Merchant approval rates in 2026 are shaped by factors far beyond gateway connectivity. Issuer behaviour, stricter PSD3 data requirements, corridor-specific risk thresholds and higher authentication expectations have created an environment where static, single-gateway setups cannot deliver consistent performance. In this landscape, payment orchestration platforms have become a critical layer, not an optional enhancement, for merchants operating across multiple markets, especially within high-risk or high-volume verticals.

The traditional gateway model was built for simplicity: one integration, one routing path, one acquirer relationship. However, issuers now rely heavily on enriched metadata, device intelligence, authentication precision and corridor stability to approve transactions. A single gateway cannot adapt to these conditions in real time. When issuer expectations shift, acquirer performance fluctuates or corridor risk increases, merchants using only one gateway experience immediate declines without the ability to reroute or optimise.

Payment orchestration platforms bridge this gap by introducing dynamic logic across routing, metadata enrichment, authentication flow selection, acquirer fallback and FX-aware decisioning. Instead of sending every transaction through a fixed path, orchestration engines make conditional decisions based on BIN ranges, issuer behaviour, past decline patterns, authentication history, FX impact and corridor performance. This transforms the merchant’s payment stack from static to adaptive.

The rise of PSD3 further accelerates the need for orchestration. The regulation demands higher data quality, improved SCA governance, structured reporting and transparent FX treatment. Orchestration platforms sit between merchant systems and acquirers, making it easier to standardise data fields, transmit complete authentication attributes and deliver consistent transaction profiles. For merchants, this improves approval rates; for acquirers, it reduces risk exposure.

By 2026, the most resilient merchants will be those who treat payments as an optimisation discipline. Orchestration platforms have moved beyond simple routing tools; they now function as intelligence layers that enhance approval performance, stabilise cross-border flows, and ensure merchants can meet evolving regulatory and issuer requirements.

- Why Traditional Gateways Can’t Meet 2026 Performance Requirements

- What Payment Orchestration Actually Is: Core Technical Components

- How Orchestration Improves Merchant Approval Rates in 2026

- Why Cross-Border Transactions Decline More Often: A 2026 Technical Breakdown

- PSD3 Requirements That Strengthen the Case for Orchestration

- Why Acquirers Prefer Merchants Using Orchestration (2026 Behavioural Drivers)

- What “Good” Orchestration Looks Like in 2026: A Technical Blueprint

- Case Study Models: How Orchestration Behaves in Real Merchant Scenarios

- How Merchants Should Build Their Orchestration Strategy for 2026: A Strategic Roadmap

- Establish a Unified Data Foundation

- Map Corridor Behaviour and BIN-Specific Patterns

- Align Authentication Pathways With Regional Requirements

- Build an Acquirer Distribution Model That Reduces Exposure

- Integrate FX and Settlement Logic Into Routing Decisions

- Implement Real-Time Monitoring and Behavioural Feedback Loops

- Govern the Ecosystem Through Policy, Not Individual Connections

- Conclusion

- FAQs

Why Traditional Gateways Can’t Meet 2026 Performance Requirements

Traditional gateways were designed for linear payment flows: a single integration, a single routing path and minimal metadata handling. In 2026, this architecture cannot support the approval stability required by global merchants, particularly those operating in high-risk or multi-corridor environments. Issuer requirements, PSD3 data standards and new authentication expectations all exceed what legacy gateways can deliver.

- Static Routing in a Dynamic Approval Environment

Traditional gateways route all transactions through one acquirer, regardless of market conditions. Approval rates in 2026 fluctuate based on BIN behaviour, issuer risk thresholds and corridor-specific trends. Without dynamic routing or fallback options, merchants remain exposed to approval drops, regional outages and sudden acquirer derisking. Static routing has become a structural limitation rather than a simplification.

- Limited Metadata Reduces Issuer Confidence

Issuer scoring models now rely on enriched metadata: device information, authentication history, address consistency, IP signals and behaviour markers. Many legacy gateways transmit only the minimum required fields, leading issuers to evaluate transactions with incomplete context. Under PSD3’s structured data requirements, insufficient metadata results in conservative scoring and higher false declines.

- Single-Acquirer Dependency Increases Corridor Volatility

Gateways typically support one acquirer per region. If that acquirer tightens MCC controls, alters fraud thresholds or encounters operational issues, the merchant has no alternative path. This creates corridor concentration risk; one acquirer’s performance shift immediately impacts entire markets. Approval resilience in 2026 depends on diversified acquirer distribution, which traditional gateways do not provide.

- Authentication Controls Are Too Rigid for PSD3 Standards

Authentication has become a major approval determinant. Issuers expect adaptive 3DS logic, correct exemption handling and challenge workflows aligned with regional norms. Traditional gateways use a single static 3DS implementation with limited flexibility. This results in unnecessary challenges, inconsistent pass rates and weaker SCA performance, all of which reduce approvals, especially on cross-border transactions.

- Insufficient Insight Into Decline Patterns and Issuer Behaviour

Most legacy gateways offer only basic reporting, with no visibility into issuer-level declines, BIN-specific issues or corridor anomalies. Without granular diagnostics, merchants cannot identify patterns early or adjust routing before losses accumulate. Real-time intelligence is essential for approval optimisation in 2026, but gateways lack the infrastructure to provide it.

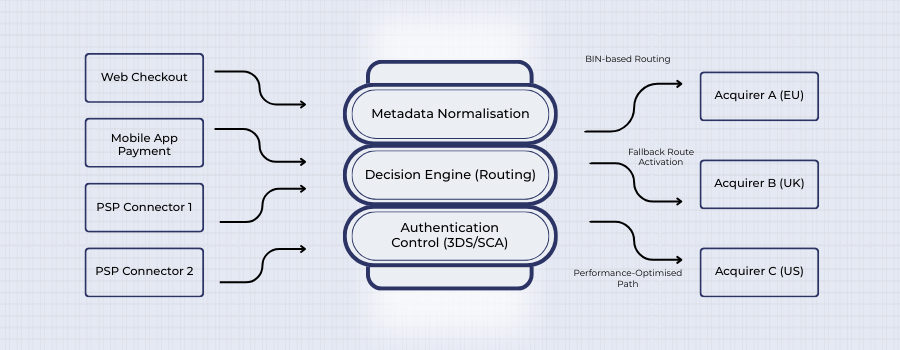

What Payment Orchestration Actually Is: Core Technical Components

Payment orchestration is often described as “smart routing”, but in reality, it is a full technical layer that sits above individual PSPs and acquirers. Its purpose is to control how each transaction is routed, authenticated, enriched and monitored across multiple payment partners. Unlike a gateway, which simply connects to one acquirer, an orchestration platform operates as a decision engine across the entire payment stack.

Routing Engine: Decision Logic Across BINs, Issuers and Corridors

The routing engine is the core of any orchestration platform. It decides where to send each transaction based on configured logic and live performance.

Key dimensions typically used include:

- BIN range and issuer country

- Merchant MCC and risk profile

- Corridor performance and decline history

- Acquirer availability and latency

- Currency and settlement preferences

In practice, this means the same card can be routed differently depending on time, corridor or recent decline patterns. If one acquirer starts underperforming for a given BIN range, the routing engine can automatically redirect volume to another acquirer without code changes at the merchant level.

Multi-Acquirer Switching and Fallback

Payment orchestration platforms natively support multiple acquirers and PSPs per corridor. This allows merchants to:

- Distribute traffic intentionally (60/40 split between acquirers)

- Send specific BINs or regions to specialist acquirers

- Trigger fallback when an acquirer returns too many soft declines, errors or timeouts.

Instead of being locked to a single acquiring partner, merchants gain a portfolio of acquirers that can be controlled centrally. This is especially important in high-risk industries, where acquirer appetite can change quickly and derisking decisions can affect specific MCCs or corridors.

Authentication Orchestration (3DS2 / SCA Handling)

A modern orchestration platform also manages how authentication is performed, not just where the authorisation is sent. This includes:

- Deciding when to trigger 3DS challenges vs frictionless flows

- Managing different ACS behaviours across issuers and regions

- Aligning SCA indicators with PSD2/PSD3 expectations

- Tracking challenge success rates by issuer or BIN.

Instead of relying on a static 3DS configuration, orchestration allows merchants to adapt authentication flows based on risk and performance data. For example, some issuers may accept more frictionless flows if certain metadata is present; others may always require a challenge for high-risk MCCs. Orchestration makes it possible to handle these variations without redesigning the checkout.

Data Enrichment and Metadata Consistency

Issuer models and acquirers increasingly expect complete, structured data on each transaction. Orchestration platforms act as a data normalisation and enrichment layer, ensuring that:

- Address, email, phone, and device details are consistent

- IP and geolocation are properly mapped

- Merchant descriptors follow agreed standards across acquirers.

This layer reduces the risk of declines caused by missing or inconsistent fields. It also supports PSD3 expectations around structured data and monitoring: the same enriched dataset can be forwarded to multiple acquirers or used to drive internal risk decisions.

FX and Settlement Configuration Awareness

While orchestration platforms are not FX engines, they increasingly incorporate FX-aware logic. That means routing decisions can consider:

- Processing currency vs issuer currency

- Settlement currency options by acquirer

- Known FX cost differences across routes.

For example, transactions from a given region could be routed to acquirers that process and settle in a currency closer to the issuer, reducing unnecessary conversions. This is particularly useful for merchants with multi-currency settlement strategies or those exposed to frequent FX slippage.

Monitoring, Analytics and Decline Intelligence

A key differentiator of orchestration is the ability to observe performance across all acquirers and corridors from one place. The monitoring layer typically covers:

- Approval/decline rates by BIN, issuer, acquirer and corridor

- Error patterns (technical vs business declines)

- Authentication outcomes

- Latency and timeout profiles

This insight allows merchants to adjust routing rules, rebalance acquirers, or investigate specific issuer patterns. Without orchestration, this level of visibility is rarely available, especially when traffic is split manually across multiple gateways or PSPs.

How Orchestration Improves Merchant Approval Rates in 2026

Orchestration improves approval rates not through a single feature, but through multiple decision layers that directly influence issuer trust, acquirer selection and authentication behaviour. In 2026, merchants gain performance advantages by controlling how every field, route and authentication event is delivered to the issuer.

To illustrate this shift, the table below shows how orchestration changes approval dynamics compared to traditional gateway routing.

Approval Impact Matrix: Gateway vs Orchestration (2026)

| Performance Factor | Traditional Gateway | Orchestration Platform | 2026 Approval Impact |

| Routing Decision | Static, single-path | BIN, issuer, corridor, FX-aware routing | +4–8% uplift |

| Authentication | One-size-fits-all 3DS | Adaptive SCA by issuer & region | +3–6% uplift |

| Metadata Quality | Limited fields | Full enrichment & structured data | +2–5% uplift |

| Acquirer Choice | 1 acquirer | Multi-acquirer + fallback | Stabilises drops |

| Decline Detection | Slow, batch reports | Real-time issuer-level monitoring | Prevents decline clusters |

Issuer-Aligned Routing (Why It Improves Approvals)

Issuer performance varies daily, especially across high-volume BINs. Orchestration evaluates:

- Recent decline ratios

- Corridor volatility

- BIN-level response trends

- Acquirer-specific risk rules

This allows transactions to be routed to the issuer-friendly acquirer on every attempt.

Traditional gateways cannot adapt, which means:

- Same BIN → same acquirer → same decline pattern

- No real-time intervention

- No corridor intelligence

Orchestration breaks this cycle.

Adaptive Authentication: Where Most Merchants Gain the Largest Uplift

Challenge vs frictionless flows vary dramatically across:

- Issuing banks

- Cardholder segments

- Regions

- BIN types

Orchestration platforms map these variations and decide:

- When to apply exemptions

- When to push challenge flows

- When to re-attempt authentication through alternate ACS paths

- When to increase metadata richness to support frictionless approval

This adaptive behaviour reduces friction and increases issuer approval confidence.

Metadata Enrichment: The Hidden Approval Lever

Issuer trust is now built on metadata, not just card details.

Orchestration ensures consistency across:

- Device ID

- IP + geolocation

- Email + phone

- Authentication flags

- Merchant descriptor

- Recurring indicators

- Account age signals

- SCA indicators (aligned with PSD3)

When issuers receive more structured data, they:

- Reduce false positives

- Lower friction

- Shift transactions out of the high-risk scoring buckets

Gateways simply cannot perform this level of enrichment.

Acquirer Fallback: Safety Mechanism for Decline Surges

When an acquirer rate drops:

- Decline clusters start forming

- Corridor approval collapses

- Issuer behavioural thresholds tighten

- Merchants lose revenue immediately

Orchestration platforms solve this with instant fallback:

- Detect soft declines rapidly

- Rebalance traffic

- Isolate the problem, BIN or MCC

- Redirect traffic to the next-best acquirer

This single capability protects approval stability.

Issuer Behaviour Diagnostics: The Part Merchants Very Rarely See

Orchestration platforms monitor performance per:

- Issuer

- BIN

- Acquirer

- Currency

- Corridor

- 3DS flow

- Soft-decline code

- Error type

This is far deeper than normal PSP reporting.

Merchants gain visibility into:

- When issuers tighten fraud thresholds

- When certain BINs begin declining

- When MCC-specific treatment changes

- When corridor risk patterns shift

This turns reactive optimisation into proactive prevention.

Why Cross-Border Transactions Decline More Often: A 2026 Technical Breakdown

Cross-border transactions face higher declines because issuers evaluate them through more conservative risk models, with multiple scoring layers applied in sequence. Each layer increases the probability of a false positive decline when data is incomplete or routing is not aligned with issuer expectations. Payment orchestration platforms reduce these failures, but to understand their impact, it’s essential to examine why cross-border payments inherently carry higher rejection rates.

Below is a layered breakdown model explaining the technical drivers of cross-border declines in 2026.

Layer 1: Geographic Inconsistency Filters

Issuers use geography as an early-stage risk signal. Any mismatch between location elements triggers additional scrutiny, especially in cross-border scenarios.

Typical inconsistency signals include:

- Card BIN country ≠ merchant country

- IP location ≠ expected customer region

- Acquirer location ≠ issuer geography

- Settlement currency ≠ processing currency

These mismatches don’t automatically cause declines, but they push the transaction into a higher-risk scoring pathway, reducing approval probability unless metadata is strong enough to compensate.

Layer 2: MCC Sensitivity and Corridor Risk Profiles

Issuer models categorise MCCs into risk tiers. High-risk or volatile categories (e.g., digital goods, gaming, certain subscription models) face:

- Stricter scoring rules

- Increased challenge requirements

- Lower tolerance thresholds

- Faster fraud-trigger activation

Some corridors also carry historical fraud exposure, meaning issuers apply region-specific risk multipliers. A transaction that would pass domestically may be flagged when routed cross-border through a high-risk corridor.

Layer 3: Authentication Flow Degradation

Cross-border authentication introduces more variability:

- Different ACS providers

- Inconsistent challenge flows across regions

- Limited behavioural history for the cardholder

- Missing SCA indicators or incorrect exemption flags

If the SCA flow fails, times out, or lacks structured information, issuers often default to decline. Authentication inconsistencies remain one of the strongest contributors to cross-border failure.

Layer 4: Metadata Fragmentation Across PSPs and Gateways

Many merchants operate with multiple PSPs or legacy gateways that structure data differently. As a result, when transactions reach the issuer:

- IP data may be missing

- Device identifiers may be inconsistent

- Customer address formats may vary

- Behavioural markers may be incomplete

Issuers interpret inconsistent metadata as a risk indicator; cross-border transactions with fragmented inputs have a significantly higher chance of being rejected.

Layer 5: Acquirer-Level Rules and Behavioural Thresholds

Acquirers apply rules based on:

- Corridor performance

- Chargeback ratios

- Fraud patterns

- Scheme-level monitoring

If a merchant’s traffic triggers any acquirer thresholds, the acquirer may:

- Increase challenge requirements

- Modify risk scoring

- Apply additional checks

This chain reaction amplifies cross-border decline rates, particularly when traffic is concentrated through one acquiring partner.

Layer 6: Issuer Machine Learning Models (2026 Edition)

Modern issuer models evaluate:

- Cardholder behavioural profiles

- Transaction history similarity

- Corridor predictability

- Device recognition

- Historical challenge outcomes

- Previous decline patterns

Cross-border transactions often have less historical similarity to the cardholder’s usual patterns, making them more likely to be flagged. When metadata doesn’t compensate, declines occur, even when the cardholder is legitimate.

Layer 7: Soft-Decline Loops and Retry Degradation

Many cross-border declines are “soft declines,” meaning the transaction should be retried. However:

- Gateways retry incorrectly

- PSPs retry too quickly

- Authentication steps aren’t updated between attempts

This results in retry degradation, where each subsequent attempt is more likely to fail because nothing was corrected.

Orchestration platforms address this by rerouting the retry to a better-performing acquirer with updated metadata.

Layer 8: FX Conversion Touchpoints

FX adds complexity across:

- Issuer processing currency

- Acquirer processing currency

- Merchant settlement currency

Multiple conversion events create FX mismatch scenarios. Issuers sometimes decline when the routing path suggests elevated FX exposure or if the merchant’s acquirer setup appears unusual for the customer’s region.

Layer 9: Latency and Cross-Border Network Delay

Cross-border hops often create additional latency.

Issuers treat delayed responses as potential fraud signals, especially when authentication takes too long.

This increases the chance of:

- Timeouts

- Incomplete authentication

- Delayed ACS responses

- Issuer throttling

All of which surface as cross-border declines.

Why This Breakdown Matters

By understanding these layers, merchants can identify where orchestration improves authorisation outcomes:

- Better routing = fewer corridor mismatches

- Consistent metadata = fewer risk flags

- Adaptive authentication = fewer challenge failures

- Multi-acquirer logic = fewer derisking impacts

- Rerouting retries = fewer soft-decline loops

In 2026, orchestration removes friction at multiple layers simultaneously, something a traditional gateway cannot achieve.

PSD3 Requirements That Strengthen the Case for Orchestration

PSD3 sets tighter expectations around data quality, authentication governance and auditability. These requirements directly benefit merchants who use orchestration platforms because orchestration standardises how transaction metadata, authentication signals and acquirer routing logic are transmitted. Below is a regulatory impact brief explaining how PSD3 drives orchestration adoption in 2026.

Regulatory Pillar 1: Data-Field Completeness (Structured Transaction Metadata)

- PSD3 Requirement: Under the EU’s Payments Package, acquirers and PSPs must ensure standardised and complete data fields for authorisation and monitoring.

- Why It Matters: Issuer scoring models increasingly rely on dozens of metadata fields. Missing or inconsistent fields trigger conservative risk decisions and unnecessary declines.

- Orchestration Advantage: Orchestration platforms act as a metadata governor, ensuring consistency across PSPs and acquirers:

- Normalised address and device fields

- Aligned SCA indicators

- Structured contact and behavioural data

- Consistent merchant descriptors across all routes

This helps merchants meet PSD3 data completeness requirements without modifying their core systems.

Regulatory Pillar 2: Authentication Quality and SCA Governance

- PSD3 Requirement

Stricter expectations around authentication strength, exemption handling and challenge governance. Issuers must receive clear, structured SCA information.

- Industry Reality

Authentication inconsistency remains one of the largest drivers of cross-border declines.

Different issuers respond differently to exemption logic, frictionless flows and 3DS challenge signals.

- Orchestration Advantage

Orchestration platforms enable adaptive authentication:

- Challenge-first logic for high-risk BINs

- Frictionless-first for stable corridors

- Exemption controls determined by issuer behaviour

- Alternative ACS routing when challenge flows degrade

This aligns SCA behaviour with PSD3’s principles and issuer-specific acceptance patterns.

Regulatory Pillar 3: FX Transparency and Routing Disclosures

- PSD3 Requirement

Clearer communication of FX margins, conversion timestamps and rate sources.

- Why FX Impacts Approvals

FX routing affects:

- Issuer risk scoring

- Corridor classification

- Mismatches between processing and settlement currencies

Issuers automatically scrutinise transactions with complex or unusual FX paths.

- Orchestration Advantage

Orchestration platforms support FX-aware routing, helping merchants avoid unnecessary conversions by directing transactions through acquirers that:

- Process in issuer-friendly currencies

- Reduce conversion layers

- Align with settlement preferences

- Match corridor expectations

This reduces FX-based mismatches that can trigger issuer decline logic.

Regulatory Pillar 4: AML/CTF Monitoring Expectations

- PSD3 Requirement

Stronger transaction monitoring and clearer responsibility allocation across PSPs, acquirers and technology providers.

- Compliance Challenge

Merchants using multiple PSPs often struggle to consolidate AML signals or present consistent behaviour profiles to acquirers.

- Orchestration Advantage

Orchestration creates a single monitoring layer, aggregating:

- Velocity anomalies

- Behavioural inconsistencies

- Corridor-level risk patterns

- Issuer-specific signals

- Recurring transaction patterns

This improves upstream risk management and aligns with PSD3’s monitoring expectations without increasing compliance overhead for merchants.

Regulatory Pillar 5: Auditability and Acquirer Reporting

- PSD3 Requirement

PSPs and acquirers must maintain detailed, timely and audit-ready records of authentication, routing logic, approvals and risk decisions.

- Operational Issue for Merchants

Legacy gateway setups often generate inconsistent logs across acquirers and PSPs, creating gaps during audits or dispute reviews.

- Orchestration Advantage

Orchestration platforms centralise and standardise reporting:

- Complete transaction histories

- Consistent metadata across all acquirers

- Unified SCA logs

- Structured routing logic documentation

This produces a clean, audit-ready data trail from a single source.

Regulatory Insight Summary

PSD3’s direction is clear:

- More structure

- More transparency

- More authentication discipline

- More monitoring accountability

Payment orchestration naturally satisfies these requirements and gives merchants the ability to adapt without rebuilding their internal payment stack.

Why Acquirers Prefer Merchants Using Orchestration (2026 Behavioural Drivers)

Acquirer behaviour has shifted significantly as fraud controls, PSD3 reporting expectations, and scheme monitoring pressures increase. In this environment, acquirers favour merchants who demonstrate stable routing patterns, consistent metadata quality and predictable authentication behaviour all of which orchestration platforms help achieve. Below is a cause–and–effect mapping of how orchestration directly influences acquirer appetite.

Cause 1: Stable, Structured Metadata Across All Transactions

Acquirers increasingly evaluate merchants based on metadata consistency, because inconsistent data triggers higher scheme monitoring scrutiny.

Effect:

Acquirers classify the merchant as “low operational risk”, reducing the probability of:

- Corridor volume caps

- Enhanced monitoring programmes

- Sudden derisking decisions

Why It Matters:

Merchants with structured routing and enriched metadata experience fewer acquirer-imposed constraints, improving approval stability.

Cause 2: Cleaner Authentication Signals and Fewer Friction Failures

Acquirers track authentication performance closely, as poor SCA behaviour often leads to issuer challenges, disputes and scheme alerts.

Effect: Acquirers see lower dispute ratios, lower challenge-failure rates and more predictable behavioural patterns.

Why It Matters: Merchants become “bankable” in acquirer scoring models, making acquirers more willing to maintain or expand corridor coverage.

Cause 3: Predictable Traffic Distribution Reduces Acquirer Exposure

When merchants send all traffic through a single acquirer, volume spikes or high-risk corridors create concentrated exposure.

Effect:

Orchestration distributes load across acquirers, reducing:

- Corridor-level risk consolidation

- Fraud concentration

- Scheme-trigger sensitivity

Why It Matters:

Acquirers prefer merchants who balance their traffic intelligently, as it stabilises risk and supports sustainable portfolio management.

Cause 4: Behavioural Alignment with Acquirer Risk Frameworks

Acquirers evaluate merchants based on how well their transactions align with internal risk systems. Orchestration engines enforce routing and data rules that match these frameworks.

Effect:

Acquirers observe fewer:

- Repeated soft-decline loops

- Inconsistent retries

- Mismatch between MCC and corridor

- Unusual authentication patterns

Why It Matters:

Merchants who “fit the acquirer framework” face fewer interventions and enjoy more predictable approval outcomes.

Cause 5: Lower Operational Noise and Fewer Investigations

Unstructured routing and inconsistent metadata create operational “noise”: tickets, alerts, false alarms, issuer escalation and scheme reviews.

Effect: Acquirers spend less time investigating anomalies, a major operational cost driver.

Why It Matters: Merchants using orchestration are lower maintenance; acquirers prefer partners who reduce operational workload rather than increase it.

Cause 6: Clearer Performance Telemetry Provided by Orchestration Platforms

Acquirers rely on data to evaluate merchant stability. Orchestration platforms provide consistent logs, structured routing histories and clean SCA event records.

Effect: Acquirers gain better visibility into merchant behaviour and can justify offering:

- Higher corridor capacity

- Faster onboarding for new regions

- Reduced deposit/rolling reserve requirements

- More flexible settlement terms

Why It Matters:

Enhanced transparency strengthens the merchant–acquirer relationship and reduces derisking scenarios.

Cause 7: Reduced Fraud Pattern Volatility

When routing and data quality are inconsistent, acquirers see volatility in fraud ratios and velocity patterns. Orchestration stabilises this upstream.

Effect: Fraud levels become more predictable, lowering acquirer fraud-risk exposure.

Why It Matters: Acquirers are more likely to retain or expand high-risk merchants when fraud signals remain stable.

Acquirers in 2026 choose to work with merchants who create predictability, data quality, and risk stability. Payment orchestration offers exactly this, making merchants operationally easier to support, financially safer to underwrite, and technically more compatible with acquirer scoring frameworks.

What “Good” Orchestration Looks Like in 2026: A Technical Blueprint

High-performance orchestration in 2026 is not defined by the number of acquirers or the sophistication of a single routing engine. Instead, “good” orchestration is characterised by its ability to create predictable transaction behaviour across all corridors, eliminate unnecessary friction, absorb issuer and acquirer volatility, and consistently present structured, authentication-aligned data to the payments ecosystem. The following blueprint outlines the attributes that define a mature orchestration model in 2026.

- A Unified Decision Layer Across All Acquirers and PSPs

In a mature setup, orchestration serves as the single point of truth for routing, authentication behaviour and data standardisation. Regardless of the upstream platform, storefront or device, every transaction is processed through the same decision framework. This produces uniform metadata signatures, reliable authentication behaviour and a predictable interaction profile for issuers, resulting in higher approval stability across regions.

- Real-Time Routing That Adapts to Issuer and Corridor Behaviour

Good orchestration recognises that approval conditions change constantly. It reacts to issuer-specific patterns, localised corridor shifts and acquirer performance in real time. Rather than allowing declines to accumulate before corrective action is taken, a mature orchestration model continuously rebalances traffic to protect approval continuity. This level of adaptation ensures that merchants do not rely on static routing assumptions in a dynamic payments environment.

- Authentication Integrated Directly Into Routing Logic

In 2026, authentication has become inseparable from approval optimisation. Mature orchestration synchronises routing with SCA expectations, ensuring each issuer receives a coherent authentication request. The best setups use authentication outcomes to influence routing decisions for future attempts, linking challenge behaviour, device recognition and corridor acceptance patterns into a single decision loop.

- Metadata Normalisation That Eliminates Fragmentation

One of the strongest indicators of orchestration maturity is the quality and consistency of metadata transmitted to acquirers. A good orchestration framework ensures uniformity across address fields, device indicators, behavioural markers, merchant descriptors and authentication values—even when merchants operate multiple integrations. This stability builds issuer trust and reduces the false positives commonly triggered by inconsistent transaction structures.

- Financial Logic Embedded Into Technical Routing Paths

Beyond approval optimisation, a high-performing orchestration model considers FX exposure, settlement configurations and cost implications within routing decisions. It directs transactions to acquirers whose currency paths, settlement behaviour and FX practices align with merchant requirements. This reduces slippage, improves reconciliation accuracy and ensures operational decisions are financially efficient.

- A Monitoring Layer With Diagnostic Depth

Good orchestration is defined by visibility. A mature setup provides granular insight into issuer responses, authentication flows, corridor-specific anomalies, acquirer decline patterns and soft-error propagation. This monitoring layer enables merchants to intervene early, preventing performance degradation. It also equips PSPs and acquirers with reliable telemetry, strengthening commercial and technical collaboration.

- Consistent Behaviour Across Markets and User Journeys

A hallmark of a well-built orchestration system is the predictable way transactions behave across markets, devices, channels and customer segments. Whether a customer is paying from a mobile device in Portugal or a desktop in Canada, the orchestration layer produces a consistent transaction signature. This reduces issuer confusion, stabilises approval outcomes and minimises unnecessary risk weighting.

Case Study Models: How Orchestration Behaves in Real Merchant Scenarios

While orchestration is often described conceptually, its value becomes most visible when applied to real operational environments. The following Micro Case Files illustrate how different merchant types experience material performance improvements through orchestration in 2026.

These examples avoid storytelling and focus strictly on technical events, behavioural patterns and measurable outcomes.

Case File A: European Gaming Merchant Stabilising Volatile Corridors

Situation:

A regulated gaming operator processed traffic from multiple EU cardholders through a single acquirer. Approval rates fluctuated significantly during issuer rule changes and scheme-level risk tightening events. Metadata inconsistencies across mobile and desktop channels amplified decline clusters.

Intervention:

The merchant implemented orchestration with unified metadata formatting, issuer-specific routing, and authentication alignment for high-risk BIN ranges. Real-time monitoring identified a corridor with repeated soft declines, triggering automated fallback.

Outcome:

Approval rates increased across the primary corridor, with reduced volatility during issuer risk adjustments. The merchant also achieved more predictable SCA outcomes across returning players.

Case File B: Subscription Platform Reducing Recurring Billing Failures

Situation:

A global subscription merchant experienced recurring billing declines due to issuer sensitivity around credential-on-file behaviour, inconsistent descriptor formatting and region-specific SCA logic.

Intervention:

Orchestration implemented structured recurring indicators, harmonised descriptors across acquirers and mapped BIN-based authentication variations. A retry engine re-attempted failed billing cycles with updated metadata rather than repeating identical requests.

Outcome:

Recurring payment recovery improved significantly, reducing involuntary churn and lowering issuer friction associated with repeat charges.

Case File C: Marketplace Managing FX Exposure During Cross-Border Expansion

Situation:

A high-volume marketplace processed mixed-origin traffic through acquirers that imposed multiple FX layers. Slippage and reconciliation discrepancies increased as new corridors were opened, affecting financial predictability.

Intervention:

Orchestration added FX-aware routing rules, selecting acquirers whose processing and settlement currencies aligned more closely with issuer geography. This reduced double-conversion paths and eliminated inconsistent metadata fields that caused misclassification.

Outcome:

FX variance decreased, settlement forecasts became more accurate and reconciliation timelines improved across the merchant’s multi-currency portfolio.

Case File D: Digital Goods Merchant Addressing Soft-Decline Saturation

Situation:

A digital content platform faced high soft-decline saturation due to rapid-fire retries from a legacy gateway. Issuers interpreted the pattern as risk escalation, worsening approval performance.

Intervention:

Orchestration applied a controlled retry structure: spacing, authentication refresh, updated SCA flags, and alternative acquirer routing for second attempts. Device and behavioural data were enriched before retrial.

Outcome:

Soft-decline recovery improved as issuers no longer received repeated identical requests. Approval stability increased during peak campaign periods.

Case File E: Travel Merchant Normalising Multi-PSP Data Fragmentation

Situation:

A travel aggregator used several PSPs, each producing inconsistent transaction formats. Issuers received variable metadata, triggering elevated fraud scoring across certain corridors.

Intervention:

The orchestration layer normalised metadata fields, aligned SCA values and unified device signals across all PSP entry points. BIN-based routing paths were aligned with acquirers known to prefer structured travel MCC profiles.

Outcome:

Metadata consistency significantly improved issuer trust scoring. Approval uplift was strongest on long-haul corridors previously affected by inconsistent data signatures.

These micro case files demonstrate how orchestration provides measurable value across different merchant models. The common thread is consistency: unified metadata, adaptive routing and structured authentication behaviour materially improve performance, regardless of industry or traffic composition.

How Merchants Should Build Their Orchestration Strategy for 2026: A Strategic Roadmap

Building an effective orchestration strategy in 2026 requires more than connecting multiple PSPs or enabling fallback routing. Merchants need to establish an operational and technical foundation that ensures the orchestration layer can interpret data accurately, react to issuer behaviours and align connected acquirers into a coherent performance framework. The strategy must be deliberate, sequenced and centred around transaction consistency.

Below is the 2026 orchestration roadmap, structured into strategic phases rather than feature lists.

Establish a Unified Data Foundation

All orchestration outcomes depend on transaction data quality. Before routing logic can be optimised, merchants must ensure the information flowing into the orchestration layer is complete, structured and uniform across channels. This involves harmonising device signals, standardising customer identifiers, normalising address formats and aligning authentication values. Without this foundation, routing and SCA logic become reactive rather than predictive.

Map Corridor Behaviour and BIN-Specific Patterns

A high-performing strategy acknowledges that issuers respond differently across BIN ranges and regions. Merchants need visibility into how each corridor behaves under varying conditions, risk thresholds, authentication friction, FX pathways and acquirer performance swings. With this mapping in place, orchestration can apply routing or authentication logic that matches issuer acceptance patterns, creating a behaviour profile that issuers recognise as consistent.

Align Authentication Pathways With Regional Requirements

Authentication surfaces as one of the most influential levers in approval optimisation. Merchants should configure orchestration engines so that authentication flows adapt by BIN, issuer and corridor. This includes determining when exemptions should be requested, when challenges should be forced and how frictionless flows should be prioritised. Alignment between authentication behaviour and issuer preference becomes critical for high-risk or cross-border corridors.

Build an Acquirer Distribution Model That Reduces Exposure

A strong orchestration strategy avoids concentration risk. Rather than allocating volume randomly across acquirers, merchants should design a distribution structure that supports corridor resilience. This includes identifying acquirers with strengths in specific regions, monitoring how risk appetite varies by MCC and determining fallback relationships that activate only when performance conditions deteriorate. The goal is not to maximise the number of acquirers but to match them to transaction behaviour strategically.

Integrate FX and Settlement Logic Into Routing Decisions

FX costs and settlement variance influence both financial performance and approval outcomes. Merchants should embed FX considerations directly into orchestration routing logic, selecting paths that minimise redundant conversions, avoid unnecessary currency mismatches and reduce volatility during settlement. This strengthens reconciliation accuracy and reduces the operational noise that often arises from inconsistent currency flows.

Implement Real-Time Monitoring and Behavioural Feedback Loops

A sustainable orchestration strategy requires continuous feedback. Merchants must deploy monitoring systems capable of detecting issuer-level changes, corridor anomalies, rising soft-decline patterns or authentication degradation. When this intelligence feeds back into routing and authentication logic, merchants shift from reactive corrections to proactive optimisation. This turns orchestration into a behaviour-shaping system rather than a simple routing engine.

Govern the Ecosystem Through Policy, Not Individual Connections

The final stage of a mature orchestration strategy is to govern the system through centralised rules rather than individual PSP connections. Policies define how transactions should behave under certain conditions, high-risk BIN ranges, SCA timeouts, MCC rejections, corridor disruptions or FX spikes. With orchestration acting as the enforcer of these policies, merchants gain a scalable, predictable payments environment across all markets.

Conclusion

In 2026, payment orchestration is no longer a competitive advantage reserved for advanced merchants; it has become the operational baseline required to achieve stability across global corridors. As issuer risk models mature, PSD3 raises data quality expectations and acquirers refine their behavioural thresholds, merchants must control how each transaction is constructed, authenticated and routed. Traditional gateways cannot provide this control, leaving merchants exposed to unnecessary declines, volatile corridor performance and fragmented metadata.

Orchestration solves these structural problems by creating a unified decision layer above all PSPs and acquirers. It delivers consistent transaction signatures, adapts authentication pathways to issuer expectations, and continuously redirects traffic based on live performance signals. Merchants gain a stable environment where approval rates are driven by predictable transaction behaviour rather than external volatility.

For acquirers and issuers, orchestration simplifies the ecosystem. Transactions become more coherent, data more complete and authentication outcomes more stable. The resulting predictability strengthens merchant–acquirer relationships and reduces the likelihood of derisking, especially in high-risk categories.

As payments continue to evolve, orchestration provides the architectural clarity and behavioural consistency the ecosystem now demands. Merchants that adopt it position themselves for sustained approval performance, greater corridor resilience and more efficient financial operations across every region they serve.

FAQs

1. What is a payment orchestration platform, and how is it different from a gateway?

A payment orchestration platform is a unified decision layer that manages routing, authentication, metadata, retries and acquirer selection across multiple PSPs. Unlike a traditional gateway that simply forwards transactions, orchestration governs how each payment is constructed and where it is sent based on real-time performance and issuer behaviour. This allows merchants to build consistent data patterns, improve approval rates, reduce FX inefficiencies and create corridor resilience. In 2026, orchestration is considered a strategic payments architecture rather than an integration tool.

2. How does orchestration improve approval rates for high-risk merchants?

High-risk merchants face heightened issuer scrutiny due to MCC sensitivity, corridor volatility and SCA failures. Orchestration improves approval performance by standardising metadata, aligning authentication flows with issuer expectations, and intelligently routing transactions to better-performing acquirers. It also reduces soft-decline loops by restructuring retry attempts. These improvements make transaction behaviour more predictable and reduce the number of false positives generated by issuer risk engines.

3. Can orchestration help with PSD3 compliance requirements?

Yes, PSD3 places stronger emphasis on structured transaction data, authentication clarity and monitoring accountability. Orchestration platforms support compliance by normalising metadata, standardising SCA values, maintaining cohesive audit trails and ensuring acquirers receive consistent information. They also enable routing decisions that reduce FX mismatches, lower operational noise and improve issuer scoring outcomes, all of which align with PSD3’s strengthened expectations for PSPs and merchants operating cross-border.

4. Do merchants need multiple acquirers to benefit from orchestration?

While multi-acquirer setups unlock the strongest orchestration benefits, merchants can still gain value with fewer acquirers. Even with two acquiring partners, orchestration enables corridor-specific routing, fallback logic, improved authentication behaviour and enriched metadata. The core benefit is behavioural consistency rather than acquirer quantity. As merchants expand, orchestration scales naturally by adding additional routes without disrupting existing architecture.

5. How does orchestration reduce FX losses and settlement inconsistencies?

FX losses often arise from unnecessary currency conversions, mismatched processing currencies and volatile rate behaviour across corridors. Orchestration reduces these inefficiencies by selecting acquirers with optimal currency alignment, minimising conversion layers and stabilising settlement timing. It also enforces metadata consistency so acquirers categorise transactions correctly. This reduces slippage, improves reconciliation accuracy and gives merchants more predictable settlement outcomes.

6. Does orchestration lead to higher costs for merchants?

Not necessarily. While orchestration platforms involve service fees, the financial value typically outweighs the cost. Improved approval rates, reduced FX losses, lower operational workload, optimised acquirer distribution and fewer dispute escalations collectively generate measurable savings. For high-risk or cross-border merchants, these gains are often significant, making orchestration a net-positive model rather than an added expense.

7. How does orchestration impact SCA and authentication performance?

Authentication failures are a major source of cross-border declines. Orchestration enhances SCA outcomes by adapting challenge behaviour to issuer profiles, applying exemptions intelligently and using metadata enrichment to support frictionless flows. It can also redirect authentication to alternative ACS pathways when required. These improvements ensure authentication behaviour aligns with issuer risk expectations, significantly boosting challenge success rates.

8. Can orchestration help merchants experiencing high decline rates in specific corridors?

Yes, decline clusters often stem from corridor-specific conditions such as inconsistent metadata, incorrect routing, issuer risk weighting or SCA discrepancies. Orchestration identifies these anomalies through real-time monitoring and adjusts routing paths, authentication logic and data formatting accordingly. Merchants gain the ability to isolate corridor issues and react quickly, improving approval stability across challenging regions.

9. Is orchestration suitable for subscription or recurring billing models?

Subscription merchants benefit significantly from orchestration due to its ability to structure recurring indicators, normalise descriptors and refresh authentication values for repeat transactions. Many recurring declines stem from outdated credentials or issuer restrictions on repeated attempts. Orchestration transforms the retry process by updating metadata and selecting better acquirers for second attempts, improving recovery rates and reducing involuntary churn.

10. How does orchestration support acquirer relationships?

Acquirers prefer merchants who present consistent, well-structured transaction data. Orchestration delivers predictable behavioural patterns, stable authentication flows and balanced corridor distribution. This lowers acquirer risk exposure, reduces operational investigation workload and strengthens their appetite for the merchant’s traffic. Over time, this results in improved commercial terms, better corridor coverage and greater resilience against derisking events.

11. What is the first step a merchant should take when implementing orchestration?

The first step is data unification. Before routing logic can be effective, merchants must ensure consistent device information, address formats, authentication values and customer identifiers across all channels. With a unified data foundation, orchestration can make accurate routing and authentication decisions. This ensures performance gains appear quickly and sustainably across all corridors.