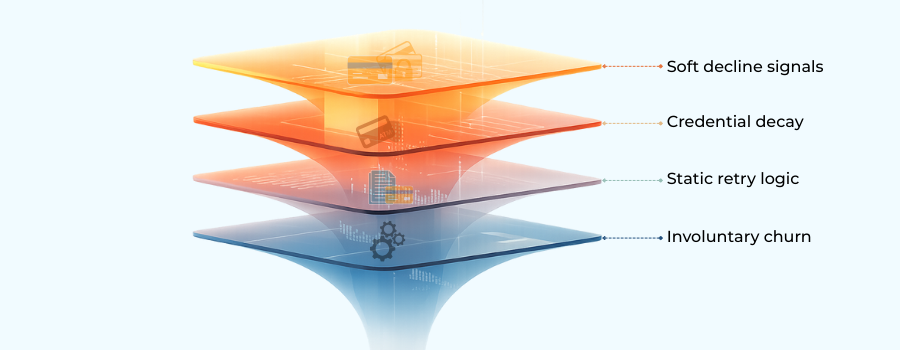

For modern subscription businesses, renewal failure in 2026 is increasingly disconnected from customer intent. Many customers still want the service, but the payment that enables renewal fails silently in the background. What was once treated as a churn or retention issue has become a systems-level payment problem.

This shift matters because involuntary churn now represents a growing share of lost recurring revenue. Issuers apply tighter controls to recurring transactions, card lifecycles are shorter, and renewal payments are processed without a customer present to correct errors. Card networks themselves acknowledge that a significant portion of recurring payment failures stem from soft declines technical signals of caution rather than a genuine inability to pay.

As a result, subscription businesses can no longer rely on legacy set-and-forget billing models. A renewal attempt is not just another transaction; it is a high-risk payment moment that demands deliberate design.

In response, leading subscription businesses are rethinking how payments support renewals. Instead of focusing only on messaging or dunning, they are redesigning payment infrastructure itself to reduce friction, anticipate failure, and recover revenue without eroding trust.

- Why Subscription Renewals Break Even When Customers Want to Stay

- The Payment Failure Patterns Driving Involuntary Churn in 2026

- Why Traditional Retry Logic Is No Longer Enough

- What Smarter Payment Design Means for Subscription Renewals

- How High-Performing Subscription Businesses Are Redesigning Renewal Flows

- Why Payment Design Has Become a Product Responsibility

- Cards vs. Open Banking (VRP) in Subscription Stability

- Designing for Declines Without Breaking the Customer Experience

- Conclusion

- FAQs

Why Subscription Renewals Break Even When Customers Want to Stay

Subscription renewals fail most often at the point where the customer is absent. Unlike checkout, renewal payments are processed without real-time confirmation, correction, or intent signalling (3DS). When something goes wrong, there is no opportunity for the customer to intervene before access is disrupted.

This creates a structural weakness. Issuers assess recurring transactions using patterns rather than context, and those patterns have become more conservative. A renewal attempt that looks ambiguous, mistimed, or repetitive can be declined even when funds are available.

The Soft Decline Trap Card networks themselves note that recurring transactions often fail for recoverable reasons, and that decline management requires more than repeated retries, as explained in Visa’s guidance on recurring decline mitigation.

At the same time, customer payment behaviour has changed. Cards are replaced more frequently, digital wallets shift default funding sources, and raw card numbers (PANs) expire faster than ever. The core issue is that most subscription platforms still treat renewals as automated repeats of the original transaction. They rely on logic designed for presence, not for absence.

The Payment Failure Patterns Driving Involuntary Churn in 2026

In 2026, involuntary churn is rarely caused by a single technical failure. It is driven by overlapping changes in issuer behaviour, customer payment habits, and subscription infrastructure that has not evolved at the same pace.

Issuer-side changes

Issuers now apply stricter logic to recurring transactions. Repeated retries without fresh data (like 3DS authentication or Network Token updates) are viewed as hostile patterns. Card networks have publicly highlighted that repeated retries without context damage Merchant ID (MID) reputation, worsening authorisation outcomes across the board.

Customer-side payment behaviour

Customers are managing more cards, wallets, and accounts than ever. Expiry, replacement, and reissuance cycles are shorter. From the customer’s perspective, nothing has changed, but from the issuer’s perspective, the credential attempting renewal is stale.

Infrastructure-side limitations

Most billing systems still rely on static rules. Retry schedules are fixed, decline types are not differentiated, and payment routing rarely adapts in real time.

As guidance from the Payment Services Regulation (PSR) and card schemes increasingly emphasises payment resilience, it is clear that involuntary churn is now a systems problem, not a customer decision.

Why Traditional Retry Logic Is No Longer Enough

For years, retry logic was the primary defence against failed renewals. When a payment declined, systems simply tried again, often multiple times. In 2026, that assumption no longer holds.

The Cost of Brute Force Issuers now interpret repeated, poorly timed retries as a negative signal. Multiple attempts without changes in context (like a transaction flag update) reinforce the perception of risk. Card schemes have acknowledged that excessive retries can degrade authorisation performance, effectively blacklisting a transaction for a set period.

The problem is that most retry strategies are blind. They do not distinguish between a temporary issuer caution signal and a genuine failure. More importantly, retries alone do not address the root issue: data decay. If the card has been reissued, retrying the old number 10 times will not work, it will only damage your standing with the issuing bank.

What Smarter Payment Design Means for Subscription Renewals

Smarter payment design starts with a simple shift in perspective: a renewal is not a repeat of the original checkout. It is a different payment event, processed under different conditions, with different failure risks.

At checkout, the customer is present. They can authenticate, switch cards, or correct mistakes. At renewal, none of that exists. The transaction is silent, issuer-mediated, and judged almost entirely on patterns and context. Designing renewals as if they behave like first-time payments is where most systems fail.

What it is NOT:

- More retries layered onto the same logic.

- More dunning messages pushed onto the customer.

What it Is: It is designed specifically for the renewal moment. That means recognising issuer caution signals, sequencing retries intelligently (e.g., waiting for payday windows), and avoiding behaviour that teaches issuers to distrust future attempts.

Crucially, smarter design respects the absence of the user. The objective is to resolve failure quietly where possible (using tools like Account Updaters), without forcing customers into friction they did not create. Only when recovery cannot happen invisibly should the customer be pulled into the process.

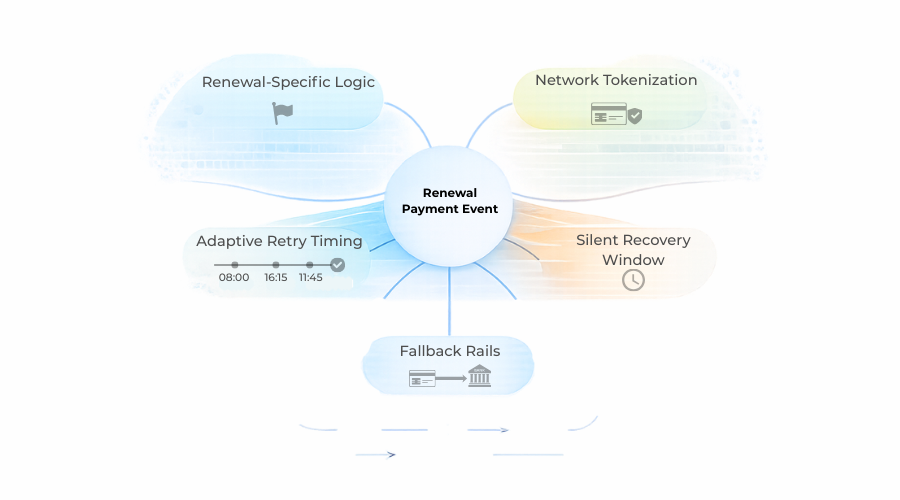

How High-Performing Subscription Businesses Are Redesigning Renewal Flows

High-performing subscription businesses no longer treat renewals as automated background events. They treat them as unique payment moments that require their own logic, sequencing, and safeguards.

Separating renewal logic from initial checkout

Initial payments optimise for conversion (speed). Renewals optimise for continuity (trust). Leading teams now maintain distinct logic paths. Renewal payments carry different metadata (using MIT – Merchant Initiated Transaction flags), follow different retry rules, and are assessed independently.

Network Tokens as the Standard

The single biggest shift in 2026 is the abandonment of raw card numbers (PANs) for renewals. Mature businesses use Network Tokenization.

- Why? When a customer gets a new card (due to expiry or loss), the Network Token updates automatically in the background. The merchant never sees the decline, and the customer never has to update their details.

Adaptive recovery instead of brute retries

Static retry schedules are being replaced with adaptive recovery models (often AI-driven). These systems interpret decline codes before acting.

Soft Decline? Retry in 24 hours at a different time of day.

Hard Decline? Check Account Updater service immediately.

Stolen Card? Suppress retry and trigger customer notification.

Building invisible fallback paths

When primary payment rails fail, high-performing businesses increasingly rely on invisible fallback. Secondary cards, wallet-backed funding sources, or account-based backups are activated quietly, preserving access while recovery happens in the background.

Why Payment Design Has Become a Product Responsibility

For a long time, subscription payments were owned almost entirely by finance teams. Their mandate was clear: process charges, reconcile revenue, and manage exceptions. Renewal failure was treated as an accounting issue, addressed after the fact through reporting or dunning.

That separation no longer holds in 2026. When a renewal fails, the customer experience breaks immediately. Access is interrupted, trust is tested, and the product promise is weakened all before finance teams can react. This has pushed payment design closer to Product Ownership, where renewal success is judged in real time.

Product teams increasingly recognise that renewals behave like core product flows, not back-office processes. Payment reliability now shapes perceived product quality, particularly for services positioned as “always on.” Industry bodies and card networks have also emphasised that recurring payments should be designed with customer experience and continuity in mind, not treated as invisible background charges.

As a result, ownership has shifted. Payment design now sits at the intersection of Product, Payments, and Revenue Operations. Decisions about retry behaviour, fallback paths, and customer intervention are no longer financial optimisations alone. They are product decisions with direct impact on retention (LTV).

Cards vs. Open Banking (VRP) in Subscription Stability

As subscription businesses reassess renewal performance, payment rail choice has become a structural decision.

Where cards still make sense, cards remain dominant at sign-up because they are familiar and flexible. However, card credentials are fragile. Expiry and reissuance introduce failure points that compound over time. This is why Network Tokenization is mandatory for long-term card health. VRPs are designed around long-lived consent for repeat payments without re-authentication each time, as described by Open Banking in its overview of Variable Recurring Payments.

Where Account-Based (VRP) outperforms In Europe and the UK, Variable Recurring Payments (VRP) via Open Banking have changed the landscape. Unlike Direct Debit (which is slow and prone to clawbacks), VRP offers:

- Permanence: Bank accounts don’t expire.

- Resilience: No lost card declines.

- Control: Real-time settlement with immediate failure feedback.

European payment initiatives under the European Payments Council increasingly promote these account-to-account models for recurring use cases due to their lower involuntary churn risk. High-performing merchants in 2026 don’t choose one or the other; they design systems that can switch between Card and VRP based on customer preference and market stability.

Designing for Declines Without Breaking the Customer Experience

Not every decline should be visible to the customer. In subscription models, renewal declines sit at a sensitive intersection between trust and continuity.

The Silent Recovery Window High-performing businesses create a grace period logic. If a payment fails on Day 30, the customer is not notified immediately. The system attempts silent recovery (via Account Updater or intelligent retry) for 3-5 days. Access remains uninterrupted.

Result: The customer never knows there was a glitch, and the subscription continues.

Where customer intervention is unavoidable, the experience is treated as a trust moment. The notification isn’t Payment Failed. Please Update Your Method. The timing and language emphasise that the business is working to maintain service, not threatening to cut it off.

In 2026, renewal recovery is no longer about maximising pressure. It is about minimising disruption.

Conclusion

In 2026, subscription renewal performance is no longer rescued by better messaging or more aggressive recovery tactics. It is shaped upstream, by how payment systems are designed to behave when customers are absent and issuers are cautious.

The businesses improving renewal rates are not those optimising individual metrics in isolation. They are the ones treating renewals as distinct payment moments, adopting Network Tokenization, leveraging VRP, and designing infrastructure that anticipates failure.

As issuer controls tighten and customer tolerance for friction continues to fall, the gap between well-designed and poorly designed renewal systems will widen. Subscription businesses that invest in smarter payment design today are not just reducing involuntary churn, they are building revenue models that are structurally immune to the “silent failures” of the past.

FAQs

1. Why do subscription renewals fail even when customers want to continue?

Because renewal payments are processed without the customer present. Issuers rely on patterns and risk signals rather than intent, and many failures are caused by soft declines, expired credentials, or outdated payment logic rather than insufficient funds.

2. What is involuntary churn in subscription businesses?

Involuntary churn occurs when a subscription ends due to payment failure rather than a customer decision. It is usually driven by declines, card replacement, or retry logic issues, not dissatisfaction.

3. What is a “soft decline” and why does it matter for renewals?

A soft decline is a temporary issuer caution signal, not a hard rejection. Many subscription systems treat soft declines as final failures, which unnecessarily ends subscriptions that could have been recovered.

4. Why does retrying failed payments often make things worse?

Poorly timed or repeated retries can damage issuer trust and reduce future authorisation rates. Issuers learn patterns, and aggressive retries can signal risk rather than recovery intent.

5. How are renewal payments different from checkout payments?

Checkout payments happen with the customer present, allowing authentication or correction. Renewals happen silently, months later, under different issuer rules and higher scrutiny.

6. What does “smarter payment design” actually mean in practice?

It means designing payment systems specifically for renewal moments, using renewal-aware logic, interpreting decline signals correctly, and recovering failures without immediately involving the customer.

7. Why is network tokenisation important for subscription renewals?

Network tokens automatically update when a card is reissued or expires. This prevents renewals from failing due to outdated card numbers and significantly reduces involuntary churn.

8. What role do Account Updater services play in renewal recovery?

Account Updaters help refresh card details when issuers replace cards. They allow merchants to recover payments without asking customers to manually update their information.

9. When should customers be notified about a failed renewal payment?

Only when silent recovery is no longer possible. Premature notifications create unnecessary friction and damage trust. High-performing businesses allow a short grace period before involving the customer.

10. Why are product teams now involved in payment design?

Because payment failure directly affects customer experience. Renewals are no longer a back-office finance issue; they are part of the product’s reliability and perceived quality.

11. Are cards still suitable for subscription payments in 2026?

Yes, especially for sign-up and global reach. However, cards are fragile over time, which is why mature subscription businesses combine them with tokenisation and fallback options.

12. What is VRP (Variable Recurring Payments) and why does it matter?

VRP is an Open Banking-based recurring payment method that uses bank accounts instead of cards. Bank accounts don’t expire, making VRP more stable for long-term renewals in supported markets.

13. Should subscription businesses choose cards or account-based payments?

They should not choose one exclusively. The most resilient systems use cards for convenience and account-based payments for long-term stability, switching intelligently when needed.

14. Can better payment design really improve renewal rates without changing pricing or messaging?

Yes. Many renewal failures are caused by system behaviour, not customer intent. Fixing payment design often recovers revenue that was previously written off as churn.

15. What is the most important mindset shift for subscription businesses today?

Stop treating renewals as automated repeats of checkout. Renewals are distinct, high-risk payment events that require their own logic, safeguards, and design discipline.