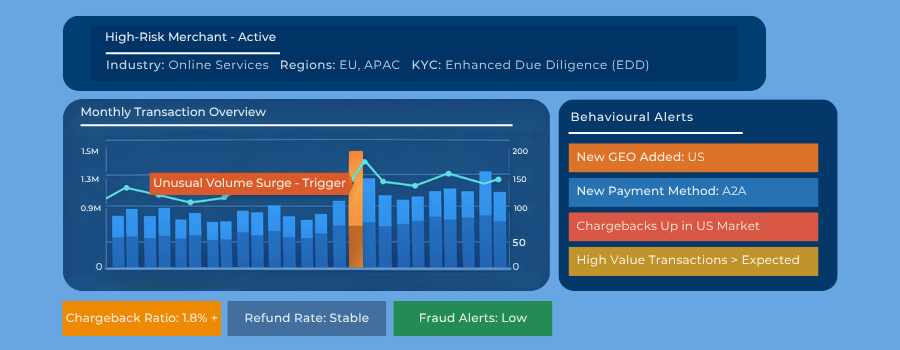

Transaction and Activity Patterns

The most visible source of behavioural insight is your transaction and activity data. PSPs and their banking partners increasingly use these signals to shape merchant risk assessments and KYC reviews.

They look at how your volumes and values move over time, not just the totals. Sudden spikes, unusual seasonality or rapid growth in particular corridors stand out, especially if they do not match the trajectory you described at onboarding. Payment method and channel mix also matter. A merchant that shifts quickly from card‑heavy to A2A‑heavy flows, or suddenly adds new pay‑in and pay‑out methods, will often draw attention, particularly in high‑risk sectors.

Risk and loss data are part of the same picture. Chargeback, refund and fraud patterns by product, geography or traffic source are watched closely. High levels in some categories may indicate genuine business challenges, but they can also point to undisclosed business models, aggressive marketing or behaviour that resembles known typologies.

Fundamentally, the PSP is looking for alignment between your declared business model and how money actually flows through your accounts. When those two diverge, KYC questions tend to follow.

Triggers for Deeper Reviews and Re-KYC

In 2026, many PSPs structure their KYC processes around trigger events or patterns that prompt fresh checks, even when the initial onboarding was clean. Some common triggers include:

- Rapid increases in total volume or average ticket size that are not explained by prior communication or expected seasonality.

- Expansion into new geographies or products that were not part of the original scope.

- Repeated unusual alerts in transaction monitoring or negative signals in external data, such as adverse media.

When these triggers fire, PSP teams may initiate an event‑driven review. That can mean asking for updated corporate documents, more detail on business model changes, explanations of volume growth, or additional evidence of controls. From a merchant perspective, it can look like extra KYC out of nowhere, but from the PSP’s perspective it is part of staying aligned with their own banking and regulatory obligations.

What This Means for High-Risk Merchants

For high‑risk merchants, the behavioural shift means that you are being assessed not only on who you are, but on how you operate in real time. You cannot fully control how PSPs interpret your data, but you can make that interpretation easier.

Keeping internal documentation on expected volume ramps, major campaigns, new GEOs or product launches makes it much simpler to explain growth or shifts when questions arise. Proactive communication about major changes, especially those that might show up as triggers, can make reviews smoother. In some cases, advance notice can allow a PSP to adjust limits or monitoring in a way that avoids unnecessary disruptions.

Having accessible, structured data on your transaction mix, customer segments and core use cases also helps. When you can articulate your own behavioural profile clearly, you are better positioned to engage with PSP teams who are increasingly looking at that same profile from their side.

Graph and Relationship Data: How PSPs See You in a Network

Moving from Individual Files to Networks

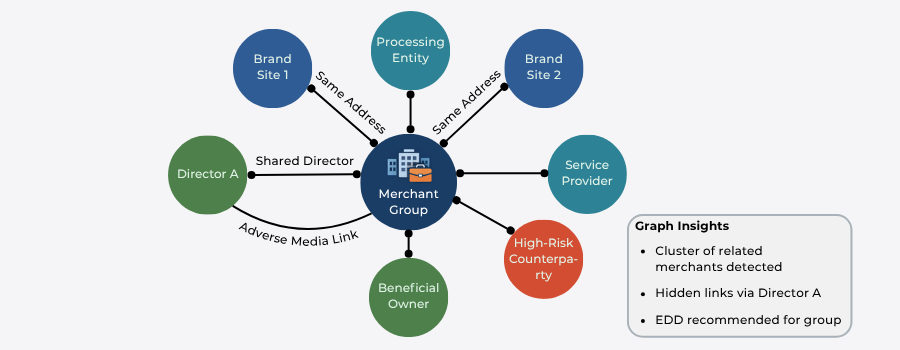

Deep KYC is not only about your own behaviour; it is also about where you sit within a wider network of entities. Graph and network analytics techniques, originally developed for complex AML investigations, are now being applied more broadly to customer and merchant data.

Instead of treating each merchant as an isolated file, PSPs and banks increasingly analyse relationships between entities: shared directors, beneficial owners, addresses, contact details, counterparties, payment flows, and links to other institutions. For high‑risk verticals, where complex ownership and family structures are common, graph views can reveal patterns that are hard to spot from documents alone.

Typical Graph Use Cases for Merchant KYC

AML and KYC graph analytics are usually presented through generic use cases, but several map directly onto merchant due diligence.

One common use case is identifying clusters of related merchants: multiple entities that share owners, directors, contact details or addresses, even if they presented themselves as unrelated in onboarding forms. Another is mapping transaction flows between merchants and counterparties, for example repeated payments to or from the same intermediary, wallet or service provider, which might indicate undisclosed relationships or layering patterns.

Graph tools can also highlight proximity to known risk entities. If an owner, director or key counterparty appears in adverse media, sanctions‑adjacent lists or prior suspicious activity reports, graph analysis can surface that proximity even when the connection is several steps away.

In all cases, the intention is to see whether the network around a merchant matches what the merchant has disclosed, and whether any unexpected connections increase risk.

Implications for High-Risk Merchants

For high‑risk merchants, graph‑based KYC means that PSPs are likely to see more than the initial paperwork shows. Shared directors across multiple entities, repeated use of similar addresses, or complex group structures can all appear in a network view even if they were not fully detailed in a particular application.

This does not automatically mean something is wrong. Many groups legitimately operate multiple brands, subsidiaries or SPVs. But it does mean that consistency matters. If a PSP’s graph view suggests that several entities are connected, and your disclosures suggest they are entirely unrelated, questions will follow.

High‑risk merchants can prepare by mapping their own group structure and relationships clearly, and by being ready to explain why they exist and how they operate. In some cases, providing more context upfront about group strategy, brand structure or shared services can reduce the risk of misunderstandings when graph‑based checks surface these links.

Deep KYC in Onboarding vs Ongoing Monitoring

Enhanced Due Diligence at Onboarding

Deep KYC is particularly visible during onboarding for high‑risk merchants. PSPs will still collect familiar documents, but the scope and depth of questions tend to be broader.

You can expect more detailed requests on your business model, including product mix, customer segments, jurisdictions, counterparties and channels. Ownership and control structures are examined more closely, with additional documentation on beneficial owners, funding sources and any regulated activities or licences. Screening is often run across multiple external sources: sanctions and PEP databases, adverse media providers, corporate registries and specialised risk data vendors.

For merchants, it can feel like being asked to justify every aspect of the business before anything has gone live. But from the PSP’s perspective, this is standard enhanced due diligence for high‑risk segments, reflecting what regulators and banks increasingly expect.

Perpetual KYC and Event-Driven Reviews

Once a merchant is live, deep KYC becomes a matter of ongoing monitoring rather than a single gate. Periodic KYC refresh cycles remain, and many PSPs will set schedules for reviewing and updating documentation and risk assessments at defined intervals.

More significantly, many also operate event‑driven or perpetual KYC models, where specific triggers changes in ownership, new directors, major shifts in product or geography, sustained volume growth, repeated alerts prompt targeted reviews. Transaction monitoring outcomes feed into this process: if certain patterns repeatedly trigger alerts or investigations, the merchant’s risk profile may be re-evaluated, even if those alerts are resolved.

In effect, a merchant’s KYC profile becomes a state that evolves with the business. PSPs are expected to keep that state in step with actual behaviour, rather than treat onboarding information as permanent.

Data, Governance and Privacy Expectations

Data Quality and Consistency

Deep KYC depends heavily on the quality and consistency of underlying data. Inconsistent company names, incomplete ownership information or mismatched addresses can make legitimate merchants look riskier, or at least harder to understand.

From a PSP’s point of view, poor data quality increases false positives in screening, complicates graph analysis and slows down monitoring. For merchants, it increases the likelihood of repeated questions and follow‑ups.

High‑risk merchants can reduce friction by maintaining clean internal corporate records, ensuring that public filings, website information and KYC submissions are aligned, and by updating PSPs when material changes occur.

Privacy, Data Protection and Proportionality

The use of behavioural and graph data naturally raises questions about privacy, data protection and proportionality. Regulators in many jurisdictions emphasise that AML and KYC programmes must be effective, but also proportionate, explainable and aligned with data protection frameworks.

In practice, this means PSPs need to be able to justify why particular data is processed, how long it is retained, who has access, and how it is used in decision making. For merchants, it is reasonable to expect PSPs to have clear policies here, and in some cases PSPs may be able to give high‑level explanations of why certain information is being requested.

From the merchant’s side, the key point is that more data is being processed than before, but that processing is being driven by regulatory expectations and bank requirements as much as by PSP preferences. Navigating that reality is part of operating in high‑risk verticals in 2026.

How High-Risk Merchants Can Prepare for Deep KYC

Make Your Own Risk View Explicit

One of the most effective ways to prepare for deep KYC is to develop an internal view of your own risk profile. That means documenting product lines, customer segments, geographies, counterparties, typical transaction sizes and patterns, and known vulnerabilities or mitigants.

When you can articulate your own risk view clearly, conversations with PSPs become less about defending surprises and more about aligning expectations. It also makes it easier to answer follow‑up questions quickly when event‑driven reviews occur.

Align Internal Records with What PSPs See

Because PSPs now use external data, relationship graphs and ongoing monitoring, it is important that internal and external records line up. Ownership structures, group entities, directors and key counterparties should be documented consistently across internal systems, public registries and PSP applications.

If your group operates multiple brands, SPVs or regional entities, mapping them clearly and explaining that mapping in onboarding and review documentation can reduce friction when graph analytics surface those relationships.

Build for Re-KYC as a Normal Process

Finally, high‑risk merchants benefit from treating re‑KYC and periodic reviews as a normal part of the relationship, not an exception. In practice, that can mean:

- Maintaining an internal KYC pack with up‑to‑date corporate documents, ownership details, licences and key policies that can be shared quickly.

- Tracking material changes new owners, new directors, new GEOs, new products and deciding when to proactively inform PSPs rather than waiting for them to ask.

- Assigning clear internal ownership for responding to PSP and bank information requests, so that reviews do not stall due to unclear responsibilities.

Approached this way, deep KYC becomes part of ongoing account management rather than a series of emergencies.

Conclusion

For high‑risk merchants in 2026, deep KYC is not an optional extra. It is a reflection of how PSPs, banks and regulators now expect risk to be understood and managed. Documents still matter, but they are only one piece of the picture. Behavioural data, relationship graphs and perpetual KYC models mean that merchants are assessed based on who they are, how they behave and who they are connected to over time.

Merchants who treat KYC purely as a hurdle to clear at onboarding are likely to be frustrated by re‑KYC cycles, ad‑hoc information requests and, in the worst cases, payout holds or relationship terminations. Those who treat it as an ongoing, cooperative process keeping data clean, documenting their own risk view, aligning internal and external records, and communicating significant changes are better positioned to navigate deep KYC without constant disruption.

Ultimately, deep KYC is about making sure that the PSP‑merchant relationship can withstand scrutiny from regulators and banks. For high‑risk merchants, engaging with that reality proactively is increasingly part of what it means to build a resilient payments stack in 2026.

FAQ

1. What is “deep KYC” for merchants?

Deep KYC goes beyond collecting basic documents at onboarding and looks at how a merchant actually behaves over time, including transaction patterns, counterparties and network relationships, to keep the risk view up to date.

2. How is deep KYC different from traditional KYC?

Traditional KYC focused on static information like company documents and ownership; deep KYC combines that with ongoing monitoring of behaviour and graph data, so PSPs can see how risk evolves instead of relying on a one‑off snapshot.

3. Why are PSPs adopting deep KYC in 2026?

Because regulators and banking partners now expect PSPs to demonstrate that their AML and KYC controls are effective in practice, with continuous monitoring and event‑driven reviews, especially for high‑risk merchants and complex business models.

4. What behavioural data do PSPs look at for merchants?

They look at transaction volumes and values over time, changes in payment methods and channels, and patterns of chargebacks, refunds and fraud by product or geography, checking whether these align with the declared business model.

5. What can trigger a re-KYC or deeper review?

Common triggers include rapid growth in volume or ticket size, expansion into new countries or products, unusual monitoring alerts, and negative signals from external data such as adverse media or corporate registry changes.

6. What is graph or network analysis in merchant KYC?

Graph analysis looks at relationships between entities, shared owners, addresses, contact details, counterparties and transaction flows, so PSPs can identify clusters of related merchants, hidden connections or proximity to known risk entities.

7. How can graph analytics affect high-risk merchants?

If graph checks reveal undisclosed links between entities, repeated use of the same controllers, or connections to adverse media subjects, PSPs may ask for more information, reassess risk or apply stricter monitoring, even if transactions individually look normal.

8. What extra information is expected at onboarding under deep KYC?

High‑risk merchants should expect more detailed questions about business models, geographies, customer segments, ownership structures, funding sources and licences, alongside broader screening across sanctions, PEP and adverse media data.

9. How often will re-KYC happen for a high-risk merchant?

There is no universal schedule, but many PSPs combine periodic reviews with event‑driven checks, meaning documentation and risk assessments may be updated when material changes or monitoring triggers occur, not only on a fixed calendar.

10. How can merchants reduce friction during deep KYC reviews?

They can maintain clean, consistent corporate records, keep an internal KYC pack ready, document expected changes in volumes, products and geographies, and proactively inform PSPs about material changes rather than waiting for surprise requests.