In 2026, the commercial success of airlines and online travel agencies (OTAs) hinges as much on their payment infrastructure as on their route network. With cross-border bookings surging post-pandemic, FX exposure and long settlement cycles have become critical cost centres that directly erode margins. As global travel recovers, the ability to optimise acquiring, settle in the right currencies, and reduce conversion slippage is no longer optional; it’s a strategic imperative.

Consider the shifting travel landscape: airline revenues are rebounding strongly, with major carriers raising their 2024-2025 profit outlook as passenger demand hits record highs. Reuters Yet, behind every lucrative booking lies a complex web of cross-border payment risk. Many OTAs still route payments through a limited number of acquiring accounts, triggering conversions across multiple currency ‘touch-points’ and absorbing substantial FX cost. This is especially true for transactions in emerging markets, where local currencies fluctuate rapidly and the settlement exposure of days, or even weeks, can eat away at profitability.

Meanwhile, instant payment rails are proliferating in key travel-origin markets. For example, Brazil’s Pix system is not only expanding within domestic commerce but also bridging cross-border travel payments. PagBrasil’s International Pix initiative enables Brazilian tourists to pay in their local currency while abroad, helping merchants avoid traditional card FX fees. With Pix’s transaction volume climbing, EBANX projects nearly 8 billion monthly payments; this rail is becoming a viable FX-optimised channel for travel merchants.

Yet the opportunity is not confined to Latin America. Across Europe, regulators are doubling down on FX transparency via new payment services rules, compelling acquirers and merchants to reveal real-time conversion costs and reduce hidden markups. European Court of Auditors. When implemented intelligently, a multi-acquirer, multi-currency strategy doesn’t just save costs, it accelerates settlement, improves liquidity, and enhances customer experience by settling in currencies native to travellers.

- The Travel Payments Problem: High FX Exposure & Slow Settlement

- Multi-Acquirer Architecture: Why Regional Routing Transforms Settlement Speed

- FX & Dynamic Currency Conversion (DCC): Cost, Transparency & Compliance

- Settlement Frameworks: SEPA Instant, PIX, and Cross-Border EMIs

- Treasury Optimisation: How PSPs Automate FX Conversion and Reduce Delays

- Compliance & Regulatory Oversight: PSD3, EBA & Global FX Requirements

- 2026 Outlook – The Rise of Tokenised Multi-Currency Settlement

- Conclusion

- FAQs

The Travel Payments Problem: High FX Exposure & Slow Settlement

Travel merchants, airlines and OTAs face structural payment cost challenges far beyond typical retail. One of the most significant is FX slippage: customers often pay in local or domestic currencies, but the merchant’s treasury receives funds in a handful of major currencies. When a Brazilian tourist books a U.S. airline ticket, for example, the purchase may be authorised in USD, then converted by the acquirer into EUR or BRL depending on the merchant’s setup. Each conversion “touch” eats into the margin, especially when rates fluctuate aggressively.

Compounding this, the settlement cycle is long and risky. Many airline acquirers and PSPs adopt delayed settlement models, often T+3 to T+14, so payment risk can be reviewed, especially for cross-border bookings. During this window, currency markets may move against the merchant, creating latent FX mismatches. Meanwhile, volatility spikes (for example, around geopolitical events) expose travel merchants in real time but only settle later, locking in unfavourable rates.

At the same time, refunds, cancellations, and chargebacks add another layer of complexity. Travel is uniquely exposed to involuntary refund risk due to flight cancellations, schedule changes, and customer no-shows. These refund events often originate in entirely different currencies, triggering reverse FX conversions at loss-making rates. Longer settlement timelines further delay the treasury’s ability to net these flows efficiently, resulting in either reserve increases or cash-flow strain.

The consequence is stark: for airlines and OTAs operating at scale, FX and settlement inefficiencies can erode 1-3% of gross booking revenue, a margin hit that rivals fuel or marketing costs. Without optimised acquiring routing and smarter FX management, travel companies risk handing away profit, even as volumes recover.

Merchant Takeaway:

Without a deliberate cross-border payment strategy, one that minimises FX conversion touch points and accelerates settlement, airlines and OTAs are implicitly subsidising foreign-exchange risk. The opportunity lies in restructuring, acquiring, and treasury flows to preserve margin and improve liquidity.

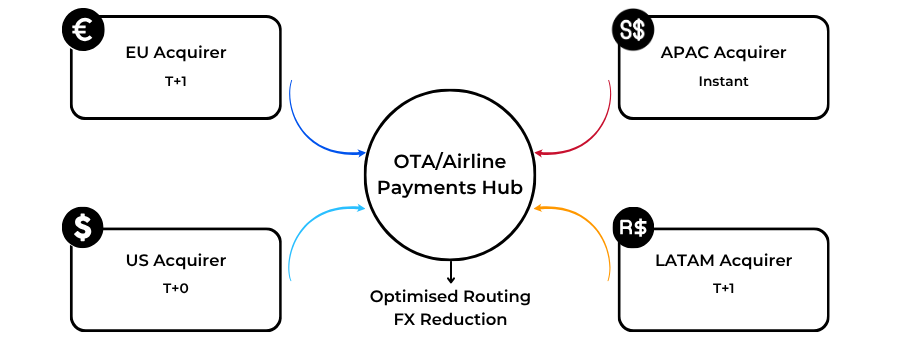

Multi-Acquirer Architecture: Why Regional Routing Transforms Settlement Speed

Airlines and OTAs operate in one of the most geographically fragmented payment ecosystems in the world. Cards remain dominant, but the routing of those card transactions determines how fast funds arrive, how many FX conversions occur, and which entity bears the risk. This is why, by 2026, travel merchants are shifting aggressively toward multi-acquirer architectures, a model where transactions are dynamically routed to the optimal acquirer based on geography, card type, currency, or regulatory requirements.

Why One Acquirer No Longer Works in Cross-Border Travel

Historically, large airlines relied on a single global acquiring partner. While operationally simple, this approach created four persistent issues:

- Slow Settlement in Cross-Border Markets

When a European acquirer handles a LATAM-origin booking or a Southeast Asian card, settlement can stretch from T+5 to T+14. Local acquirers, by contrast, settle in T+1 or T+2 because schemes classify the transaction as domestic.

- Unnecessary FX Conversions

A US-based acquirer processing a Mexican peso (MXN) transaction usually converts MXN → USD → EUR (or the merchant’s treasury currency).

Every hop creates slippage. With a regional acquirer, settlement occurs in MXN first, giving the merchant the option to convert at a mid-m arket or contracted rate.

- Higher Scheme Fees for Cross-Border Acquiring

Visa and Mastercard apply additional cross-border assessment fees when issuing and acquiring are in different regions. Routing region-to-region instantly reduces cost, even before FX considerations.

- Harder Risk Control

A single acquirer sees the world through one risk lens. Regional acquirers, however, understand local fraud behaviour (e.g., Brazil’s high card-not-present chargeback rates; India’s RBI-driven SCA requirements).

How Multi-Acquirer Routing Works in Practice

By 2026, OTAs commonly use:

- Intelligent Gateway Routing: The PSP or gateway decides, in milliseconds, whether a Japanese issuer card should route to a Singapore acquirer or a European one, prioritising cost, approval rate, and settlement speed.

- Local-to-Local Pairing: A Brazilian customer using a domestic credit card gets routed to a Brazil-registered acquirer, preventing unnecessary FX conversion and reducing declines.

- Fallback & Redundancy Routing: If Acquirer A has a downtime event, routing automatically shifts to Acquirer B without impacting the conversion rate.

- Currency-Sensitive Logic: High-volatility currencies (ZAR, COP, MXN) are routed where settlement is fastest and where the merchant holds or hedges in those currencies.

Impact on Settlement Time & Cash Flow

The shift to multi-acquirer routing typically reduces settlement windows from T+7 to T+2 for cross-border flows.

For airlines operating with thin margins and high operational costs, this time reduction directly improves:

- Liquidity forecasting

- FX conversion strategy

- Refund provisioning

- Exposure during volatile rate swings

In a sector that often works on pre-payments and deferred service delivery, faster settlement equals lower financial risk.

FX & Dynamic Currency Conversion (DCC): Cost, Transparency & Compliance

Cross-border travel payments are inherently exposed to foreign exchange friction. Airlines and OTAs process millions of transactions per day across dozens of issuing regions, and each payment pathway embeds multiple FX variables: issuer currency, cardholder billing currency, settlement currency, acquirer currency, and the merchant’s treasury currency. By 2026, regulators and card networks are tightening rules around FX transparency, especially for Dynamic Currency Conversion (DCC), to protect consumers and maintain fairness in cross-border transactions.

Understanding FX Leakage in Travel Payments

FX loss isn’t caused by a single event; it accumulates across four layers:

- Issuer FX: When customers pay in their local currency, the issuing bank sets the rate. Rates can deviate significantly from mid-market pricing.

- Acquirer FX: When acquirers settle in a different currency (e.g., accepting MXN but settling in USD), merchants face spread + markup.

- Scheme FX: Visa and Mastercard have their own daily FX tables, updated per scheme rules.

- Merchant Treasury FX: Final conversion into operating currency (USD, EUR, GBP) is where many airlines incur avoidable slippage if they convert during periods of market volatility.

Each stage introduces basis-point erosion, often unnoticed until aggregated at scale across 12–18 months of settlement data.

Where DCC Fits Into the FX Equation

Dynamic Currency Conversion allows the customer to pay in their home currency at the point of sale, with the rate set by the merchant’s acquirer or PSP instead of the issuer.

In the travel sector, DCC is widely deployed in:

- Online card checkout for OTA bookings

- In-flight POS terminals

- Kiosks and airport desks

- Hospitality bundles connected to airline loyalty programmes

While DCC can increase revenue through shared margins, it has become a compliance-sensitive product, particularly in the EU and UK.

Regulatory Landscape: Transparency Is No Longer Optional

Under the EU Cross-Border Payments Regulation (CBPR2) and Payment Services Directive amendments (PSD2/PSD3):

- Merchants must disclose the FX markup relative to the latest ECB exchange rate.

- Acquirers must report conversion rules clearly and maintain audit trails for all FX decisions.

(Reference: European Commission – Cross-Border Payments Regulation)

Similarly, the UK Payment Systems Regulator (PSR) has increased scrutiny of FX transparency for international card payments, pushing PSPs to standardise markup disclosure and reduce opaque pricing models.

(Reference: UK Payment Systems Regulator – FX Transparency & Surcharging Guidance 2024)

Compliance Pitfalls for Airlines & OTAs

Travel merchants frequently fail to meet FX and DCC standards due to:

- Outdated checkout flows that display only the converted total, not the markup

- PSPs applying variable spreads without disclosure

- Lack of audit documentation during regulatory review

- Use of “pre-selected” DCC options, which regulators increasingly consider non-compliant

These issues elevate risk for airlines and OTAs because non-transparent conversion is treated as consumer detriment, leading to fines and acquirer remediation programmes.

Best Practices for FX & DCC Compliance (2026 Standard)

To ensure compliant and optimised FX operations:

- Display markup vs ECB/BoE reference rates

Mandatory in the EU; increasingly expected globally. - Provide a clear opt-in/opt-out choice for DCC

Opt-out may soon become the regulatory default in multiple markets. - Use PSPs with live FX feeds

Real-time pricing lowers slippage and eliminates stale-rate disputes. - Segment FX strategy by route

LATAM, Africa and APAC require localised FX plans due to high volatility. - Audit FX decisions quarterly

Regulators are requesting evidence, not narratives, during audits.

Merchant Takeaway: Airlines and OTAs must treat FX and DCC as regulated financial products, not mere checkout add-ons. Transparent FX pricing reduces compliance risk, protects margins, and strengthens customer trust in cross-border booking flows.

Settlement Frameworks: SEPA Instant, PIX, and Cross-Border EMIs

For airlines and OTAs, the most persistent financial bottleneck is settlement speed. Customers book instantly, but funds often take 3-10 days to reach merchant treasury accounts, introducing FX exposure, cash-flow strain, and reconciliation delays. By 2026, three settlement infrastructures are reshaping global travel payments: SEPA Instant (EU), PIX (Brazil), and cross-border Electronic Money Institutions (EMIs).

Each offers faster settlement, lower FX drag, and greater transparency compared to traditional card acquiring.

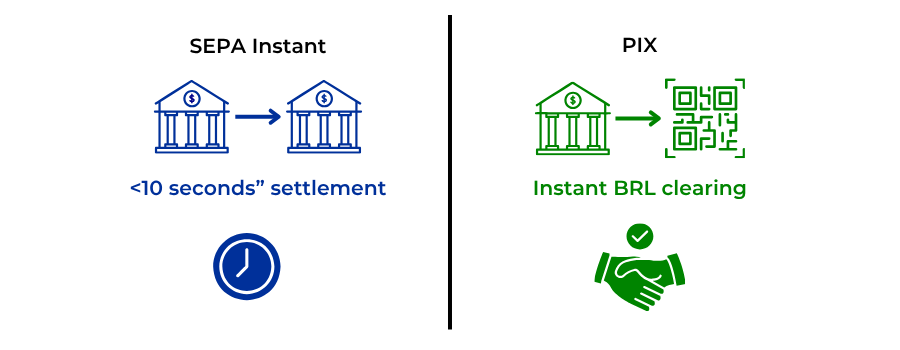

SEPA Instant: Europe’s 10-Second Settlement Standard

SEPA Instant Credit Transfer (SCT Inst) allows EUR-denominated transfers to settle in under 10 seconds across the EU and EEA. As of 2024, SEPA Instant covers more than 2,300 payment service providers and is transitioning toward mandatory acceptance under the upcoming EU PSD3 legislative frameworks.

Why SEPA Instant matters for airlines & OTAs:

- Instant EUR settlement reduces multi-day holding periods typical of card acquirers.

- Lower FX exposure because EUR inflows reach treasury accounts before market movements.

- High reliability: 24/7/365 processing, unlike card settlement cut-off windows.

- Strong chargeback immunity: credit transfers have no Visa/Mastercard-style chargeback mechanism.

Use case for travel: European customers paying for international flights can use open-banking-powered A2A payments that settle instantly through SEPA Instant, enabling same-day balance sheet recognition for airlines.

Official reference:

European Payments Council – SEPA Instant Rulebook

PIX: Brazil’s Real-Time Payment Engine Transforming LATAM Travel

Launched by Banco Central do Brasil, PIX has become the fastest-adopted instant payments system in the world, processing billions of monthly transactions. It enables real-time settlement between consumers and businesses, including cross-border travel merchants operating locally.

Why PIX is strategically important for airlines & OTAs:

- Immediate settlement of BRL funds: reducing dependency on cross-border acquiring.

- Significantly lower fees: compared to card payments in Brazil.

- Reduced refund overhead: refunds are instant and trackable.

- Increased approval rates: PIX is not subject to issuer decline logic.

LATAM relevance: Brazil represents one of the largest outbound travel markets in the region. Airlines localising payments with PIX often see conversion increases of 20-40% over card-only checkout flows.

Official reference:

Banco Central do Brasil – PIX Regulation

Cross-Border EMIs: The New Treasury Rails for OTAs & Airlines

Electronic Money Institutions (EMIs) have expanded rapidly across the UK, EU, Singapore, Hong Kong, and UAE, offering multi-currency accounts, wallet-based settlement, and alternative clearing channels.

Unlike banks and traditional acquirers, EMIs specialise in:

- Fast multi-currency settlement (T+0 / T+1)

- Wallet-to-wallet cross-border movement

- On-demand FX conversion at interbank or mid-market pricing

- Segregated accounts for reconciliation clarity

- Direct integration with open banking APIs

EMIs are particularly valuable for OTAs with high transaction volumes and numerous supplier payouts (hotels, transfer operators, regional carriers). By routing fund flows through an EMI, merchants can avoid unnecessary intermediate FX steps, consolidating liquidity across EUR, GBP, USD, AED, SGD, and more.

Official references: FCA Register – E-Money Institutions

Why These Settlement Frameworks Matter for 2026

Across Europe, LATAM, Asia, and MENA, the trend is unmistakable:

- Card settlement delays are no longer acceptable in a high-volume, thin-margin sector.

- A2A and wallet settlement rails offer predictable FX windows, crucial for volatile currencies.

- Regulators encourage transparent, instant, low-cost transaction frameworks, favouring A2A and EMI models over card schemes.

- Suppliers demand faster pay-outs, especially regional hotels and transport partners that rely heavily on OTAs.

In short, SEPA Instant, PIX, and EMI wallets are becoming the foundation of next-generation travel treasury architecture.

Treasury Optimisation: How PSPs Automate FX Conversion and Reduce Delays

In the travel sector, treasury is often the silent victim of payment design inefficiency. Airlines and OTAs operate with global customer bases, regional suppliers, and multi-currency revenue streams, yet most treasury teams still rely on manual FX conversion, batch reconciliation, and end-of-cycle settlement practices inherited from legacy acquiring models.

By 2026, leading PSPs and acquirers are introducing automated treasury optimisation tools to eliminate FX slippage, reduce settlement lag, and synchronise global cash flow.

Why Treasury Struggles in Cross-Border Travel

Treasury teams face four structural challenges:

- Multi-day settlement windows

Global acquiring often settles in T+5 to T+14, creating FX exposure during volatile periods. - Forced bank-driven conversions

When acquirers settle in major currencies (USD/EUR/GBP), treasuries lose control over the FX rate applied. - High refund volatility

Airlines experience spikes in refund volume during weather events, route cancellations, or operational disruptions. - Supplier payment complexity

OTAs and airlines must pay hotels, regional carriers, tour operators, and GDS suppliers, each in different currencies.

This complexity creates an environment where cash is constantly moving across currencies, time zones, and banking partners.

How PSPs Are Automating FX Conversion in 2026

Modern PSPs are introducing FX automation engines, powered by real-time pricing, netting algorithms, and treasury APIs. These tools transform FX risk management from a reactive to a predictive approach.

1. Real-Time FX Exposure Dashboards

PSPs now provide dashboards showing:

- Currency inflows by region

- Exposure windows

- Predicted settlement timing

- Volatility alerts

- Recommended conversion moments

These dashboards leverage live market data from regulated FX venues.

Reference: European Securities and Markets Authority (ESMA) Market Data Quality Framework

2. Smart Auto-Conversion Rules

Airlines can set logic such as:

- Convert BRL to USD only when volatility < X%.

- Hold MXN until settlement day minus one.

- Convert only when the interbank spread falls below Y basis points.

PSPs apply rules programmatically, ensuring consistency and compliance.

3. Split Settlement Logic

Instead of settling 100% of a booking in one currency, PSPs can settle:

- 40% in local booking currency (for supplier payouts)

- 60% in core treasury currency (for cash management)

This eliminates unnecessary round-trip conversions and reduces slippage.

4. Supplier Payout Match

OTAs pay thousands of suppliers. PSPs now automate:

- Matching inflow currency with supplier payout currency

- Pooling liquidity regionally

- Auto-netting currency balances daily

This dramatically reduces excess FX conversion.

Reference: European Banking Authority – Payment Services Guidelines

5. Virtual Accounts and Multi-Currency Wallets

EMIs in the UK, EU, Singapore, and Hong Kong offer virtual IBANs where airlines and OTAs can:

- Hold 30-150 currencies

- Convert at interbank pricing

- Settle instantly across wallets

- Net supplier invoices across currencies

Wallets give treasurers unprecedented control over conversion timing.

Reference: FCA Register – Authorised Electronic Money Institutions

How Automation Reduces Delays and Improves Liquidity

Before automation: FX conversion happens post-settlement, often based on acquirer-driven pricing.

After automation: Travel merchants convert before settlement clears or based on ideal market conditions.

This improves:

- Liquidity forecasting

- Cash allocation

- Refund funding

- Supplier payout precision

- FX risk exposure windows

For airlines with thin margins, these improvements can recover 0.5-2.5% of gross booking value, depending on route volatility and currency mix.

By 2026, treasury optimisation is no longer an operational enhancement; it’s a competitive necessity. PSPs that offer real-time FX automation, split settlement, and multi-currency wallets enable airlines and OTAs to regain control over margins and reduce exposure to unpredictable FX cycles.

Compliance & Regulatory Oversight: PSD3, EBA & Global FX Requirements

In 2026, compliance is no longer a back-office checkbox for airlines and OTAs; it is a strategic payment architecture layer. Cross-border acquiring in travel is under intense regulatory scrutiny, given its complexity, currency flows and consumer-protection footprint. Merchants must now structure acquiring and settlement flows with full awareness of the evolving regulatory regime: the Payment Services Directive 3 (PSD3) in the EU, the Payment Systems Regulator (PSR) in the UK, and equivalent mandates in key travel-origination countries across Asia and LATAM.

EU / PSD3 & PSR: Harmonised Oversight for Cross-Border Flows

Under PSD3, the Payment Services Regulation (PSR) (EU) will expand the scope of recurring payment standards, multi-currency transaction governance and FX transparency obligations. PSD3 seeks to:

- Mandate uniformly the disclosure of currency conversion mark-ups and settlement delays.

- Extend strong customer authentication (SCA) and fraud-monitoring standards to card-, wallet- and A2A-based acquiring.

- Require full audit trails of FX conversions, routing logic and settlement timing.

For travel merchants, this means that routing cross-border payments via stateless acquirers without documented local compliance may trigger regulatory risk, elevated scrutiny or sharper reserve requirements.

In the UK, the PSR’s 2024 market review found dramatic increases in cross-border interchange fees and questioned how acquiring models were passing costs to merchants. psr.org.uk The PSR emphasises transparency and may extend oversight into travel-specific flows, particularly where high-volatility currencies and long-settlement durations exist.

Global Standards Affecting Travel Acquiring

Beyond Europe, several regulatory trends affect airlines and OTAs:

- The Cross‑Border Payments Regulation 2 (CBPR2) requires card-based international payments to disclose FX mark-ups relative to the European Central Bank (ECB) rate.

- Licencing and operational rules for electronic money institutions (EMIs) in travel-relevant jurisdictions now carry increased capital, transparency and data-sharing obligations under PSD3-style frameworks.

Why Travel Merchants Are of Special Interest to Regulators

Travel payments differ from standard retail because they involve:

- Higher average transaction values

- Cross-border card usage

- High refund and chargeback exposure due to cancellations

- Chain settlements (customers → OTA/airline → supplier)

Regulators view these as higher-risk flows, meaning non-compliance can lead not just to fines, but to acquirer monitoring, MID downgrades or loss of settlement preferential terms.

Compliance Implications for FX & Acquiring Models

For airlines and OTAs, key compliance implications include:

- Documenting full routing and settlement logic (which acquirer, which MID, which currency, what timeframe).

- Keeping FX conversion logs for audit and regulatory review, especially if using multi-MID and multi-currency wallet models.

- Verifying that local acquiring partners are licensed under the relevant regime (especially important in LATAM, Africa and APAC where local shells may operate).

- Monitoring emerging regulation in major origin markets (e.g., Brazil, India) to anticipate changes to cross-border settlement and local acquiring mandates.

Compliance in cross-border acquiring is no longer optional; it is integral to maintaining a healthy margin. Airlines and OTAs that proactively align with PSD3, PSR, CBPR2 and regional FX disclosure regimes will not only reduce the cost of funds but will qualify for better acquirer terms, lower reserves and faster settlement.

2026 Outlook – The Rise of Tokenised Multi-Currency Settlement

By 2026, the global travel industry will be moving beyond conventional card-based settlement and into a new generation of tokenised, multi-currency treasury rails. Airlines and OTAs, long constrained by slow settlement cycles and unpredictable FX markets, are adopting digital settlement models powered by blockchain-based tokens, stablecoins, and PSP-issued digital liquidity instruments.

The goal is not to replace traditional currencies, but to settle faster, convert smarter, and reduce FX drag.

1. Tokenised Settlement: A New Layer Above Traditional FX

Tokenised settlement allows PSPs and treasuries to convert and move value using a token representation of fiat currency (USD, EUR, GBP, BRL, AED, SGD, etc.). These tokens are:

- Backed 1:1 by regulated institutions

- Settled on permissioned or semi-permissioned chains

- Designed for instant clearing

- Fully auditable for regulatory oversight

Unlike cryptocurrencies, these are regulated digital settlement instruments, closely aligned with stablecoin models such as USDC, EURC and SGD-denominated stablecoins being piloted in Asia.

Reference:

Circle (2024–2025) – Stablecoin (USDC/EURC) Compliance and Settlement Reports

2. Why Travel Merchants Care: Faster Settlement, Lower FX Cost

Tokenised settlement models address the three structural weaknesses of cross-border acquiring:

a. Settlement moves from days → minutes

Through PSP-to-PSP token transfers, airlines can receive liquidity within minutes, not days.

This directly reduces FX exposure windows.

b. Cross-currency netting becomes instantaneous

Tokens allow the treasury to convert, hold and net value across currencies without requiring immediate conversion to fiat. This helps avoid “forced conversion” at acquirer-driven spreads.

c. Supplier payouts become cheaper and faster

OTAs can pay hotels, regional carriers and tour operators in tokenised currency equivalents, settling via EMI or digital-asset-regulated channels at near-zero delay.

Reference:

Monetary Authority of Singapore – Project Guardian (Tokenised Settlement Trials, 2024–2025)

3. Stablecoin Settlement Corridors for Travel

Several PSPs and EMIs are piloting stablecoin-based settlement corridors connecting:

- EU → Singapore

- US → LATAM

- Middle East → Asia

- UK → Africa

These corridors reduce FX spread, avoid SWIFT delays, and offer instant settlement. Travel is an early beneficiary because it operates high-volume, thin-margin, cross-border revenue streams.

Reference: Ripple / UAE & Singapore (2024) – Tokenised Cross-Border Payments & FX Efficiency

4. AI-Driven Treasury Routing for Tokenised FX

By 2026, AI will be integrated into PSP and treasury systems to:

- Predict FX volatility

- Recommend conversion timing between tokenised currencies

- Route settlement to the cheapest corridor

- Forecast liquidity gaps by region

This ensures FX conversion is no longer reactive; it becomes predictive and automated.

Reference:

Bank for International Settlements (BIS) – AI & Tokenised Payments (2024–2025 reports)

5. Regulatory Acceptance: From Pilot to Production

Regulators from the EU, UK, Singapore, and UAE are beginning to formalise rules around tokenised settlement vehicles, focusing on:

- Segregation of reserves

- Auditability

- Consumer transparency

- AML / KYC obligations

- Cross-border reporting standards

PSD3 and UK PSR both acknowledge tokenisation as a future pathway for multi-currency clearing, provided FIAT on/off-ramps comply with AMLD6 and local EMI regulations.

Reference:

European Commission – PSD3 Package (Digital Money & Settlement Innovation Context)

6. Strategic Impact for Airlines & OTAs

Tokenised settlement offers measurable commercial benefits:

- Cuts FX loss by 20–60 bps by reducing timing mismatch

- Compresses settlement windows from T+5 to T+0/T+1

- Improves supplier payouts through instant cross-wallet transfers

- Supports multi-currency holding for strategic FX timing

- Eliminates approval dependency on issuer/acquirer rails

Airlines and OTAs that adopt tokenised treasury infrastructure will gain a multi-year competitive advantage in liquidity, cost efficiency, and global payment flexibility.

Tokenised settlement isn’t a speculative trend; it is the next infrastructure layer for global travel commerce. By 2026, the merchants that integrate multi-currency token rails, stablecoin corridors and automated FX engines will significantly outperform competitors relying solely on traditional cross-border acquiring.

Conclusion

The global travel sector has always been the ultimate stress test for cross-border payments, high-value transactions, volatile routes, dozens of currencies, and geographically dispersed customers. But by 2026, airlines and OTAs will no longer be passive participants in the settlement process. A new generation of multi-acquirer routing, instant payment rails, automated FX engines, and tokenised treasury flows is transforming what was once a cost centre into a controllable, optimisable profit lever.

Across Europe, PSD3 is enforcing unprecedented transparency in FX markups and settlement practices. In LATAM, PIX’s instant settlement architecture is becoming indispensable for travel merchants acquiring in Brazil. In APAC, regulators like MAS and RBI are formalising FX disclosure rules and encouraging digital settlement pilots. In the Middle East and global wholesale corridors, tokenised settlement platforms such as mBridge are challenging the dominance of card-based clearing for high-volume cross-border payments.

The message is clear: cross-border acquiring is shifting from static to strategic. Airlines and OTAs that continue to rely on single-region acquirers, stateless routing, or forced bank-driven FX conversions will continue to lose margin and liquidity, regardless of booking volume or flight demand improvements. Meanwhile, merchants adopting regional acquiring, multi-currency wallets, automated conversion logic, and real-time settlement options are clawing back 0.6–4% of revenue that was historically lost to FX, delays, and inefficiencies.

A modern travel treasury must operate like a global liquidity engine, not a payment inbox. By restructuring, acquiring infrastructures, adapting to regulatory reform and moving toward tokenised settlement, airlines and OTAs can stabilise margins, accelerate cash flow and protect against volatility in an increasingly unpredictable international travel market.

Cross-border acquiring is now a commercial strategy, not a technical process. In 2026 and beyond, margin growth in travel will come from optimising where and how payments settle, not just how many bookings are made.

FAQs

1. Why is cross-border acquiring more complex for airlines and OTAs than for other sectors?

Airlines and OTAs operate in one of the most cross-border-heavy ecosystems worldwide. Customers purchase in over 100 currencies, but merchants settle in only a few base currencies, creating structural FX exposure. Travel also carries long fulfilment windows, high refund rates, and multi-party supply chains, including customers, carriers, hotels, and GDS providers, which amplify settlement delays. Unlike e-commerce, travel merchants face ongoing FX risk from booking to departure, making cross-border acquiring a core margin driver rather than a back-office function.

2. How do airlines lose money through FX conversion during cross-border bookings?

Most losses occur during settlement: the booking currency is often different from the settlement currency, and acquirers apply FX rates days after authorisation. If FX markets move unfavourably during this window, the airline absorbs the loss. Additional leakage occurs through issuer FX, scheme-level conversion, and forced acquirer-driven conversions. Airlines operating without multi-currency wallets or automated FX timing can lose 0.6-3% of revenue depending on route volatility.

3. What is the benefit of using multiple acquirers instead of a single global acquirer?

Multi-acquirer routing allows airlines and OTAs to process transactions through regional acquirers that match the cardholder’s issuing country or currency. This reduces cross-border interchange fees, avoids unnecessary FX conversions, increases approval rates, and shortens settlement timelines. Regional routing can reduce settlement windows from T+7 to T+2 or faster. A single global acquirer cannot optimise approval rates or settlement speed across diverse regions such as LATAM, APAC, EU, and the Middle East.

4. How does Dynamic Currency Conversion (DCC) affect travel merchants?

DCC lets customers pay in their home currency, with the rate set by the merchant’s acquirer. While it can create incremental revenue through margin sharing, it is tightly regulated. Under PSD3 and EU FX transparency laws, merchants must disclose the FX markup versus the ECB reference rate at checkout. Poor DCC implementation can result in compliance breaches, consumer disputes, and acquirer penalties, making transparent pricing essential for airlines and OTAs.

5. What role do SEPA Instant and PIX play in accelerating settlement?

SEPA Instant enables euro-denominated transfers that settle in under 10 seconds across the EU, while Brazil’s PIX delivers real-time settlement for BRL payments at near-zero cost. When integrated into airline and OTA payment flows, these rails reduce dependency on card settlement cycles and minimise FX exposure windows. Using PIX for Brazil-origin travel bookings can improve conversion by 20-40% and provide instant BRL liquidity to treasury teams.

6. How do EMIs help OTAs and airlines reduce FX exposure?

Electronic Money Institutions (EMIs) provide multi-currency wallets, virtual IBANs, and real-time settlement solutions that allow treasurers to hold, convert, and net currencies on demand. Instead of being forced into acquirer-led FX conversion, airlines can choose optimal conversion timings using interbank or contracted rates. EMIs also accelerate supplier payouts and provide clearer reconciliation paths than traditional cross-border bank transfers.

7. What treasury automation tools do PSPs offer travel merchants in 2026?

Modern PSPs offer automated FX engines, volatility alerts, split settlement configurations, and predictive exposure dashboards. These tools analyse inflows by currency, route volatility, and refund patterns to determine the ideal conversion moment. Airlines can set rules such as: “Hold BRL until volatility drops below 1.5%,” or “Convert MXN only when spread <X basis points.” Automation eliminates manual FX timing errors and reduces slippage.

8. How do tokenised settlement rails reduce FX cost?

Tokenised settlement models allow PSPs to represent fiat currencies (USD, EUR, BRL, SGD) as regulated digital tokens. These tokens settle instantly across permissioned blockchain networks. Airlines benefit through reduced FX exposure windows, cheaper cross-border transfers, and instant supplier payouts. Tokenisation also enables multi-currency netting without requiring immediate conversion to fiat, preserving margin in volatile FX periods.

9. Are stablecoins like USDC and EURC relevant for airline settlements?

Yes, when used in regulated PSP and EMI environments. Stablecoins provide fast, low-cost, auditable cross-border liquidity options that help reduce settlement delays. While airlines won’t accept customer payments directly in stablecoins, they increasingly use them for treasury routing, supplier payouts, and intra-entity liquidity movements. Regulatory frameworks in the EU, Singapore, UAE, and Hong Kong now support tokenised settlement pilots for institutional payments.

10. What are the main regulatory risks when processing multi-currency travel transactions?

PSD3, CBPR2, the UK PSR, MAS, and RBI all require transparent FX disclosures and accurate reporting of settlement timelines. Non-compliance includes failing to disclose FX markups, inaccurate DCC presentation, using unlicensed acquiring partners in restricted markets, or lacking audit trails for conversion decisions. Travel merchants face elevated scrutiny because of high-value transactions and frequent refunds.

11. How can airlines improve approval rates for cross-border card payments?

Approval rates improve when transactions are routed to local acquirers that match the cardholder’s region. Implementing multi-acquirer orchestration, network tokenisation, and SCA optimisation significantly reduces issuer friction. Airlines should also reduce unnecessary cross-border flags by configuring regional MIDs and enabling 3DS2 in high-risk markets such as LATAM and India.

12. What does Payment Mentors recommend for travel merchants in 2026?

Payment Mentors advises adopting a three-layer treasury framework:

- Local acquiring first (reduce FX and increase approvals).

- Multi-currency wallets + automated FX timing (control rate execution).

Instant and tokenised settlement rails (accelerate liquidity).

This ensures margin stability, predictable cash flow, and compliance with PSD3 and CBPR2 standards.