For CBD and supplement merchants operating in Europe, payment challenges in 2026 are no longer centred on initial approval. Many businesses can now secure a merchant account, often through specialized high-risk providers or aggregators. The real issue is whether that payment relationship remains stable as the business grows, comes under review, or expands into new markets.

This shift matters because payment instability has become commercially disruptive, not just operationally inconvenient. Sudden reserve increases, restricted payment methods, or quiet account terminations can interrupt cash flow, delay fulfilment, and damage customer trust. For CBD and supplement brands built on repeat purchases and brand credibility, even brief disruptions can have lasting effects.

At the same time, CBD and supplements continue to sit in a fragile risk category for many Payment Service Providers (PSPs). Regulatory interpretation remains uneven across Europe, enforcement approaches vary by market, and changes to products or marketing can trigger reassessment without warning. Approval alone no longer guarantees continuity.In response, more established merchants are rethinking how they approach payments. Instead of treating processing as a utility, they are focusing on building long-term transparent relationships with PSPs that can withstand scrutiny, reviews and scale. In 2026, that mindset is increasingly central to sustainable growth.

- Why CBD and Supplements Still Sit in a Fragile Payment Category

- What Broke Payment Relationships for CBD Merchants in the Past

- What a Long-Term Payment Relationship Means in 2026 (In Practice)

- How Mature CBD Merchants Are Redesigning Their Payment Profile

- The Role of Regulation and Labelling in PSP Confidence

- Why PSPs Now Prefer Fewer, Deeper CBD Relationships

- Supplements vs CBD: Where Payment Risk Diverges

- Conclusion

- FAQs

Why CBD and Supplements Still Sit in a Fragile Payment Category

Despite wider market adoption, CBD and supplement merchants continue to sit in a fragile payment category because risk is defined less by legality and more by interpretation. For PSPs, the challenge is not whether these products can be sold, but whether their risk profile can remain stable over time as regulation, enforcement, and consumer scrutiny evolve.

CBD remains particularly exposed to regulatory ambiguity across Europe. Product classification, THC thresholds and Novel Food status are not enforced uniformly, creating uncertainty that payment providers must absorb. Supplements face fewer headline restrictions but carry their own risk through health claims, cross-border distribution and variable consumer expectations.

In both cases, PSPs are managing exposure in categories where definitions can shift faster than contracts. If a merchant inadvertently drifts into selling a banned substance (like high-THC derivatives disguised as CBD) or makes an unverified health claim, the PSP faces potential Card Scheme integrity fines from Visa or Mastercard that far exceed the profit from that merchant.

This fragility influences behaviour long before problems surface. PSPs tend to onboard cautiously, monitor closely and reassess frequently. Small changes in a new product line, updated marketing language, or expansion into a new market can prompt internal reviews because they introduce fresh interpretive risk.

What Broke Payment Relationships for CBD Merchants in the Past

Most payment failures in the CBD space were not triggered by outright non-compliance. They emerged from structural weaknesses in how relationships were formed, managed, and allowed to drift over time. Many merchants assumed that approval signalled acceptance, when in reality it only reflected temporary tolerance.

Onboarding without long-term conviction

Historically, many PSPs onboarded CBD merchants cautiously, often under pressure to expand category coverage. These relationships were rarely built with a clear view of how the business would evolve. As volumes grew or scrutiny increased, the original risk assumptions no longer held, forcing PSPs into defensive reassessment.

Category drift and uncontrolled expansion

CBD businesses frequently expanded product lines or markets faster than their payment relationships could absorb. Moving from topical products into ingestibles, or drifting into grey area psychoactive cannabinoids (like HHC or Delta-8 variants), introduced new regulatory interpretations that were not always disclosed or understood in advance.

Marketing behaviour triggering payment risk

Claims around wellness, relief, or health outcomes often became the breaking point. Even when legally defensible, changes in marketing language exposed PSPs to reputational and regulatory risk they had not initially priced in.

When these pressures converged, relationship breakdown followed a familiar pattern:

Silent internal reclassification of merchant risk.

Escalation of reserves or rolling holds without clear thresholds.

Removal of specific payment methods or corridors.

Abrupt termination is framed as risk appetite change.

In most cases, the failure was relational rather than transactional. Payment access collapsed not because the business stopped complying, but because the PSP lost confidence in its ability to anticipate what would happen next.

What a Long-Term Payment Relationship Means in 2026 (In Practice)

In 2026, a long-term payment relationship is no longer defined by how quickly a CBD or supplement merchant can be approved, or how many payment methods are initially enabled. Stability is measured by what happens after onboarding, when the business begins to scale, attract attention, or operate across multiple markets.

From a PSP perspective, a long-term relationship is one where risk remains predictable. That does not mean static. Volumes can grow, product ranges can evolve and geographies can expand, but those changes need to arrive in a way that can be understood, assessed, and absorbed without surprise. Payment partners are no longer willing to discover material shifts through transaction data alone.

For merchants, this reframes the role of payments entirely. Processing is no longer a background utility that only matters when it fails. It becomes an ongoing relationship that requires consistency in how products are positioned, how customers are acquired, and how regulatory exposure is managed. The absence of disruption is not accidental; it is the result of alignment.

How Mature CBD Merchants Are Redesigning Their Payment Profile

CBD merchants that have achieved payment stability in 2026 have not done so by finding more tolerant PSPs. They have done it by reducing uncertainty at the source. The redesign starts with how the business presents itself operationally, not how it negotiates terms.

Stabilising the product and category narrative

One of the most common changes among mature merchants is tighter control over product scope. Rather than expanding aggressively across loosely related categories, stable businesses draw clear internal lines around what they sell and how those products are classified. This clarity matters because PSPs assess risk at the category level first. Merchants that simplify their catalogue make it easier for payment partners to understand and defend ongoing exposure.

Aligning claims, marketing, and payments

In 2026, marketing language is no longer separate from payment risk. PSPs increasingly view claims as an input into compliance and reputational exposure. Mature merchants now treat claims discipline as part of payment management. Messaging is reviewed not only for legal defensibility but for how it may be interpreted by acquiring banks, card schemes, and regulators. Fewer surprises mean fewer escalations.

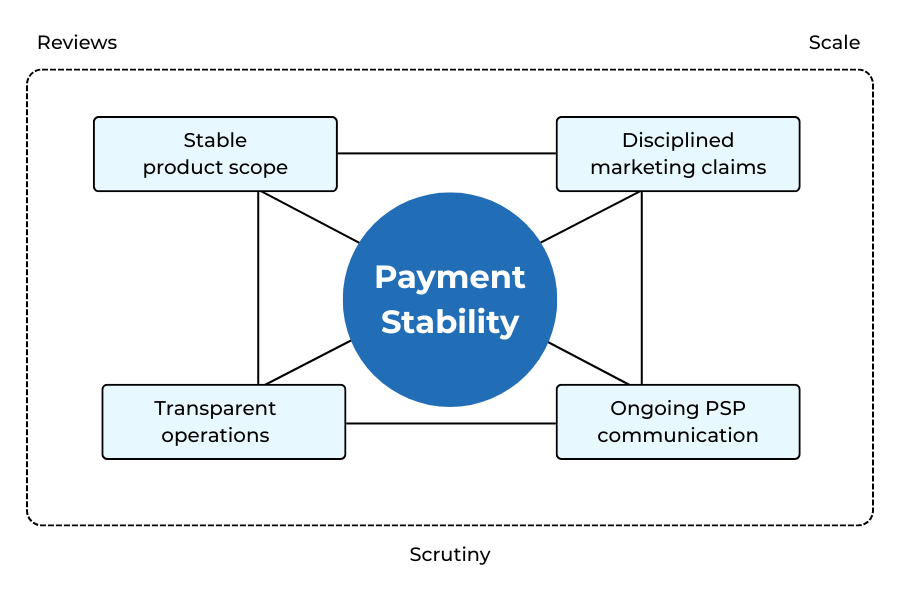

Operational transparency as a trust signal

Stable payment relationships are supported by consistent disclosure. Instead of treating onboarding as a one-time truth exercise, established merchants maintain ongoing transparency.

- Consistent product scope and classification.

- Disciplined claims and marketing language.

- Live, batch-specific COA transparency: Ensuring lab reports on the site match the exact batch being sold.

- Readiness to evidence compliance on request.

Taken together, these changes shift the merchant’s payment profile from reactive to predictable, a prerequisite for long-term stability in a sensitive category.

The Role of Regulation and Labelling in PSP Confidence

For CBD and supplement merchants, regulation influences payment stability less through formal approvals and more through how defensible a business appears under scrutiny. PSPs are not acting as regulators, but they are highly sensitive to how easily they can justify supporting a merchant if questions are raised by banks, schemes, or authorities.

In Europe, CBD remains exposed to regulatory interpretation rather than outright prohibition. Novel Food positioning, THC thresholds and product classification vary by jurisdiction. From a PSP perspective this creates exposure that cannot be ignored.

Labelling plays a central role here. Clear ingredient disclosure, conservative positioning and readily available documentation reduce ambiguity during reviews. Certificates of Analysis (COA), traceability and accurate product descriptions allow PSPs to assess risk without relying on assumptions. Where labelling is vague or marketing language stretches into implied health outcomes, confidence erodes quickly.

Key Insight: PSPs tend to care less about whether a product sits at the edge of regulation and more about whether that edge is managed responsibly.

Why PSPs Now Prefer Fewer, Deeper CBD Relationships

By 2026, many PSPs have moved away from broad exposure to the CBD category. This shift is not driven by reduced demand, but by the operational cost of managing uncertainty at scale. Supporting a large number of small, inconsistent CBD merchants proved expensive, review-heavy and difficult to defend internally.

As regulatory interpretation evolved and enforcement attention increased, PSPs began reassessing portfolio strategy. Rather than spreading risk thinly across many merchants, providers increasingly favour fewer relationships where behaviour is predictable and communication is reliable. Depth has become easier to manage than breadth.

For PSP risk teams, deeper relationships reduce surprise. Merchants that disclose changes early, scale in measured steps, and maintain consistency across products and markets are less likely to trigger emergency reviews. This lowers internal escalation frequency and allows risk to be managed through adjustment rather than withdrawal.

Supplements vs CBD: Where Payment Risk Diverges

While CBD and supplements are often grouped together by PSPs, the risk drivers behind each category are not identical.

Where supplements behave differently

Traditional supplements generally benefit from clearer regulatory categorisation. Ingredients are more widely recognised, enforcement is more consistent, and PSPs are less exposed to interpretive risk around legality. As a result, payment reviews tend to focus more on merchant behaviour than on the product category itself. For supplements, risk is often driven by:

- Aggressive or misleading health claims.

- Cross-border selling without localisation.

- Chargeback sensitivity linked to subscription or continuity models.

Where the risks converge

Despite these differences, CBD and supplements intersect at several critical pressure points. Both categories sit close to health and wellness outcomes, making marketing language a primary risk input. Both face heightened scrutiny when expanding across borders and both can trigger PSP concern when customer complaints or disputes rise suddenly.

In practice, PSPs apply similar expectations to both categories: consistency, defensibility, and predictability.

Conclusion

In 2026, payment stability for CBD and supplement merchants is no longer a technical concern sitting behind the business. It has become a commercial strategy that directly influences growth, resilience, and brand credibility. Approval alone is no longer sufficient in a category where interpretation, scrutiny, and reassessment are constant.

Merchants that are succeeding are not those chasing tolerance or short-term workarounds. They are the ones designing their businesses to be predictable partners for PSPs, disciplined in product scope, careful in marketing claims, and transparent in how they operate. These behaviours reduce uncertainty, which is ultimately what destabilises payment relationships.

As PSPs narrow their exposure and prioritise fewer, deeper relationships, the balance of power has shifted. Long-term payment stability now belongs to merchants that understand how risk is perceived and managed on the other side of the relationship. In a sensitive category like CBD and supplements, that understanding is becoming a decisive advantage.

FAQs

1. Why do CBD and supplement merchants still struggle with payment stability in 2026?

Because the risk is driven by interpretation rather than legality. PSPs must manage regulatory ambiguity, marketing claims, and reputational exposure, not just compliance status.

2. Is it easier to get a CBD merchant account in Europe now than before?

Yes, onboarding has become more accessible, but approval alone does not guarantee long-term payment continuity.

3. What usually causes CBD payment accounts to be terminated after approval?

Most terminations stem from loss of confidence, triggered by product drift, marketing claims, regulatory reassessment, or unexpected changes in business activity.

4. Why do PSPs care so much about marketing claims?

Because health or wellness claims can expose PSPs to card scheme scrutiny, regulatory complaints, and reputational risk, even if the merchant believes the claims are defensible.

5. How does product expansion affect payment relationships?

Expanding into new CBD formats, supplements, or grey-area cannabinoids can reclassify risk and invalidate the original onboarding assumptions if not managed transparently.

6. Are supplements considered lower risk than CBD for payment providers?

Generally yes, but supplements still carry risk through health claims, subscription models, cross-border selling, and chargeback exposure.

7. What role does labelling play in payment stability?

Clear, conservative labelling reduces ambiguity during PSP reviews and makes merchant risk easier to defend internally.

8. Why do PSPs now prefer fewer CBD merchants rather than many?

Managing uncertainty across a large CBD portfolio is costly. PSPs increasingly prioritise deeper relationships with predictable, well-managed merchants.

9. Does compliance alone protect CBD merchants from payment disruption?

No. Compliance is necessary, but payment stability depends on predictability, transparency, and ongoing alignment with PSP expectations.

10. How important are Certificates of Analysis (COAs) for payment providers?

COAs help demonstrate product consistency and traceability, reducing uncertainty during reviews, especially for ingestible CBD products.

11. Can payment stability improve without changing PSPs?

Often yes. Many stability issues are resolved by improving disclosure, tightening product scope, and aligning marketing with payment risk realities.

12. What does a “long-term payment relationship” actually look like in practice?

It is characterised by fewer surprise reviews, proportionate controls, predictable settlements, and ongoing dialogue rather than reactive enforcement.

13. Are CBD merchants expected to disclose changes proactively to PSPs?

Increasingly, yes. PSPs now expect early disclosure of product, market, or marketing changes to avoid defensive reactions.

14. Is payment instability always a sign of wrongdoing?

No. In most cases, instability reflects uncertainty rather than misconduct, especially in sensitive categories like CBD and supplements.

15. What is the biggest mindset shift CBD merchants need to make in 2026?

Moving from treating payments as a utility to treating them as a long-term relationship that requires discipline and consistency.