By 2026, many merchants have proven that open banking payments can convert well, reduce certain costs, and deliver faster confirmation than traditional card rails in a single market. The challenge now is scaling that success across multiple countries without introducing inconsistency, customer confusion, or operational risk.

This matters because open banking behaves very differently once it crosses borders. Bank coverage varies by market, customer consent journeys are not uniform, instant payment rails operate under different scheme rules, and refund expectations rarely align with card-based assumptions. Merchants that treat open banking as a simple alternative payment method often discover these gaps only after support volume increases and confidence starts to erode.At the same time, regulatory and infrastructure momentum is raising expectations. In the UK, open banking is increasingly framed as a mainstream payment capability. Across the EU, instant credit transfer requirements are pushing account-to-account payments toward higher standards of speed and reliability. Customers now expect pay by bank to work predictably wherever it is offered.

- What Scaling Open Banking Payments Actually Means for a Merchant

- Why Pay by Bank Behaves Differently in Every Market

- Where Multi-Market Pay by Bank Rollouts Fail in Practice

- The 2026 Operating Model: Build One Payment Product, Localise the Control Layer

- How High-Performing Merchants Are Scaling Successfully

- Instant Payments and Open Banking: Why Faster Rails Change Merchant Risk

- Fraud and Authorised Push Payment Risk: Scaling Without Losing Trust

- UK vs EU Reality: What Merchants Must Not Assume When Scaling

- Merchant Checklist: Are You Ready to Scale Pay by Bank Across Markets?

- Conclusion

- FAQs

What Scaling Open Banking Payments Actually Means for a Merchant

For most merchants, scaling open banking payments does not mean increasing transaction volume. It means delivering the same outcome for customers and operations as the payment expands into new markets. That outcome includes predictable completion, clear confirmation, and confidence that the payment has genuinely succeeded.

In a single market, merchants can often manage variation informally. Customer expectations are familiar, bank coverage is well understood and operational teams know where edge cases sit. Once open banking is deployed across multiple markets, those assumptions break down. Completion rates vary by bank, consent flows differ and settlement timing may no longer feel consistent to customers or fulfilment teams.

This is why scaling open banking is fundamentally about consistency rather than reach. A payment method that works technically but behaves differently by country creates friction that customers interpret as unreliability. Over time, that perception undermines adoption, even if the underlying rails are sound.

From a merchant perspective, successful scaling is measured by whether open banking behaves as a dependable payment option across markets, not as a collection of local exceptions.

In practice, scaling open banking requires merchants to manage:

- Market-by-market coverage and reachability

- Checkout completion and abandonment patterns

- Consistency of confirmation and settlement signals

- Refund handling expectations across markets

- Reconciliation accuracy as volumes increase

Why Pay by Bank Behaves Differently in Every Market

Although pay by bank is often discussed as a single capability, it behaves very differently once it moves across borders. Open banking is built on local banking infrastructure and those foundations vary significantly by market. The result is that customer experience, payment certainty, and operational handling are shaped as much by geography as by technology.

One source of variation is bank participation. In some markets, open banking coverage is broad and familiar to consumers. In others, coverage is fragmented, connections are less stable, or customer awareness is lower. From a merchant perspective, this can look like inconsistent completion rates even when the checkout experience appears identical.

Instant payment rails introduce further complexity. While instant credit transfers are becoming more widely available, scheme rules, cut-off times and exception handling differ by country. A payment that confirms in seconds in one market may behave more cautiously in another, creating challenges for fulfilment and customer communication.

Consent and authentication journeys also differ. Redirection flows, approval steps and return behaviour are not standardised, which means customers encounter subtly different experiences depending on their bank and location. When those differences are not anticipated, they are often perceived as payment failure rather than local variation.

For merchants, the implication is clear. A single, uniform pay by bank experience rarely scales cleanly. Successful expansion depends on recognising that local banking behaviour shapes payment outcomes, and designing systems that absorb those differences without exposing them to the customer.

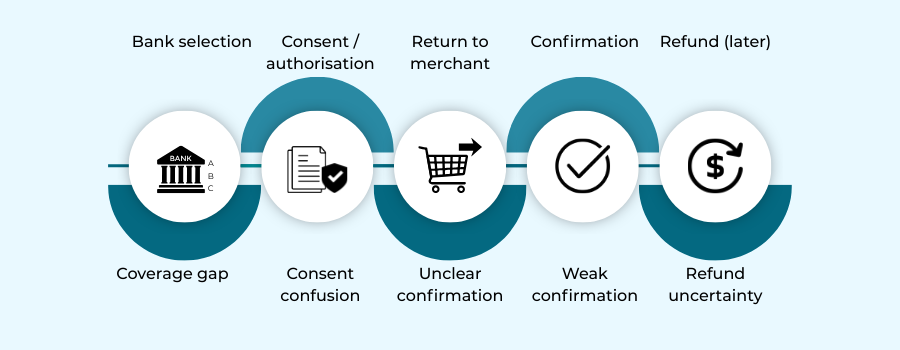

Where Multi-Market Pay by Bank Rollouts Fail in Practice

Most multi-market open banking rollouts do not fail because the technology is unavailable. They fail because the payment behaves differently from what merchants and customers expect once it is live at scale. These issues tend to surface only after launch, when real users interact with real banks under real conditions.

Coverage gaps that look like choice but behave like declines

In some markets, open banking coverage is broad and dependable. In others, key banks are missing, connections are unstable, or customers are unfamiliar with the flow. When these gaps are not surfaced clearly at checkout, customers experience them as unexplained failure rather than limited availability. What looks like customer choice on paper behaves like a decline in practice.

Customer journey breaks at consent and return

Open banking relies on redirection and consent, but those journeys are not uniform. Customers may struggle to understand what is happening, fail to complete authorisation, or not return cleanly to the merchant site. Weak confirmation messaging amplifies this problem, leaving customers unsure whether payment has actually succeeded.

Refund expectations copied from cards

Many merchants apply card-based refund assumptions to account-to-account payments. When refund timing, method, or reversibility differs, customers feel misled. That mismatch often results in increased support contacts and reduced trust in pay by bank as a reliable option.

In practice, multi-market rollouts break down around the same friction points:

- Inconsistent bank coverage and reachability

- Confusing consent, redirection, or return flows

- Weak or delayed payment confirmation

- Refund handling that does not match customer expectations

- Reconciliation mismatches across markets

These failures are rarely catastrophic on their own. Over time, however, they erode confidence and stall adoption, even when open banking works technically.

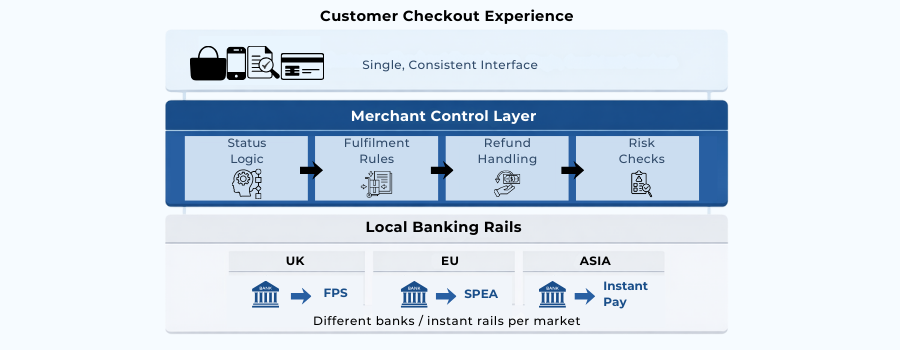

The 2026 Operating Model: Build One Payment Product, Localise the Control Layer

Merchants that scale open banking successfully do not treat each market as a separate payment product. They build a single core payment experience and localise the control layer around it. This distinction is subtle, but it is what allows consistency to survive expansion.

The core product defines what pay by bank means to the customer: how the option is presented, what confirmation looks like, and how payment status is communicated. That experience remains stable across markets. What changes is how the system manages local behaviour underneath. Coverage rules, routing logic, settlement timing, refund handling, and exception management are adapted to the realities of each banking environment without exposing that complexity to the user.

This operating model matters because most friction in multi-market rollouts does not come from checkout design. It comes from edge cases: delayed confirmations, partial failures, refunds that behave differently by country, or reconciliation that breaks once volumes increase. Localising the control layer allows these differences to be handled deliberately rather than reactively.

In 2026, scaling open banking is less about standardisation at all costs and more about controlled variation. Merchants that separate customer experience from local payment mechanics are better able to expand without creating confusion in operational strain or loss of trust.

How High-Performing Merchants Are Scaling Successfully

Merchants that have scaled open banking payments across multiple markets successfully tend to share one characteristic: they design for operational clarity, not just checkout completion. Their focus is on ensuring that payments behave predictably once real customers, real banks, and real exceptions are involved.

Designing checkout around reassurance, not redirection

High-performing merchants recognise that open banking redirection can feel unfamiliar. Rather than treating it as a technical step, they design checkout messaging to explain what will happen next, what the customer should expect to see, and how confirmation will be delivered. Clear reassurance reduces abandonment and support queries, especially in markets where pay by bank is still gaining familiarity.

Building confirmation you can operationalise

Successful scaling depends on treating payment status precisely. Merchants distinguish clearly between a payment being initiated, authorised, and completed. Fulfilment rules are aligned to the appropriate confirmation level, avoiding situations where goods or services are released before certainty exists. This discipline becomes critical as volumes grow and instant and non-instant rails coexist.

Making refunds and reversals predictable

Merchants that maintain trust handle refunds explicitly. Customers are told how refunds will be processed, how long they may take, and whether the funds will return automatically or require action. Internally, refund logic is adapted to local banking behaviour rather than copied from card workflows.

Across successful multi-market implementations, several execution patterns recur:

Clear payment status states exposed in the customer journey

Fulfilment decisions tied to confirmation certainty

Refund communication aligned to local expectations

Defined exception paths for delayed or failed payments

These practices do not eliminate complexity, but they prevent that complexity from reaching the customer, which is what allows adoption to scale sustainably.

Instant Payments and Open Banking: Why Faster Rails Change Merchant Risk

Instant payment rails are often framed as a pure improvement: faster confirmation, better customer experience, and reduced uncertainty. In practice, they change the merchant risk profile as much as they improve speed.

When payments confirm in seconds, customer confidence increases. There is no waiting period and no ambiguity about whether funds will arrive. However, that same immediacy compresses the window for fraud detection, review and intervention. Once an instant payment settles, reversal options are limited and highly dependent on cooperation between banks.

This creates a different operational challenge from card payments. With cards, merchants often have time to identify anomalies before fulfilment or settlement completes. With instant account-to-account payments, risk controls must operate in real time. Decisions about whether to release goods, services, or access need to be aligned tightly with confirmation certainty.

As instant payments become more widely available across Europe, customer expectations are also shifting. Delays that were once tolerated now feel like failures. Merchants scaling open banking across markets therefore need to balance two pressures: delivering the speed customers expect, while ensuring controls are strong enough to prevent irreversible loss.

In 2026, successful merchants treat instant rails as a different risk environment, not just a faster version of existing payments. They adapt monitoring, fulfilment timing, and exception handling to match the realities of irrevocable, real-time settlement.

Fraud and Authorised Push Payment Risk: Scaling Without Losing Trust

As open banking payments scale, fraud risk does not disappear, it changes shape. Account-to-account payments reduce certain card-based risks, but they introduce greater exposure to authorised push payment (APP) fraud, where customers are manipulated into approving transfers themselves.

This matters because APP fraud sits in a sensitive space for merchants. The payment is technically authorised, yet the customer still experiences loss. As a result, trust is affected not only by whether fraud occurs, but by how merchants communicate, detect, and respond when it does.

Regulators and industry bodies across Europe have increasingly highlighted that prevention, rather than reimbursement alone, is central to managing APP risk. This places pressure on merchants to recognise suspicious behavioural signals before payment initiation completes, rather than relying on post-transaction remediation. In multi-market environments, this challenge is amplified by differing fraud patterns, consumer awareness levels, and bank-side controls.

Merchants scaling successfully avoids framing open banking as low-fraud by default. Instead, they design layered protections around payment initiation, customer messaging, and fulfilment timing. Clear warnings at the right moment, consistent confirmation language, and realistic expectations about irreversibility all play a role in maintaining trust.

In 2026, confidence in pay-by-bank payments depends not on promising zero fraud, but on demonstrating that risks are understood, monitored, and handled responsibly across every market where the payment is offered.

UK vs EU Reality: What Merchants Must Not Assume When Scaling

Merchants often assume that success with open banking in the UK can be replicated across the EU with minimal adjustment. In practice, the two environments behave very differently, and those differences become more pronounced at scale.

The UK: Open Banking maturity and emerging VRPs

The UK market benefits from relatively high consumer familiarity with open banking and a more standardised ecosystem. Payment initiation journeys are well understood, and regulatory momentum is pushing toward broader use cases, including Variable Recurring Payments (VRPs). For merchants, this creates an environment where pay by bank can increasingly support repeat use and predictable customer behaviour. However, expectations around speed and confirmation are also higher, leaving little tolerance for inconsistent execution.

The EU: Fragmentation and instant payments momentum

In the EU, open banking adoption and instant payment availability vary widely by country. While regulatory initiatives are accelerating SEPA Instant reachability, customer experience remains uneven. Merchants must account for differences in bank behaviour, consumer trust, and settlement timing. A model that works smoothly in one EU market may behave very differently in another.

The key mistake is assuming convergence has already happened. In 2026, scaling successfully requires recognising that the UK and EU are moving in the same direction, but not at the same pace or in the same way.

Merchant Checklist: Are You Ready to Scale Pay by Bank Across Markets?

Use this checklist to validate whether your open banking payment setup is designed to scale without eroding customer trust or operational control.

- Customer journeys explain what happens next

Consent, redirection, return, and confirmation are communicated clearly so customers are not left guessing. - Refund handling is predictable and market-aware

Refund timelines, methods, and limitations are aligned to local A2A behaviour, not copied from card flows. - Risk controls operate in real time

Monitoring and decisioning reflect the irreversible nature of instant payments and APP fraud exposure.

If most of these conditions are met, pay by bank is positioned as a reliable, scalable payment option rather than a market-specific experiment.

Conclusion

Scaling open banking payments across multiple markets is no longer about proving that pay by bank works. That question has already been answered. In 2026, the real challenge is whether the payment behaves consistently enough to earn trust as it expands into new banking environments.

Merchants that succeed are not those that deploy the widest coverage fastest, but those that design open banking as a dependable payment product. They recognise that customer confidence is shaped by what happens around the payment: clear confirmation, predictable refunds, and reassurance when something does not go exactly as planned. These details determine whether pay by bank is perceived as reliable or risky.

As instant payment rails become the norm and regulatory momentum continues to push account-to-account payments forward, expectations will only rise. Merchants that invest in operating models built for variation, rather than assuming uniformity, will be best positioned to scale. In open banking, sustainable growth belongs to those who prioritise consistency and trust over speed of rollout.

FAQs

1. Why is scaling open banking payments harder than launching them in one market?

Because open banking behaviour varies by country. Bank coverage, consent journeys, instant payment availability, and refund handling differ across markets, making consistency harder to maintain at scale.

2. What does “scaling pay by bank” actually mean for merchants?

It means delivering predictable outcomes across markets: reliable completion, clear confirmation, understandable customer journeys, and operational confidence in refunds and reconciliation.

3. Why do pay-by-bank completion rates vary by country?

Differences in bank participation, customer familiarity, consent flows, and instant payment infrastructure all affect how reliably payments complete in each market.

4. How do instant payments change merchant risk?

Instant payments reduce uncertainty for customers but compress the time available for fraud detection and intervention. Once funds settle, reversals are limited, requiring real-time controls.

5. Why do customers sometimes distrust pay-by-bank payments?

Distrust usually stems from uncertainty. Unclear confirmation, confusing redirection, or vague refund expectations can make customers feel the payment has failed even when it has not.

6. Are open banking refunds the same as card refunds?

No. Account-to-account refunds behave differently from card refunds. Applying card-based assumptions often leads to confusion, delays, and increased support contact.

7. What role does customer communication play in adoption?

A significant one. Clear messaging around what happens next, when confirmation occurs, and how refunds work reduces abandonment and builds confidence, especially in newer markets.

8. How does authorised push payment (APP) fraud affect open banking adoption?

APP fraud shifts responsibility toward prevention and customer awareness. Merchants must design controls and messaging that reduce manipulation without undermining trust in the payment method.

9. Can the same pay-by-bank experience be used in the UK and EU?

Not reliably. The UK has higher maturity and emerging recurring use cases, while the EU remains more fragmented. Merchants must adapt control layers even if the core experience looks similar.

10. What is the biggest mistake merchants make when scaling open banking?

Treating it as a checkout feature rather than an operating model. Most failures come from post-payment handling, not from the initial payment initiation.

11. Does wider bank coverage automatically mean better scaling?

No. Coverage without clear journeys, confirmation logic, and refund handling can increase confusion rather than adoption.

12. What signals that a merchant is ready to scale pay by bank across markets?

When payment status drives fulfilment, refund behaviour is predictable, customer journeys are clearly explained, and risk controls operate in real time across all markets.