For many merchants, payments only become a serious topic once something stops working. In the early stages, a PSP is often chosen because it is quick to integrate and easy to operate. Transactions are approved, funds settle, and the system feels reliable enough. It is only when the business starts looking beyond its initial market that the consequences of that early choice begin to surface.

Expansion changes how payments behave. New markets introduce different issuer expectations, regulatory requirements, and customer habits, all of which place pressure on the payment stack. Processes that were invisible at lower volumes authentication handling, settlement timing, dispute flows, data availability become operational concerns rather than background mechanics.

At that point, the risk is rarely that a PSP fails outright. More often, it becomes harder to understand why performance shifts, why approval rates soften, or why cash flow becomes less predictable. These issues tend to appear gradually, which makes them easy to misdiagnose as market problems rather than structural ones.

Aligning PSP selection with long-term growth means recognising that payments infrastructure must remain stable as variation increases. The right choice is not the one that works today, but the one that continues to behave predictably as the business expands.

- PSP Selection Is an Operating Model Decision, Not a Procurement One

- What Actually Changes When Merchants Expand Into New Markets

- Aligning PSP Capabilities With Long-Term Growth Requirements

- Where PSP Selection Commonly Breaks During Expansion

- Designing PSP Selection Around Control, Portability, and Resilience

- Growth Without Fragmentation: Managing Multiple Markets Cohesively

- Merchant Readiness Check: Is Your PSP Stack Built for Expansion?

- Conclusion

- FAQs

PSP Selection Is an Operating Model Decision, Not a Procurement One

When merchants first select a PSP, the decision is often treated like a procurement exercise. The focus sits on features, pricing, integration effort, and whether the provider can support the immediate launch plan. Those factors matter, but they only describe how payments will function under stable, familiar conditions.

In reality, a PSP shapes the operating model behind every transaction. It determines where decision-making lives, how much visibility exists once something deviates from the expected path, and how easily payment behaviour can be adjusted as conditions change. These characteristics are rarely obvious at the start, because they only come into play when scale introduces variation.

As growth accelerates or new markets are added, the payments system is asked to do more than authorise transactions. It must cope with different issuer responses, shifting regulatory demands, uneven settlement behaviour, and changes in customer payment habits. At that stage, limitations are no longer abstract. They affect how quickly issues can be identified, how confidently risk can be managed, and how predictable outcomes remain.

Seen through this lens, PSP selection is less about buying a service and more about defining how payments will be governed over time. Choices made early establish boundaries around control, flexibility, and resilience. Those boundaries tend to persist long after the initial decision is forgotten.

What Actually Changes When Merchants Expand Into New Markets

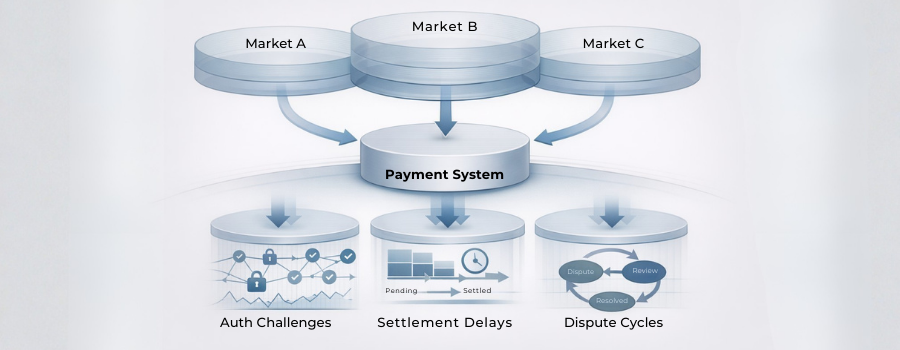

Market expansion does not simply add volume. It introduces variation, and payments systems are particularly sensitive to it. Issuers respond differently by region, customer expectations around authentication shift, and regulatory requirements begin to influence how transactions are challenged or approved. Behaviour that once looked consistent starts to fragment.

One of the first changes merchants notice is in authorisation performance. The same transaction profile can produce different outcomes depending on where the card is issued or how local networks interpret risk. Declines become harder to explain, especially when decisioning logic is abstracted away. At the same time, authentication steps that were rarely triggered in a domestic setup may become routine in certain markets, altering conversion in ways that are difficult to predict.

Settlement behaviour also changes. Expansion introduces new currencies, different clearing cycles, and variations in how quickly funds become available. What was once a straightforward settlement flow can turn into a set of parallel timelines, each with its own liquidity implications. Refunds and disputes follow similar patterns, with timeframes and customer behaviour diverging by market.

Operationally, this means payments stop behaving like a single system. Without deliberate design, they become a collection of loosely connected processes that are harder to monitor and manage.

In practice, expansion changes payments in a few consistent ways:

Authorisation outcomes become market-dependent rather than uniform

Authentication frequency and friction increase unevenly

Settlement and cash availability lose predictability

Refund and dispute behaviour diverge across regions

Aligning PSP Capabilities With Long-Term Growth Requirements

Once expansion introduces variation, the limitations of early PSP choices become clearer. Capabilities that felt secondary at launch begin to matter because they influence how much control a merchant has as complexity increases. The challenge is not identifying every possible future requirement, but understanding which capabilities determine whether the payments system remains adaptable over time.

Control Versus Convenience in Early PSP Choices

Convenience-led PSP selection tends to optimise for speed and simplicity. Integration is fast, configuration is minimal, and many decisions are handled on the merchant’s behalf. This approach works well while payment behaviour remains predictable. As markets are added, however, convenience often comes at the cost of visibility and control.

When transaction routing, authentication handling, or decline logic cannot be adjusted, merchants are left reacting to outcomes rather than managing them. Diagnosing why performance shifts becomes difficult, particularly when behaviour differs by market. What was once an acceptable abstraction starts to feel like an operational blind spot.

Market Expansion Requires Predictability, Not Just Coverage

PSP coverage is often described in terms of how many countries or payment methods are supported. Coverage alone, however, does not guarantee consistency. Expansion places value on predictable behaviour across markets: similar decline handling, comparable authentication experiences, and settlement flows that can be understood and forecast.

Capabilities that support this predictability, such as consistent data access, stable processing logic, and clear separation between markets tend to matter more than headline reach. Without them, each new region adds operational noise rather than controlled complexity.

In practice, aligning PSP capabilities with growth means prioritising characteristics that hold steady as markets change:

- Clear visibility into transaction and decline behaviour

- The ability to manage authentication and routing consistently

- Settlement structures that remain understandable as currencies and regions increase

- Sufficient flexibility to adjust the model without rebuilding it

Where PSP Selection Commonly Breaks During Expansion

Breakdowns in PSP alignment rarely appear as sudden failures. More often, they emerge as small shifts that accumulate as new markets come online. Because these changes happen gradually, they are easy to attribute to external factors such as customer mix or regional demand, rather than to structural constraints within the payment setup itself.

One common pressure point is authorisation quality. As issuers and networks apply market-specific risk models, approval rates can soften in ways that are difficult to diagnose. Without clear insight into decline reasons or the ability to adjust decisioning behaviour, merchants are left with limited options beyond accepting lower performance or escalating issues without meaningful context.

Authentication introduces a different set of challenges. Requirements vary by region, and customer tolerance for friction differs by market. When authentication logic is rigid or opaque, step-ups can occur more frequently than expected, undermining conversion without a clear explanation. Over time, this erodes confidence in the payments system as a controllable component of the business.

Settlement and liquidity pressures often follow. Expansion increases the number of settlement paths, each with its own timing, currency exposure, and reserve behaviour. Delays or unexpected holds become harder to anticipate, complicating cash flow planning. At scale, even small inconsistencies in settlement timing can have material operational consequences.

Finally, reconciliation and reporting strain under growth. As transactions span more regions and entities, fragmented data makes it harder to form a coherent view of performance and risk. What was manageable at a lower scale becomes a source of ongoing operational drag.

Designing PSP Selection Around Control, Portability, and Resilience

As expansion increases variation, the role of the PSP shifts. It is no longer just a processing layer, but part of the control surface through which risk, performance, and liquidity are managed. Designing for growth means paying attention to where control sits and how easily the payments model can adapt when conditions change.

Control starts with visibility. When transaction outcomes, decline reasons, authentication results, and settlement movements can be observed at a granular level, issues become diagnosable rather than speculative. Without that visibility, merchants are left inferring behaviour from symptoms, which slows response and increases operational risk. Over time, the absence of clear data becomes more limiting than any individual feature gap.

Portability matters for similar reasons. Expansion is rarely linear, and priorities change as markets perform differently from expectations. If the payments setup cannot be adjusted, rebalanced, or exited without significant disruption, early choices harden into long-term constraints. Portability does not imply frequent change, but it preserves the option to change when circumstances demand it.

Resilience ties these elements together. A resilient payments model absorbs market-specific shocks without destabilising the wider system. This depends less on redundancy and more on clarity: knowing which parts of the flow can fail, how failures are contained, and how quickly normal behaviour can be restored.

In practical terms, PSP selection that supports long-term growth tends to share a few characteristics:

Consistent access to transaction-level data across markets

Clear separation between market-specific behaviour and core processing

Settlement structures that remain understandable as complexity grows

The ability to adjust or unwind the setup without rebuilding it entirely

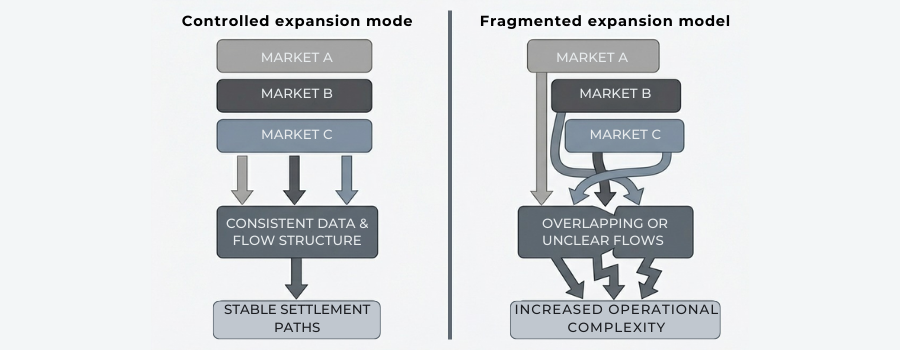

Growth Without Fragmentation: Managing Multiple Markets Cohesively

One of the less visible risks of expansion is fragmentation. As new markets are added, payments can begin to behave differently in each region, even when the customer experience appears consistent on the surface. Over time, this creates a system where performance, risk exposure, and operational effort vary in ways that are difficult to reconcile.

Fragmentation often develops unintentionally. PSP configurations are adjusted to accommodate local requirements, regulatory expectations, or issuer behaviour, but those changes are not always reflected elsewhere in the system. What starts as a reasonable market-specific adjustment can gradually erode consistency across the wider payments operation.

The impact is rarely immediate. Merchants may notice that some regions require more manual intervention, that reporting no longer aligns cleanly, or that customer outcomes differ despite similar transaction profiles. As this divergence grows, payments become harder to manage as a single system and more difficult to govern with confidence.

Managing growth cohesively does not mean forcing uniformity across markets. It means ensuring that differences are deliberate, visible, and controlled. PSP selection plays a central role in this, as it determines whether market-level variation can be absorbed without fragmenting the underlying operating model.

When payments remain cohesive under expansion, merchants retain the ability to assess performance holistically, respond to issues proportionately, and plan growth without accumulating hidden operational debt.

Merchant Readiness Check: Is Your PSP Stack Built for Expansion?

By the time expansion is being discussed seriously, most merchants already have a PSP in place. The question is rarely whether payments work, but whether the current setup will continue to behave predictably as new markets introduce variation. This is where assumptions made earlier start to matter.

Readiness, in this context, is not about volume or ambition. It is about whether the existing PSP stack exposes enough of its behaviour to be managed as complexity increases. Expansion tends to surface issues gradually, which makes it easy to underestimate how structural they are. A short pause to validate those assumptions can prevent misattributing future friction to market conditions rather than to design constraints.

What matters most is not how many features are available, but how the system responds when conditions diverge across regions. If behaviour changes cannot be observed, compared, or explained, control is already limited. That limitation becomes more pronounced as more markets are added.

A useful sense check before expansion is to ask:

- Can payment performance and decline behaviour be clearly understood on a per-market basis?

- Does authentication behaviour remain visible and explainable as requirements change?

- Is settlement timing predictable enough to support cash flow planning across regions?

- If priorities shift, is it realistically possible to rebalance or change the setup?

If these questions are difficult to answer with confidence, expansion may still be possible, but it is unlikely to be smooth. In most cases, the issues that surface later are not new problems, but existing constraints finally being put under pressure.

Conclusion

PSP selection has long-term consequences that are easy to overlook at the point of launch. As merchants expand into new markets, early decisions begin to influence not just acceptance, but how variation is managed, how quickly issues can be understood, and how predictable outcomes remain under pressure.

Expansion rarely causes payments to fail outright. More often, it exposes constraints that were already present but invisible at lower scale. Declining approval rates, inconsistent settlement behaviour, and rising operational effort are usually symptoms of a payment model that was not designed for divergence.

Aligning PSP selection with long-term growth means moving beyond feature comparisons and thinking in terms of operating stability. Merchants that treat PSP choice as a structural decision are better positioned to expand without accumulating hidden complexity or losing control as markets change.

FAQs

1. Why does PSP selection matter more as merchants expand into new markets?

Because expansion introduces variation. Different issuer behaviour, regulatory requirements, and settlement models place stress on payment systems that were designed for a simpler environment. A PSP that works well domestically may struggle to handle this added complexity predictably.

2. Can a PSP that performs well today become a limitation later?

Yes. Limitations often emerge gradually as volume increases or new regions are added. Reduced visibility, rigid authentication handling, or inconsistent settlement behaviour typically surface only once the payment model is under pressure.

3. Is PSP selection mainly a technical decision?

No. While technical capability matters, PSP selection ultimately defines how payments are governed. It shapes control, data access, and the ability to respond when behaviour changes across markets.

4. Does market expansion always require changing PSPs?

Not necessarily. Some PSP setups can support expansion effectively. The key factor is whether the existing model can absorb variation without fragmenting performance, reporting, or cash flow management.

5. How does PSP choice affect authorisation rates during expansion?

Issuer responses and risk models vary by region. If decline behaviour cannot be analysed or adjusted at a market level, approval rates may soften without a clear explanation or corrective path.

6. What role does authentication play when scaling into new markets?

Authentication requirements differ across regions, and customer tolerance for friction varies. PSPs that offer limited visibility or control over authentication flows can unintentionally increase step-ups and reduce conversion.

7. Why is settlement behaviour a concern during expansion?

Adding markets often introduces new currencies, clearing cycles, and reserve structures. Without predictable settlement behaviour, cash flow planning becomes more difficult as complexity grows.

8. How important is data access when selecting a PSP for growth?

Data access is critical. Transaction-level visibility allows merchants to understand performance shifts, diagnose issues, and manage risk as conditions change. Without it, decisions are made with incomplete information.

9. What does portability mean in the context of PSP selection?

Portability refers to how easily a payments setup can be adjusted, rebalanced, or exited if priorities change. It preserves optionality and prevents early decisions from becoming long-term constraints.

10. Is using a single PSP risky for long-term expansion?

A single-PSP model can work, but only if it maintains consistent behaviour and sufficient control as markets are added. Risk arises when expansion creates fragmentation that cannot be managed within the existing setup.

11. When should merchants reassess whether their PSP is still fit for purpose?

Reassessment is most valuable before entering new markets or significantly increasing complexity. Waiting until performance degrades often means addressing issues reactively rather than structurally.

12. What is the biggest mistake merchants make when choosing a PSP for growth?

Treating PSP selection as a short-term enablement decision. The most common issues during expansion stem from early choices that did not account for how payments behave as variation and scale increase.