")

Tokenisation began as a security upgrade. In the early PCI-DSS era, its purpose was simple: to protect card numbers by replacing them with encrypted substitutes. Over time, the payments industry discovered that tokenisation was not just a compliance tool; it was an identity layer. When Visa and Mastercard introduced network tokenisation, the shift became structural: tokens evolved into stable, lifecycle-managed credentials that issuers trusted more than raw PANs.

In 2026, that evolution is expanding beyond cards. Tokenisation is becoming the common language across A2A payments, open banking APIs, wallets, instant payment systems, and alternative payment methods. Every rail is converging on the same principle: secure, persistent, updateable payment identities that reduce fraud, improve authentication outcomes and eliminate credential fragility.

The pressure for this shift is coming from every direction. Regulators are tightening API and credential-security standards under PSD3/PSR and the UK’s FCA framework.

(Reference: FCA Publications: https://www.fca.org.uk/publications)

Banks are preparing for the SPAA (SEPA Payment Account Access) model, which requires structured, tokenised consent for both data access and payment initiation.

Instant payment rails across APAC from UPI to PayNow and PromptPay already use alias-token systems instead of raw account numbers. Wallet ecosystems use device-bound tokens as their default security architecture.

The result is a rapidly emerging multi-rail reality: tokens are no longer a card technology. They are becoming the foundation of every major digital payment rail.

For merchants, PSPs and orchestration platforms, this shift creates a new advantage the ability to unify identity across cards, A2A, wallets and alternative methods under a single, persistent token framework. Tokens bring continuity where credentials have historically been fragile, whether it is a card expiry, a consent renewal, a mandate refresh or a change in bank account details.

2026 marks the moment when tokenisation becomes more than a technical layer. It becomes the infrastructure for approval stability, fraud reduction, cross-rail routing and long-term customer retention. The payment ecosystem is moving beyond static credentials to dynamic, multi-rail identity and tokenisation is the bridge.

- Evolution of Tokenisation: From PCI Protection to Multi-Rail Identity

- Network Tokenisation Today: The Card Benchmark (VTS / MDES)

- Why Open Banking Needs Tokenisation (UK/EU Under PSD3 + SPAA)

- Data Token vs Payment Token: Scope, Usage & ISO Alignment

- A2A Tokenisation: How Open-Banking Providers Apply Tokens for VRP and Recurring A2A

- Instant Payment Rails & Alias Token Systems (APAC + EU)

- Wallets & APMs: Device Tokens, Network Tokens & Alias Tokens

- Multi-Rail Technical Architecture: The 2026 Token Blueprint

- Regulatory Requirements Across Regions (EU, UK, India, Singapore)

- Fraud, SCA & Identity Continuity Across Rails

- Merchant Use Cases: SaaS, Gaming, FX, Marketplaces

- 2026 Forecast: Token Standards Convergence (EMVCo + EPC)

- Implementation Roadmap: Deploying Multi-Rail Tokenisation

- Step 1: Establish a rail-agnostic identity model

- Step 2: Integrate with a multi-rail token vault

- Step 3: Expand rails progressively via orchestration

- Step 4: Align with regulatory frameworks per region

- Step 5: Optimise routing and reporting based on token metadata

- A roadmap designed for long-term performance

- Conclusion

- FAQs

Evolution of Tokenisation: From PCI Protection to Multi-Rail Identity

Tokenisation originally emerged as a way to reduce PCI exposure. Merchants were struggling with the risk of storing raw card numbers, and replacing those numbers with randomly generated tokens offered an immediate compliance benefit. At this stage, tokenisation was purely a defensive one more layer between merchants and sensitive data.

Over the next decade, this function expanded dramatically. As fraud pressure increased and issuers sought better risk signals, card networks introduced network tokenisation, led by Visa Token Service (VTS) and Mastercard MDES. Unlike merchant-generated tokens, network tokens were tied to the underlying card at the scheme level and could be automatically refreshed whenever the card was reissued or replaced. This transformed tokenisation into an identity system rather than a storage mechanism.

From Secure Storage → Stable Identity

Network tokens introduced lifecycle updates, device binding and richer metadata, allowing issuers to recognise a customer more consistently across channels. Approvals stabilised, fraud declined and 3DS2 challenges became more predictable. Tokenisation shifted from a compliance feature to a performance engine.

The next phase: beyond cards

By 2026, tokenisation will have begun extending into open banking, A2A payments, instant-payment systems and digital wallets. Regulators are encouraging this shift, particularly under PSD3 and the SPAA framework, where banks are expected to issue secure, token-based identities for API access and payment consent.

At the same time, APAC instant-payment networks such as UPI, PromptPay and PayNow use alias-based tokens instead of exposing bank account details. Wallets rely on device-bound tokens rather than static credentials. Across these rails, the pattern is consistent: raw identifiers are disappearing, replaced by stable tokens that retain continuity even when underlying data changes.

A multi-rail identity layer is emerging

This evolution is creating a unifying trend across the payments industry. Instead of treating cards, A2A, wallets and instant-payment systems as separate infrastructures, tokenisation is becoming the common identity layer that connects them. By 2026, tokens represent not just card numbers but consent, mandates, payer identity and routing logic, forming the foundation for more secure and resilient multi-rail commerce.

Network Tokenisation Today: The Card Benchmark (VTS / MDES)

Card-network tokenisation remains the reference point for all other token models emerging in 2026. Visa Token Service (VTS) and Mastercard’s MDES system were the first to show how tokens could operate not just as secure substitutes for PANs, but as stable, issuer-trusted credentials that improve performance across the payment lifecycle.

Lifecycle continuity is the defining feature

The biggest strength of network tokens is their ability to remain valid even when the underlying card changes. When a bank reissues or replaces a card whether due to expiry, fraud or portfolio migration, the network updates the token automatically. Merchants don’t need to prompt customers to update their card details, and transactions continue without interruption.

This continuity became a breakthrough for subscription merchants and high-frequency businesses, where card reissuance is a major cause of failed renewals. The token evolves with the customer’s account behind the scenes, creating a more consistent payment identity.

Why issuers trust network tokens more than PANs

Another advantage is the enhanced metadata linked to network tokens. Device information, wallet binding, cryptograms and transaction-specific signals give issuers stronger confidence during authentication and authorisation. As a result, network tokens often achieve higher approval rates than raw PANs, especially in e-commerce and cross-border flows.

This trust is central to why tokenisation works. Issuers treat network tokens as living identities with a behavioural history, rather than static pieces of card data that may be outdated or misused.

The model that other rails are now copying

Because network tokenisation has proved so effective, its core concepts lifecycle management, issuer-linked updates, metadata enrichment and secure vaulting are now influencing token strategies in open banking, A2A payments and alternative payment rails. What began as a card innovation is becoming the template for multi-rail identity in 2026.

This makes network tokens the benchmark: the most mature, widely deployed and performance-proven token framework in the market. The next sections explore how this model is now being adapted to bank APIs, instant-payment rails and wallet ecosystems.

Why Open Banking Needs Tokenisation (UK/EU Under PSD3 + SPAA)

Open banking was originally designed around secure APIs and customer-initiated consent, but by 2026 it faces a structural challenge: too many authorisations, too many expiring permissions and too much friction for recurring or high-frequency A2A payments. This is where tokenisation becomes essential. Instead of relying on raw account details and repeated authentication prompts, bank APIs are moving toward token-based identities that can survive consent refresh, account changes and long-lived payment mandates.

The shift from raw bank details to API-level tokens

Under the PSD3 framework, the EU is tightening requirements around secure API access and data minimisation. Banks must avoid exposing identifiable account details when not strictly required. Tokenised account identifiers, consent tokens and mandate tokens meet this requirement by replacing sensitive credentials with secure, non-reversible references.

This allows Payment Initiation Service Providers (PISPs) and Account Information Service Providers (AISPs) to operate without handling raw, high-risk identifiers.

SPAA and the rise of structured, tokenised consent

The SEPA Payment Account Access (SPAA) framework accelerates this transformation. SPAA introduces commercial API access alongside regulated access, meaning banks and PISPs exchange structured digital tokens representing:

- Data-access consent

- Payment initiation approval

- Mandate permission for recurring A2A flows.

Instead of repeatedly asking the customer to confirm access, banks issue a “consent token” that PISPs can re-use while respecting PSD3’s rules on authentication and security. This mirrors how network tokens extend the life of card credentials after a reissue.

UK open banking is heading in the same direction

In the UK, the FCA and the Open Banking Implementation Entity have signalled the need for longer-lasting, tokenised permissions, particularly as Variable Recurring Payments (VRP) expand beyond sweeping into broader commercial use cases.

Without tokenisation, VRP flows would require constant customer re-authentication, making them impractical for subscriptions, wallets or top-up services.

Why open banking cannot scale without tokens

Open banking volumes are growing, but recurring A2A payments still face a drop-off because account access expires, bank details change, or consent becomes invalid. Tokenisation solves these issues by introducing continuity exactly the continuity that network tokenisation brought to cards. Tokens ensure consent remains durable, payer identity remains stable and payment initiation stays frictionless long after the initial setup.

As PSD3 and SPAA reshape the regulatory landscape, tokenisation becomes the foundation that allows open banking to operate as a reliable, scalable alternative to cards.

Data Token vs Payment Token: Scope, Usage & ISO Alignment

As open banking and A2A payments scale, regulators and banks are increasingly distinguishing between two very different types of tokens: data tokens and payment tokens. Both improve security and reduce exposure to sensitive information, but they operate in separate layers of the API ecosystem. Understanding this distinction is essential for merchants, PSPs and orchestration platforms building multi-rail payment flows in 2026.

Data tokens: representing account access and customer permissions

Data tokens are issued when a customer authorises an AISP to view their account information. Instead of providing the AISP with raw identifiers, the bank issues a secure reference token that represents the permission. The AISP uses this to request statements, balances or categorised spending data without needing to handle the customer’s actual account details.

Under PSD3 and SPAA, this model became the standard. It satisfies data-minimisation rules and ensures that account changes such as switching banks or updating account metadata do not break the connection between the customer and the AISP.

Payment tokens: representing consent for initiating payments

Payment tokens enable PISPs to initiate payments without re-authenticating the customer each time. When a customer authorises a payment mandate, the bank issues a reusable token representing their approval. This token flows through the payment chain and allows recurring or variable recurring payments (VRP) to execute smoothly.

This mirrors the structure of card network tokenisation:

- The underlying account can change

- The token remains stable

- And the merchant can continue using it

Why the distinction matters

In 2026, merchants will increasingly rely on both token types. A subscription business may use data tokens to validate account status while using payment tokens to process ongoing A2A charges. A marketplace may use data tokens to monitor account verification but rely on payment tokens for seller disbursements.

The separation also reduces fraud. Data tokens cannot be used to initiate payments, and payment tokens cannot be used to access account information. Each token represents a clearly scoped permission, a requirement strengthened under PSD3’s focus on explicit customer consent.

ISO alignment across Europe and beyond

Token structures are being aligned with ISO 20022 and emerging EPC standards, which ensures interoperability across EU banks and makes it easier for PSPs to manage multi-bank, multi-rail flows. Over time, the industry is moving toward unified token attributes that support both data-access consent and payment authorisation, creating a more predictable technical environment for high-risk and cross-border merchants.

As more markets adopt similar models, the distinction between data and payment tokens becomes a foundational part of next-generation financial infrastructure.

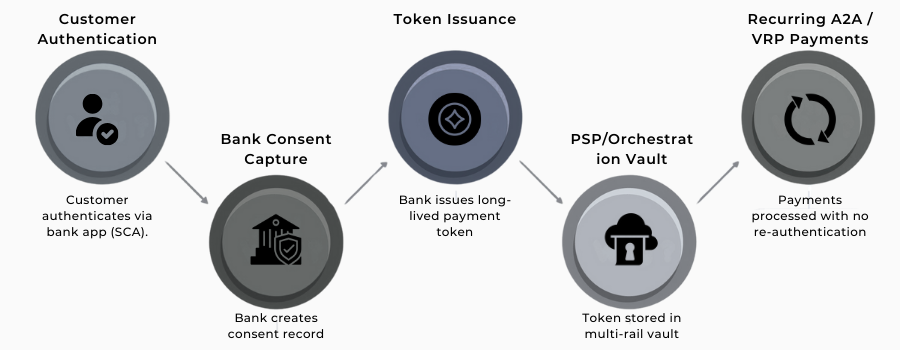

A2A Tokenisation: How Open-Banking Providers Apply Tokens for VRP and Recurring A2A

As open banking expands into higher-frequency and commercial payment use cases, traditional consent models are no longer sufficient. In 2026, providers across the UK and EU are adopting tokenised consent frameworks that allow recurring or variable recurring A2A payments to operate with the same continuity merchants expect from card-on-file models. Instead of asking customers to approve each transaction, banks issue secure, long-lived tokens that represent both identity and mandate permission.

Tokenised VRP consent in the UK

The UK’s Variable Recurring Payment (VRP) framework relies heavily on tokenisation. When a customer approves a VRP mandate via their banking app, the bank generates a token that encapsulates the consent parameters, such as maximum amount, permitted frequency and merchant identity. The PSP uses this token to initiate payments without requiring repeated SCA challenges, unless the mandate conditions are exceeded. This removes the friction that would otherwise make A2A unsuitable for subscriptions, wallet top-ups or usage-based billing.

EU providers adopting similar models under PSD3 and SPAA

Across Europe, the push toward secure, long-lasting consent is being driven by PSD3 and the SPAA framework. Banks are expected to issue payment tokens that encapsulate customer authorisation for recurring or on-demand A2A payments.

This makes A2A more stable for merchants who need predictable billing cycles, especially in digital goods, FX, mobility and subscription sectors. Without tokenised mandates, these flows would require customers to re-authenticate frequently, creating breakpoints that undermine conversion and retention.

How providers maintain consent continuity

Payment tokens behave similarly to network tokens for cards:

- If a customer updates their bank account, the token remains valid.

- If authentication rules change, the mandate token still reflects the original approval.

- If the PSP switches the routing path, the token remains the same across banks.

This continuity allows recurring A2A payments to function reliably, even in cross-bank or multi-PSP environments. Providers also use refresh cycles seamless background updates that renew consent tokens without requiring customer action ensuring that mandates don’t suddenly expire during a billing cycle.

Why recurring A2A now depends on tokenisation

Without tokenisation, A2A would remain a single-payment rail. Every recurring charge would require a new SCA, and every change to the customer’s account would break the billing relationship. Tokenisation transforms A2A from a one-off transfer method into a viable alternative to cards for ongoing transactions. It preserves identity, retains mandate validity and ensures payments remain consistent even as underlying account details change.

This is the foundation enabling A2A to compete with card-on-file experiences in 2026.

Instant Payment Rails & Alias Token Systems (APAC + EU)

Instant payment systems are expanding rapidly in 2026, and many of them already operate on token-based identity rather than exposing raw bank details. Unlike card networks, these rails never allowed merchants or PSPs to handle sensitive information such as account numbers. Instead, they rely on alias identifiers that act as tokens for routing payments securely.

UPI VPAs: the most mature alias-token model

India’s Unified Payments Interface (UPI) is one of the clearest examples. Every payer and payee uses a Virtual Payment Address (VPA), such as name@bank, instead of a bank account number. Behind the scenes, the VPA acts as a token:

- It abstracts the customer’s bank details

- It remains the same even if the user switches banks

- And it is fully portable across PSP apps

When a customer changes their primary bank account, the VPA token can be re-mapped without requiring merchants to collect new payout or mandate information. This makes UPI one of the most token-native instant-payment systems globally.

(Reference: Reserve Bank of India: https://www.rbi.org.in)

PayNow and PromptPay: mobile-number tokenisation

Singapore’s PayNow and Thailand’s PromptPay use a similar approach, but instead of VPAs, they tokenise the customer’s mobile number or national ID. The alias acts as the public-facing credential, while the underlying account details remain hidden within the banking network. This model improves safety, simplifies onboarding and reduces the need for merchants to manage sensitive data.

Europe: SEPA Instant adopting structured payer-identifiers

Within the EU, SEPA Instant Credit Transfer (SCT Inst) is moving toward structured payer tokens as part of the wider PSD3 and SPAA reforms. While IBANs are still used today, regulators are encouraging the development of reusable payer identifiers and tokenised mandate references, especially for recurring or VRP-style instant transfers.

Some PSPs already map IBANs into internal tokens to avoid repeatedly handling raw account information and to enable cross-PSP retry flows.

A growing global pattern: account details are disappearing

Across APAC and Europe, the direction is the same: instant-payment systems want to remove account numbers from the merchant-PISP relationship entirely. Alias tokens and structured identifiers reduce fraud, cut sensitive data exposure and make payment credentials more stable across banks and digital wallets.

This lays the foundation for genuine multi-rail routing, where a merchant can hold a single token representing the customer and use it across cards, instant rails, A2A and wallets.

Wallets & APMs: Device Tokens, Network Tokens & Alias Tokens

Wallets and alternative payment methods have been token-first for years, long before open banking and A2A began adopting similar models. Apple Pay, Google Pay, PayPal, GrabPay, and regional super-apps all rely on secure, device-bound identifiers that never reveal the underlying credential to the merchant. By 2026, these wallet and APM token frameworks will influencing how broader multi-rail tokenisation is being designed.

Device tokens as the foundation of wallet payments

Apple Pay and Google Pay generate device-specific tokens whenever a card is provisioned to a mobile wallet. These tokens are tied to the customer’s device, secure enclave and biometric authentication. When the wallet initiates a transaction, the merchant never sees the actual card number; they only receive a tokenised version issued through the card network. This is one reason wallet payments typically achieve strong approval rates: issuers trust the cryptographic signatures linked to device-bound tokens.

Network tokens inside wallet ecosystems

Wallets also rely on network tokens (via VTS and MDES). When a customer adds a card to a wallet, the wallet does not store the PAN. Instead, it stores a token that inherits all network-managed lifecycle updates. If the card is replaced or reissued, the token is updated automatically. This reduces payment breakage and makes wallets ideal for subscription or top-up flows in high-frequency sectors.

APM alias tokens for top-ups and payouts

Beyond wallets, many APMs use alias tokens for stored-value accounts or wallet top-ups. Examples include:

- PayPal’s internal tokenised customer ID

- GrabPay and ShopeePay mobile token identifiers

- GCash and Maya alias systems in the Philippines

- WeChat Pay and Alipay user-based wallet IDs.

These APMs rarely expose bank credentials or underlying rails. Instead, they use alias tokens that tie the customer to a stored-value ecosystem. This facilitates payouts, refunds and instant top-ups without exposing sensitive information.

The convergence toward a token-only wallet ecosystem

By 2026, almost all wallets will operate with layered tokenisation:

- Device token

- Network token

- Alias token inside the APM

- Payment token (for recurring charges via card or A2A)

This layered approach protects sensitive information and creates identity continuity across devices, funding sources and channels. It also allows PSPs and orchestration platforms to treat wallets as stable payment identities rather than variable or fragile credentials.

Wallet ecosystems are one of the strongest proofs that tokenised identities can thrive across multiple rails, a structure that the rest of the payments industry is now adopting.

Multi-Rail Technical Architecture: The 2026 Token Blueprint

As tokenisation expands beyond cards, merchants and PSPs need a single technical model that can manage tokens across every major rail card, open banking, A2A, instant payments and wallets. By 2026, this multi-rail architecture will become a structural requirement. Instead of storing fragmented identifiers, merchants increasingly rely on a unified token layer that maps a customer’s identity across multiple rails within the orchestration stack.

A unified token identity mapped to multiple funding sources

In the emerging model, each customer is associated with a rail-agnostic identity token, generated either by the PSP, orchestration platform or wallet provider. This token does not store any sensitive information. Instead, it links to specific payment tokens underneath:

- Card network tokens (VTS/MDES)

- Open-banking payment tokens (VRP or mandate tokens)

- Instant-rail alias tokens (UPI VPAs, PayNow/PromptPay IDs)

- Wallet or APM internal tokens

This hierarchical structure allows the orchestration system to switch between rails without changing the merchant’s relationship with the customer.

Token vaults evolving into multi-rail identity repositories

Traditional card token vaults stored only PAN-substitute tokens. In 2026, vaults are evolving into multi-rail repositories, capable of managing:

- Lifecycle updates from card networks

- Consent refreshes for A2A/VRP

- Alias-token remapping for instant rails

- Device-token updates for wallets

- Metadata updates across all tokens

The vault becomes a dynamic identity layer, not just a secure storage component.

How orchestration platforms route using tokens

Once a customer’s identity is mapped across multiple rails, the orchestration engine can route payments intelligently:

- Using a card network token when approvals are likely

- Shifting to A2A payment tokens for lower costs

- Selecting an instant-payment alias when speed matters

- Or retrying a failed transaction on another rail using the same root identity token

This multi-rail routing is only possible because tokens are stable identifiers that represent the same customer across systems.

Metadata as the glue between rails

Metadata attached to each token issuer information, consent parameters, device-binding attributes, and risk signals allows the orchestration layer to make smart routing decisions. In card payments, metadata improves issuer trust; in A2A flows, it validates mandate conditions; in instant rails, it confirms alias authenticity. As standards mature under PSD3 and SPAA, cross-rail metadata becomes more aligned, making this multi-rail architecture easier to implement.

Why this blueprint matters in 2026

High-risk and cross-border merchants increasingly rely on multiple payment methods to maximise approval rates and reduce costs. Without a unified token architecture, each rail would operate in isolation, creating fragmentation and operational risk. The 2026 blueprint replaces this fragmentation with a consistent identity layer, improving reliability and enabling merchants to switch rails seamlessly as customer behaviour or regulatory requirements evolve.

Regulatory Requirements Across Regions (EU, UK, India, Singapore)

Tokenisation is not only a technical trend, it is increasingly a regulatory expectation. By 2026, major markets will have introduced rules that shape how banks, PSPs and merchants handle payment identifiers. While each region takes a different approach, the direction is the same: reducing the exposure of raw credentials and promoting stable, secure, tokenised identifiers.

EU: PSD3 and the SPAA framework

Europe’s transition to PSD3 and the Payment Services Regulation (PSR) strengthens its focus on API security and consent durability. Under these rules, banks must minimise the use of raw account data and rely on tokenised identifiers where possible. The SPAA initiative further formalises the concept of tokenised consent for both data (AIS) and payment initiation (PIS) APIs.

In practical terms, this means open banking in the EU is moving toward a model where recurring A2A and VRP-style flows must be supported by long-lived, structured tokens rather than repeated customer re-authentication.

UK: VRP expansion and FCA expectations

In the UK, the FCA continues to expand expectations around Variable Recurring Payments (VRP). As commercial VRP grows beyond sweeping, banks and PISPs are expected to support richer, more stable consent structures.

Tokenisation is central to this model, because VRP mandates would be unworkable if banks required customers to authenticate every transaction.

UK regulators also emphasise data minimisation, which reinforces the use of tokenised account references instead of exposed identifiers.

India: RBI-driven tokenisation across cards and instant payments

India was one of the earliest adopters of tokenisation at scale. The Reserve Bank of India mandated card tokenisation to reduce exposure of PANs, and similar principles are now embedded in UPI architecture through Virtual Payment Address (VPA) alias tokens.

UPI’s VPA system is essentially a national tokenisation model for bank account routing, and the RBI’s regulatory push has accelerated this approach across banks, wallets and PSPs.

Singapore: MAS guidelines and PayNow alias models

Singapore follows a structured token-based approach through its PayNow system, which tokenises mobile numbers or NRIC identifiers instead of revealing account numbers. The Monetary Authority of Singapore (MAS) supports frameworks that reduce sensitive-data risk and encourage secure, token-based payment initiation.

Singapore’s regulations emphasise traceability, strong authentication and data minimisation all of which directly support tokenisation as the default identity architecture.

A global regulatory direction

Across all four regions, regulators are moving toward the same outcome:

- Fewer exposed credentials

- More stable tokenised identities

- Stronger authentication

- And safer multi-rail payment ecosystems.

Tokenisation is no longer optional, it is becoming the design baseline for secure, regulated commerce in 2026.

Fraud, SCA & Identity Continuity Across Rails

As payment methods diversify across cards, A2A, instant payments and digital wallets, maintaining a consistent approach to fraud control and customer authentication becomes more challenging. In 2026, tokenisation acts as the stabilising layer that keeps identity intact across these different rails. Instead of managing multiple sets of raw credentials, merchants rely on tokenised identities that remain valid even when customers update accounts, change devices or reissue cards.

Fraud reduction through minimised exposure

Tokenisation reduces fraud by removing the most sensitive elements in the payment flow. When merchants no longer handle PANs, IBANs or direct account credentials, the attack surface shrinks significantly. Tokens cannot be reverse-engineered, carry no standalone monetary value and provide no usable information to a fraudster. This is why many issuers and A2A providers show lower fraud rates for tokenised transactions compared to raw-data flows.

Improving Strong Customer Authentication outcomes

Under PSD2 and future PSD3 rules, SCA challenges are often triggered when issuers lack confidence in a transaction’s risk profile. Tokenisation improves this confidence. For card payments, network tokens carry metadata that links the transaction to a known device, wallet or customer profile. For A2A, payment tokens embed mandate details, consent conditions and authentication history. These signals help issuers and banks determine when frictionless authentication is appropriate, reducing unnecessary step-ups that can impact conversion.

Continuity despite underlying data changes

One of the biggest operational advantages of tokenisation is that it preserves payment continuity even as the customer’s details evolve.

- A card may be replaced.

- A bank account may move to a different provider.

- A mobile device may be upgraded.

Despite these changes, the token persists. Behind the scenes, token vaults and banking APIs remap the underlying data while keeping the primary token stable. This continuity is what makes tokenisation the backbone of recurring payments, VRP flows, subscription billing and in-app commerce.

Cross-rail identity consistency

Without tokenisation, identity in payments is fragmented and the customer appears differently across each rail. With tokenisation, the merchant can treat the customer as a single, stable identity, regardless of whether they pay via card, A2A, wallet, or instant rail. This consistency improves fraud controls, simplifies analytics and makes orchestration engines more effective. It also reduces edge-case disputes caused by mismatched or outdated credentials.

A strategic fraud-control asset for 2026 merchants

By reducing exposure to raw credentials, embedding rich metadata and enabling cross-rail identity continuity, tokenisation is becoming a central component of fraud prevention. High-risk sectors, iGaming, FX, e-commerce and subscription platforms increasingly depend on tokenisation not simply for security, but for stable performance in an environment where identity signals determine approval outcomes.

Merchant Use Cases: SaaS, Gaming, FX, Marketplaces

Tokenisation becomes most powerful when viewed through real operational scenarios. By 2026, merchants across high-risk and high-volume sectors are using network, A2A and alias tokens not only for security, but to stabilise recurring payments, reduce involuntary churn and manage multi-rail billing strategies. Each vertical benefits from tokenisation differently, but they all rely on the same foundation: keeping the payment identity consistent even when underlying credentials change.

SaaS and subscription platforms

Subscription businesses face a constant battle with involuntary churn caused by card expiry, account changes or expired open-banking consents. Tokenisation helps eliminate these breakpoints. Network tokens refresh automatically when a card is reissued, and A2A payment tokens remain valid even if a customer moves to a different bank. For SaaS platforms, this means fewer failed renewals, more predictable cash flow and reduced reliance on dunning processes. As recurring VRP expands across the UK and EU, SaaS merchants increasingly treat tokenisation as the baseline for maintaining long-term customer relationships.

Gaming and iGaming merchants

Gaming requires fast, frictionless top-ups and reliable payouts both of which benefit from tokenised identities. Device tokens in wallets allow returning players to fund instantly, card network tokens increase approval stability, and instant-payment alias systems (such as UPI or PayNow) create consistent payout identifiers that don’t change when customers switch accounts. In high-risk iGaming corridors, tokenisation also helps reduce fraud-related declines by preserving strong authentication signals and improving issuer trust.

FX, trading and brokerage platforms

FX and trading platforms rely on real-time deposits and fast withdrawals. Tokenisation supports this by reducing credential volatility and improving SCA confidence. A customer funding via card, A2A or instant payment rail appears as the same identity within the PSP’s orchestration layer, which allows platforms to route payments dynamically to whichever rail offers the highest approval or lowest fee at that moment. For withdrawal flows, alias-based tokens (UPI VPAs, PayNow mobile IDs) reduce payout failures caused by outdated account details.

Marketplaces and multi-seller ecosystems

Marketplaces must manage both pay-ins and payouts at scale. Tokenisation allows them to maintain stable seller identities without storing sensitive account data. A seller’s UPI VPA, PayNow alias, card token or A2A mandate token can all link back to the same marketplace identity record. This keeps disbursements reliable even when sellers update banks or switch payout methods.

For marketplaces operating across multiple regions, tokenisation becomes essential for unifying their settlement logic and reducing operational overhead.

A shared theme: stability across change

Across all these use cases, the underlying value of tokenisation is the same. It removes brittle, volatile credentials from the payment relationship and replaces them with stable, refreshable identifiers. Whether the customer changes their device, card, bank or payout rail, the merchant’s link to that customer remains intact and so does the revenue flow.

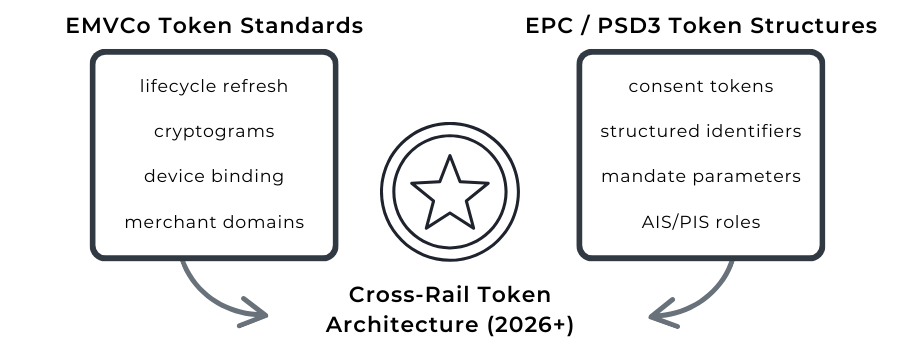

2026 Forecast: Token Standards Convergence (EMVCo + EPC)

Tokenisation has developed independently across multiple rails cards, A2A, wallets, and instant-payment systems. But by 2026, regulators and industry bodies are moving toward a more unified token framework. The two most influential forces behind this shift are EMVCo, which defines global card token standards, and the European Payments Council (EPC), which sets standards for SEPA and open-banking interoperability across the EU.

Although their origins differ, both bodies increasingly share the same objective: replacing sensitive payment identifiers with stable, portable tokens that behave predictably across markets and rails.

EMVCo’s role: mature, lifecycle-managed card token standards

EMVCo’s tokenisation specifications have already shaped how network tokens operate across Visa, Mastercard and digital wallets. Their framework introduced key mechanisms such as lifecycle updates, cryptographic authentication, device binding and merchant-specific domains.

These same technical concepts now influence how banks and PSPs approach tokens in A2A and open banking. As recurring A2A and VRP flows grow, EMVCo’s established lifecycle logic is becoming the default reference model.

EPC’s direction: structured token models for SEPA and open banking

The European Payments Council is steering SEPA toward structured identifiers for both instant payments and API-based account access. While not “tokens” in the card sense, these identifiers share many of the same characteristics:

- They abstract underlying account data

- Support consent-based access

- And operate across multiple banks using a standard format

Under PSD3, this alignment becomes more important. Banks must adopt secure, token-like identifiers for both AIS (data access) and PIS (payment initiation), reducing exposure of IBANs and other sensitive credentials.

Why convergence is becoming inevitable

As payment rails support more similar use cases, subscription billing, recurring A2A, one-click pay-ins, and instant payouts regulators want consistent security behaviours. EMVCo’s lifecycle refresh model and EPC’s standardised consent framework both address this need.

Banks and PSPs increasingly recognise that separate standards create unnecessary friction. In a multi-rail ecosystem, merchants want predictable behaviour, whether the payment moves through VTS, MDES, SEPA Instant, VRP or a wallet.

This is pushing the industry toward interoperable token structures, where card tokens, A2A tokens and alias tokens share common metadata fields and similar lifecycle-management principles.

What merchants can expect by 2026 and beyond

The practical outcome is a more unified token architecture across Europe:

- Cross-rail orchestration capable of routing based on a single identity token

- More consistent authentication logic across different banks and issuers

For high-risk and cross-border merchants, this convergence is a strategic advantage. It simplifies integration, strengthens approval rate stability and makes multi-rail routing more predictable all without handling sensitive credentials.

Token standards are not fully merged yet, but the direction is clear: EMVCo and EPC frameworks are moving closer each year, forming the foundation of the multi-rail identity layer that will define payments beyond 2026.

Implementation Roadmap: Deploying Multi-Rail Tokenisation

As tokenisation expands across cards, A2A, instant-payment systems and wallets, the challenge for merchants is no longer whether to adopt tokens but how. A multi-rail token framework requires coordination between PSPs, orchestration platforms, open-banking providers and internal merchant systems. In 2026, successful deployments follow a clear sequence: unifying identity, choosing the right vaulting approach, and aligning with regulatory requirements across markets.

Step 1: Establish a rail-agnostic identity model

The first step is defining how the merchant identifies a customer across multiple payment methods. Instead of linking identity to the PAN, IBAN or device ID, merchants map each customer to a single, high-level identity token.

This token does not store sensitive information; it simply acts as an anchor for all subsequent payment and alias tokens. By doing this early, merchants avoid having to restructure customer records later when adding new rails.

Step 2: Integrate with a multi-rail token vault

Traditional card vaults often cannot store A2A, alias or wallet tokens in a unified structure. In 2026, merchants will rely on PSPs or orchestration platforms that offer multi-rail vaulting capabilities.

These vaults manage:

- Network token lifecycle updates,

- VRP or A2A mandate token refresh cycles,

- Alias-token remapping for instant-payment rails,

- And metadata tagging for routing.

This central vault becomes the operational core of the token strategy.

Step 3: Expand rails progressively via orchestration

Merchants typically begin with card tokens, then introduce A2A payment tokens, followed by instant-payment alias tokens and wallet-based device tokens. The orchestration platform routes using the identity token as the starting point, ensuring that customer experience remains consistent even as new rails are added. This staged rollout avoids disruption and reduces risk.

Step 4: Align with regulatory frameworks per region

Tokenisation rules vary across markets.

- In the EU, PSD3 and SPAA require structured consent and secure API access.

- In the UK, VRP expansion introduces new token-based mandate requirements.

- In India, RBI rules govern card tokenisation and alias mapping through UPI VPAs.

- In Singapore, MAS guidelines influence PayNow identifier security.

Ensuring compliance at the design phase prevents costly rework once volumes scale.

Step 5: Optimise routing and reporting based on token metadata

Token metadata helps merchants and PSPs make informed routing decisions. Device signals may push a wallet transaction to a tokenised card rail, while consent timing may favour an A2A route. Reporting tools analyse approval variance, retry success, alias uptime and fraud reduction across tokenised rails, allowing merchants to refine their strategy over time.

A roadmap designed for long-term performance

Implementing multi-rail tokenisation is not a one-time project. It is a structural redesign of how merchants manage identity, authentication and payment continuity. By approaching tokenisation as a phased, multi-rail strategy supported by orchestration, vaulting and strong regulatory alignment merchants can significantly enhance approval rates, reduce fraud exposure and create more resilient customer relationships in 2026 and beyond.

Conclusion

Tokenisation began as a security measure, but by 2026, it has become the identity layer that connects every major payment rail. As cards, A2A, wallets and instant-payment systems converge, merchants no longer manage separate, fragile credentials. Instead, they rely on stable, refreshable tokens that preserve continuity even when customers update cards, migrate banks or switch devices.

This shift is being accelerated by regulation. PSD3, SPAA, FCA guidance, and regional frameworks in India and Singapore all encourage token-based identifiers that reduce exposure to sensitive data. At the same time, orchestration platforms are adopting multi-rail vaulting and identity mapping, enabling tokens to power approvals, retries, mandates and cross-rail routing.

For high-risk and cross-border merchants, tokenisation is no longer optional. It is the infrastructure that supports reliability, reduces fraud, strengthens authentication and stabilises recurring payments across diverse rails. As standards move toward convergence, and as banks expand VRP and instant-payment capabilities, tokenisation will continue to evolve from a security tool into a foundational element of global digital commerce.

FAQs

1. What is multi-rail tokenisation in 2026?

Multi-rail tokenisation refers to using tokens across several payment methods cards, A2A, instant payments, wallets and alternative rails. Instead of storing raw credentials such as PANs or account numbers, merchants rely on secure, refreshable tokens that represent the customer’s payment identity. In 2026, this improves approval stability, reduces fraud exposure and supports recurring payments across different rails. As PSD3 and SPAA reshape bank API requirements, multi-rail tokenisation has become the new baseline for secure, regulated digital payments.

2. How is tokenisation used in open banking and A2A payments?

In open banking, tokenisation replaces raw account identifiers with bank-issued payment tokens and consent tokens. These tokens allow merchants and PSPs to initiate recurring A2A or VRP payments without asking the customer to re-authenticate each time. They also remain valid when a customer updates or switches bank accounts. This makes A2A payments more reliable and puts them on par with card-on-file experiences, especially under PSD3 and SPAA’s strengthened API security rules.

3. What is the difference between data tokens and payment tokens?

Data tokens are used for account information access (AIS), allowing financial apps to retrieve balances or transaction history without exposing account details. Payment tokens are used for payment initiation (PIS), enabling recurring A2A or VRP flows. The key distinction is purpose and scope: data tokens provide read-only access, while payment tokens carry consent to initiate payments. Under PSD3, both token types must follow structured consent rules and reduce reliance on raw account identifiers.

4. Why do approval rates improve with tokenisation?

Tokens generally achieve higher approval rates because they provide issuers with stronger authentication signals. Network tokens carry device data, lifecycle updates and cryptographic signatures that PANs cannot provide. A2A payment tokens embed mandate details and past authentication history, which reduces the need for repeated SCA challenges. As a result, banks trust tokenised transactions more, leading to fewer declines and more consistent acceptance across regions.

5. How do instant-payment rails such as UPI and PayNow use tokenisation?

Instant-payment systems in APAC rely on alias tokens, such as UPI VPAs or PayNow mobile-number identifiers, to route payments without revealing bank account numbers. These aliases act as secure, stable tokens that remain valid even when customers change banks. This reduces operational failures, supports fast payouts and improves account security. The EU is moving in a similar direction with structured payer identifiers under SEPA Instant.

6. What role does orchestration play in multi-rail tokenisation?

Orchestration platforms act as the glue between tokenised rails. They map each customer to a unified identity token that links to card tokens, A2A tokens, alias tokens and wallet tokens underneath. When a transaction fails on one rail, the orchestration engine can retry it on another without requiring new authentication. This makes tokenisation far more powerful, as it enables dynamic routing and reduces payment breakage for high-risk merchants.

7. Are regulators mandating tokenisation in 2026?

While not always mandated explicitly, regulators strongly encourage tokenisation to reduce fraud and data exposure. PSD3 and the SPAA framework promote tokenised consent for both AIS and PIS. The FCA supports VRP expansion, which depends on reusable payment tokens. The RBI mandates card tokenisation and enables alias-based identity through UPI VPAs. MAS frameworks support PayNow’s mobile token model. Across all major regions, tokenisation is becoming the default regulatory expectation.

8. How does tokenisation reduce fraud for merchants?

Tokenisation removes sensitive information from the merchant environment. Tokens cannot be reversed into account numbers or PANs, and they include richer metadata that helps banks validate the legitimacy of a transaction. Fraudsters have nothing meaningful to steal or reuse. Combined with SCA and behavioural risk signals, tokenised transactions reduce phishing, credential compromise and synthetic identity fraud especially in digital, high-risk or cross-border commerce.

9. Can tokenisation support recurring payments without cards?

Yes, payment tokens in open banking and A2A rails allow merchants to process recurring payments with the same stability as card-on-file. VRP tokens remain valid even if customers switch banks, and instant-payment aliases can be remapped without requiring new credentials. This enables subscription, usage-based and top-up models to operate securely across non-card rails, an essential capability for 2026 merchants expanding beyond traditional card processing.

10. What’s the long-term future of tokenisation across payment rails?

By 2026 and beyond, tokenisation is moving toward convergence. EMVCo standards for cards and EPC frameworks for SEPA/APIs are gradually aligning, creating compatible structures for lifecycle updates, consent, metadata and security signals. Over time, merchants will rely on a single, multi-rail customer identity token that works across cards, A2A, instant payments, digital wallets and alternative payment rails. This unified identity layer will define the next era of global payments.