In 2025, CBD and cannabis businesses are expanding faster than the banking frameworks built to support them. What began as a niche wellness trend has matured into a regulated global sector spanning consumer health, medicinal therapies, and lifestyle products. Yet, despite its legitimacy in markets such as Canada, the UK, and Australia, payment access remains one of the industry’s hardest barriers.

Traditional card acquirers and high-street banks still classify cannabinoid-derived products as high-brand-risk, leaving legitimate operators facing account closures, withheld settlements, and surging chargebacks. The result is a wave of merchants turning to offshore acquiring, alternative payment rails, and local account-to-account networks such as PIX (Brazil) and Interac (Canada) to keep cash flowing securely.

This guide from Payment Mentors explores how regulated CBD and cannabis companies can structure compliant payment ecosystems across jurisdictions, balancing legal access, anti-fraud protection, and global scalability.

- The Global Legal Landscape (US vs. Canada vs. Europe vs. Australia)

- Card Network Policies & Scheme Risk (Visa & Mastercard)

- Banking Access Strategies: How CBD and Cannabis Merchants Secure Reliable Financial Infrastructure

- The Reality of Banking Restrictions

- Tier 1: Specialist Partner Banks (Domestic, Licensed)

- Tier 2: Third-Party Aggregators and EMIs

- Tier 3: Offshore Acquiring in CBD-Friendly Jurisdictions

- Tier 4: Alternative Payment Methods (APMs) and Local Rails

- Designing a Multi-Banking Strategy

- How Payment Mentors Supports Access

- CBD Fraud & Chargeback Risks: How to Detect and Mitigate Them

- Why CBD Is a Prime Target for Fraud

- The Four Major Types of CBD-Related Fraud

- How Fraud Affects Underwriting & Merchant Stability

- Advanced Tools to Combat CBD-Specific Fraud

- Managing Chargebacks Through Education and Transparency

- AML Linkage: Fraud as a Gateway to Money Laundering

- Building a Fraud-Resilient Payment Model

- The Offshore Advantage: How Global Structures Enable Legal Market Access

- Why Offshore Structures Exist in the CBD and Cannabis Ecosystem

- Leading Offshore Jurisdictions for CBD & Cannabis Payments

- Structuring Offshore Entities: The Compliance Model

- Offshore as an AML Shield, Not a Loophole

- The Role of Offshore Aggregators and Gateways

- Payment Mentors’ Offshore Structuring Framework

- Conclusion

- FAQs

The Global Legal Landscape (US vs. Canada vs. Europe vs. Australia)

Understanding the Patchwork of Global Regulation

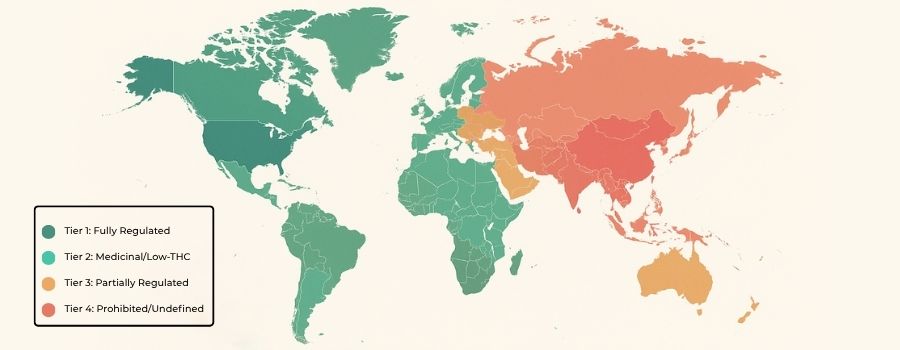

The CBD and cannabis industries operate in one of the most fragmented legal environments worldwide. What is considered a regulated consumer product in Canada or the UK may still constitute a criminal offence in parts of the United States or Asia. For payment processors and underwriters, this patchwork directly determines who they can legally serve, and under what conditions.

To succeed in this landscape, high-risk merchants must understand four regulatory tiers:

| Tier | Region/Example | Legal Status | Payment Processing Feasibility |

| Tier 1 – Fully Regulated Cannabis | Canada | Legal nationwide for medical & recreational use | Full card & banking access under FINTRAC oversight |

| Tier 2 – Medicinal or Low-THC Only | UK, Australia, New Zealand, South Africa, Brazil | Legal with product & THC thresholds | Card acquiring possible for compliant merchants |

| Tier 3 – Partially Regulated CBD | EU Member States (France, Germany, Netherlands) | CBD legal if THC <0.2-0.3% and novel food authorised | Restricted by acquirer policy; Open Banking/EMI alternatives growing |

| Tier 4 – Prohibited or Undefined | Asia, Middle East (except medical pilots) | No clear legal framework | Offshore acquiring or APM-only routes required |

United States: Legality with Federal Limitations

Despite widespread state-level legalisation, the U.S. remains the most complex jurisdiction.

- CBD (hemp-derived, ≤0.3% THC) was federally permitted under the 2018 Farm Bill, yet banks remain cautious due to inconsistent FDA enforcement and ongoing scrutiny of health claims.

- Cannabis (THC products) remains illegal at the federal level (Schedule I), although the DEA’s proposed reclassification to Schedule III (May 2025) could relax medical use and banking restrictions in future.

- Payment impact: Visa and Mastercard prohibit direct card acquiring for THC transactions; merchants rely on ACH, closed-loop wallets, or cashless ATMs (many of which are now being phased out).

Canada: The Global Benchmark for Legal Market Integration

Canada remains the gold standard for compliant cannabis processing.

- Cannabis has been fully legal since 2018, with licensing through Health Canada and strict AML obligations under FINTRAC.(Source: Cannabis in Canada)

- Merchants can accept credit/debit cards, Interac e-Transfers, and digital wallets, provided they maintain age verification and reporting controls.

- Many acquirers classify cannabis merchants as restricted but serviceable under enhanced due diligence (EDD).

United Kingdom & European Union: CBD-Only, Strictly Controlled

In the UK, cannabis remains a controlled substance, but CBD products are legal if derived from approved hemp and compliant with novel food regulations.

- The Food Standards Agency (FSA) maintains a Public List of approved CBD products (2025 version lists ~3,500 entries).(Source: CBD businesses to reformulate products on the Public List for safety reasons)

- Products outside this list are considered non-compliant, and merchants selling them risk deactivation by acquirers.

- EU Member States apply varying THC limits (0.2%-0.3%) and require product traceability, certificates of analysis (COAs), and transparent labelling.

Payment impact:

While the UK and EU support regulated CBD commerce, Visa and Mastercard still treat CBD as a high-brand-risk vertical, requiring dedicated merchant category codes (MCC 5499 – Misc. Food Stores) and often imposing rolling reserves or delayed settlements.

Australia & New Zealand: Medical Use Under Tight Control

Australia legalised medical cannabis in 2016, but recreational use remains prohibited.

- Dispensaries and licensed producers operate under Therapeutic Goods Administration (TGA) oversight.

- AUSTRAC enforces strict AML compliance on reporting entities, with emphasis on cross-border data sharing and suspicious matter reports (SMRs).

- New Zealand mirrors this model, approving limited medical cannabis programmes but restricting consumer CBD imports.

Payment impact:

CBD merchants often rely on domestic EMIs or offshore processing in regulated zones such as Malta or the Isle of Man to maintain international card acceptance.

LATAM: Brazil’s Medical Market Emerges

Brazil has rapidly become LATAM’s most structured CBD market.

- Under ANVISA RDC 3/27/2019, registered firms can sell medical-grade cannabis products with <0.2% THC.

- In 2025, regulators proposed expanding access via pharmacies, aligning with European models.

- Payments rely heavily on PIX, Brazil’s instant payment network, which offers real-time settlement and low fraud exposure.

South Africa: Controlled, Not Criminalised

South Africa’s SAHPRA has authorised limited CBD formulations for sale (<20 mg daily dose; <0.001% THC).

- Cannabis for recreational use remains prohibited but decriminalised for private consumption.

- AML regulation via FSCA and Financial Intelligence Centre (FIC) mirrors FATF recommendations.

The Legal Map in Practice

| Region | CBD Legal? | Cannabis Legal? | Bank Access? |

| UK/EU | ✔️ Regulated CBD only | ❌ No | Limited / Offshore |

| USA | ✔️ CBD / ❌ THC | ❌ Federally | ACH / Closed Loop |

| Canada | ✔️ | ✔️ | Full Access |

| Brazil | ✔️ (Medical only) | ❌ | PIX / Local EMI |

| Australia/NZ | ✔️ (Medical) | ❌ | EMI / Offshore |

| South Africa | ✔️ (Low-dose) | ❌ | EMI / Limited Bank |

Card Network Policies & Scheme Risk (Visa & Mastercard)

Why Card Schemes Still Classify CBD as High Brand Risk

Despite growing legalisation, both Visa and Mastercard continue to categorise CBD and cannabis-related merchants under their high-brand-risk verticals. This means acquirers must apply enhanced due diligence (EDD), conduct ongoing transaction monitoring, and in many cases, establish rolling reserves or delayed settlements.

The concern isn’t legality alone, it’s brand association and reputational risk. Card networks operate globally, so policy uniformity matters more than national legality. Even if a merchant is fully licensed in Canada or the UK, transactions could still be declined if the acquirer or issuer bank operates in a jurisdiction where cannabis remains prohibited.

Key risks identified by Visa and Mastercard:

- Unverified or unlicensed CBD merchants marketing medical or therapeutic claims.

- Cross-border transactions involving products legal in one market but not the buyer’s.

- Mislabelling or COA (Certificate of Analysis) inconsistencies.

- Brand complaints or excessive chargebacks tied to unclear billing descriptors.

Visa’s Stance: CBD vs. Cannabis

Visa Inc. distinguishes sharply between CBD-only products and cannabis/THC-derived products.

- CBD derived from hemp (≤0.3% THC) may be accepted if the product is legally sold under local regulations.

- Cannabis or THC-containing products remain prohibited worldwide under Visa policy, regardless of local legality.

- Acquiring banks must confirm the merchant’s full supply chain transparency, including source country and lab certifications.

- Visa mandates that acquiring partners maintain an Acceptable Use Policy Register identifying all CBD merchants and validating their legal basis for sale.

Visa’s 2024-2025 compliance update introduced the CBD Merchant Classification Matrix, requiring acquirers to report product type, THC content, jurisdiction, and evidence of compliance before boarding.

Practical outcome:

Merchants without local incorporation in an approved jurisdiction (e.g., the UK, Canada, Malta) often face automatic rejection from Visa-connected acquirers in the U.S. and Asia.

Mastercard’s Position: The High-Brand-Risk Framework

Mastercard applies an even stricter policy under its Brand Risk Evaluation Process (BREP). CBD merchants fall into Tier 3 of its High-Brand-Risk hierarchy, which also includes sectors like nutraceuticals, tobacco, and adult entertainment.

To onboard CBD merchants, acquirers must:

- Provide evidence of ongoing product testing and lab certification.

- Implement descriptor accuracy (no misleading medical or curative claims).

- Conduct bi-annual audits and transaction-level monitoring.

Mastercard also requires transparent payment page disclaimers, age verification where applicable, and the ability for cardholders to clearly identify CBD products before checkout to reduce chargebacks.

Example: In 2024, several European acquirers were fined for onboarding CBD merchants selling oils and gummies without a valid Novel Foods application, an explicit breach of Mastercard’s brand protection policy.

Descriptor, Labelling, and Content Compliance

Both Visa and Mastercard are particularly sensitive to misleading product descriptors and non-compliant advertising. Even a single mention of healing, medical, or pain relief without scientific approval can trigger scheme-level chargeback rights or merchant termination.

Best practices for compliance:

- Use accurate, neutral descriptors (CBD supplement, not medical CBD oil).

- Display third-party COAs (Certificates of Analysis) on-site.

- Avoid medical or disease claims unless approved by the regulator (e.g., FSA, FDA, or Health Canada).

- Use age-gated payment pages where CBD products are subject to 18+ restrictions.

Payment Mentors often advises CBD clients to undergo a Pre-Onboarding Audit, ensuring all descriptors, COAs, and terms meet both acquirer and scheme requirements before submission, this can reduce rejection risk by up to 70%.

Legitimate Workarounds and Offshore Pathways

While card networks remain cautious, compliant CBD merchants can still gain access to global rails through offshore or specialist acquirers.

Common legitimate solutions include:

- Partnering with offshore acquirers in CBD-friendly jurisdictions such as Malta, Lithuania, Gibraltar, or the Isle of Man, where banking regulation aligns with EU AML standards.

- Using EMI (Electronic Money Institution) gateways that tokenise transactions, protecting acquirers from brand exposure.

- Routing payments via local A2A rails (like PIX, Interac, or Open Banking) for domestic transactions.

- Maintaining dual descriptors: one for retail checkout and one for card statement clarity, to reduce refund friction.

Important: Workaround does not mean circumvention. All processing models must stay within card networks and AML frameworks. Offshore acquirers simply provide a jurisdictionally compliant buffer where domestic banks decline service.

Summary: Scheme Risk as a Strategic Variable

In essence, Visa and Mastercard’s cautious approach isn’t anti-CBD, it’s anti-ambiguity. Merchants who present clear, transparent compliance documentation and maintain full control of their marketing, descriptors, and payouts can access stable processing, even under the high-brand-risk label.

For CBD operators expanding globally, the smartest strategy isn’t fighting scheme risk, it’s engineering compliance into the payment model from day one.

Banking Access Strategies: How CBD and Cannabis Merchants Secure Reliable Financial Infrastructure

The Reality of Banking Restrictions

For all its growth, the global CBD and cannabis sector still faces an uncomfortable truth:

Most mainstream banks and acquirers continue to deny onboarding, even for fully legal operators.

This reluctance has little to do with legality itself and everything to do with risk layering:

- Regulatory ambiguity: Even small policy shifts can render a previously legal market non-compliant overnight (e.g., FDA enforcement in the U.S.).

- Perceived AML exposure: Banks fear reputational damage from unknowingly servicing grey-market operators.

- Cross-border inconsistencies: A CBD product legal in the UK may breach import laws in France or Dubai.

- Card network pressure: Visa/Mastercard scheme compliance requires banks to maintain high monitoring standards, which few want to assume.

To overcome this, legitimate CBD merchants adopt tiered banking strategies, partnering with multiple institutions, EMIs, and offshore acquirers to ensure operational continuity and regulatory alignment.

Tier 1: Specialist Partner Banks (Domestic, Licensed)

In regulated markets like Canada, the UK, and the EU, a handful of specialised banking partners are open to working with high-risk industries under defined compliance conditions.

Examples include:

Canada

FINTRAC-regulated banks and credit unions (Alterna Bank, DUCA) offer cannabis business accounts under enhanced due diligence and strict transaction reporting.

UK

A few EMI-based banks (e.g., ClearBank, Modulr, and PaySafe) support CBD-only accounts with proof of FSA approval and complete supply-chain traceability.

EU

Licensed payment institutions in Lithuania, Malta, and the Netherlands onboard EU-based CBD merchants under SEPA IBANs with full AML monitoring.

Requirements to qualify:

- Local incorporation & valid trade licence

- Source of product verification (hemp origin certificate, COA)

- Product legality confirmation from local regulator (e.g., FSA, MFSA)

- Business model narrative (use case, distribution method, customer geography)

Best practice: CBD merchants should prepare a Banking Compliance Dossier, containing these verified elements before approaching any financial institution.

Tier 2: Third-Party Aggregators and EMIs

When direct banking is unavailable, Electronic Money Institutions (EMIs) or third-party aggregators act as crucial bridges.

These platforms aren’t banks but are regulated payment institutions capable of holding funds and processing payments securely under e-money licensing frameworks (PSD2 in Europe, or equivalent).

Common EMI partners for CBD:

- Europe: Ecommpay, PayAlly, Nium, and TrustPayments, offer card acquiring, SEPA payouts, and FX settlement.

- UK: Checkout.com and Rapyd, support legal CBD merchants with compliant MCC allocation and rolling reserves.

- Canada: Payment Rails / Trolley, focus on digital payouts (Interac, EFT).

- Australia: Airwallex and Novatti, handle cross-border flows under AUSTRAC oversight.

Advantages:

- Lower entry barriers than banks

- Pre-built compliance reporting

- Multi-currency & multi-rail settlement

- Shorter underwriting cycles

However, EMIs typically cap monthly volumes and hold rolling reserves (5-10%) until transactional trust is established.

Tier 3: Offshore Acquiring in CBD-Friendly Jurisdictions

For global CBD operators or cannabis-adjacent merchants (e.g., edibles, vapourisers, or CBD cosmetics), offshore acquiring remains the most scalable solution.

Preferred jurisdictions include:

- Malta: Recognised under the EU regulatory passport system, hosting multiple EMI and acquirer licences for nutraceutical and CBD verticals.

- Gibraltar: Integrates gambling, crypto, and high-risk processing oversight with clear AML/KYC mandates.

- Curacao: Common for eCommerce and iGaming crossover merchants handling CBD as a lifestyle supplement.

Offshore acquiring benefits:

- Access to global card networks despite domestic restrictions

- Flexible compliance review processes

- Multi-currency IBANs and rapid settlements

- Optional integration with crypto-gateways or stablecoin settlements

However, offshore solutions must never be used to conceal beneficial ownership or evade tax obligations, doing so breaches FATF and OECD AML standards.

Best practice: Align offshore banking with transparent parent-company reporting and sub-licensing structures compliant with home-market rules.

Tier 4: Alternative Payment Methods (APMs) and Local Rails

In markets where card acceptance remains difficult, Alternative Payment Methods (APMs) offer a compliant and customer-friendly route.

Examples:

- Brazil: PIX instant payments, enables 24/7 real-time transactions with in-built fraud detection and biometric validation.

- Canada: Interac e-Transfer, widely used for CBD sales via local accounts, integrated with AML transaction tracking.

- UK & EU: Open Banking, allows direct bank-to-bank payments, reducing reliance on card networks.

- South Africa: EFT Secure, supports verified A2A transactions for online CBD stores.

These systems not only reduce chargeback exposure, but also support strong customer authentication (SCA) and real-time AML screening.

Challenge: settlement reconciliation and refund handling can be complex, requiring robust reporting infrastructure.

Designing a Multi-Banking Strategy

For sustained stability, Payment Mentors recommends a multi-layered banking architecture:

| Layer | Partner Type | Purpose | Risk Level |

| Tier 1 | Domestic Specialist Bank | Core business account | Low |

| Tier 2 | EMI / PSP | Daily settlements & payouts | Medium |

| Tier 3 | Offshore Acquirer | Global card access | Medium-High |

| Tier 4 | APM / Open Banking | Local market optimisation | Low-Medium |

This layered approach ensures continuity, if one acquirer withdraws, operations continue seamlessly through alternative rails.

How Payment Mentors Supports Access

At Payment Mentors, we help CBD and cannabis merchants navigate this fragmented ecosystem by:

- Preparing full compliance packs for onboarding (KYC, COA, AML narrative).

- Matching merchants with jurisdiction-appropriate banking partners (EU, LATAM, UK, APAC).

- Establishing redundant payment setups to prevent liquidity lock-ins.

- Providing underwriting audit support to reduce rejection risk.

In an environment where a single compliance error can mean total de-banking, strategic payment structuring is not a luxury, it’s survival.

CBD Fraud & Chargeback Risks: How to Detect and Mitigate Them

Why CBD Is a Prime Target for Fraud

CBD and cannabis merchants sit at the intersection of eCommerce, health, and regulatory grey zones, making them a magnet for both legitimate consumers and malicious actors.

Fraudsters exploit the industry’s fragmented regulation, high average transaction values, and limited banking oversight. At the same time, genuine customers may unintentionally trigger chargebacks when they misunderstand product legality or effects.

Key fraud dynamics include:

- Ambiguity in product labelling or country-of-origin.

- Low consumer education around CBD legality and effects.

- Payment providers misclassify CBD under prohibited MCCs, causing refunds or cancellations.

- Exploitation of refund-friendly policies by opportunistic customers.

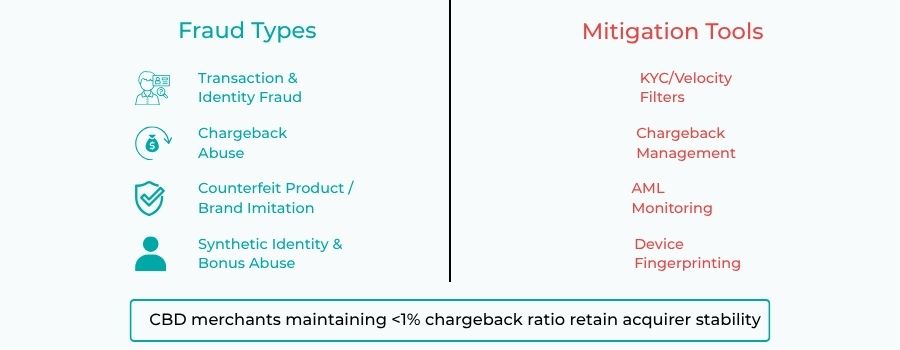

The Four Major Types of CBD-Related Fraud

1. Transaction & Identity Fraud

Fraudsters use stolen cards to purchase CBD products online, capitalising on merchants with weak KYC or velocity controls.

- Typically involves multiple small orders under threshold values.

- Often linked to reshipping scams, where goods are forwarded abroad to bypass import restrictions.

Mitigation:

- Implement device fingerprinting and IP geolocation verification.

- Enforce 3D Secure (3DS2) and Strong Customer Authentication (SCA).

- Use fraud scoring tools (e.g., Ekata, Kount, Riskified) with CBD-tailored rule sets.

2. Chargeback Abuse (Friendly Fraud)

Common among consumers who claim I didn’t authorise this or the product didn’t work.

- CBD’s subjective benefits make product dissatisfaction easy to claim.

- High refund rates trigger acquirer scrutiny and rolling reserves.

Mitigation:

- Transparent billing descriptors and refund policies.

- Product traceability (batch numbers, COAs).

- Chargeback representation tools that include delivery confirmation, age verification, and COA documentation.

Tip: Underwriters reward merchants who maintain <1% chargeback ratio, a key threshold for acquirer retention.

3. Counterfeit Product & Brand Imitation Fraud

As CBD demand surges, so does counterfeit production.

Fraudsters clone legitimate brand websites, use similar domains, or hijack payment pages to harvest card data.

Indicators:

- Domain names resembling major CBD brands.

- Unusual checkout behaviour (abandoned carts, repeated declines).

Mitigation:

- Register brand trademarks in every operating jurisdiction.

- Use SSL certificates, DNS monitoring, and merchant-verified trust seals.

- Employ content authenticity tracking (e.g., digital watermarking).

4. Synthetic Identity & Bonus Abuse

In subscription-based CBD models (e.g., wellness boxes or monthly tincture deliveries), fraudsters create synthetic identities to exploit first-time discounts or trial offers.

These accounts generate false loyalty metrics and artificial traffic, inflating marketing ROI and corrupting underwriting analytics.

Mitigation:

- Deploy velocity limits on IP and BIN usage.

- Cross-check customer IDs with databases such as LexisNexis or ComplyAdvantage.

- Implement automated KYC for repeat customers using biometric verification or selfie-ID match.

How Fraud Affects Underwriting & Merchant Stability

Fraud directly impacts how underwriters classify risk. A merchant with a history of chargebacks, refund spikes, or disputed transactions is automatically flagged in acquirer networks.

Consequences:

- Elevated rolling reserves (up to 15%).

- Delayed settlements (Net-30/45).

- Termination from card networks.

- Placement on MATCH or TMF lists (Terminated Merchant File).

In high-risk verticals like CBD, even a small surge in dispute ratios (e.g., 1.5%) can lead to account reviews or suspension. Thus, merchants must combine real-time fraud analytics with manual review processes to maintain underwriting trust.

Advanced Tools to Combat CBD-Specific Fraud

1. Device Fingerprinting & Behavioural Analytics

Tools such as FingerprintJS and Sift Science track device IDs, browsers, and session patterns to flag suspicious transactions.

2. Localised Velocity Checks

For LATAM and EU merchants, apply limits by payment method (PIX, SEPA, card) to prevent transaction bursts.

3. Geo-Fencing

Block or require manual review for orders from restricted markets (e.g., Middle East, China).

4. Tokenisation & Encrypted Vaults

Store card data using PCI-DSS compliant vaults (Level 1): reducing breach liability.

5. AI-driven Risk Scoring

Platforms such as Fraud.net and Sardine integrate across CBD gateways to deliver adaptive fraud detection with regulatory-specific rule sets.

Managing Chargebacks Through Education and Transparency

Education is often the most effective fraud prevention tool. CBD merchants that clearly communicate dosage, ingredients, and effects experience significantly lower chargeback rates.

Steps to take:

- Maintain visual COA documentation on every product page.

- Include disclaimers about medical efficacy (“Not intended to diagnose or cure”).

- Provide customer support contact before checkout and in confirmation emails.

- Offer refund credits instead of cash refunds to reduce cash-flow disruption.

Case Study Example:

A UK-based CBD oil merchant reduced chargebacks by 43% after redesigning its product pages with medical disclaimers and proof of COA sourcing, resulting in a positive acquirer reclassification from High to Moderate Risk.

AML Linkage: Fraud as a Gateway to Money Laundering

Underwriters now assess CBD fraud not just as a commercial risk, but as an AML exposure vector. Fraudulent CBD transactions can mask illicit transfers by using chargeback credits, refunds, or third-party wallets as a laundering layer.

To prevent this, acquirers require:

- Enhanced due diligence (EDD) for all high-volume refund issuers.

- Real-time transaction screening using AML APIs (Refinitiv, Dow Jones).

- KYC on both sides: customers and suppliers, to ensure legitimacy.

The UK Financial Conduct Authority (FCA) and FINTRAC (Canada) specifically classify CBD merchants as high risk for layered transactions, requiring documented transaction monitoring.

Building a Fraud-Resilient Payment Model

CBD businesses should view fraud prevention as an operational pillar, not a compliance box-tick. A resilient model combines technology, education, and policy control:

| Layer | Action | Outcome |

| Tech | AI fraud scoring, device tracking, geo-blocks | Prevents 80% of fraud attempts |

| Process | Manual review + velocity thresholds | Stops abnormal bursts |

| Policy | Clear descriptors, COAs, disclaimers | Reduces chargebacks |

| Banking | Segregated accounts & reserves | Mitigates acquirer exposure |

By adopting this structured model, CBD merchants demonstrate maturity, gain underwriter trust, and reduce reserve requirements over time.

The Offshore Advantage: How Global Structures Enable Legal Market Access

Why Offshore Structures Exist in the CBD and Cannabis Ecosystem

Even in 2025, most traditional payment institutions treat CBD and cannabis as unacceptable risk sectors. This is not purely because of product legality, it’s due to cross-border inconsistencies in compliance, especially in relation to AML, taxation, and banking transparency.

Offshore jurisdictions step into this gap, providing regulated, transparent pathways for compliant merchants to operate globally. These structures are not designed for secrecy, but rather for efficiency, financial access, and international trade flexibility.

Key benefits of offshore frameworks:

- Access to multi-currency payment processing (USD, EUR, GBP).

- Flexible acquirer partnerships for CBD and nutraceutical verticals.

- Clear AML/KYC expectations aligned with FATF guidelines.

- Simplified corporate structuring for global sales and supply chain management.

Offshore setups essentially serve as compliance bridges, allowing merchants to maintain legal operations while meeting local and card-scheme standards.

Leading Offshore Jurisdictions for CBD & Cannabis Payments

Each jurisdiction offers distinct advantages depending on your business model, target markets, and risk profile.

1. Malta: The EU-Integrated Model

- Strength: EU passporting, clear high-risk merchant licensing under PSD2.

- Why it works: Malta permits CBD products derived from hemp under 0.2% THC and enables licensed acquirers to onboard CBD merchants via EU SEPA channels.

- Compliance standards: AMLD6-aligned EDD, beneficial ownership disclosure, and regular reporting to the Financial Intelligence Analysis Unit (FIAU).

Ideal for: EU-based CBD eCommerce and nutraceutical brands.

2. Gibraltar: Multi-Vertical Friendly Gateway

- Regulator: Gibraltar Financial Services Commission (GFSC)

- Strength: Established frameworks for iGaming, fintech, and now CBD.

- Why it works: Gibraltar allows hybrid merchant licensing for industries that combine eCommerce and digital wallets, under a single regulatory perimeter.

- AML Requirements: FATF-standard KYC checks, biannual audits, and transaction monitoring through GFSC-approved PSPs.

Ideal for: CBD marketplaces, multi-brand platforms, or crypto-integrated payment flows.

3. Isle of Man – Low-Tax, High-Compliance Hub

- Strength: Tiered merchant licensing and financial privacy protections.

- Why it works: The IOM allows CBD merchants to operate under its “Wellness Product Framework,” provided full source documentation and non-THC certification are maintained.

- AML/KYC: 100% transparency for UBOs (Ultimate Beneficial Owners) and proof of legitimate trade activity.

Ideal for: B2B CBD exporters and multi-market merchants seeking low corporate tax (0-10%).

4. Curacao – Offshore Flexibility for Global Expansion

- Regulator: Central Bank of Curacao and Sint Maarten (CBCS)

- Strength: Easy international payment licensing and cross-border merchant integration.

- Why it works: Curacao allows non-THC CBD merchants to operate under general eCommerce licensing, supported by offshore acquiring networks connected to SEPA and SWIFT.

- AML/Compliance: Requires transaction logs, periodic reporting, and local representative presence.

Ideal for: LATAM and North American CBD operators seeking wider card acceptance and alternative payout rails.

Structuring Offshore Entities: The Compliance Model

Setting up offshore must never be confused with evading regulation. The goal is compliant accessibility, not avoidance.

The compliant offshore model includes:

| Layer | Compliance Component | Purpose |

| Legal | Parent entity in home jurisdiction; subsidiary offshore | Ensures traceable legal structure |

| AML | FATF-aligned AML/KYC policy | Meets acquirer expectations |

| Audit | Quarterly transaction reporting | Transparency to banks |

| Licensing | Valid trade licence or eCommerce permit | Regulatory legitimacy |

| Banking | Offshore IBAN & EMI partner | Enables global card acceptance |

By adhering to this structure, CBD companies can unlock payment rails across multiple continents without violating their home-market laws.

Best practice: Maintain a transparent corporate ownership tree and align accounting across both jurisdictions.

Offshore as an AML Shield, Not a Loophole

Regulators now view offshore processing as acceptable only when merchants demonstrate:

- Clear proof of legal product sourcing and composition (COA).

- Transaction traceability via banking logs.

- Open reporting of cross-border sales and remittances.

Offshore processors are obliged to report suspicious activity under FATF Recommendation 23, and many work directly with regulators such as the FIAU (Malta) or GFSC (Gibraltar) for AML oversight. Therefore, a transparent offshore setup actually enhances compliance posture, protecting both merchant and acquirer from inadvertent AML breaches.

The Role of Offshore Aggregators and Gateways

Modern offshore aggregators function as global payment intermediaries, providing end-to-end coverage, from merchant onboarding to settlement and FX management.

Key roles:

- Act as Master Merchants for multiple sub-merchants.

- Conduct KYC on behalf of acquirers.

- Handle card settlements, crypto conversions, and APM reconciliation.

- Provide compliance documentation for audit trails.

These aggregators must be licensed and FATF-compliant, ensuring funds flow only through verified accounts.

Payment Mentors’ Offshore Structuring Framework

At Payment Mentors, we’ve helped multiple CBD and cannabis operators gain sustainable offshore access by building multi-jurisdictional payment ecosystems.

Our framework includes:

- Jurisdiction analysis (EU vs. offshore) to match risk appetite.

- Acquirer mapping to connect with compliant processors.

- KYC & COA documentation readiness.

- AML audit preparation to pre-empt acquirer concerns.

Our philosophy is simple:

Offshore should mean more transparency, not less. When built correctly, offshore structures allow CBD businesses to operate globally while satisfying all AML, tax, and scheme-compliance requirements.

Summary

Offshore banking and acquiring for CBD isn’t a legal grey area, it’s a compliance-driven access layer.

Used correctly, it helps legitimate CBD and cannabis merchants:

- Access stable financial services.

- Maintain clear transaction reporting.

- Demonstrate regulatory responsibility.

- Expand into multi-region markets with reduced payment friction.

Conclusion

CBD and cannabis payment processing has evolved from a legal grey area into one of the most complex, risk-managed verticals in global fintech. Yet, for legitimate operators, the story isn’t about restriction, it’s about resilience.

Today, high-risk no longer means unbanked. It means regulated differently. Merchants who understand that distinction can turn compliance from a cost centre into a competitive advantage.

The Four Pillars of a Sustainable CBD Payment Ecosystem

Based on the insights explored in this guide, the merchants that succeed long-term build around these four interconnected pillars:

- Regulatory Literacy

Understand and track the evolving legal status of CBD and cannabis in every jurisdiction where you sell, from FSA (UK) to Health Canada, FDA (U.S.), EU Novel Foods, and AUSTRAC rules. Compliance begins with clarity. - Transparent Banking Partnerships

Whether operating with specialist domestic banks, EMIs, or offshore acquirers, full disclosure of product composition, supply chains, and ownership structure ensures financial continuity and regulatory confidence. - Fraud & AML Integration

Modern CBD payment ecosystems must embed real-time fraud analytics, chargeback defence, and AML monitoring directly into payment flows.

This isn’t only about preventing losses, it’s about proving to underwriters that your business is trustworthy and well-controlled.

As the global payment landscape shifts toward APMs and open banking, CBD merchants that diversify beyond cards (PIX, SEPA, Interac, or crypto gateways) reduce dependency and increase resilience.

FAQs

1. Why is CBD payment processing considered high risk?

CBD and cannabis payments are classed as high risk due to fragmented legality, inconsistent product regulation, and elevated chargeback rates. Financial institutions treat these merchants cautiously because CBD legality differs across countries and card schemes maintain strict underwriting standards for this vertical.

2. Is CBD legal to sell and process payments for in the UK?

Yes, but only under strict conditions. The UK’s Food Standards Agency (FSA) allows CBD products derived from industrial hemp containing less than 0.2% THC, and all ingestible products must appear on the FSA’s Novel Foods list. Merchants must maintain COAs (Certificates of Analysis) and compliant labelling to qualify for payment processing.

3. Why do traditional banks refuse CBD or cannabis merchants?

Most mainstream banks avoid CBD transactions because of reputational risk and cross-border compliance complexity. They rely on standardised industry codes (MCCs) that classify CBD alongside prohibited pharmaceuticals or controlled substances, triggering automatic declines.

4. How do offshore payment processors help CBD merchants?

Offshore payment providers in regulated jurisdictions such as Malta, Curacao, Gibraltar, and the Isle of Man allow CBD businesses to legally access global card networks while adhering to FATF-compliant AML and KYC frameworks. They act as compliance intermediaries, not loopholes.

5. What are the main types of fraud in the CBD sector?

CBD merchants face transaction fraud, synthetic identity fraud, chargeback abuse, and counterfeit product scams. Fraudsters exploit unclear labelling and high refund ratios. Merchants can mitigate this with device fingerprinting, velocity checks, and transparent refund and COA policies.

6. How can merchants lower chargeback ratios in CBD payments?

Transparency is key: clearly display COAs, provide accurate product descriptions, and use recognisable billing descriptors. Combining these with 3D Secure authentication and proactive customer support reduces chargebacks and acquirer risk classification.

7. What card network policies apply to CBD and cannabis sales?

Visa and Mastercard require CBD merchants to demonstrate legal sourcing, clear THC limits, and full compliance with regional regulations. Non-compliance can trigger fines or termination under the Visa Global Brand Risk Programme or Mastercard Integrity Framework.

8. Are CBD payments allowed on PayPal, Stripe, or Square?

Generally, no. These mainstream PSPs prohibit or heavily restrict CBD-related transactions under their Acceptable Use Policies. High-risk merchants should instead partner with specialist acquirers or offshore PSPs licensed for CBD verticals.

9. How do acquirers verify CBD merchants before approval?

Underwriters conduct Enhanced Due Diligence (EDD), including UBO verification, product testing documentation, merchant website review, and chargeback history analysis. They also assess supplier legitimacy and compliance with local labelling laws.

10. What role does AML compliance play in CBD payments?

AML monitoring ensures that CBD transactions are not used to disguise illicit transfers or laundering. Regulators like the FCA (UK) and FINTRAC (Canada) require ongoing monitoring of transaction flows, beneficiary verification, and suspicious activity reporting (SARs).

11. Can I process payments for both CBD and THC products together?

No. Merchants cannot process both under the same MID or account. THC remains a controlled substance in most jurisdictions, and acquirers segregate legal CBD from illicit cannabis to comply with AML and card network requirements.

12. How do offshore aggregators reduce risk for CBD operators?

They pool multiple compliant CBD merchants under a master licence and manage KYC, settlement, and risk controls on their behalf. This structure allows smaller merchants to gain access to global acquiring networks without breaching compliance thresholds.

13. What documentation is needed to open a CBD merchant account?

Typically required documents include:

- Certificate of Incorporation and business licence.

- COA and third-party lab results for all products.

- Proof of domain ownership.

- Processing history or projected turnover.

- UBO identification and bank statements.

14. Is offshore banking for CBD merchants legal?

Yes, provided the jurisdiction is FATF-compliant and the business maintains transparent reporting. Reputable offshore centres like Malta or the Isle of Man require full AML/KYC adherence and beneficial ownership disclosure to remain compliant.

15. How can Payment Mentors help my CBD business get approved for processing?

At Payment Mentors, we guide CBD and cannabis businesses through end-to-end onboarding, from legal structure and acquirer selection to AML documentation and fraud controls. Our expertise ensures faster approvals and sustainable, compliant access to global payment networks.