In 2026, volatility in global currency markets has quietly become one of the biggest profit leaks in online gaming. Every spin, bet, and payout that crosses borders now carries a hidden FX cost. While most operators obsess over bonus efficiency or conversion rates, far fewer examine the difference between a deposit authorised in euros, a payout settled in sterling, and a reserve account held in dollars. Those micro-mismatches, often measured in basis points, compound into six-figure losses when multiplied across millions of transactions each month.

The Bank for International Settlements (BIS) reports that global foreign-exchange turnover reached $9.6 trillion per day in 2025, up 28 % from 2022, reflecting sharp rate divergence between the USD, EUR, and emerging-market pairs. For high-risk merchants processing in multiple settlement currencies, this volatility translates directly into shrinking profit margins and liquidity stress. A single percentage-point swing between authorisation and clearing can erase the entire take rate on low-margin transactions such as card deposits or affiliate payouts.

Compounding the problem, many acquirers and PSPs still route cross-border flows through default settlement currencies, usually USD or EUR, triggering double conversion: first by the card network at authorisation, then by the acquirer at settlement. Each step applies a separate spread, and when combined with card-network cross-border assessments (typically 0.6-1.0 %) and post-Brexit UK↔EEA interchange uplifts, operators face an effective cost that can exceed 2 % per transaction. Because FX losses are buried inside acquirer statements rather than merchant dashboards, few treasurers quantify their daily impact.

Timing risk adds another layer. Payouts or chargeback refunds often occur days after the original deposit, meaning a 48-hour currency move can convert accounting profit into realised loss. Even well-capitalised operators rarely hedge short-term exposures; they rely instead on static PSP conversion tools that provide convenience but little control over rate source, cut-off, or liquidity depth.

Regulatory momentum is accelerating the need for better FX governance. The European Commission’s Instant Payments Regulation (2025) will make near-real-time EUR transfers mandatory, reducing timing windows but demanding continuous liquidity and transparent pricing. Meanwhile, the UK FCA’s Consumer Duty (2025) requires clearer disclosure of international payment fees, including FX mark-ups. Together, these frameworks elevate FX control from back-office optimisation to a compliance-critical function.

For high-risk iGaming operators, the message is clear: unmanaged currency exposure is no longer a cost of doing business; it is a controllable risk. The winners in 2026 will be those who treat FX like fraud or AML: measurable, monitored, and automated.

- FX Flow Mapping: Understanding Deposit vs Withdrawal Mismatches

- Mapping the Exposure – Where iGaming Loses Money on FX

- Hedging and Conversion Strategies – From Forwards to Stablecoins

- Regional Pain Points – FX Volatility in Africa, LATAM and Asia

- Bank & PSP Solutions – Multi-Currency Wallets and Payout Reconciliation

- Risk Management Checklist – Monitoring FX Exposure in Real Time

- 2026 Forecast – Smart Treasury and Automated FX Pricing

- Conclusion

- FAQs

FX Flow Mapping: Understanding Deposit vs Withdrawal Mismatches

Behind every iGaming transaction lies an intricate currency journey that few merchants ever see in full. From a player’s deposit to a final withdrawal, funds often traverse three or more conversion points, each introducing a measurable spread and timing risk. Mapping this flow is the first step to diagnosing how volatility silently erodes profitability.

1. The Deposit Leg: Authorisation Currency vs Settlement Currency

When a player deposits using a card issued in one currency but plays in another, the card network typically performs a real-time FX conversion at the authorisation stage, applying a daily Mastercard or Visa rate plus ~0.5 % spread (Mastercard Currency Conversion Rates, 2025; Visa Exchange Rates, 2025). If the acquirer later settles in a different base currency, say USD or EUR, the same transaction may be reconverted again during clearing. This double conversion produces compounding costs of 1-1.5 % per transaction.

Post-Brexit, the Payment Systems Regulator (PSR) confirmed that UK↔EEA card-not-present interchange fees rose from 0.2/0.3 % to 1.15/1.5 % for debit/credit, respectively (UK PSR Cross-Border Card Fees Report, 2024). For gaming operators, that uplift amplifies the baseline FX burden before a single wager is placed.

2. The Wallet Stage: Internal Currency Holding

Once funds enter a player’s wallet, they are often held in the platform’s functional currency, typically EUR or USD, even if the bet occurs in GBP or BRL. This internal translation creates latent FX exposure between the deposit and gameplay. Many PSP dashboards still quote balances in the operator’s settlement currency, masking mismatches between local-currency deposits and global-currency ledgers.

The Bank for International Settlements (BIS) notes that “corporates operating across multiple EM currencies face FX timing risk akin to financial institutions” (BIS Quarterly Review, June 2025). For high-risk gaming, this risk materialises each time a player wins or withdraws in a currency different from the ledger currency.

3. The Payout Leg: Settlement and Reversal Risk

Withdrawals reintroduce conversion at payout, often days later, after rates have moved. A two-day 2 % move between EUR and GBP can wipe out the entire operator margin on a single high-value player.

Chargebacks and refunds magnify the problem: card networks reimburse at the current rate, not the original transaction rate, creating a realised loss whenever currencies weaken against the merchant base. Visa Europe estimates that “FX variance on refunds adds 30-70 bps to effective dispute costs” (Visa Risk Operations Report, 2024).

4. The Reconciliation Gap

Because most acquirer reports aggregate transactions by currency after conversion, operators seldom have a line-by-line view of true FX slippage. Without ISO 20022 transaction IDs or virtual IBAN (vIBAN) structures, matching incoming and outgoing currencies requires manual work, introducing errors and audit gaps. The European Banking Authority (EBA) now encourages PSPs to include FX rate source and timestamp data in payment messages to improve transparency (EBA Opinion on Instant Payments Supervision, 2025).

Merchant Takeaway:

FX mismatches are rarely visible in day-to-day reporting but are almost always material. By mapping each currency touchpoint, from player deposit to settlement and refund, operators can pinpoint where spreads, timing lags, and chargeback FX losses accumulate. The goal is not to eliminate conversion but to control it through clear routing rules, accurate data, and trusted rate sources.

Mapping the Exposure – Where iGaming Loses Money on FX

Currency volatility hurts iGaming operators not because they speculate on FX markets, but because they sit at the centre of thousands of cross-border micro-transactions each day. Each stage, from deposit to payout and refund, carries its own loss mechanism. Understanding the origin of these costs is the foundation for designing a resilient treasury model.

1. Cross-Border and Scheme Fees: The Unseen Tax on Volume

Whenever a card is issued in one country and processed in another, the card networks levy a cross-border assessment fee, typically 0.6 – 1.0 % of the transaction. These fees are distinct from FX conversion spreads and apply even when both currencies are the same. Since Brexit, the Payment Systems Regulator (PSR) has confirmed that card-not-present (CNP) interchange rates between the UK and EEA rose from 0.2 / 0.3 % to 1.15 / 1.5 % for consumer debit/credit transactions (PSR Cross-Border Fees Report, 2024). For high-risk verticals such as iGaming, where margins often fall below three %, this single regulatory change effectively doubled processing costs overnight.

Card schemes defend the increase as compensation for “higher cross-border fraud risk,” but the outcome is a structural FX disadvantage: every EEA deposit or withdrawal routed through a UK acquirer now carries a material surcharge independent of market volatility.

2. Double Conversion and Dynamic Currency Conversion (DCC) Traps

The next leak appears when PSPs or acquirers layer multiple conversions between authorisation and settlement. A typical scenario: a German player deposits €100, the acquirer settles in USD, and the merchant treasury converts back to EUR for reporting. That three-step journey incurs three distinct spreads.

Dynamic Currency Conversion (DCC) options offered at the checkout can worsen results; while they promise transparency, they often embed mark-ups exceeding 3-5 % over wholesale interbank rates (Mastercard DCC Advisory, 2025). Regulators have begun tightening oversight, and the European Commission’s Retail Payments Strategy flags DCC as an area for consumer price intervention by 2026 (European Commission Retail Payments Strategy Update, 2025).

3. Timing Risk and Chargeback FX Losses

Volatility in short-dated currency pairs can transform small operational lags into realised losses. A 1.5 % intraday swing between EUR and GBP is enough to erase an operator’s net revenue on high-value deposits.

When chargebacks occur, card-network rules require refunds at the prevailing rate, not the original authorisation rate, crystallising FX differences directly in the merchant P&L. Visa Europe estimates that FX variance adds 30 – 70 basis points to effective dispute costs (Visa Risk Operations Report, 2024).

Some operators attempt to hedge by maintaining multi-currency reserves, but without automated netting or rolling forwards, these balances simply transfer risk from pricing to liquidity management.

4. Liquidity and Prefunding Costs

Every payout corridor that uses a non-native currency requires prefunding. Holding idle balances across five or six currencies ties up working capital and exposes operators to mark-to-market loss. The European Banking Authority (EBA) has warned PSPs that “unhedged prefunding of instant-payment accounts introduces systemic settlement risk” (EBA Opinion on Instant Payments Settlement Risk, 2025).

In practice, merchants bear both the opportunity cost of trapped liquidity and the conversion cost when those accounts are eventually rebalanced.

5. Data Opacity and Rate-Source Risk

Finally, many operators rely on acquirer statements that provide no reference rate or timestamp for conversions. Without visibility into whether the rate came from a wholesale feed, a PSP markup, or a card-scheme table, treasury teams cannot validate pricing. The UK FCA’s Consumer Duty (2025) now obliges payment providers to disclose “the effective FX rate applied, the benchmark rate used, and any margin or fee in basis-point terms”.

Hedging and Conversion Strategies – From Forwards to Stablecoins

Once an operator understands where FX costs accumulate, the next step is to neutralise them. In 2026, treasury efficiency in iGaming depends less on predicting markets and more on engineering certainty, locking in rates, automating conversions, and selecting settlement mechanisms that balance speed with compliance. The tools range from conventional derivatives to emerging blockchain rails, all converging on one goal: eliminating unplanned currency exposure.

1. Forward Contracts: Locking in Predictability

The most established hedge remains the FX forward, allowing operators to buy or sell a currency at a fixed future rate. Short-dated (30-60 day) forwards match naturally with payout cycles and affiliate remittances. The Bank for International Settlements (BIS) noted that forward and swap turnover reached $5.3 trillion per day in 2025, driven by corporates hedging short-term exposures (BIS Triennial Survey 2025).

For iGaming treasurers, this approach transforms variable settlement costs into known expenses. The trade-off is cash-flow discipline: forwards require collateral or credit lines, making them best suited for mid-sized and regulated operators with predictable volume.

2. PSP Auto-Conversion and Rate-Lock Tools

Most major payment processors now offer auto-conversion modules that execute currency swaps at defined thresholds or within preset rate bands. For example, when EUR/USD moves beyond ±0.5 %, the system auto-converts merchant balances into the target settlement currency.

While convenient, the hidden risk lies in opacity: many PSPs apply undisclosed mark-ups above wholesale rates. Under the UK FCA Consumer Duty (2025), acquirers must now disclose the source rate and spread applied to every conversion. Merchants should treat automation as a trigger mechanism, not as a substitute for transparent pricing.

3. Stablecoin Settlements: Faster, But Not Yet Friction-Free

An emerging hedge against short-term volatility is stablecoin settlement, typically using regulated USD-pegged tokens such as USDC or PYUSD. Because these instruments settle on-chain within minutes, they remove the intraday timing risk between payout initiation and clearing.

However, regulatory scrutiny is intensifying. The EU Markets in Crypto-Assets Regulation (MiCA, 2024) restricts e-money tokens to issuers authorised in the EU and imposes daily redemption and reserve-audit requirements.

For gaming operators, this means stablecoin settlements are viable only through PSPs holding MiCA-compliant licences or through custodial banking partners that can immediately convert on receipt. Used correctly, they can stabilise USD flows and bypass weekend liquidity constraints; used poorly, they introduce custodial and on-chain AML risk.

4. Natural Hedging via Multi-Currency Wallets

A practical middle ground lies in natural hedging, maintaining local-currency inflows and outflows within the same wallet. For example, EUR player deposits fund EUR payouts, eliminating FX. Multi-currency wallets and virtual IBAN (vIBAN) structures now allow treasurers to net positions automatically before converting residual balances. The European Banking Authority (2025) encourages vIBAN segregation to improve transparency and liquidity tracking.

When paired with instant-payment rails like SEPA Instant or Faster Payments, this approach allows near-real-time currency matching and minimises timing gaps.

5. Building a Layered Hedge Policy

Effective FX management rarely relies on one instrument. A layered framework might combine:

- Operational hedges (matching inflows/outflows by currency),

- Financial hedges (rolling forwards for major pairs), and

- Liquidity buffers (stablecoin or overnight swaps for weekend coverage).

The Institute of Corporate Treasurers (UK, 2025) recommends “triangulated hedging” for high-frequency merchants, using forwards for predictability, automation for agility, and stablecoins for immediacy (ACT Treasury Tech Survey 2025).

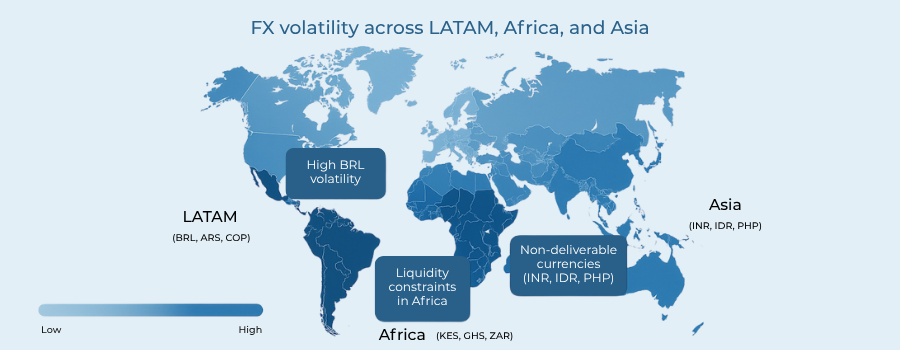

Regional Pain Points – FX Volatility in Africa, LATAM and Asia

The challenge of managing foreign exchange risk in iGaming isn’t distributed evenly across the globe. Markets with rapid adoption of digital payments, especially in Africa, Latin America (LATAM), and Asia, also exhibit the highest currency volatility and liquidity fragmentation. Understanding each region’s pain points allows operators to choose the right hedging and settlement tools before entering or scaling operations.

1. LATAM – High Adoption, High Volatility

No region has embraced instant payments as rapidly as Latin America. Brazil’s PIX processed over 5 billion transactions in Q1 2025, with adoption exceeding 90% of adult users. Yet while PIX lowers transaction fees and settlement times, it exposes operators to local-currency volatility, especially in BRL, ARS, and COP pairs.

- The Brazilian Real (BRL) is among the most volatile major emerging currencies, averaging 12-15% annualised volatility in 2024–2025 (Bank for International Settlements, 2025).

- Argentina’s capital controls restrict offshore conversion, forcing PSPs to rely on local liquidity providers and informal FX corridors.

- Colombia’s Transfiya network, modelled on PIX, improves domestic transfers but not currency convertibility.

For gaming operators, this means deposits in local currencies often must be converted to USD or EUR before settlement, introducing multi-step FX exposure. PSPs like dLocal and EBANX mitigate some risk through multi-currency wallet infrastructure, yet operators remain responsible for final treasury conversion. Regulatory uncertainty, particularly around crypto-based hedging, limits the use of stablecoins for cross-border settlements.

Mitigation: Implement real-time rate monitoring, forward contracts for BRL/USD, and regional liquidity buffers to smooth weekend volatility.

2. Africa – Mobile Money Dominance Meets Currency Fragility

Africa’s payments landscape is defined by mobile money, not cards. Platforms like M-Pesa (Kenya), Airtel Money (Nigeria), and EcoCash (Zimbabwe) process billions in low-value payments monthly, but underlying currencies remain thinly traded and volatile. The African Development Bank (AfDB) estimates that sub-Saharan currencies depreciated 8-12% on average in 2024, primarily due to inflation and dollar scarcity (AfDB Digital Finance Outlook, 2025).

Even with national instant-payment systems such as TIPS (Tanzania) and RPP (South Africa), cross-border liquidity remains a bottleneck. The Pan-African Payment and Settlement System (PAPSS), live in 10 countries as of 2025, enables intra-African currency clearing but still relies on USD as a settlement intermediary (Afreximbank PAPSS Progress Report, 2025).

For iGaming operators, this means exposure not only to currency depreciation but also to liquidity delays. PSPs in Kenya or Ghana may require 24-48 hours to convert KES or GHS into USD, introducing timing risk even when the payment rails themselves are instant.

Mitigation: Pair local payout rails (M-Pesa, RPP) with centralised treasury FX aggregation. Use forward NDFs (non-deliverable forwards) for KES/USD or ZAR/USD to hedge short-term volatility.

3. Asia – Non-Deliverable Currencies and Capital Controls

In Asia, payment infrastructure is highly advanced, but currency convertibility is often restricted. India’s UPI, Singapore’s PayNow, and Malaysia’s DuitNow have created near-instant domestic rails, yet operators face hurdles when repatriating funds or managing cross-border settlements.

- The Indian Rupee (INR), Indonesian Rupiah (IDR), and Philippine Peso (PHP) are all non-deliverable currencies, meaning offshore FX hedging requires NDF contracts rather than deliverable forwards.

- China’s digital yuan pilots remain domestic-only, limiting cross-border applicability for gaming PSPs.

Additionally, regional regulators impose strict remittance approvals. In India, for example, the Liberalised Remittance Scheme (LRS) limits outward flows and subjects gaming-related settlements to enhanced due diligence (Reserve Bank of India LRS Guidelines, 2025).

Mitigation: Use multi-currency acquiring where possible to avoid INR or IDR conversion until the point of payout. Implement NDF hedges via licensed counterparties and monitor onshore–offshore rate differentials daily.

4. Europe & UK – Mature Markets, New Transparency Rules

Although volatility is lower in EUR and GBP, regulatory FX scrutiny is higher. The EU Instant Payments Regulation (2025) requires price parity between instant and standard transfers, while the UK FCA’s Consumer Duty (2025) demands transparent disclosure of all FX-related fees. For iGaming operators licensed in both jurisdictions, the key risk is non-compliance rather than market movement.

Mitigation: Standardise reporting across acquirers, publish FX cost ranges to meet disclosure rules, and adopt instant rails (SEPA Instant, Faster Payments) to eliminate timing variance.

Bank & PSP Solutions – Multi-Currency Wallets and Payout Reconciliation

For high-risk iGaming operators, solving the FX challenge isn’t only about market timing; it’s about infrastructure design. The right combination of banking partners, PSP orchestration, and reconciliation architecture determines whether currency exposure is a controlled variable or an operational liability. As regulators demand real-time visibility and players expect instant withdrawals, multi-currency treasury integration has become a core risk-control function, not just a back-office upgrade.

1. Multi-Currency Acquiring: Pricing and Settling in the Player’s Currency

The simplest way to eliminate FX risk is to avoid unnecessary conversion. Multi-currency acquiring enables merchants to price, authorise, and settle in the same currency the player uses. Leading acquirers now support over 150 settlement currencies across Visa and Mastercard networks.

This approach shields operators from mid-cycle volatility and preserves transparency for both acquirers and regulators.

However, acquirer availability is not uniform. Post-Brexit, some UK acquirers have restricted EEA currency settlement, forcing iGaming merchants to rely on EU-licensed PSPs. The European Banking Authority (EBA) advises PSPs to maintain “clear disclosures on currency handling and conversion practices” under the 2025 Instant Payments Regulation (EBA Opinion on Instant Payments Supervision, 2025).

Best Practice: Request acquirer disclosures detailing supported currencies, cut-off times, and applicable FX mark-ups. Merchants with high EUR, GBP, or BRL volumes should maintain dual acquiring relationships in both home and regional markets.

2. Multi-Currency Wallets and Virtual IBAN (vIBAN) Architecture

Modern PSPs and fintech banks now offer multi-currency wallets with unique virtual IBANs (vIBANs) per client or sub-wallet. Each vIBAN acts as a segregated account for incoming player deposits, payouts, or affiliate settlements, mapped by currency and jurisdiction.

The European Payments Council (EPC) recognises vIBANs as a key enabler for transparent reconciliation, allowing merchants to segregate flows without breaching PSD2 safeguarding rules. For operators, this architecture means every payout and refund can be matched to its original funding currency in real time, eliminating “ghost FX” entries caused by cross-ledger mismatches.

When combined with instant-payment rails, SEPA Instant (EUR), Faster Payments (GBP), and PIX (BRL), vIBAN wallets allow for localised disbursement and instant fund visibility. The Bank for International Settlements (BIS) highlights that real-time FX reconciliation reduces operational losses by up to 40% in multi-currency treasuries.

3. Reconciliation Automation and Data Standardisation

In high-volume gaming operations, manual reconciliation is both costly and prone to error. Modern PSPs employ ISO 20022 messaging standards to embed rate, timestamp, and currency fields directly within payment confirmations. This ensures every transaction, deposit, payout, and refund arrives with its FX rate metadata attached.

The Pay.UK New Payments Architecture (NPA) programme mandates richer data payloads for real-time transactions to “support end-to-end reconciliation, fraud analytics, and liquidity reporting”. For merchants, these data enhancements mean reconciliation systems can auto-post FX differences and generate granular P&L attribution per currency pair.

Advanced orchestration platforms such as Mambu, ACI, and Airwallex—already integrate AI reconciliation engines capable of flagging FX anomalies (e.g., unexpected rate deviations >50bps). These controls not only improve accuracy but also support FCA and EBA audit requirements for traceable FX pricing.

4. Liquidity Orchestration Across PSPs and Banks

A final frontier is real-time liquidity management. Holding prefunded balances across multiple currencies can tie up capital and amplify FX exposure. PSPs now offer API-based liquidity sweeps, transferring surplus balances automatically between wallets or banks when exposure exceeds preset limits.

The European Central Bank (ECB) and Swiss National Bank (SNB) have jointly explored instant cross-currency settlement between EUR and CHF corridors, targeting reduced settlement latency and credit risk (ECB–SNB Interlinking Feasibility Report, 2025). Such initiatives pave the way for fully automated, cross-rail FX orchestration by 2026.

Best Practice: Implement dashboards that display total exposure by currency, prefunded ratio, and net FX P&L. Liquidity transparency builds trust with acquirers and supports regulatory audits under PSD3’s forthcoming treasury-reporting clauses.

Risk Management Checklist – Monitoring FX Exposure in Real Time

Even the most sophisticated multi-currency infrastructure will fail to protect margins if FX risk isn’t continuously monitored. In high-risk verticals like iGaming, where payment flows operate 24/7 across multiple jurisdictions, exposure can change by the minute. A robust FX risk framework combines real-time visibility, automated thresholds, and policy discipline across treasury, compliance, and operations.

1. Continuous FX P&L Visibility

FX control begins with live data. Treasury teams should track realised and unrealised gains or losses per currency pair across all payment rails, cards, instant payments, and e-wallets. Modern treasury systems now provide API-based rate feeds (via Refinitiv, Bloomberg, or PSPs) that calculate the delta between the transaction rate and live mid-market pricing.

The Association of Corporate Treasurers (ACT) notes that “real-time FX dashboards improve exposure accuracy by up to 80%, particularly in high-volume e-commerce and gaming environments” (ACT Treasury Tech Survey, 2025).

This transparency is increasingly expected by regulators. Under PSD3, PSPs must ensure merchants have access to auditable FX rate data within each transaction record (European Commission PSD3 Proposal, 2025).

2. Net Position Limits and Auto-Hedge Triggers

Operators should define daily net exposure limits per major currency (e.g., USD/EUR, GBP/EUR, BRL/USD). Once a threshold is breached, preconfigured rules can automatically execute a conversion or forward hedge.

Platforms like ACI Worldwide and Airwallex offer integrated FX exposure modules that can auto-trigger swaps based on defined variance bands, minimising human error.

The Bank for International Settlements (BIS) emphasises that corporates adopting algorithmic hedge triggers experience “reduced hedging lag and 25–35% lower average exposure duration” (BIS Innovation Hub Quarterly, 2025).

Such systems are particularly valuable during volatile trading sessions or after major macro events that move rates sharply between player deposits and payouts.

3. Benchmark Rate Auditing

Without verifying rate sources, even automated systems can drift from fair market value. The UK Financial Conduct Authority (FCA) Consumer Duty (2025) mandates that payment providers disclose the FX rate benchmark (e.g., ECB, Reuters, Mastercard) and any associated margin.

Gaming operators should reconcile each PSP’s conversion rate daily against an independent benchmark, typically the ECB Reference Rate or WM/Reuters 4 pm Fix.

Auditing these benchmarks ensures treasury teams can explain every basis-point deviation during acquirer or regulator reviews.

4. Counterparty Concentration and Credit Risk

Many operators underestimate counterparty risk, the danger that a PSP or FX broker fails during volatile periods. Diversifying across two or more settlement providers per major currency reduces dependency on a single liquidity source.

The European Banking Authority (EBA) advises that PSPs managing instant-payment liquidity must hold “real-time collateral coverage and redundancy in correspondent relationships”.

Operators should apply similar principles:

- Set maximum counterparty exposure limits (e.g., ≤40% of total FX volume).

- Conduct quarterly reviews of PSP balance-sheet strength and regulatory capital.

- Maintain dual banking arrangements to ensure payout continuity in a stress event.

5. Governance and Policy Oversight

Even the most advanced analytics require governance. A formal FX Risk Policy, approved by senior management and audited annually, should outline:

- Reporting frequency and format (daily dashboards, monthly summaries).

- Hedging instruments allowed (forwards, NDFs, stablecoin conversion).

- Risk limits and escalation paths for breaches.

- Review cadence (quarterly board or compliance review).

According to PwC’s Treasury Risk Report 2025, organisations with codified FX policies show “40% lower variance in monthly treasury P&L” compared to those relying on ad-hoc decision-making (PwC Treasury Risk Report, 2025).

Documented policy frameworks also help satisfy the FATF’s Recommendation 15, requiring risk-based oversight of new payment technologies (FATF AML Guidance, 2024).

6. Key Components of a Real-Time FX Risk Dashboard

A compliant and efficient treasury dashboard should include:

- Real-time rates from at least two independent data feeds.

- Exposure per currency pair (gross and net).

- Counterparty concentration ratio.

- Daily realised/unrealised FX gain-loss report.

- Alert system for exposure or rate deviations >50 bps.

- Drill down by PSP, acquirer, and payment rail for audibility.

2026 Forecast – Smart Treasury and Automated FX Pricing

By 2026, FX management in iGaming will look radically different from the manual spreadsheets and static PSP conversions that defined the industry a decade earlier. Treasury teams are moving toward autonomous FX engines, systems that predict exposure, price conversions dynamically, and execute hedges without human intervention. Driven by new regulations, higher volatility, and the rise of instant settlement, the future of FX in high-risk gaming is algorithmic, real-time, and fully auditable.

1. AI-Driven Treasury Engines: Predicting Exposure Before It Happens

The next evolution in FX management is predictive treasury modelling. Using historical player behaviour, seasonality, and market volatility indicators, AI engines can estimate inflow and outflow currency ratios hours or even days in advance.

This allows operators to pre-position liquidity or lock in forward rates before exposure materialises.

The Bank for International Settlements (BIS) notes that machine-learning–based prediction systems have reduced corporate FX exposure by 20-30% in pilot implementations. For iGaming, where deposits may spike during sporting events or lunar holidays, this predictive capability is transformative.

By 2026, major PSPs are expected to integrate predictive FX models into their merchant dashboards, offering exposure forecasts alongside live balances.

2. Dynamic FX Markup Algorithms

Static FX mark-ups (+100 bps over ECB rate) will become obsolete. Instead, PSPs are rolling out dynamic FX pricing, where spreads adjust based on liquidity, time of day, rail availability, and market depth.

For example:

- During low-liquidity weekend trading, markups widen to cover volatility.

- When instant rails like SEPA Instant or PIX reduce timing risk, spreads narrow.

- In periods of low volatility, automated pricing engines can convert balances at tighter margins.

The European Commission’s PSD3 and PSR proposals explicitly encourage transparent, variable FX pricing models that reflect market conditions rather than fixed fees (European Commission PSD3 Proposal, 2025). This shift allows regulators to monitor fairness while enabling PSPs to deliver pricing that aligns with real-time liquidity conditions.

3. Automated Multi-Rail Routing to Reduce FX Slippage

By 2026, orchestration platforms will not simply route payments based on cost—they will route them based on FX impact.

A payout initiated in Brazil, for example, may be:

- Routed through PIX if the operator holds a BRL balance.

- Routed through Visa Direct if the user holds an international card.

- Settled via USD vIBAN if a forward contract is in place.

This kind of FX-aware routing minimises unnecessary conversions and reduces exposure windows.

The European Payments Council (EPC) notes that next-generation ISO 20022 messages allow “conditional routing logic for cross-border transactions based on real-time FX pricing and liquidity”.

4. Stablecoin: Fiat Hybrid Liquidity Models

Stablecoins will not replace fiat rails in regulated gaming, but they will augment them. Under MiCA (2024), only authorised e-money tokens (e.g., USDC under an EU-licensed issuer) can be used for settlement (MiCA Regulation, 2024).

In practice, this means PSPs may use stablecoins for:

- Overnight liquidity positioning,

- Weekend conversions,

- Buffering large USD/USDT flows in volatile LATAM or APAC markets.

The advantage is near-instant settlement, minimising timing exposure. The risk is custodial compliance: regulated iGaming merchants must maintain robust AML controls and transparency over on-chain movements. Expect regulators to require real-time blockchain analytics tools for PSPs using stablecoin legs in settlement chains.

5. Regulator-Mandated FX Transparency and Automation

Both the EU Instant Payments Regulation (2025) and the UK FCA Consumer Duty (2025) are accelerating the shift toward automation.

By 2026, merchants should expect:

- Automated disclosure of FX markups on every transaction,

- Mandatory reporting of rate source, timestamp, and margin,

- Machine-readable FX audit trails for supervisory reviews.

The European Banking Authority (EBA) confirms that PSPs must “embed FX rate information directly into instant-payment messages to ensure transparent end-user pricing and universal auditability” (EBA Instant Payments Supervision Opinion, 2025).

This regulatory push forces the industry to move from opaque, manual FX processes to automated, standardised, and regulator-visible FX workflows.

6. By 2026: FX Management Becomes Fully Embedded in Payments Infrastructure

The big trend is convergence: FX management will no longer sit in treasury alone; it will be a native layer of every PSP, payment orchestrator, and acquirer dashboard.

Operators will increasingly rely on:

- Automated swaps at settlement

- Self-adjusting FX margins

- Predictive liquidity alerts

- Instant cross-currency routing,

- And full, real-time reconciliation with embedded FX metadata.

This evolution mirrors the broader fintech trend described by the World Bank’s 2025 Cross-Border Payments Roadmap, which highlights “embedded FX layers as the future of frictionless cross-border commerce”.

Conclusion

By 2026, FX management is no longer an optional optimisation for iGaming operators, it is a defining marker of operational maturity. Currency volatility, cross-border fees, and timing mismatches have become structural costs baked into the economics of high-risk processing. At the same time, regulatory expectations across the EU, UK, LATAM, Africa, and APAC increasingly require transparent FX pricing, audit-ready rate data, and real-time liquidity controls.

The shift toward instant payment rails, SEPA Instant, Faster Payments, PIX, UPI, tightens the window between deposit and payout, compressing the time available to manage FX fluctuations. Regulators such as the European Banking Authority (EBA) and the UK FCA now expect PSPs and merchants to maintain full auditability of FX decisions and rate sources, embedding transparency directly into payment messages under PSD3 and the EU Instant Payments Regulation.

For gaming operators processing thousands of micro-transactions across EUR, GBP, USD, BRL, INR, ZAR, and emerging-market currencies, the real challenge is not volatility itself, but the compounding effect of unobserved FX decisions across multiple payment rails. The merchants that thrive in 2026 will be those that view FX holistically: not as a treasury function, not as a PSP feature, but as a multi-layered risk discipline spanning payments, compliance, liquidity, and technology.

Ultimately, FX stability is now directly linked to player experience, acquirer trust, and licence sustainability. Treasury teams that embrace automation, hedging discipline, and transparent pricing will unlock higher margins, smoother multi-market expansion, and stronger relationships with regulators and banking partners.

FAQs

1. Why do iGaming operators lose money on FX in the first place?

Most FX losses come from small mismatches across the deposit, wallet, and payout cycle. When players deposit in one currency but operators settle in another, PSPs apply multiple conversions, each with its own spread. Timing differences between authorisation and payout magnify the loss, especially during volatile periods. Card-scheme cross-border fees and post-Brexit UK–EEA interchange uplifts add another layer. Without line-by-line FX transparency, these losses remain hidden within acquirer statements.

2. What is the difference between deposit FX and payout FX?

Deposit FX occurs at the moment of authorisation, usually using Visa or Mastercard’s daily rate, plus a small spread. Payout FX occurs when funds leave the merchant back to the player, often days later. Because currency markets move continuously, payout conversions happen at a different rate than deposit conversions. The gap between the two is the operator’s timing risk, and it is often the largest source of realised FX loss.

3. How can multi-currency acquisition reduce FX losses?

Multi-currency acquiring allows operators to price, authorise, and settle in the same currency the player uses. This eliminates double conversion and protects against intraday volatility. When paired with virtual IBANs (vIBANs) and multi-currency wallets, merchants can match inflows and outflows locally and only convert residual balances. This is one of the most effective ways to stabilise FX costs.

4. Are stablecoins a safe option for managing FX exposure?

They can be, if used within regulation. Under MiCA (2024), only authorised e-money tokens are permitted for settlement in the EU. Stablecoins such as USDC (when issued by a regulated entity) can reduce timing risk for USD flows, especially over weekends. However, operators must ensure strong chain analytics monitoring, custodial oversight, and AML controls. Stablecoins should complement, not replace, fiat settlement rails.

5. How do forward contracts help iGaming operators?

FX forwards lock in a future exchange rate, giving operators certainty over their most volatile currency pairs, BRL/USD, GBP/EUR, INR/USD, etc. Forwards are ideal for hedging affiliate commissions, monthly settlements, or predictable payout cycles. They do require credit lines or collateral, so they are generally used by mid-tier and licensed operators. In periods of high volatility, forwards significantly reduce exposure to adverse FX swings.

6. What is the best way to reduce FX losses in LATAM?

LATAM volatility, especially in BRL, ARS, and COP, requires a layered approach:

- Use local settlement rails (PIX, SPEI) to minimise timing gaps

- Convert BRL to USD/EUR at predictable intervals using forwards

- Maintain local-currency buffers to avoid peak-hour spreads

- Work with PSPs offering multi-currency wallets and transparent rate sources

LATAM merchants must also avoid informal FX corridors due to compliance risk.

7. Why do African markets create unique FX challenges?

African FX markets combine mobile-money dominance with low-liquidity currencies such as KES, GHS, and ZAR. Conversion can take 24-48 hours, exposing operators to timing risk even when payments are instant. Many currencies are thinly traded offshore, making NDF hedging essential. Liquidity scarcity also means spreads widen during global volatility. Regional systems like PAPSS may help long-term, but still rely on USD intermediaries today.

8. How do non-deliverable currencies (NDFs) affect iGaming FX strategy?

Currencies like INR, IDR, and PHP cannot be freely traded offshore. Operators must use NDF contracts, derivatives that settle the difference in USD instead of delivering the local currency. NDF hedging is essential for Asia-facing operators because it provides rate certainty without requiring physical delivery. It also aligns with central-bank capital-control rules, reducing regulatory exposure.

9. What is the role of reconciliation in controlling FX losses?

Accurate reconciliation ensures every conversion can be traced to its rate source, timestamp, and currency pair. ISO 20022 payment messages now embed this data automatically. When operators reconcile daily, they catch PSP mark-ups, double conversions, and unplanned currency shifts. Strong reconciliation is essential for PSD3, the EU Instant Payments Regulation, and the UK FCA Consumer Duty, all of which require transparent FX disclosures.

10. How can operators automate their FX management in 2026?

Modern PSPs and treasury systems now support:

- Auto-conversion thresholds

- Real-time exposure dashboards

- Predictive liquidity alerts

- Automated routing based on FX impact

- Instant sweeps across multi-currency wallets

These tools minimise timing risk and ensure consistency with regulatory expectations on pricing transparency and auditability.

11. Should operators hedge all currency exposures?

Not necessarily. Best practice is selective hedging:

- Hedge predictable or high-volume pairs (EUR/GBP, BRL/USD).

- Use natural hedging (matching inflows/outflows) wherever possible.

- Avoid over-hedging exotic or thinly traded currencies unless business volume justifies it.

The optimal mix is usually: operational hedging + short-dated forwards + automated conversion.

12. How does FX volatility affect player experience?

Indirectly, FX volatility impacts payout speeds and payout amounts. When treasurers must hold settlements or wait for liquidity, withdrawals slow down. When PSPs apply unfavourable FX margins, players receive lower payout amounts than expected, damaging loyalty. Stable FX processes enable faster payouts, increased trust, and fewer customer complaints, especially in cross-border gaming markets.

13. What do Payment Mentors recommend for 2026?

Payment Mentors recommends a five-pillar FX framework:

- Multi-currency acquiring for core markets

- Predictive treasury modelling and exposure dashboards

- Forward or NDF hedging for volatile EM pairs

- Routing payouts through FX-efficient local rails

- Full FX auditability integrated with compliance reporting

This approach minimises FX leakage, strengthens banking relationships, and supports sustainable multi-market expansion.