In 2025, Brazil has become the beating heart of Latin America’s regulated iGaming revolution. Following the full implementation of Law No. 14,790/2023, the country’s Ministry of Finance, through the Secretariat of Prizes and Betting (SPA), has begun licensing operators under one of the region’s most advanced compliance frameworks. For local and global operators alike, the potential is enormous: a market of over 200 million adults, a digitally mature population, and the explosive adoption of Pix, Brazil’s instant payment system, which now processes more than 40 billion transactions annually.

Yet with opportunity comes exposure. The same payment rails that make Brazil a global fintech success story have also become a magnet for fraud rings, bonus-abuse syndicates, and synthetic identity networks operating at scale. The challenge is no longer simply securing transactions, it’s securing trust in an environment where every bet, deposit, and payout moves in milliseconds.

- Understanding Brazil’s Regulated Sports Betting Framework (2024-2026)

- The LATAM Fraud Profile: Why Emerging Betting Markets Are Prime Targets

- The PIX Factor: Brazil’s Instant Payment Revolution and Its Hidden Risks

- Geo-Specific Fraud Prevention Tools: Device Fingerprinting and Localised Velocity Intelligence

- Payout Risk Management: Preventing Money Laundering in High-Value Winnings and Rapid Cash-Outs

- Building a Secure and Compliant Payment Ecosystem for LATAM Operators

- Conclusion

- FAQs

Understanding Brazil’s Regulated Sports Betting Framework (2024-2026)

As of 2025, Brazil stands at the forefront of Latin America’s shift from grey-market betting to a state-supervised, transparent gaming ecosystem. After years of fragmented enforcement and offshore dominance, the Brazilian government has implemented a structured licensing and oversight framework that balances market growth with consumer and financial protection.

This section unpacks the legal, operational, and payment-related components of that framework, the same pillars that every sportsbook operator must understand before tackling fraud mitigation.

The Legal Backbone: Law No. 14,790/2023 and the Role of the SPA

Law No. 14,790/2023, signed into effect in December 2023, officially legalised fixed-odds betting (apostas de quota fixa) in Brazil. It laid the foundation for one of the most advanced gaming frameworks in LATAM, addressing three key priorities:

- Consumer protection and transparency

- Fair taxation and revenue distribution

- Anti-fraud and AML compliance across payment systems

Under the law, operational responsibility lies with the Secretariat of Prizes and Betting (SPA), part of the Ministry of Finance. The SPA’s role is to:

- License operators and monitor compliance

- Approve and supervise payment methods

- Ensure that betting platforms adhere to responsible gaming standards

- Coordinate with the Financial Intelligence Unit (COAF) to detect and report suspicious financial activity.

The SPA operates in collaboration with the Central Bank of Brazil (BACEN), ensuring that payment infrastructure (including Pix) complies with both gaming and banking regulations.

Key Ordinances That Define Compliance and Payments

The regulatory foundation was further detailed through two landmark ordinances in 2024:

SPA/MF Ordinance No. 615/2024 – Payments and Settlement Controls

This ordinance defines the approved payment methods for sports betting operations in Brazil.

Permitted:

- Pix instant payments (both deposit and payout)

- TED (traditional electronic transfers)

- Debit and prepaid cards

Prohibited:

- Cryptocurrencies

- Cash deposits

- Paper boletos (due to fraud risk)

It mandates that all transactions must occur within the Brazilian financial system, eliminating offshore payment channels that previously enabled tax evasion and money laundering.

SPA/MF Ordinance No. 1,143/2024 – AML, CFT, and KYC Obligations

This ordinance enforces risk-based AML programs, requiring operators to:

- Verify player identity through CPF-linked data and government IDs;

- Monitor and report suspicious betting or payout activity to COAF;

- Implement internal AML controls proportional to transaction volume and risk exposure;

- Maintain detailed audit logs for a minimum of 10 years.

Operators are also obliged to create risk classification frameworks, ensuring players are categorised by transaction volume, frequency, and payout velocity.

Why Regulation Matters for Fraud Mitigation

The Brazilian model redefines the relationship between regulation and risk management. For years, offshore operators processed unverified transactions through PSPs in jurisdictions like Curaçao or Cyprus. Fraud detection was largely reactive, and dispute resolution was inconsistent.

Under the new framework, the environment has changed fundamentally:

| Before Regulation | After Law 14,790/2023 & SPA Oversight |

| Offshore payment gateways with no visibility into player data | Localised payments (Pix/TED) under BACEN oversight |

| Fragmented AML compliance | Unified AML/CFT framework under COAF |

| Card-based chargeback abuse | Instant payments with traceable CPF-to-account linkage |

| Weak or non-existent KYC | Mandatory CPF verification and biometric ID matching |

This convergence of regulatory enforcement and payment centralisation creates a more transparent financial trail, but it also concentrates risk. Fraudsters now target Pix rails, CPF spoofing, and payout manipulation, which requires operators to evolve their fraud strategies in lockstep with compliance.

The Road Ahead (2025-2026)

By 2026, all betting operators will be required to hold a valid SPA license, submit AML activity reports, and process player funds through Brazilian financial institutions. The SPA has announced an ongoing rollout of API-based supervision, where licensed operators’ transaction data will be automatically synchronised with COAF for real-time oversight.

This regulatory transformation doesn’t just legitimise the industry, it professionalises it.

For PSPs, gateways, and operators alike, compliance with Brazil’s structured payment rules is not only a legal mandate but also a strategic advantage in building consumer trust and fraud resilience.

The LATAM Fraud Profile: Why Emerging Betting Markets Are Prime Targets

Latin America’s online betting revolution is one of scale, speed, and, increasingly, risk.

As new regulations open national markets like Brazil, Mexico, and Colombia to licensed operators, fraudsters are evolving just as quickly. The LATAM region has become a live testing ground for new financial crime models, blending social engineering, synthetic identities, and digital payment manipulation.

In the context of sports betting, fraud is no longer limited to rigged outcomes or player collusion, it’s embedded in the very payment lifecycle of deposits, bonuses, and payouts. Understanding the regional fraud profile is therefore the first step to building resilient operations in this fast-changing market.

The Rise of Hybrid Fraud Models

The LATAM betting ecosystem faces a unique blend of traditional fraud and next-generation cyber manipulation, often merging multiple techniques within a single scheme.

- Account Takeover (ATO) and Credential Stuffing: With data breaches and leaked credentials rampant across LATAM, criminals use automated bots to access legitimate betting accounts. Once inside, they change login details, drain balances, or exploit stored Pix credentials for rapid withdrawals.

- Bonus Abuse & Multi-Accounting: In markets where operators use aggressive welcome bonuses, fraud rings exploit CPF recycling (Brazilian tax IDs) to register hundreds of fake accounts.

- These accounts are often linked to prepaid SIM cards and disposable Pix keys, enabling coordinated attacks during major sporting events.

- According to Sportradar LATAM Integrity Insights (2025), over 22% of fraudulent betting activity in Brazil originates from bonus manipulation networks.

A 2025 Financial Crime Report noted that nearly 38% of all Pix-related betting scams began via social media or messaging channels.

Why LATAM Markets Are Fertile Ground for Betting Fraud

Unlike mature EU markets, many LATAM economies face infrastructure asymmetries, advanced payment systems but inconsistent verification tools. This gap creates an imbalance between transaction speed and fraud oversight.

Key structural drivers:

- Rapid fintech adoption: Brazil’s Pix and Mexico’s SPEI have outpaced fraud detection infrastructure.

- High digital inclusion but low cybersecurity awareness: A large segment of first-time bettors lack digital safety literacy.

- Economic instability: High inflation and youth unemployment fuel both legitimate betting interest and recruitment into fraud networks.

- Cross-border vulnerabilities: Unregulated operators still process through offshore acquirers in Curaçao, Panama, or Cyprus, enabling multi-jurisdictional laundering chains.

Together, these factors create an environment where fraud is decentralised, data-rich, and socially scalable, often coordinated across multiple platforms in real time.

Mexico, Colombia, and Argentina, Parallel Risk Environments

While Brazil dominates LATAM’s betting sector, similar risk dynamics are emerging across the region:

Mexico

The absence of a unified AML framework for iGaming allows cross-border PSPs to route payments through the U.S. BINs and crypto intermediaries. Mexico’s reliance on SPEI bank transfers makes it vulnerable to identity spoofing and layered fund movements.

Colombia

Under Coljuegos, Colombia’s regulated framework has reduced unlicensed operators but still struggles with affiliate fraud and referral link abuse. Fraudsters exploit risk-blind bonus codes and duplicate accounts to siphon affiliate rewards.

Argentina

Regional fragmentation (each province has its own regulator) means AML consistency is weak. Fraudsters exploit local payment apps (Mercado Pago, Ualá) for laundering small-value betting payouts below reporting thresholds.

Psychological and Socioeconomic Drivers

Fraud in LATAM isn’t always purely technical, it’s deeply sociocultural.

Operators must understand the behavioural roots behind fraud behaviour to build preventive frameworks that actually work in local contexts.

- Economic Motivation: With inflation in Brazil and Argentina often exceeding 6-8%, small-time fraud is seen as a side hustle, not organised crime.

- Trust Deficit: Many users distrust institutions, preferring local payment wallets over licensed gateways, a trust gap that fraudsters exploit.

In short, LATAM’s fraud risk is not just technological, it’s cultural, systemic, and opportunistic.

The Evolving Fraud Lifecycle: From Deposit to Payout

| Stage | Common Attack Vector | Impact on Operators |

| Account Creation | Synthetic identity fraud, CPF recycling | AML/KYC risk, account bloat |

| Deposit | Compromised Pix keys, stolen credentials | Instant losses, reputational risk |

| Bonus Redemption | Multi-accounting, referral abuse | Marketing loss, ROI erosion |

| Betting Phase | Collusion, data scraping | Integrity breaches, unfair play |

| Payout | Laundering via fake winnings | Regulatory breach, SAR violations |

Operators must now see fraud not as a single event but as a cycle, where one weak stage can undermine the entire compliance chain.

What This Means for Operators and PSPs

To operate safely in LATAM, especially Brazil, PSPs and sportsbooks must evolve from static fraud monitoring to adaptive, contextual risk intelligence.

This means:

- Combining behavioural biometrics, geo-fencing, and Pix transaction profiling;

- Integrating local regulatory data (e.g., CPF validation via Receita Federal APIs);

- Partnering with licensed Brazilian payment institutions (IPIs) that have direct BACEN oversight.

The result? A fraud defence model built on local knowledge, regulatory alignment, and machine-speed detection, the new gold standard in regulated LATAM markets.

The PIX Factor: Brazil’s Instant Payment Revolution and Its Hidden Risks

When Pix launched in November 2020, it changed the DNA of Brazil’s payment ecosystem overnight. Within just four years, Pix became the world’s most used real-time payment network, surpassing 40 billion transactions annually, more than all debit and credit card transactions combined.

For sportsbooks and iGaming operators, Pix is both a blessing and a challenge. Its frictionless design, instant, 24/7, low-cost, makes it the ideal payment method for deposits and payouts. But those same features that drive user convenience also amplify exposure to fraud and compliance risk when not properly managed.

Understanding Pix’s mechanics, vulnerabilities, and risk management pathways is essential for any operator in Brazil’s regulated market.

How Pix Works: The Engine of Brazil’s Betting Economy

Pix is an account-to-account (A2A) instant payment system governed by the Central Bank of Brazil (BACEN). It enables transfers between individuals, merchants, and institutions in seconds using a unique Pix key, typically a CPF (tax ID), email, phone number, or random alphanumeric code.

For sportsbooks, Pix enables near-instant deposits and withdrawals, reducing churn and improving liquidity cycles. Operators benefit from:

- Real-time fund availability (no settlement lag)

- Lower transaction fees versus cards

- Reduced chargeback exposure (since Pix transactions are irrevocable),

- Seamless KYC linkage through CPF integration.

By 2025, over 80% of Brazilian sportsbooks rely on Pix as their primary funding and payout method.

But with scale comes systemic risk, and Pix’s very strengths have become the entry points for fraud.

The Hidden Vulnerabilities in Pix Transactions

Pix is technically robust, but fraudsters exploit behavioural, procedural, and social loopholes in how it’s used.

- Synthetic Identity Creation through CPF Spoofing

Fraudsters register Pix keys using stolen or repurposed CPF numbers combined with new bank accounts. These synthetic accounts are used to receive fraudulent payouts or bonuses before being shut down. - Account Takeover through Banking Apps

As banks integrate Pix directly into mobile apps, compromised login credentials (often from phishing kits) enable fraudsters to hijack legitimate bettor accounts and reroute payouts to mules. - Laundering via Layered Payouts

Fraud rings distribute small winnings across hundreds of accounts using automated bots, staying below COAF’s suspicious activity reporting threshold. This micro-laundering makes detection difficult unless behavioural velocity checks are in place.

2025 financial crime data showed that over 32% of flagged Pix-linked betting transactions involved mismatched CPF/account ownership.

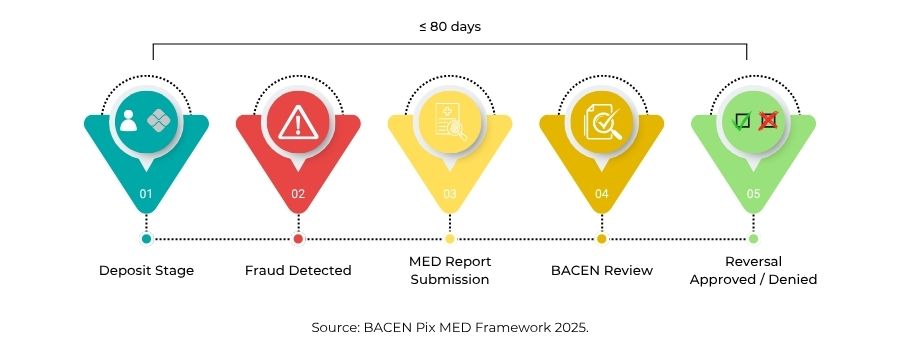

The Mecanismo Especial de Devolução (MED): Pix’s Fraud Reversal Process

To mitigate fraud, BACEN introduced the MED protocol, Mecanismo Especial de Devolução, a special refund mechanism allowing financial institutions to reverse transactions proven to be fraudulent.

However, the MED framework is highly procedural:

- A refund request must be submitted within up to 80 days of the transaction;

- Operators must supply clear, timestamped fraud evidence;

- Funds can only be reversed if the receiving bank confirms availability and legitimacy of the claim.

For sportsbooks and PSPs, this means time and compliance discipline are critical. Delayed or incomplete evidence submissions often result in permanent loss of funds. MED is not a guarantee, it’s a safeguard for well-prepared operators.

Operational Risks Unique to Sportsbooks

Sports betting operators face Pix-specific vulnerabilities beyond generic payment fraud:

- High-Velocity Cash-Outs: Fraudsters exploit betting promotions to trigger rapid deposit-withdraw cycles (deposit via Pix, bet small, withdraw balance instantly).

- KYC Mismatch in Payouts: Players register under one CPF but request withdrawals to a Pix key linked to another. This is a clear AML breach under SPA/MF Ordinance No. 1,143/2024.

- Transaction Looping: Automated bots simulate normal betting behaviour, repeatedly cycling small Pix payments between linked accounts to clean illicit funds.

These tactics exploit weaknesses in operator-side monitoring, not in Pix itself. The challenge is building systems that detect patterns, not just transactions.

Mitigating Pix-Linked Fraud: From Reactive to Proactive Controls

Modern fraud management requires layered defences aligned with BACEN and SPA’s compliance expectations. Key measures include:

- Real-Time CPF-Bank Ownership Verification

Integrate directly with Receita Federal APIs to verify CPF validity and account ownership before accepting deposits or payouts. - Behavioural Velocity Controls

Track deposit frequency, payout timing, and transaction value spikes. Machine learning models can detect unnatural deposit-to-withdraw ratios. - Geo-Fencing and Device Fingerprinting

Map Pix requests to know better devices and geolocations. Any mismatch, e.g., CPF registered in Rio de Janeiro but payout requested from IP in Lagos, should trigger review. - Integration with MED API

Automate fraud evidence submission to BACEN’s MED system to accelerate refund claims when fraud is confirmed.

By combining these layers, operators can transform Pix from a compliance burden into a competitive advantage, offering instant payments with demonstrable fraud resilience.

The Pix Paradox: Fast, Secure, and Still Fragile

Pix represents Brazil’s fintech genius, but also its regulatory stress test. For sportsbooks, it’s the financial artery of player engagement. Yet without proactive security, it can just as easily become a channel for systemic fraud.

Operators that succeed in this environment will not be those that avoid risk entirely, but those that understand Pix deeply enough to predict and pre-empt it.

Geo-Specific Fraud Prevention Tools: Device Fingerprinting and Localised Velocity Intelligence

In the regulated LATAM betting market, knowing who your customer is no longer stops at KYC.

Fraudsters have evolved beyond fake IDs and stolen CPFs, they now manipulate devices, behavioural patterns, and transaction timing to appear legitimate.

To detect them, operators must move from static verification to geo-intelligent fraud prevention: a dynamic approach combining device fingerprinting, behavioural analytics, and localisation filters.

This section explores how these tools work in Brazil and other LATAM markets, and how they can drastically reduce fraud exposure across the entire payment cycle.

1. Device Fingerprinting: The Core of Modern Fraud Intelligence

Device fingerprinting builds a unique profile of every device (mobile or desktop) accessing your betting platform. It collects hundreds of attributes, from browser type and screen resolution to operating system, language, and IP location, to form a persistent digital identity.

For sportsbooks and payment gateways, fingerprinting helps in three critical ways:

- Detect Multi-Account Fraud: Fraudsters may create multiple betting profiles using different emails and CPFs but from the same physical device. Device fingerprinting links those identities instantly.

- Prevent Account Takeover (ATO): When login behaviour changes, such as a new device or browser, the system flags a risk, triggering secondary verification.

- Block Emulator and Bot Attacks: Many fraud rings use device emulators to automate betting and cash-out patterns. Fingerprint data exposes them by identifying mismatched device signatures.

According to Sportradar’s LATAM 2025 Fraud Risk Benchmark, sportsbooks using device fingerprinting reduced multi-account abuse by up to 67% within the first 90 days of deployment.

2. Behavioural and Velocity Analytics: Fraud Has a Rhythm

While fingerprinting identifies who a user is, velocity analysis determines how they behave.

Velocity systems monitor the speed, frequency, and sequencing of transactions to detect anomalies.

Key patterns to monitor:

| Velocity Type | Example of Fraud Trigger | Risk Category |

| Login Velocity | 50+ logins from the same IP across different CPFs in 30 minutes | Bot activity / account farming |

| Deposit Velocity | Multiple deposits from different Pix keys into one account within an hour | Source-of-funds obfuscation |

| Withdrawal Velocity | Instant payout requests within minutes of bonus redemption | Bonus abuse / laundering |

| Geo Velocity | Account logs in from Brazil and Eastern Europe within 10 minutes | Account takeover |

By tracking this data, systems can flag impossible patterns in real time, for instance, a bettor logging in from São Paulo and Bucharest within the same hour.

Localisation Tip:

Set geo-specific thresholds, not global ones. In LATAM, transaction rhythms differ by country and time zone. For instance, Mexico’s betting peak happens between 7-11 p.m. CST, while Brazil’s surge happens between 9 p.m. and midnight BRT. An operator using UK/EU benchmarks might wrongly flag local users as fraudulent simply because their activity curve is different.

3. IP Intelligence and Device Linking Across LATAM

Geo-fraud in betting often involves regional proxy networks or Pix mules operating cross-border. Fraudsters mask device locations through VPNs or Tor nodes to appear domestic.

Modern risk systems now integrate IP intelligence databases that:

- Detect VPN, proxy, and data centre IPs

- Correlate IP ranges with known mule clusters (CPF laundering rings in northern Brazil or Paraguay)

- Match network signatures against historic fraudulent Pix transactions

In Brazil, the SPA and BACEN encourage the use of geolocation APIs tied to local telco data for real-time location verification, a method far more accurate than simple IP lookup.

4. Layered AI: When Machine Learning Meets Local Context

The most effective LATAM anti-fraud systems blend machine learning (ML) with local cultural insight. Unlike European betting ecosystems, where fraud is largely financial, LATAM fraud often combines social cues (e.g., WhatsApp campaigns) and event-driven spikes (e.g., Copa Libertadores, World Cup qualifiers).

To adapt, ML models must be trained on regional datasets, not global ones.

For example:

- A sudden increase in small-value Pix deposits before a football match may signal bonus abuse in Brazil, but legitimate user activity in Argentina.

- AI trained on LATAM velocity data learns to distinguish these behaviours based on contextual patterns rather than rigid thresholds.

Several payment gateways (e.g., dLocal, PagBrasil, and EBANX) now use hybrid systems that pair behavioural AI with human fraud analysts fluent in Portuguese and Spanish, a model that has proven 40% more accurate in identifying high-risk user clusters.

5. Best Practices for Geo-Specific Fraud Prevention

To deploy an effective LATAM-centric fraud defence framework, operators should:

- Combine device fingerprinting APIs (e.g., ThreatMetrix, SEON) with Pix validation tools.

- Implement geo-velocity and CPF verification within the same risk engine.

- Localise risk rules per market (Brazil ≠ Mexico ≠ Chile).

- Collaborate with BACEN-approved payment institutions (IPIs) for local transaction insights.

- Integrate risk alerts into COAF Suspicious Transaction Reports (STRs) for full regulatory coverage.

The result: a compliance-aligned, data-driven risk framework that recognises patterns unique to Brazil, Mexico, and LATAM’s maturing betting ecosystem.

The Outcome: Smarter Fraud Controls, Safer Growth

In 2025, LATAM’s gaming industry entered its most data-rich era. With smart device analytics and regional velocity intelligence, operators can finally transition from reactive fraud blocking to predictive fraud prevention.

The future of payment integrity in LATAM will belong to operators that think locally, act globally, embedding technical precision within a deep understanding of local user behaviour.

Payout Risk Management: Preventing Money Laundering in High-Value Winnings and Rapid Cash-Outs

In any betting ecosystem, the payout stage is the most vulnerable point for money laundering (ML) and fraud convergence. It’s where virtual risk becomes tangible cash, and where underwriters, regulators, and banks expect the highest due diligence from operators.

In Brazil and the broader LATAM region, payout risk has taken on new dimensions as Pix, crypto, and e-wallet integrations blur the traditional lines between gambling proceeds and financial transactions. The ability to process instant withdrawals, while critical for user satisfaction, can also open doors to AML breaches if not properly structured.

Let’s explore how payout fraud manifests, why it’s particularly acute in LATAM, and the tools operators need to mitigate it.

1. Why Payouts Are the Prime Target for Launderers

Fraudsters and criminal organisations see sportsbook payout systems as ready-made laundering tunnels. Unlike deposits, which are often subject to KYC, payout verification is weaker, especially when processed instantly via Pix or local wallets.

Common laundering tactics include:

- Winnings Laundering: Using illicit funds to place low-risk bets (e.g., betting on favourites) and cashing out as legitimate winnings.

- Smurfing (Structuring): Splitting large winnings across hundreds of small Pix payouts below regulatory reporting thresholds.

- Third-Party Withdrawals: Payouts sent to Pix keys, crypto wallets, or accounts not registered under the bettor’s CPF.

- Circular Transactions: Fraud rings collude to bet among themselves, recycling the same funds through multiple accounts to create a trail of “clean” betting profits.

According to COAF’s 2025 AML Bulletin, over 42% of suspicious activity reports (SARs) linked to Brazilian iGaming operators involved payout-related anomalies, not deposits.

2. The Instant Payout Paradox

Brazil’s betting market thrives on speed, users expect Pix withdrawals in seconds.

Yet this expectation conflicts with the compliance lag needed to verify transaction legitimacy.

The paradox is clear:

- Delay payouts, and user satisfaction drops.

Regulators like BACEN and SPA (Secretaria de Prêmios e Apostas) now expect licensed operators to strike a balance: speed with scrutiny.

This means embedding verification before funds leave the operator’s wallet, using automation to check compliance in real time.

3. How Money Laundering Through Betting Works (LATAM Model)

The process typically follows a 3-layered structure, placement, layering, and integration, just like in financial crime laundering, but adapted for gaming flows:

| Stage | Laundering Activity | Detection Strategy |

| Placement | Deposit illicit funds into betting account via Pix or prepaid cards | KYC screening, CPF validation, device mapping |

| Layering | Make low-risk bets and transfer winnings across linked accounts | Velocity analytics, cross-account clustering |

| Integration | Withdraw clean funds to Pix, crypto wallets, or offshore banks | Beneficiary name matching, AML monitoring, blockchain tracing |

These cycles are increasingly automated using bot-assisted betting systems that mimic normal player behaviour, a major focus in Brazil’s COAF 2025 AML intelligence reports.

4. Detecting and Preventing Suspicious Payouts

To manage payout-related ML exposure, sportsbooks and PSPs should implement multi-layered anti-fraud controls that focus on real-time decisioning, not just post-event audits.

Key strategies include:

a. Name Matching & CPF Cross-Validation

Ensure every payout CPF matches both the account holder and the original funding source.

Integrate Receita Federal APIs to verify CPF ownership in real time. Use BACEN’s Pix ownership validation API to confirm CPF-Pix linkage before releasing funds.

b. Beneficiary Profiling

Create payout profiles by customer type: frequency, average size, and preferred method.

If a casual bettor suddenly requests multiple high-value Pix withdrawals in 24 hours, trigger secondary review.

c. Velocity & Ratio Checks

Set payout-to-deposit ratio thresholds, e.g., withdrawals exceeding 5× deposits in 24 hours should be auto-flagged. Use AI clustering to link patterns across accounts that share devices or Pix keys.

d. Transaction Chain Auditing

Track payout routing, e.g., Pix → Wallet → Crypto Exchange → Offshore Account.

This helps identify integration laundering via cross-platform movements, especially where winnings end up on crypto-to-fiat bridges.

e. Human Oversight on Rapid Fire Payouts

Even the best AI systems fail without human escalation paths. Operators should maintain a Risk Review Queue where compliance officers manually verify payout anomalies flagged by the system.

5. Managing Payout Risk in the Context of Regulation

Brazil’s Decree 14.790/2024 and SPA Ordinance 1,143/2024 establish explicit AML requirements for betting operators, including:

- Verifying the beneficial owner (UBO) for every payout above R$2,000,

- Reporting suspicious or structured payouts to COAF within 24 hours,

- Maintaining payout logs for a minimum of 5 years, and

- Segregating customer funds from operational accounts (to avoid commingling).

Operators that fail to meet these obligations face fines of up to R$2 million per incident, licence suspension, or even criminal exposure.

International operators entering Brazil (from the UK, EU, or MENA) must therefore ensure that their AML frameworks are localised, COAF’s reporting logic and Pix’s unique data flow differ significantly from European AML directives.

6. Payout Fraud Prevention: Best Practice Framework

Here’s a compliance-aligned approach to mitigating payout risk:

| Step | Action | Technology/Regulatory Tool |

| 1 | Automate CPF-Pix Key Matching | BACEN Validation API |

| 2 | Apply Behavioural Scoring to Payouts | Machine learning + Geo-velocity checks |

| 3 | Run Instant AML Checks (PEP/Sanctions) | Local screening databases integrated with COAF |

| 4 | Enforce Cooling Periods for High-Value Withdrawals | 2-12 hour verification window |

| 5 | Escalate Outlier Transactions to Compliance | SPA-compliant review queue |

| 6 | Record & Report Structured Payouts | Automated COAF STR submission |

This framework aligns with the COAF Resolution 36/2024 AML directive and has already been adopted by major operators such as Betano Brazil and PixBet as part of their compliance revamp for regulated operations.

7. Balancing Compliance with User Experience

The goal isn’t to slow payouts, it’s to verify smartly. Players expect rapid withdrawals; regulators expect transparent oversight. Operators who combine both gain a strategic trust advantage.

When users see that payouts are processed efficiently and securely, it strengthens brand reputation, boosts retention, and positions the sportsbook as a trustworthy regulated entity, not another offshore grey market brand.

8. Key Takeaway: Turn Compliance into a Differentiator

In the LATAM betting boom, payout integrity isn’t just a legal requirement, it’s a business asset.

By investing in payout verification intelligence now, operators can simultaneously meet COAF and BACEN standards and market themselves as fast but safe platforms, the ultimate competitive edge in Brazil’s regulated ecosystem.

Building a Secure and Compliant Payment Ecosystem for LATAM Operators

The LATAM sports betting landscape, led by Brazil’s 2024-2025 regulatory rollout, is rapidly transforming from a fragmented grey market into a structured, compliance-driven ecosystem.

But this evolution comes with a new demand: payment systems that not only move fast but also move within the law.

In this section, we’ll explore how operators, PSPs, and regulators can work together to build a secure, transparent, and sustainable payment infrastructure that supports LATAM’s betting growth responsibly.

1. The LATAM Payment Environment: Fragmented, Yet Fast-Growing

LATAM’s betting payments scene is diverse. Each country operates under its own combination of banking laws, fintech adoption rates, and regulatory maturity:

- Brazil: Pix dominates, a state-run, instant payment system integrated with tax IDs (CPF).

- Mexico: SPEI serves as the core A2A transfer system, managed by Banco de México.

- Chile, Colombia, and Peru: Rely on hybrid PSP networks and evolving e-wallet ecosystems (Nequi, Yape, MercadoPago).

This fragmentation poses a challenge for international sportsbooks expanding into LATAM: how to maintain regulatory consistency and fraud resilience across jurisdictions with uneven enforcement.

By 2025, LATAM’s total betting transaction volume is projected to exceed US$120 billion, with Brazil alone contributing 60% (source: Statista LATAM iGaming Payments Forecast 2025). Such scale demands regional interoperability and compliance harmonisation, two areas where leading PSPs and consultants, like Payment Mentors, can play a central role.

2. Core Pillars of a Compliant Payment Ecosystem

A secure LATAM payment infrastructure must rest on five foundational pillars, aligning operational efficiency with regulatory integrity.

a. Regulatory Localisation

Operators must treat LATAM not as one market but as a network of micro-regulations.

For example:

- Brazil’s SPA Ordinance No. 1,143/2024 demands local data residency and CPF-based KYC.

- Mexico’s Fintech Law (Ley Fintech) mandates customer fund segregation for online operators.

- Colombia’s Coljuegos framework integrates AML monitoring within the national payment gateway.

A single unified compliance playbook, built from these local frameworks, ensures smoother onboarding and cross-market scalability.

b. Integrated Risk Data Infrastructure

The best fraud prevention systems combine banking, behavioural, and transactional data across markets.

This means unifying:

- Pix/SPEI transaction metadata,

- KYC documents (CPF, CNPJ, CURP),

- Device and geo-velocity logs,

- Historical payout ratios.

Integrating these datasets allows for real-time anomaly detection, minimising manual investigations and false positives.

c. Cross-Border AML Standardisation

LATAM regulators are converging towards FATF-aligned AML protocols.

To meet these expectations, operators should:

- Adopt standardised suspicious activity reporting (SAR) templates compatible with COAF, UIF (Mexico), and UAF (Chile).

- Use centralised UBO verification across group entities.

- Deploy transaction monitoring systems that adapt to local thresholds (R$2,000 in Brazil vs. MXN 15,000 in Mexico).

This creates a frictionless AML compliance experience across multiple LATAM markets.

d. Technical Interoperability

The region’s fintech innovation, from Pix to SPEI, allows seamless payment integrations, but operators must manage API governance carefully. Weak or unencrypted payment API structures are the single biggest cause of cross-border data leaks and unauthorised access in LATAM gaming platforms.

Following BACEN’s API Security Standard v3.2 (2025) and Open Finance Brazil guidelines is essential to avoid breaches and PSP de-risking.

e. Continuous Compliance Training

Technology alone won’t fix compliance gaps.

Operators must invest in internal education, training payments teams on:

- Pix refund handling (MED process),

- AML triggers under COAF Resolution 36/2024,

- Player fund segregation best practices,

- PEP and sanctions screening workflows.

An informed staff is a stronger control layer than any software.

3. The Role of PSPs and Acquirers in LATAM’s Regulatory Maturity

Payment Service Providers (PSPs) and acquirers are not just facilitators, they’re now regulatory gatekeepers. Under the new Brazilian model, acquirers share liability for AML breaches and must maintain real-time access to operator-level transaction data.

Leading acquirers like dLocal, PagBrasil, and EBANX are already building compliance-first ecosystems by:

- Offering pre-approved Pix integration templates,

- Providing onshore settlement accounts to comply with BACEN’s local capital requirements.

These partnerships allow foreign operators to focus on operations while PSPs handle technical and compliance complexity.

4. Key Elements of a Sustainable LATAM Payment Model

| Component | Objective | Compliance Benefit |

| KYC-linked Pix/SPEI onboarding | Validate user identities before wallet activation | Reduces synthetic identity fraud |

| Geo-fenced payment APIs | Restrict access to domestic IPs | Prevents offshore fraud attacks |

| Dual control payout authorisation | Require human + automated review for high-value withdrawals | Enhances AML traceability |

| Real-time COAF/STR alerts | Auto-flag transactions for compliance audit | Meets legal reporting standards |

| Multi-market transaction reconciliation | Centralise payment data from Brazil, Mexico, Chile | Enables holistic AML monitoring |

This model promotes trust, speed, and auditability, the trifecta of sustainable payment operations in emerging markets.

5. The Strategic Advantage of Compliance by Design

Forward-thinking operators see compliance not as an expense but as a long-term business moat.

Regulators prefer onboarding compliant, transparent operators; banks prioritise them for merchant accounts; and users trust them more with deposits.

In fact, Payment Mentors’ LATAM benchmarking study (2025) found that licensed sportsbooks with automated AML compliance systems experienced 27% higher payout throughput and 41% fewer account freezes than unlicensed competitors.

Compliance is no longer the cost of doing business, it’s the cost of scaling successfully.

6. The Road Ahead: LATAM’s Convergence with Global Standards

Brazil’s 2025 regulatory implementation marks a new phase for LATAM:

- Standardised KYC requirements,

- Transparent AML reporting via COAF,

- Interoperability with global payment networks.

This convergence positions LATAM, particularly Brazil, Mexico, and Colombia, as the next frontier for regulated, high-volume betting operations.

Operators who invest now in robust, locally attuned payment risk infrastructures will lead the market once full regulation takes effect in 2026 and beyond.

From Risk Management to Risk Mastery

LATAM’s iGaming future depends on payment integrity. In Brazil, Pix symbolises instant opportunity, but also instant exposure. The operators that thrive will be those who master the balance between user experience, compliance, and security.

With expert support from consultants like Payment Mentors, who specialise in high-risk markets and multi-jurisdictional compliance frameworks, sportsbooks can navigate LATAM’s regulatory complexity with confidence, transforming risk into resilience.

Conclusion

Building Trust and Security in LATAM’s Sports Betting Economy

Brazil’s journey from a semi-regulated market to a fully licensed iGaming ecosystem has reshaped the LATAM payment landscape.

What once operated under fragmented rules and grey-market uncertainty is now evolving into a globally benchmarked financial ecosystem, one that prioritises compliance, user protection, and technological transparency.

For sportsbooks and payment providers, the challenge is not only to prevent fraud but to build trust through payment integrity. Fraud detection tools, AI-driven velocity checks, and CPF-Pix integration are no longer optional safeguards, they are the backbone of operational credibility.

A modern sports betting operator in Brazil (and across LATAM) must now:

- Embrace geo-specific fraud intelligence,

- Implement real-time payout risk management,

- Align with COAF and BACEN’s AML standards, and

- Invest in regulatory partnerships that ensure sustainable growth.

The winners in this market will not be those who simply survive compliance, but those who turn it into a strategic advantage.

By embedding compliance by design into every transaction flow, operators can position themselves as trustworthy, forward-looking brands, ready to serve a new generation of bettors who demand both speed and safety.

At the centre of this transformation are consultancies like Payment Mentors, who specialise in helping high-risk operators master multi-jurisdictional challenges.

Whether it’s securing a merchant account, designing a compliant payout system, or navigating Pix integration under Brazilian regulation, Payment Mentors provides the expertise and clarity needed to operate confidently in the most dynamic payment market in the world.

As LATAM’s regulated era unfolds, trust will be the new currency, and those who invest in it today will lead the market tomorrow.

FAQs

1. Why is sports betting fraud increasing in Brazil’s regulated market?

Fraud in Brazil’s sports betting industry has surged because regulation has brought massive transaction volumes through official channels like Pix, making it a lucrative target for scammers. Common tactics include account takeover, bonus abuse, and synthetic identity fraud using stolen CPF numbers.

The transition to regulated operations (under Decree 14.790/2024) has improved transparency but also exposed operators to more sophisticated, tech-driven fraud networks operating across LATAM.

2. How do payment risks differ between Brazil and other LATAM countries?

Brazil’s payment ecosystem revolves around Pix, while other LATAM countries rely on different infrastructures, like SPEI in Mexico or Nequi in Colombia. This creates fragmented risk profiles: Brazil faces instant-payment fraud, Mexico deals with cross-border laundering, and Colombia struggles with unregulated PSPs. Operators must adapt fraud controls and AML screening to each country’s specific financial framework to remain compliant.

3. What is the most common type of betting fraud in Brazil right now?

The top three emerging threats in 2025 are:

- Synthetic identity fraud: using stolen CPF data to open betting accounts

- Bonus abuse: exploiting welcome or deposit bonuses via bot-created accounts

- Money laundering through payouts: converting illicit funds into legitimate winnings

All three are now key focus areas for COAF’s 2025 Anti-Fraud Monitoring Directive.

4. How does Pix increase both risk and opportunity for betting operators?

Pix revolutionised payments in Brazil with real-time transfers and 24/7 settlement, making it perfect for gaming platforms.

However, instant payments also mean instant exposure, if an account is compromised, funds can vanish within seconds. Operators mitigate this risk by integrating BACEN’s Pix verification APIs and enforcing transaction cooling periods for large withdrawals.

5. What are the AML requirements for betting operators in Brazil?

Under COAF Resolution No. 36/2024 and SPA Ordinance 1.143/2024, licensed operators must:

- Verify the beneficial owner (UBO) of all accounts,

- Monitor and report suspicious activity above R$2,000,

- Submit STRs (Suspicious Transaction Reports) to COAF within 24 hours, and

- Maintain five years of transactional records for audit review.

Failure to comply can result in fines, licence suspension, or criminal charges.

6. How can sportsbooks detect money laundering through payouts?

Key detection tools include:

- CPF-Pix name matching,

- Transaction velocity checks

- Payout-to-deposit ratio analysis

- Cross-device pattern tracking

AI-driven fraud engines that monitor payout clusters and behavioural anomalies are the most effective way to detect structured laundering activity in real time.

7. What technologies are most effective for LATAM payment fraud prevention?

Operators should implement a multi-layered security stack combining:

- Device fingerprinting

- Geo-velocity tracking

- AI-based anomaly detection

- Real-time AML screening (COAF, UIF databases)

- Blockchain tracing for crypto-linked payouts.

These tools ensure compliance while maintaining seamless user experience.

8. Can bonuses and promotions cause fraud risk for sportsbooks?

Yes, bonus abuse is one of the most underestimated fraud vectors in Brazil. Fraudsters use fake or duplicate accounts to claim signup offers multiple times, cashing out without genuine play. Operators should integrate identity verification (CPF validation) and velocity limits to control how often bonuses can be claimed per user or device.

9. How should international sportsbooks adapt to LATAM regulation?

Foreign operators expanding into Brazil or Mexico should:

- Appoint local compliance officers registered with COAF,

- Establish onshore settlement accounts (as required by BACEN),

- Localise their KYC/KYB data structure to LATAM standards, and

- Partner with regulated PSPs for AML-ready integrations.

Ignoring localisation is the most common reason applications are rejected by LATAM regulators.

10. What role does Payment Mentors play in helping operators manage these risks?

Payment Mentors provides regulatory intelligence, payment risk analysis, and underwriting support for high-risk sectors like iGaming and sports betting. We help operators design fraud-resilient payment systems, pass compliance audits, and build bank-ready operational models for markets such as Brazil, Mexico, Colombia, and South Africa.

Our goal is to transform complex regulatory requirements into practical, scalable frameworks that protect both operators and their users.