Adult and dating platforms rarely struggle with demand. Where growth most often breaks down is at the payment layer, when scrutiny increases and existing controls are no longer defensible. In 2026, the difference between platforms that scale and those that stall is not audience size or monetisation creativity, but whether their payment design can withstand sustained compliance review.

This matters because payments in adulthood and dating are never neutral. Card schemes apply heightened expectations around Age Assurance, consent, and content governance, while Payment Service Providers (PSPs) operate with very limited tolerance for ambiguity. In the UK, platform obligations under the Online Safety Act have become explicit, with Ofcom enforcing that protections must be operational rather than theoretical. Similar Duty of Care expectations are now standard across the EU under the Digital Services Act (DSA).

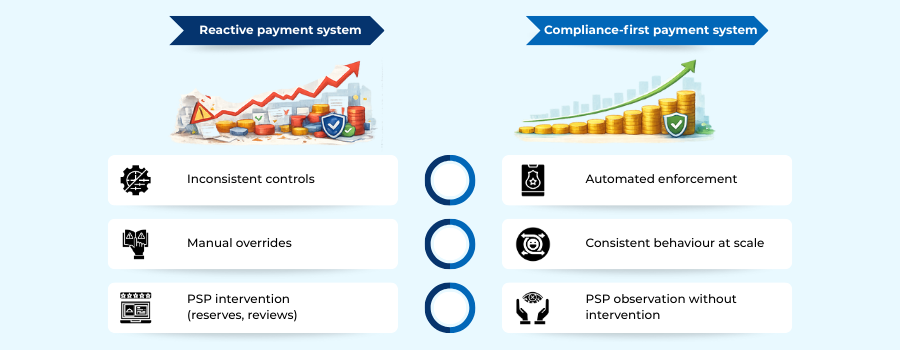

As a result, traditional growth approaches that prioritise feature launches over controls are failing faster. Payment providers escalate reviews earlier and respond more decisively when compliance is reactive instead of embedded.In response, leading adult and dating platforms are adopting Compliance-First Payment Design. By aligning monetisation, verification, and governance from the outset, they are building payment systems that support growth without collapsing under scrutiny.

- Why Adult and Dating Platforms Are Structurally High-Risk

- The Two Rulebooks That Determine Payment Survival in 2026

- Where Adult and Dating Payment Models Historically Break Down

- What Compliance-First Payment Design Actually Means in 2026

- How Leading Adult and Dating Platforms Are Redesigning Payments

- The Role of Card Schemes and PSP Expectations in Adult Payments

- Why Compliance-First Payment Design Strengthens PSP Relationships

- Adult vs. Dating Platforms: Where Payment Risk Diverges

- Designing Payment Systems That Scale Without Triggering Enforcement

- Conclusion

- FAQs

Why Adult and Dating Platforms Are Structurally High-Risk

Adult and dating platforms are treated as structurally high-risk not because of their business models, but because of the reputational exposure they create for the payment ecosystem.

For card schemes (Visa/Mastercard) and PSPs, the risk is that a single failure, a minor accessing content or non-consensual material being monetized can escalate into a global brand crisis.

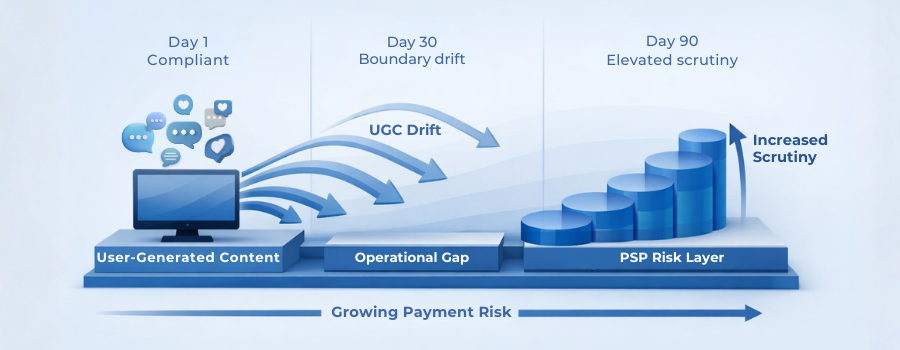

- The Drift Problem: User-generated content (UGC) is dynamic. A platform might be safe on Monday but non-compliant on Tuesday based on what users upload.

- The Operational Gap: Many platforms operate lawfully but fail reviews because they cannot prove it in real-time. Card schemes have made clear: policies are not controls. You must demonstrate how a specific transaction was checked for age and consent before it was processed.

The Two Rulebooks That Determine Payment Survival in 2026

Adult and dating platforms operate under two overlapping rulebooks that shape whether payment access survives scale. Misunderstanding either is the fastest way to trigger a MATCH list (TMF) termination.

Card Scheme Integrity Programs (VIRP & AN 4647)

- Visa Integrity Risk Program (VIRP): Replacing the old GBPP, Visa now classifies Adult and Dating merchants as Tier 1 (High Integrity Risk). This requires rigorous registration and often a dedicated Control Assessment by a third-party auditor.

- Mastercard Revised Standards (AN 4647): Mastercard requires that platforms be able to link every transaction to the documented consent of the person depicted in the content. If you cannot produce the consent record for a specific video, the payment for it is considered non-compliant.

Regulatory Safety Duties (Online Safety Act & DSA)

- UK Context: The Online Safety Act requires highly effective Age Assurance (not just self-declaration). Ofcom has signalled that payment providers are a key enforcement choke-point for non-compliant platforms.

- EU Context: Under the DSA, Very Large Online Platforms (VLOPs) face strict auditing requirements. PSPs increasingly mirror these standards, meaning if a platform cannot demonstrate alignment with safety duties, providers will exit the relationship to avoid regulatory blowback.

Where Adult and Dating Payment Models Historically Break Down

Payment failures in this sector rarely come from a single breach. They emerge from structural weaknesses that compound over time.

Ambiguity in Moderation and Verification

Many platforms rely on policy statements that sound robust but lack operational depth. Age checks may exist at onboarding but are not enforced consistently across monetised features. From a PSP perspective, this creates uncertainty about how risk is handled once transactions are live.

Monetisation Launched Ahead of Governance

Reactive Fixes After PSP Escalation

In many cases, platforms only strengthen controls after a payment provider raises concerns. By that point, trust has already eroded. PSPs are then more likely to impose blunt safeguards (like Rolling Reserves of 10-20%) rather than engage in incremental adjustment.

What Compliance-First Payment Design Actually Means in 2026

Compliance-first payment design is often misunderstood as a constraint on growth. In practice, it is a stabilising layer. It means recognising that payments are one of the most powerful enforcement points on a platform.

A compliance-first approach starts before features are launched. Verification states, content boundaries, and behavioural expectations are designed into payment access itself, rather than layered on after problems appear.

- Shift in Mindset: Instead of responding to audits or reviews, platforms anticipate how their payment flows will be interpreted under scrutiny. Controls are visible, measurable, and enforceable.

How Leading Adult and Dating Platforms Are Redesigning Payments

Platforms that are achieving payment stability are redesigning how payments interact with verification and governance, so that risk is constrained by design.

Tying Payment Access to Verification State

One of the most significant shifts is the explicit linking of payment privileges to verification status. Age Assurance and identity checks are no longer treated as onboarding formalities; they act as a gate for the payment rail.

Monetising User-Generated Content with Traceability

Where platforms support creator monetisation, payments are structured to enforce traceability. Every transaction is tagged with metadata linking it to:

- A verified creator ID.

- A specific content asset ID.

- A timestamped record of pre-publication moderation.

This allows the platform to answer the PSP’s hardest question: Can you prove this $50 tip was for consensual, legal content?

Using Payment Mechanics to Limit Risk Exposure

Leading platforms use payment design to shape behaviour. Spend limits, velocity controls (preventing rapid-fire transactions), and feature gating reduce the likelihood of abuse or coercion without relying solely on human moderation.

The Role of Card Schemes and PSP Expectations in Adult Payments

In adult and dating categories, card schemes exert influence long before formal enforcement actions occur. Their expectations shape how PSPs assess risk, design controls, and respond to uncertainty.

The Auditability Requirement

Card schemes (via programs like VIRP) expect PSPs to demonstrate that adult and dating transactions sit within clearly controlled environments. The absence of visible controls increases perceived exposure, even if no incident has occurred.

- The Consequence: PSPs translate these expectations into conservative operating behaviour. When controls are unclear, providers over-enforce through reserves or restrictions. This is not punitive; it is defensive.

Defensibility is Survival

For platforms, payment design must assume periodic scrutiny. Controls need to be understandable to external reviewers (auditors), not just internal teams. Where payment flows align with scheme expectations (e.g., matching the AN 4647 consent standards), reviews tend to be incremental. Where they do not, escalation is abrupt.

Why Compliance-First Payment Design Strengthens PSP Relationships

In adult and dating categories, payment relationships rarely fail because of a single breach. They fail because uncertainty accumulates. From a PSP’s perspective, every unanswered question about controls, moderation, or escalation increases the cost of maintaining the relationship.

Compliance-first payment design reduces that uncertainty. When controls are embedded into payment access, PSPs no longer have to infer how risk is managed. They can see it directly in how transactions behave, how monetisation is gated, and how exceptions are handled. This visibility changes the nature of the relationship.

Rather than relying on blunt safeguards like reserves or transaction caps, PSPs can manage exposure incrementally. Reviews become structured rather than reactive. Adjustments are discussed instead of imposed. Over time, this predictability makes adult and dating platforms easier to support than merchants who rely on policy assurances without operational proof.

There is also a portfolio effect. PSPs increasingly prefer fewer relationships they can defend confidently over broader exposure that demands constant intervention. Platforms that demonstrate disciplined payment design are more likely to retain access, expand corridors, or introduce additional methods as they grow.

In this context, compliance-first design is not about appeasing providers. It is about becoming a predictable counterparty. For adult and dating platforms, that predictability is what turns fragile payment access into a sustainable partnership.

Adult vs. Dating Platforms: Where Payment Risk Diverges

Although often grouped together as High Risk, the sources of payment risk differ significantly between these two categories.

Adult Platforms: Explicit Content Risk

- The Focus: Risk centres on consent and age. Can you prove everyone on screen is an adult and consented to be there?

- The Control: Pre-publication review and documented model releases (identity + consent) for every asset.

- The Payment Impact: PSPs focus on Illegal Content flags. A single confirmed report of non-consensual content can shut down the MID (Merchant ID).

Dating Platforms: Behavioural & Scam Risk

- The Focus: Risk centres on user safety and fraud. Are users real? Are they being scammed into subscriptions (romance fraud)?

- The Control: Identity verification (to prevent bots/impersonation) and velocity checks on spending.

Designing Payment Systems That Scale Without Triggering Enforcement

As platforms scale, payment behaviour stops being assessed transaction-by-transaction and starts being judged as a pattern.

Consistency at Scale

Many platforms design payments to work correctly, but not to behave consistently under pressure. Manual judgement or informal overrides may work at low volume, but they introduce variability as volume grows. From a PSP perspective, variability equals uncertainty.

Automated Compliance Rails

Platforms that scale without disruption design payment systems to behave the same way at 10x volume as they did at launch.

Example: If a platform automatically holds a payout when a creator changes their bank account details (to prevent account takeovers), that rule must fire 100% of the time, regardless of how famous the creator is.

Consistency, not just restraint, is what allows growth to continue without triggering enforcement.

Conclusion

In 2026, payment stability in adult and dating platforms is not secured through negotiation. It is the outcome of design choices that determine how risk is controlled, evidenced, and communicated.

The platforms that scale successfully are not those pushing boundaries fastest, but those whose payment systems remain defensible under the sustained scrutiny of Visa VIRP, Mastercard Standards, and the Online Safety Act.

Compliance-first payment design reframes payments from a fragile dependency into a stabilising layer. By aligning monetisation with verification and ensuring systems behave predictably at scale, platforms reduce the uncertainty that triggers enforcement. Growth becomes something the payment layer can absorb, rather than resist.

FAQs

1. Why are adult and dating platforms considered high-risk by payment providers?

Because payments in these categories expose card schemes and PSPs to reputational, regulatory, and enforcement risk. Even a single failure around age assurance, consent, or content moderation can escalate beyond the merchant relationship.

2. Does being legally compliant guarantee stable payment processing?

No. Legal operation does not automatically translate into payment acceptability. PSPs assess whether compliance controls are operational, auditable, and consistently enforced, not just whether a platform is lawful.

3. What does “compliance-first payment design” actually mean?

It means designing payment systems so that monetisation is conditional on verification, consent, and governance controls. Compliance is embedded into payment access, rather than added reactively after issues arise.

4. Why do payment providers escalate reviews as platforms grow?

As transaction volume increases, payment behaviour is assessed as a pattern rather than isolated events. Growth increases visibility, complaint exposure, and scheme scrutiny, making weak controls more visible.

5. Why are policies alone not enough for payment reviews?

Card schemes and PSPs require evidence. Platforms must be able to demonstrate how age checks, consent verification, and content moderation are enforced in real time, not just described in documentation.

6. How does user-generated content increase payment risk?

UGC is dynamic and unpredictable. Content that is compliant today can become non-compliant tomorrow. Payments linked to UGC must therefore be traceable, monitored, and controllable to remain defensible.

7. What typically triggers reserves or payment restrictions?

Reserves and restrictions are usually imposed when PSPs perceive uncertainty. This can arise from unclear controls, inconsistent enforcement, sudden growth, or inability to evidence compliance during reviews.

8. Why do card schemes focus so heavily on age assurance and consent?

Because failures in these areas can expose schemes to regulatory enforcement and brand damage. Payments linked to underage access or non-consensual content represent unacceptable risk.

9. How are adult platforms and dating platforms assessed differently?

Adult platforms are scrutinised primarily around explicit content, consent, and performer verification. Dating platforms face greater focus on behavioural risk, including scams, impersonation, and subscription abuse.

10. Can compliance-first payment design support growth rather than limit it?

Yes. Platforms that embed controls into payment systems experience fewer disruptions, fewer surprise reviews, and more stable PSP relationships, allowing growth to continue without repeated intervention.

11. Why do PSPs prefer fewer, deeper relationships in this sector?

Managing uncertainty is costly. PSPs increasingly favour platforms that are predictable, auditable, and defensible over a broad portfolio of merchants with inconsistent controls.

12. What role do payment systems play in platform governance?

Payments act as enforcement checkpoints. They determine who can monetise, what can be monetised, and under what verification conditions revenue is allowed to flow.

13. Why is enforcement often triggered without a single major incident?

Enforcement usually follows accumulated uncertainty rather than isolated failures. Inconsistent system behaviour or unclear controls can be enough to prompt defensive action.

14. How can platforms scale without triggering payment enforcement?

By designing payment systems that behave consistently under growth. Controls should be automated, enforceable by default, and resilient at higher volumes.

15. What is the most important mindset shift for adult and dating platforms in 2026?

Stop treating payments as a neutral utility. In high-sensitivity categories, payments are a core compliance layer that directly determines whether growth is sustainable.