The warning signs usually appear at the boarding gate. A passenger’s name is on the manifest, the ticket number checks out, and the payment was “approved” days ago. Yet an airline agent pulls the traveller aside, the booking has been flagged, the cardholder has disputed the transaction, and the ticket has effectively turned into a liability. By the time the aircraft leaves the stand, the airline is already absorbing the loss. The real fraudster is nowhere near the airport. They cashed out hours earlier, having resold the stolen-ticket itinerary through a fake online travel agency operating on WhatsApp, Instagram, or a throwaway shop domain.

Scenes like this are no longer exceptions; they are the cost of doing business in a digital travel economy. Airlines, OTAs, consolidators, and ticketing platforms now operate in one of the top three most fraud-exposed industries globally, driven by the perfect combination of high-value transactions, global payment fragmentation, and rapid customer movement across borders, channels, and devices. In 2024–2025, industry studies show that ticketing fraud, loyalty account breaches, and synthetic identity abuse have accelerated far faster than traditional card fraud controls can respond, pushing acquirers to classify travel merchants as ultra-high-risk and tightening underwriting standards accordingly.

At the centre of this shift is a single, structural reality: modern travel fraud is no longer about stolen cards, it is about stolen identities. Fraudsters now deploy AI-generated documents, deepfake-enhanced traveller profiles, and hybrid synthetic identities that slide past conventional KYC, 3DS, and transaction scoring. These identities aren’t just used to buy tickets; they are used to open loyalty accounts, abuse promotions, apply for BNPL travel credit, and recycle refunds into multi-rail payouts. In this new environment, a fraudulent booking no longer ends at a chargeback; it propagates through an airline’s entire ecosystem, from seat inventory to loyalty liability to settlement exposure with PSPs, BSP/ARC systems, and acquirer partners.

By 2026, this shift forces a simple but critical realisation:

Fraud at 35,000 feet is fundamentally an identity problem, and payments are only the surface where it becomes visible.

The travel merchants who remain “bankable” in this high-risk climate will be those who adopt identity-first security, behavioural analytics, cross-channel risk orchestration, and real-time collaboration with acquirers, IATA networks, and global fraud intelligence frameworks. Everyone else will face escalating chargebacks, ADMs, frozen merchant accounts, and an erosion of trust with partners and regulators.

- The Modern Fraud Surface in Airline & Travel Payments

- Synthetic Identities: The Invisible Passengers in Your Booking Funnel

- Anatomy of a Fraud Journey: How a Ticket Is Stolen, Sold, and Eventually Disputed

- 3DS2, Tokenisation & Smart Routing: Fixing the Cross-Border Decline Problem

- Real-Time Screening & Behavioural Analytics: What a 2026 Fraud Stack Looks Like

- Collaboration Frameworks: The New Era of Shared Fraud Intelligence

- Regional Fraud Profiles: How Travel Fraud Differs Globally

- The 2026 Fraud Prevention Playbook for Travel PSPs & Merchants

- Conclusion:

- FAQs

The Modern Fraud Surface in Airline & Travel Payments

Fraud Vector #1: Stolen Cards & High-Risk CNP Ticketing

Problem:

Bookings in the travel industry, especially via online or mobile channels, often occur as card-not-present (CNP) transactions. Fraudsters exploit this environment, purchasing high-value tickets with stolen credentials and reselling them, leveraging the speed and complexity of travel commerce to evade detection.

Insight:

A study by Ravelin found that 53% of travel sector companies report losses of US$10 million or more per year due to online fraud. Source:

Further, according to Accertify data, the global fraud-pressure rate for airlines in H1 2025 dropped to 0.25% (one attempt per every 400 bookings). While the rate is comparatively low, the value of individual bookings (often several thousand dollars) means the financial impact per fraud attempt is disproportionately large in travel.

Solution:

Merchants and acquirers must deploy layered defences for CNP ticketing:

- Bin intelligence and card-holder behavioural profiling (e.g., frequent one-way bookings, high-value itineraries).

- Risk-based challenge for high-value tickets (for example, integrate dynamic 3DS2 logic, as will be discussed in later sections).

Fraud Vector #2: Fake Travel Agents, OTA Imitators & Triangulation

Problem:

Fraudsters increasingly operate fake or compromised online travel agent (OTA) platforms, purchasing tickets with stolen credentials, then reselling the tickets to unsuspecting end-users at a discount, a scheme known as triangulation. The merchant (airline or legitimate OTA) fulfils the service, unaware that the original cardholder may dispute the transaction later, leaving the payout chain exposed.

Insight:

Research indicates that airlines lose about 1.2% of online revenue to payment fraud (and this number excludes related abuse such as loyalty programme fraud). Additionally, the existence of “dark web travel agencies” has been publicly reported: a 2025 news article estimates around US$37 billion in fraudulent online travel transactions globally in the past year.

Solution:

Merchants and acquirers need to apply robust merchant onboarding and agent-monitoring protocols:

- Monitor agent booking patterns for unusual resale behaviour or unusual BIN-to-PNR links.

Fraud Vector #3: Loyalty Program Abuse & Miles Theft

Problem:

Loyalty programmes are rich fraud targets: low friction in account creation, high value of rewards (flights/hotels), and often weaker authentication controls than payment rails. Fraudsters exploit these weaknesses to create fake or synthetic accounts, transfer points, and redeem them for high-value tickets or black-market resale.

Insight:

According to the Sift Digital Trust Index (Q1 2025), rewards-programme points recorded the highest fraud attack rate at 6.19%, surpassing other alternative payment methods and signalling a shift upstream in fraud tactics.

Solution:

- Integrate loyalty accounts into the fraud-monitoring stack as a high-value asset.

- Apply stronger identity proofing at account creation (especially for high-tier status).

- Monitor transfers or redemptions of miles points in unusual patterns (e.g., across multiple accounts, or rapid accumulation then redemption).

Fraud Vector #4: Refund, Voucher & Credit Abuse

Problem:

After the initial ticket sale, travel merchants face further risks: refunds to alternate rails, vouchers issued and resold, no-shows, and chargebacks. Fraud cycles often extend into the post-travel phase and can cost far more than the ticket value through settlement fees, administrative costs and merchant downgrades.

Insight:

A report by Chargeback Gurus indicates that friendly fraud (chargebacks by customers) can account for nearly 40% of all chargebacks in the travel & hospitality industry. Also, large-scale fraud vulnerabilities are not restricted to booking; decay in loyalty or voucher environments continues to drive cost.

Solution:

- Define strict voucher/offer-redemption processes (e.g., link to the same identity, device, booking chain).

- Implement chargeback-deflection strategies: gather granular evidence (PNR, IP, device, itinerary) at booking time to support disputes.

- Treat refund pathways as high-risk rails and subject them to screening (e.g., reversal requests, alternate-rail destination).

Fraud Vector #5: BNPL & Cross-Border High-Value Ticket Fraud

Problem:

With affluent travellers and international bookings driving high-ticket average values, the rise of Buy-Now-Pay-Later (BNPL) and alternative payment methods presents exacerbated risk for ticketing fraud. Fraudsters exploit the weaker underwriting and the high ticket values to maximise value.

Insight:

While specific travel-vertical BNPL data is limited, industry commentary confirms that fraudsters are shifting into alternative payment methods and high-value segments where authentication is often weaker.

Solution:

- Apply value-threshold monitoring for high-ticket bookings, combining identity scoring, velocity, and geographic risk.

- Leverage network tokens (for card payments) and dynamic routing to reduce exposure on direct-card transactions.

Synthesis: Mapping the Travel Merchant Fraud Surface

Insight:

Rather than discrete fraud types, travel merchants operate across an integrated surface composed of: card credentials (CNP), agent networks, loyalty assets, refund rails, alternative payments, and global bookings. The underlying enabler across these vectors is identity manipulation, whether via stolen credentials, fake agents or synthetic personas.

Solution:

Merchants, PSPs and acquirers must adopt a layered architecture combining:

- Identity proofing & behavioural analytics

- Transaction scoring & routing

- Post-transaction monitoring (refunds, loyalty, chargebacks)

- Data sharing (agents, acquirers, loyalty networks)

Merchant Takeaway:

High-value travel bookings deserve bespoke fraud rules, treat BNPL and cross-border payments as enhanced-risk rails, not as “normal checkout” flows.

Synthetic Identities: The Invisible Passengers in Your Booking Funnel

What Synthetic Identity Fraud Really Looks Like in 2026

Problem:

Fraud is no longer simply about stolen credit cards; the industry’s most significant risk vector today is the synthetic identity. These are personas built partly from real personal data and partly from fabricated details; they can pass KYC checks and live undetected for months, even years.

For travel merchants and PSPs, the problem becomes especially acute: synthetic travellers can create multiple accounts, collect loyalty points, book high-value tickets, issue refunds, or open BNPL accounts, all under the radar of traditional fraud controls.

Insight:

According to TransUnion, synthetic identity exposure for U.S. lenders grew to US $3.3 billion in 2024, with new account openings under synthetic IDs increasing.

Meanwhile, the Boston Federal Reserve highlights how generative AI is enabling fraudsters to generate highly convincing synthetic identities at scale, including fabricated images, documents and social-media footprints. Federal Reserve Bank of Boston In the travel/loyalty domain, a survey found 46% of all fraudulent transactions now involve airline reward programmes, which are increasingly prone to synthetic-identity abusers.

Solution:

To combat this, travel-facing merchants and PSPs must adopt an “identity-first” strategy:

- Deploy enhanced ID verification at account creation, including document forensics, device-and-behavioural biometrics and cross-device link-analysis.

- Continuously monitor account creation, login and behavioural anomalies (e.g., multiple high-value bookings from a newly created identity).

- Integrate loyalty and booking systems into the fraud stack, treat synthetic IDs as high-value asset risks, not only payment risks.

How Synthetic Identities Exploit Travel Payments

Problem:

Synthetic identities find multiple levers in the travel ecosystem: they open fraudulent user accounts (on OTAs or airline portals), make bookings using stolen credentials, build loyalty balances, then redeem or transfer value. Because they may appear benign for many months, they exploit the delay and trust built into travel commerce.

Insight:

Fraud-behaviour lifecycle studies show that synthetic IDs often undergo “incubation”, making harmless transactions and building identity-legitimacy (for example, small bookings, loyalty activity) before executing high-value fraud.

In travel, this can play out as: synthetic account created → small booking + loyalty accrual → multiple bookings layered → one large ticket or voucher transfer → fraud hit. For example, a travel brand saw up to 97% legit redemption rate for trusted users, yet the synthetic-ID monitoring system flagged 94% of fraudulent login attempts in a year.

Solution:

- Link identity attributes (device, email, phone, IP, behavioural patterns) across booking/loyalty/payment systems.

- Use temporal analytics: a new identity making high-value bookings within weeks is anomalous.

- Apply tiered controls: newly onboarded accounts face extra scrutiny until an established trust baseline is reached.

The Identity-First Security Trend in Travel

Problem:

Traditional payment fraud controls (card-BIN checks, CVV/AVS, transaction scoring) are increasingly bypassed when the attacker is a synthetic identity that seems legitimate, at least initially. The merchant may approve a booking, a voucher is issued, the route flown, and only later do chargebacks, loyalty theft, or ADMs trigger. The visibility window is too late.

Insight:

Industry reviews indicate that digital document forgeries have increased by over 244% in recent years, and generative-AI tools make the fabrication of identity assets cheaper and faster.

For travel merchants: identity verification systems that integrate device, behavioural, loyalty and booking-history data are becoming mission-critical.

Solution:

- Introduce “identity score” thresholds for high-risk actions: loyalty redemption over threshold, refund to new rails, and one-way high-value bookings.

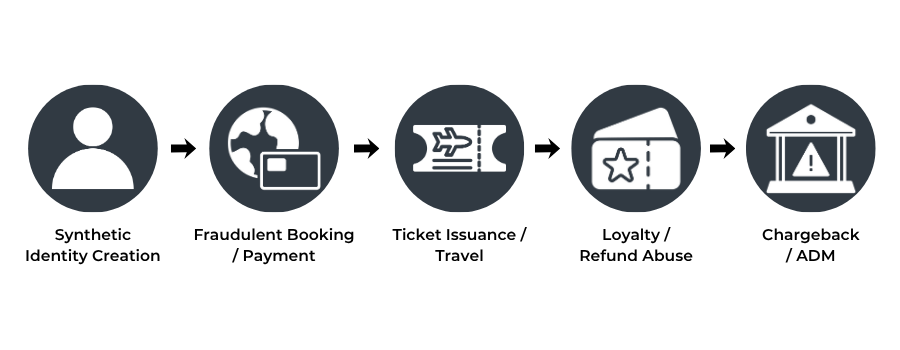

Anatomy of a Fraud Journey: How a Ticket Is Stolen, Sold, and Eventually Disputed

Fraud in travel rarely appears at the point where the merchant first notices it. By the time a chargeback arrives, or an Agency Debit Memo is issued, the damage was set in motion days, even weeks, earlier. Ticketing fraud is not a single event; it is a sequence, and each stage exploits a different weakness across identity verification, booking flows, and global payment rails.

Understanding this journey is essential for PSPs, acquirers, and travel merchants operating in a high-risk environment where fraud losses are concentrated in a small handful of transactions that slip through multiple layers of controls.

Stage 1: A Synthetic Identity Is Created

Every modern ticketing fraud scheme begins with an identity, but not a real one. Criminal groups today rely on identities built from fragments of genuine personal information merged with fabricated details. Europol has warned that organised crime networks increasingly use digitally altered or AI-generated identity artefacts to bypass online verification procedures, enabling synthetic users to interact with merchant systems undetected.

Source: Europol – Identity Crime in the Digital Age

These identities are then used to open travel accounts, create loyalty profiles, join promotional programmes, or act as the “front” for fake travel agencies and reseller operations.

Stage 2: A Fake OTA or Discount Travel Page Goes Live

Once the synthetic identity is established, fraudsters set up a storefront. This might be a simple website with scraped airline branding, or more commonly, a WhatsApp or Instagram-based “travel agent” offering discounted fares.

INTERPOL has carried out multiple multinational operations exposing these illicit travel agents, confirming that thousands of airline tickets purchased with compromised cards are resold to unsuspecting travellers every year.

Source: INTERPOL – Operation Hydra / Airline Ticket Fraud

These pages attract genuine customers, families, students, and migrant workers who believe they are buying a legitimate discount fare. In reality, they are buying a ticket funded by a stolen card.

Stage 3: The Stolen Card Transaction Runs Through a Legitimate Airline or OTA

The illicit agent now books a ticket using stolen payment credentials. For the airline or OTA, it appears as an ordinary inbound CNP (card-not-present) transaction. Because travel merchants often prioritise rapid ticketing, the booking passes into the queue quickly.

According to the European Central Bank, more than 80% of the value of card fraud in Europe now comes from card-not-present transactions, making digital travel sales one of the most exposed sectors in payments.

Source: European Central Bank – Card Fraud Report

To the fraudster, this is the moment the scheme succeeds: the ticket is issued, the fake agent receives payment from the customer, and the stolen card funds the transaction.

Stage 4: The Traveller Flies and the Fraud Matures

The genuine passenger, who purchased the ticket from the fraudulent agent, goes on to complete the journey normally. Airline and airport systems recognise the ticket as valid. The seat is flown. The value is consumed.

Meanwhile, the original cardholder still has no visibility of the transaction. There is no complaint, no alert, no dispute, not yet.

INTERPOL and Europol both highlight that this “silent delay” is one of the key reasons travel fraud is so damaging: the service is delivered long before the fraud is detected, and merchants lose any chance of recovery once the aircraft departs.

Sources: Europol – Airline ticketing fraud operations

By the time the fraud surfaces, the criminal is long gone, and the merchant is left with the financial liability.

Stage 5: The Dispute Arrives Chargeback, ADM, or Settlement Loss

The fraud is finally discovered when the legitimate cardholder notices the unauthorised transaction and initiates a dispute. Under EU law, unauthorised card transactions fall squarely under strong consumer protection rules, meaning the merchant must absorb the loss unless it can provide compelling evidence of authentication.

For airlines and OTAs, the cost is not limited to the refund:

- The dispute may trigger an ADM (Agency Debit Memo) under IATA rules.

- Excessive card disputes may trigger acquirer monitoring, increased reserves, or termination.

- In markets like the UK, the Payment Systems Regulator emphasises that cross-border fraud disputes impose a significant financial and operational burden on high-risk merchants.

The fraud journey that began with a synthetic identity ends with a direct earnings loss, reputational risk, and potential merchant-account instability.

Why This Matters: Fraud at 35,000 Feet Is a Whole-System Breakdown

Each stage of the fraud journey exploits a different part of the travel commerce ecosystem:

- Identity verification

- Merchant onboarding

- CNP payment authentication

- Ticketing workflows

- Dispute and settlement processes

A weakness at any point allows fraud to propagate across all of them.

This is why ticketing fraud is so hard to fight: it is not a payment problem, but a system-level identity and trust problem.

3DS2, Tokenisation & Smart Routing: Fixing the Cross-Border Decline Problem

Cross-border travel payments remain one of the most challenging environments for airlines, OTAs and PSPs. High transaction values, multi-country issuer–merchant combinations, and fragmented SCA requirements often lead to false declines, a problem that damages revenue and creates openings for fraudsters. By 2026, the most resilient travel merchants will be those who adopt intelligent authentication strategies, tokenisation, and smart routing methods that reduce unnecessary friction while keeping fraud in check.

Using 3DS2 Intelligently (Not Blanket Challenges)

Strong Customer Authentication (SCA) under EU rules was never designed to be a blanket challenge mechanism, yet many travel merchants continue to apply 3DS2 uniformly across all transactions. This approach increases abandonment, depresses approval rates, and does little to prevent sophisticated cross-border fraud.

The European Banking Authority has clarified repeatedly that SCA must be applied through a risk-based approach, allowing exemptions when risk indicators are low and mandating challenges only when justified.¹ For airlines and OTAs, this creates a strategic opportunity: challenge where risk is genuinely elevated, streamline where the customer and corridor demonstrate low exposure.

Where intelligent 3DS2 pays off

- Route-based exemptions: Low-risk, intra-EEA routes can often qualify for SCA exemptions.

- High-risk corridor logic: Long-haul, last-minute, and mismatched IP–issuer–merchant geography combinations should escalate to full 3DS2.

- Airline-specific risk populations: Frequent fliers, enrolled loyalty members, and previously authenticated profiles benefit from frictionless flows.

When tuned correctly, 3DS2 becomes an asset rather than a conversion cost, a targeted gatekeeper that protects high-risk transactions without undermining legitimate travellers.

Network Tokenisation for Travel

Tokenisation is now a central pillar of global card policy. Visa, Mastercard, and the European Commission all endorse tokenisation as a key safeguard against online fraud, helping merchants reduce exposure to raw card data.

For travel merchants, tokenisation delivers three critical advantages:

1. Preventing account takeover for stored cards

Stored credentials held in airline or OTA profiles are highly attractive to fraudsters. Using tokens instead of primary account numbers (PANs) limits the value of breached data.

2. Improving cross-border approval rates

Tokens provide issuers with richer metadata and lifecycle context, easing approval decisions, especially across high-friction corridors.

3. Protecting loyalty & wallet-linked payments

Many loyalty ecosystems now link points redemption or wallet payouts to a stored card. Tokenising these rails reduces the risk of fraudulent redemptions and synthetic ID laundering.

Regulators in the EU have recognised tokenisation as part of the broader payments-security upgrade under PSD3 and PSR, further signalling its relevance for 2025-2026-standard merchant compliance.

PSP/Acquirer Smart Routing for Travel Merchants

Even with strong authentication and tokenisation, approval rates can deteriorate when transactions travel across multiple regions, currencies, and network configurations. For this reason, travel merchants increasingly rely on smart routing strategies supplied by PSPs and acquirers.

Where smart routing makes the difference

- Multi-acquiring: Working with more than one acquirer diversifies routing pathways and reduces reliance on a single risk engine.

- Currency choice: Presenting the transaction in a currency preferred by the issuer (or in the traveller’s home-market currency) can significantly improve approvals in cross-border environments.

- High-risk BIN controls: Certain issuer ranges consistently present elevated dispute or decline rates. Routing through alternative acquirers or additional KYC steps minimises unnecessary exposure.

The European Commission’s push for improved transparency and interoperability in EU payment frameworks signals that PSPs must strengthen routing logic and real-time coordination across borders. For travel merchants, this is central to reducing false declines without weakening fraud defences.

Fraud prevention and conversion are no longer opposing goals. By applying 3DS2 intelligently, adopting network tokenisation, and routing transactions in line with issuer expectations, travel merchants can:

- Increase approvals

- Reduce fraud

- Protect loyalty and stored-card ecosystems

- Stabilise acquirer relationships

In a cross-border marketplace where a large portion of travel bookings originates outside a merchant’s home region, the technical sophistication of the payment stack directly determines both revenue and risk posture.

Real-Time Screening & Behavioural Analytics: What a 2026 Fraud Stack Looks Like

Travel fraud has evolved beyond static rules and transactional checks. By 2026, the most effective defences will increasingly rely on behavioural intelligence, continuous device analysis, and real-time orchestration that connects payment data with booking patterns and itinerary behaviour. This reflects a wider regulatory trend: European authorities continue to emphasise the importance of strong, dynamic fraud monitoring across the full payment cycle, not just during authentication.

For airlines and OTAs, this shift means adopting a fraud stack that behaves more like a living system than a set of fixed controls.

Device Fingerprinting + Velocity Bundles

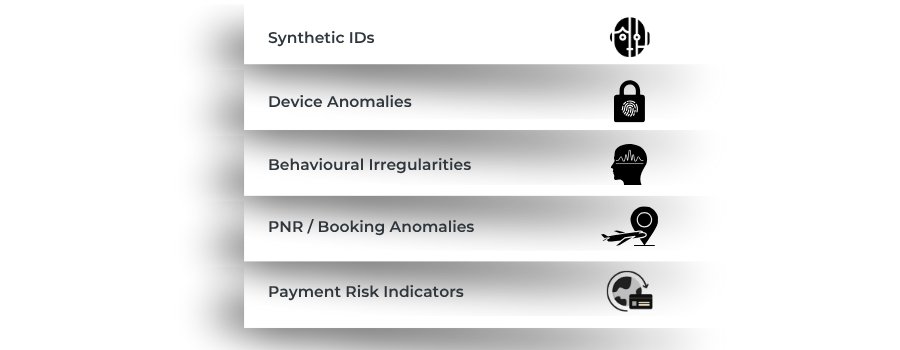

One of the most reliable early-warning indicators in travel fraud is the device. Fraudsters consistently rotate between VPNs, emulators, newly minted devices, and shared digital fingerprints that appear across unrelated booking attempts. Identifying these patterns early disrupts synthetic identity creation and payment abuse long before the card is charged.

Regulators increasingly expect merchants and PSPs to track behavioural anomalies. The European Payments Council’s Payment Threats & Fraud Trends report highlights abnormal device behaviour, geo-spoofing and automated booking flows as key threat drivers across cross-border digital payments.

How travel merchants apply these insights

- Linking devices → identities → itineraries

- Applying velocity rules to prevent cycling of bookings (e.g., multiple attempts for different passengers within minutes)

- Flagging mismatches between device location and claimed traveller origin

In the travel sector, where itinerary value can be thousands of pounds, early device-based alerts often outperform late-stage payment checks.

Behavioural Biometrics for Travel Flows

Behavioural analytics have become a critical differentiator in distinguishing genuine travellers from fraud operators. Factors such as typing cadence, navigation style, scroll behaviour, timing patterns during form completion, and even how a mobile device is handled provide a subtle but powerful authentication layer.

This approach aligns with the trajectory set by European regulators: PSD2/PSD3 frameworks explicitly encourage the incorporation of “inherence” factors, behaviours or characteristics unique to a user, as part of Strong Customer Authentication.

Where behavioural signals help in travel

- Spotting bot-driven booking scripts

- Distinguishing legitimate customers from synthetic profiles created in batches

- Identifying unusual movement through booking flows (skipping fields, autofill spikes, inconsistent timing)

- Detecting remote-access Trojan behaviour or session hijacking

For airlines and OTAs, behavioural biometrics serve as an invisible checkpoint that adds security without friction.

Risk AI Using PNR + Payment Data

One uniquely powerful asset in travel is the Passenger Name Record (PNR), a structured dataset containing itinerary details, passenger information, travel timing, and booking behaviour. When combined with payment intelligence, PNR becomes a high-value tool for fraud detection.

The European Commission’s aviation and passenger-data regulations reinforce the importance of robust data governance and cross-checking of PNR information for security and risk assessment. Although these frameworks were originally designed for border and aviation security, the same principles can be applied within merchant fraud systems, provided data protection rules (e.g., GDPR) are respected.

What PNR-linked fraud detection uncovers

- Unusual flight combinations or rapid multi-leg routes

- Seat map anomalies (strange seat-selection clusters seen across different identities)

- Bookings inconsistent with past travel behaviour

- Loyalty profiles redeemed in atypical patterns

By connecting PNR data with payment-risk engines, merchants gain a real-time view of fraud signatures that would otherwise look like normal purchases.

Behavioural intelligence, device forensics and PNR-integrated risk models now define the modern travel fraud stack. Static rules are no longer capable of protecting high-value bookings in a fast-moving, cross-border environment. The merchants and PSPs that invest in these real-time systems will not only reduce fraud but also increase approval rates, positioning themselves as low-risk partners for acquirers going into 2026.

Collaboration Frameworks: The New Era of Shared Fraud Intelligence

Travel fraud is not a threat that any single airline, OTA, PSP, or acquirer can tackle alone. Fraudsters move across borders, exploit weak links in global distribution systems, and operate through digital identities that slip across multiple platforms. By 2026, coordinated intelligence-sharing has become one of the strongest defences in the travel ecosystem, not only across merchants and PSPs, but also through industry regulators, aviation bodies, and settlement networks.

Collaboration is no longer optional; it is an operational requirement.

IATA, ARC & BSP Risk Requirements

The travel industry’s settlement networks, particularly IATA’s BSP (Billing and Settlement Plan) and ARC in North America, increasingly influence how fraud is managed. These systems were originally designed for reconciliation, but rising fraud has forced them to tighten controls around agent behaviour, ticketing anomalies, and settlement integrity.

Why this matters

- IATA’s global security bulletins emphasise the growing role of fraudulent agencies, ticketing manipulation and misuse of stolen payment cards in global bookings.

- IATA resolutions allow airlines to issue Agency Debit Memos (ADMs) for improper transactions, a major pain point for OTAs with weak fraud controls.

What this means for merchants

- Agents must be vetted through formal accreditation checks (IATA ID, local licensing).

- Airlines and OTAs must monitor for abnormal ticketing patterns, excessive void/reissue behaviour, and last-minute high-value bookings.

- PSPs underwriting travel merchants must screen for high-risk agency operational models.

Acquirer + PSP Data Sharing

Acquirers and PSPs sit at the centre of transaction-level intelligence. Yet historically, many fraud signals remained siloed due to privacy concerns or commercial separation. Regulators are now pushing for structured data-sharing to increase fraud visibility across PSPs.

Regulatory direction

Where does this help travel?

- BIN-level fraud alerts allow travel PSPs to route suspicious issuer ranges differently.

- MCC-specific datasets highlight fraud patterns in MCC 4511 (airlines) and 4722 (travel agencies).

- Acquirer-level anomaly detection helps spot abnormal booking spikes or synthetic ID clusters.

Source:

Council of the European Union – Press Release on modernising EU Payments Framework (2025)

Airline Alliances & GDS Networks

Global Distribution Systems (GDS) and airline alliances represent another critical collaboration layer. These networks link airlines, agents, and booking platforms through shared PNR, itinerary, and ticketing structures, making them uniquely positioned to detect cross-carrier anomalies.

Examples of collaborative benefits

- Cross-airline PNR validation identifies inconsistent passenger details across carriers.

- Alliance-level antifraud programmes help flag itineraries involving unusually rapid multi-leg travel or irregular redemption activity.

These systems were created for operational efficiency and border security, but their fraud-prevention potential has grown dramatically as criminals exploit multi-airline itineraries for laundering ticket value.

No travel merchant can defend against fraud in isolation. The most effective approach in 2026 blends three collaboration layers:

- Industry-level oversight via IATA/ARC/BSP

- Payment-level intelligence via PSP and acquirer data sharing

- Operational-level coordination through GDS and airline alliances

Together, these mechanisms create a connected fraud perimeter, one capable of stopping criminal activity that would otherwise move silently across borders, merchants, and systems.

Regional Fraud Profiles: How Travel Fraud Differs Globally

Travel fraud is a global problem, but it does not manifest uniformly. Each region carries its own mix of regulatory expectations, payment-rail vulnerabilities, and behavioural fraud patterns. By 2026, PSPs and travel merchants must understand these differences with precision, because fraud controls built for Europe rarely withstand the dynamics of Africa, Southeast Asia, or emerging travel corridors.

This section breaks down the most relevant patterns shaping regional travel fraud today.

Europe (EU/UK)

Europe remains one of the most regulated payment ecosystems in the world, with robust authentication requirements and detailed fraud-monitoring obligations. Yet travel merchants still face elevated risks, especially in digital bookings and loyalty systems.

Strong Customer Authentication (SCA) pressures

Under PSD2, SCA is mandatory for most electronic payments within the EEA. While this significantly reduced certain fraud vectors, regulators continue to report vulnerabilities in card-not-present (CNP) travel transactions, particularly across cross-border bookings where issuers, acquirers and customer locations do not align neatly.

Growth in APP (authorised push payment) fraud

The UK Payment Systems Regulator highlights a continuous increase in authorised push payment fraud, where victims are manipulated into paying fraudulent agents or travel intermediaries directly.

In travel, these scams often appear as “discount fares” promoted via messaging apps or social channels.

High account takeover (ATO) rates in loyalty programmes

The European Commission has repeatedly emphasised the need for stronger authentication across stored-value and account-based systems, which includes airline loyalty portals increasingly targeted for point theft and voucher redemption scams.

Africa

Fraud dynamics in Africa differ substantially from Europe. While card penetration is lower, digital fraud is high due to rapid mobile-based commerce adoption, informal travel markets, and widespread use of messaging platforms for ticketing.

WhatsApp and Instagram-based “travel agents”

Many fraudulent ticket brokers operate through social media and messaging apps. INTERPOL collaborates with African law enforcement agencies to disrupt travel scams facilitated through informal digital channels.

These scams often target migrant workers and students buying cross-border tickets.

Fraudulent visa/ticket bundles

Several African jurisdictions issue recurring public warnings about fraudulent visa and ticket schemes, targeting outbound travellers moving to Europe, the Middle East, or Asia. Government consular services across multiple countries regularly publish scam alerts involving falsified itineraries, forged documents, and compromised payment methods.

Cross-border card leakage

Because many African travellers book outside their domestic region, often via European or Middle Eastern online gateways, cards issued in African markets encounter higher decline and fraud-screening rates. Regulators note that cross-border CNP transactions remain among the highest-risk categories globally.

Southeast Asia

Southeast Asia is one of the fastest-growing digital travel markets, but also one of the most fraud-exposed. High mobile adoption, super-app ecosystems, and cross-border movement create complex risk conditions.

Super-app ecosystems

Many SEA travellers book flights through super-apps combining transport, wallets, rewards and travel modules. Government digital-finance authorities in markets like Singapore and Malaysia emphasise the fraud challenges posed by integrated wallets and multi-service apps. These ecosystems can mask device or identity anomalies that traditional travel PSPs would otherwise detect.

High synthetic ID penetration

Identity fraud is a rising concern across SEA. Regional law-enforcement bodies cooperating with INTERPOL report increasing use of hybrid digital identities across travel, financial services and immigration fraud.

Where KYC consistency varies widely between markets, synthetic identities exploit the gaps.

A2A and wallet fraud patterns

Southeast Asia’s strong bank-transfer and mobile-wallet adoption (e.g., Singapore FAST, Malaysia DuitNow, Indonesia BI-FAST) has introduced significant vulnerabilities in authorised payment scams. Regulators, including Singapore’s MAS, emphasise real-time payment fraud as a priority in cross-border contexts.

Travel fraud does not travel uniformly across the globe.

- Europe struggles with cross-border CNP fraud and APP scams.

- Africa faces informal-agent fraud, document manipulation and cross-border payment leakage.

- Southeast Asia grapples with synthetic identity clusters, wallet/A2A fraud, and super-app masking.

Yet one pattern repeats across all regions:

Synthetic identities are the underlying engine powering nearly every form of modern travel fraud.

A single global fraud framework cannot protect travel merchants; only a regionally aware one can.

The 2026 Fraud Prevention Playbook for Travel PSPs & Merchants

By 2026, fraud prevention in travel is no longer a set of tools; it is a strategic function that determines whether a merchant remains bankable, compliant and operational. Airlines, OTAs, consolidators and travel PSPs now face a regulatory climate where identity controls, authentication intelligence and cross-border payment transparency are not “best practice” but minimum requirements.

This Playbook outlines the structural components required for long-term resilience.

Maturity Model (Level 1 → Level 3)

The travel sector’s fraud maturity typically falls into three tiers. Understanding where a merchant stands is the first step toward reducing risk and improving approval rates.

Level 1: Reactive

Merchants at this level rely on:

- Simple rule-based scoring

- Manual review queues

- Basic velocity limits

- Heavy reliance on 3DS challenges

Fraud losses are high, approval rates are inconsistent, and synthetic identities freely enter the system.

This mirrors the risk exposures flagged in the European Payments Council’s threat assessments, which note that businesses with weak monitoring face elevated cross-border fraud patterns.

Level 2: Integrated

Merchants begin to combine:

- Identity + device + behavioural intelligence

- Tokenisation of stored credentials

- Risk-based SCA strategy (in line with EBA requirements)²

- Early-stage synthetic ID detection

- PNR-linked anomaly checks

Fraud rates decrease, ADMs drop, and approval rates stabilise.

Level 3: Strategic

This is the 2026 benchmark for leading travel merchants:

- Identity-first screening across account creation, loyalty, and refunds

- Real-time behavioural analytics

- Fully tokenised card and wallet ecosystem

- Multi-acquirer smart routing

- Continuous fraud-data sharing with PSPs, acquirers and IATA/ARC/BSP

- Airline–PSP co-governed fraud steering groups

This approach aligns with the EU Commission and Council’s direction for a modernised, data-sharing-enabled payment framework across the EU.

Build vs Buy: Fraud Stack Decisions

Travel merchants often face a difficult decision: build an in-house fraud stack or rely on external solutions. The right decision depends on:

1. Identity infrastructure

If a merchant lacks in-house capability for document verification or ICAO-aligned identity screening, outsourcing becomes essential. ICAO’s travel-document standards are now a global benchmark for identity integrity.

2. Real-time behavioural monitoring

Building behavioural biometrics internally is resource-intensive and requires specialised expertise. Many PSPs now integrate these capabilities directly.

3. PNR + payments orchestration

Because PNR data is governed under strict EU regulations, merchants must ensure compliance when integrating travel-data analytics.

4. Multi-acquirer routing logic

Most merchants benefit from buying or partnering rather than building routing engines, as routing depends heavily on issuer-level intelligence available only to PSPs and card schemes.

A balanced approach:

Most high-risk travel merchants end up with a hybrid model, strategic internal controls combined with PSP-provided intelligence and orchestration.

Governance: Who Owns Fraud in Travel Companies

One of the biggest weaknesses in travel businesses is unclear ownership of fraud.

Fraud sits at the intersection of:

- Payments

- Product

- Operations

- Compliance

- Customer experience

- Loyalty management

Regulators consistently emphasise that fraud prevention must be a cross-functional responsibility, particularly under evolving European payments legislation.

Best-practice governance model:

- The payments team owns the transaction and routing logic

- Risk team owns identity, device and behavioural intelligence

- Ops team owns check-in, PNR validation and ADM prevention

- Compliance team ensures PSD2/PSD3, SCA and PNR regulatory alignment

- Executive ownership sits at CFO (financial risk) + COO (operational risk)

When responsibilities are clearly divided but tightly coordinated, fraud drops significantly.

Costs → ROI Mapping

For many merchants, the challenge is justifying the investment. Fraud controls cost money, but unmanaged fraud costs far more.

Key ROI drivers

- ADM reduction

Better PNR and identity integrity reduces airline-issued ADMs, which often exceed the value of the ticket itself. - Higher approval rates

Smart routing and tokenisation improve cross-border approvals, creating direct revenue uplift. - Lower acquirer reserves

As merchants demonstrate a strong fraud posture, acquirers reduce collateral requirements. - Reduced operational load

Behavioural analytics and device intelligence significantly reduce manual reviews.

The long-term equation

Fraud management in travel is not a cost centre; it is a revenue protection mechanism. For high-volume cross-border merchants, the return on fraud investment is often realised in under 90–180 days.

In 2026, a travel merchant’s competitiveness, and even survival, depends on the maturity of its fraud strategy. Identity-first screening, behavioural analytics, smart routing and multi-layer governance form the core of the modern fraud stack. Merchants who adopt this playbook reduce fraud, increase revenue and earn the trust of acquirers and regulators alike.

Conclusion:

By 2026, one truth has become impossible to ignore: the most damaging forms of travel fraud do not begin at the payment layer; they begin with identity. Fraudsters no longer rely solely on compromised card numbers. They build hybrid identities, manipulate travel documentation, exploit gaps in cross-border KYC standards, and move value through loyalty programmes, vouchers and complex multi-leg itineraries long before a transaction is disputed.

European regulators increasingly frame payment security around this same principle. The European Commission’s evolving PSD3/PSR framework places stronger emphasis on identity integrity, behavioural monitoring and cross-PSP data sharing, recognising that fraud prevention must start before a payment is authorised and continue after it is settled.¹ Likewise, INTERPOL and Europol repeatedly warn that synthetic identities and forged digital documents are now key enablers of aviation and online fraud, not outdated card-skimming tactics.

For airlines, OTAs and travel PSPs, this shift has profound implications:

- Fraud prevention becomes an identity discipline, not just a payments discipline

- Behavioural analytics and PNR-integrated intelligence become mandatory, not “advanced”

- Tokenisation, smart routing and risk-based SCA become revenue tools, not compliance hurdles

- Collaboration with IATA/ARC/BSP and PSPs becomes foundational, not optional

When viewed through this lens, travel fraud is no longer a scattered set of attacks; it is a connected ecosystem that thrives when identity controls, booking flows, operational checks, and payment routing operate in isolation.

The merchants that win in 2026 will be those that unify these layers into a single fraud strategy:

identity → behavioural → transactional → operational → post-travel.

This is the architecture that reduces fraud losses, protects loyalty value, improves cross-border approvals and strengthens acquirer confidence.

Ultimately, fraud at 35,000 feet is not a payments problem at all. It is an identity problem, and travel merchants who treat it as such will be the ones that remain bankable, compliant and competitive in the years ahead.

FAQs

1. What is ticketing fraud in the travel industry?

Ticketing fraud refers to airline or OTA bookings made using stolen cards, synthetic identities, or fraudulent intermediary agents. The transaction appears legitimate during booking and travel, but is later disputed by the cardholder, resulting in chargebacks or Agency Debit Memos (ADMs). Under EU consumer protection rules, merchants are liable for unauthorised payments unless strong customer authentication can be validated. In 2026, ticketing fraud increasingly involves synthetic IDs paired with compromised cards, making early identity screening essential for high-risk travel merchants.

2. Why is travel considered a top-three fraud target globally?

Travel is uniquely attractive to fraudsters because of high-value CNP bookings, international customer profiles, weak cross-border identity controls, and fast-moving itineraries.

Fraudsters can exploit agents, vouchers, loyalty accounts and multi-leg routes with minimal friction. Regulators such as the ECB highlight that over 80% of card fraud value in Europe originates from CNP transactions, making digital travel a prime target due to its heavy online booking volume.

3. What is synthetic identity fraud in travel payments?

Synthetic identity fraud involves constructing a persona using a mixture of real and fabricated information, then using that identity to create travel accounts, collect loyalty points, or book tickets with stolen cards. Europol reports a sharp rise in digitally manipulated IDs and hybrid profiles. In the travel sector, synthetic identities allow fraudsters to bypass account creation checks, exploit promotions, and “launder” ticket value over multi-leg routes before triggering disputes.

4. Why do fake OTAs and fraudulent travel agents cause so much financial damage?

Fraudulent travel agents, often operating through WhatsApp, Instagram, or disposable websites, route bookings through stolen cards while reselling the ticket to genuine travellers. The airline or OTA fulfils the flight, but the fraud loss appears weeks later as a chargeback or ADM. INTERPOL’s global airline fraud operations show that thousands of fraudulent tickets annually originate from such illicit intermediaries, making agent vetting essential for PSPs and acquirers.

5. How can airlines detect synthetic identities at account creation?

Airlines and OTAs can combine document verification (aligned with ICAO standards), device fingerprinting, behavioural signals and email/phone intelligence to detect synthetic profiles. High-risk indicators include new accounts making high-value bookings, mismatched device behaviour, or identity fragments inconsistent with PNR data. Identity-first screening is one of the most effective defences for reducing travel fraud in 2026.

6. Does 3DS2 help reduce airline payment fraud?

Yes, but only when used intelligently. The European Banking Authority emphasises that SCA should be applied through risk-based logic. Blanket 3DS challenges can increase abandonment and still allow synthetic identity fraud. Effective use involves applying 3DS2 to risky routes, mismatched issuer–merchant locations, and high-value itineraries, while allowing exemptions for trusted customers and low-risk corridors.

7. How does tokenisation improve travel payment security?

Tokenisation replaces raw card details with secure network tokens, reducing the risk of card compromise and improving cross-border approval rates. It protects stored credentials, loyalty-linked payments and wallet-based redemptions, all of which are common entry points for account takeover. The European Commission recognises tokenisation as a key component of modernised payment security under PSD3/PSR.

8. What behavioural indicators help detect travel fraud?

Behavioural analytics monitors patterns such as typing cadence, navigation flow, scroll behaviour and device handling to distinguish genuine customers from synthetic or automated activity. These signals support Strong Customer Authentication’s “inherence” factor under EU rules, making them highly relevant for detecting travel fraud that originates through bots, remote-access tools or credential-stuffing attacks.

9. How does PNR data contribute to fraud prevention?

Passenger Name Record (PNR) data contains itinerary, timing, route and booking details that can expose anomalies not visible in payment data alone. When combined with payment-risk engines, PNR-linked AI models can identify unusual multi-leg patterns, mismatched passenger information or inconsistent booking behaviour. EU PNR regulations emphasise the importance of structured data and cross-checking, principles that travel merchants can safely apply (within GDPR limits) to reduce fraud.

10. Why do loyalty programmes attract so much fraud?

Loyalty accounts often lack strong identity verification and hold valuable assets such as miles, vouchers or upgrade credits. Fraudsters use synthetic profiles or account takeover to accumulate points and redeem them for flights or sell them externally. Because loyalty data often lives outside the core payments infrastructure, it becomes a blind spot unless integrated into a unified fraud stack.

11. How can travel merchants reduce false declines in cross-border payments?

False declines can be reduced through smart routing, tokenisation, issuer-preferred currency presentation and risk-based SCA. The Council of the European Union’s 2025 payment framework stresses the need for enhanced PSP coordination to reduce unnecessary cross-border declines. Travel merchants that optimise routing and authentication typically gain higher approvals and lower dispute rates simultaneously.

12. What role does collaboration play in preventing travel fraud?

Collaboration is critical. IATA and ARC monitor agency behaviour; GDS networks share PNR anomalies; PSPs and acquirers exchange BIN-level and issuer-level fraud alerts. Under Europe’s upcoming payments reforms, PSPs will be required to share more fraud-related information across borders, strengthening detection and reducing siloed risk across global travel flows.

13. What do Payment Mentors recommend for travel merchants in 2026?

Travel merchants should adopt a unified fraud strategy that combines identity intelligence, behavioural analytics, tokenisation, multi-acquirer routing, and region-specific risk controls. Fraud teams must work closely with operations, payments, loyalty and compliance to meet the expectations of regulators, airlines and acquirers. Ultimately, merchants that treat fraud as an identity-first discipline will maintain the strongest approval rates, the lowest ADM exposure and the highest acquirer confidence.