In 2025, one of the most pressing issues confronting iGaming operators across the UK and Europe isn’t player fraud or bonus abuse, it’s affiliate payouts. Once seen purely as a marketing expense, affiliate commissions have now become a critical focus area for regulators, auditors, and banking partners.

The UK Gambling Commission (UKGC), the Malta Gaming Authority (MGA), and even the Financial Intelligence Units (FIUs) in both jurisdictions have warned operators that unverified affiliate networks are a growing source of illicit fund flows. According to the UKGC’s compliance communications (SR Code 1.1.2 of the Licensing Conditions and Codes of Practice), gambling companies are fully responsible for any third-party affiliate who markets or earns commission under their brand. In effect, a poorly vetted affiliate can drag a licensed operator into AML or POCA violations, even when the operator has no direct intent to breach compliance.

- Designing AML-Aware Commission Models: How Payout Structures Create or Reduce Risk

- Vetting Affiliates: Building a Robust Enhanced Due Diligence (EDD) Framework

- Tax and Jurisdictional Issues: Managing Global Compliance for Affiliate Payouts

- Anatomy of Fraud in Affiliate Payouts

- Payout Governance & Controls (Finance + Risk)

- Creative & Media Compliance: What Must Be in the Contract

- Template Clauses (Operator-Affiliate Agreement)

- Building the Operating Model: People, Process, and Technology

- Conclusion

Designing AML-Aware Commission Models: How Payout Structures Create or Reduce Risk

In the high-risk iGaming ecosystem, the way affiliate commissions are structured can make the difference between compliance and catastrophe. While marketing teams see commissions as a tool for acquisition, underwriters and MLROs now view them as financial transactions subject to AML scrutiny.

The UKGC, MGA, and FIAU have each warned that poorly structured affiliate payment models, especially those without transparent metrics or staged validation, create perfect conditions for money laundering, tax evasion, and fraud layering.

Let’s explore how certain models heighten regulatory risk, and how operators can design AML-aware alternatives that stand up to audit.

The Core Problem: Incentive-Driven Laundering

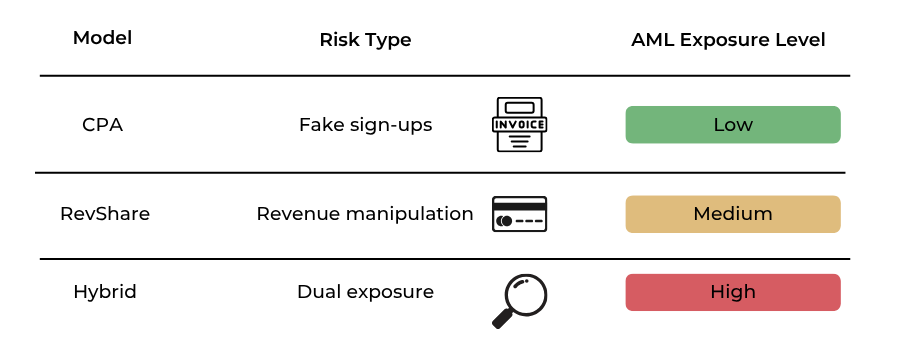

Most affiliate programmes still operate on one of three payout models, Cost Per Acquisition (CPA), Revenue Share, or Hybrid.

Each presents unique AML exposure points if not carefully governed:

| Model | Risk Type | AML Exposure |

| CPA (Cost Per Acquisition) | Affiliates receive a lump-sum payment for every new depositor. | Fake sign-ups or ghost accounts can be created to trigger payouts, providing a vehicle for cash extraction and circular fund movement. |

| Revenue Share (RevShare) | Affiliates receive a percentage of player net revenue over time. | Revenue manipulation (e.g., bonus recycling, synthetic wagering) can conceal source of funds and distort LTV data. |

| Hybrid | Combines CPA upfront + ongoing RevShare. | Harder to audit; creates dual risk channels and inflates payment complexity for AML monitoring. |

A 2024 study by the European Gaming & Betting Association (EGBA) found that over 22% of affiliate-driven player accounts in grey markets showed suspicious transaction patterns within 60 days of registration, including repeated deposits and withdrawals across linked devices. These statistics underline the necessity of integrating risk-based commission structures into affiliate contracts.

Step 1: Apply a Compliance-by-Design Approach to Commission Payouts

Traditional affiliate systems were built for growth, not compliance. To meet AML expectations in 2025, operators must adopt a compliance-by-design model, embedding checks, validations, and EDD triggers directly into the commission pipeline.

Key controls include:

- Deferred Commission Release: Don’t pay CPA immediately upon registration. Use a staged release system, paying only after:

- KYC verification of the player.

- Minimum wagering or activity threshold.

- No chargeback or refund activity in the first 30-60 days.

- Tiered Payout Approval: Require dual sign-off (Marketing + Compliance) for any affiliate payout exceeding a defined threshold (e.g., £10,000 or equivalent in euros).

- Rolling Reserve on Commissions: Similar to merchant reserves, hold back 10-20% of affiliate payouts for 90-180 days. This buffer protects against clawbacks from fraudulent traffic or post-payment AML findings.

- Transparency Rule: Each affiliate invoice must include verified bank account details (registered to the legal entity) and supporting transaction logs. Payments to personal or unverified third-party accounts should be strictly prohibited.

Step 2: Embed AML Controls into Affiliate Agreements

A well-structured affiliate contract isn’t just a commercial document, it’s an AML control framework.

Under UKGC LCCP 1.1.2, operators must ensure third-party affiliates comply with the same anti-money laundering, marketing, and data integrity standards as the licensee.

Essential clauses to include:

- UBO & KYB Disclosure: The affiliate must disclose all beneficial owners and directors, with updates required every 12 months.

- Bank Account Verification: Payouts only to verified accounts matching the affiliate’s KYB details.

- No Sub-Affiliate Payments Without Written Approval: Prevents unmonitored payout chains.

- Audit Rights: Operator reserves the right to review affiliate traffic data, invoices, and financial statements.

- Clawback & Suspension Clause: Allows operators to freeze or recall payments if AML anomalies or player fraud patterns are detected.

- Record-Keeping: Affiliates must maintain and provide data logs for a minimum of five years (aligned with POCA retention rules).

Including these clauses in every affiliate contract ensures operators can demonstrate reasonable steps during compliance inspections or regulatory audits.

Step 3: Link Commission Metrics to Verified Player Quality

In a compliant ecosystem, payout amounts should reflect verified value, not volume.

Here’s how to integrate measurable AML indicators into your commission logic:

- Active Player Rate (APR): Percentage of new sign-ups who complete full KYC and show genuine transactional activity.

- Chargeback Ratio (CBR): Affiliates exceeding 0.5-1% chargeback rates should be flagged for review.

- RG/AML Flag Ratio: If more than 3% of referred players are later self-excluded or reported under AML suspicion, freeze that affiliate’s commissions.

- Traffic Anomaly Index (TAI): Use device fingerprinting and IP clustering to flag suspicious acquisition spikes, especially before payout cycles.

By combining behavioural and transactional analytics, operators can identify whether affiliate earnings align with legitimate player activity.

Step 4: Audit-Ready Payout Documentation

Every affiliate payment must leave a traceable, reconcilable paper trail.

Regulators and auditors expect this trail to demonstrate transparency from referral to payment.

An audit-ready affiliate payout file should include:

- Affiliate’s full KYB/UBO verification results.

- Signed contract with AML clauses.

- Invoice with matching bank data and currency.

- Proof of underlying player acquisition metrics (KYC, deposits, wagers).

- Payment release approval log (dual sign-off).

When these elements are combined into one compliance folder, it satisfies both POCA audit standards (UK) and FIAU record-keeping obligations (Malta).

The Business Payoff: Risk-Weighted Efficiency

Building AML-aware commission structures isn’t just about avoiding fines, it’s about future-proofing your payment relationships.

Operators with clear, traceable payout governance find it easier to:

- Maintain banking and PSP relationships (lower de-risking pressure).

- Reduce fraud-induced losses.

- Pass regulatory inspections without remediation orders.

- Negotiate better terms with acquirers and investors who demand AML clarity.

By converting affiliate payout systems into compliance assets, iGaming operators can turn one of their biggest risk zones into a strategic advantage.

Vetting Affiliates: Building a Robust Enhanced Due Diligence (EDD) Framework

Affiliate partnerships remain one of the biggest grey areas in iGaming compliance. While affiliates can drive massive acquisition growth, they also represent a potential AML, reputational, and regulatory liability if not properly vetted.

Both the UK Gambling Commission (UKGC) and the Malta Gaming Authority (MGA) now explicitly state that gambling operators are legally accountable for the actions of their affiliates. This means that even a single non-compliant partner, such as one using illegal advertising, misrepresenting bonuses, or masking beneficial ownership, can jeopardise the operator’s entire licence.

At its core, vetting affiliates through Enhanced Due Diligence (EDD) is no longer optional; it’s a regulatory necessity.

Why Affiliate Vetting Is a Regulatory Priority

The 2024-25 surge in AML enforcement across the UK and EU followed a series of headline cases in which unverified affiliates were used to funnel illicit proceeds through commission payments.

For example:

- In 2024, the Financial Intelligence Analysis Unit (FIAU) in Malta fined a leading sportsbook €420,000 for failing to verify the beneficial ownership of six high-earning affiliates.

- The UKGC issued multiple warning notices to licensees that did not conduct sufficient checks to establish the legitimacy of affiliate partners or the provenance of affiliate traffic.

These examples underline a key regulatory view: affiliates are effectively financial counterparties, not marketing subcontractors. They fall under the same AML/KYC/KYB obligations as any other business relationship involving the movement of funds.

Core Pillars of a Strong EDD Framework for Affiliates

1. Know Your Business Partner (KYB) Verification

Before any payment is made, operators should confirm the affiliate’s legal and operational legitimacy through comprehensive KYB checks.

A compliant KYB pack should include:

- Company registration documents (Certificate of Incorporation, Articles of Association).

- UBO identification: listing all individuals holding ≥25 % ownership or control.

- Regulatory status: confirmation of licensing (if operating in a regulated market).

- Registered address validation: physical and digital address cross-verification.

- Bank account validation: ensuring payout accounts match the corporate entity.

Operators working with global affiliates should also perform sanctions and PEP screening against databases like OFAC, EU Consolidated List, and HMT Sanctions List.

2. Behavioural and Reputational Analysis

EDD extends beyond documentation, it’s about ongoing behaviour monitoring.

A robust compliance framework should include:

- Website & Content Audit: Review affiliate sites for false claims, underage-targeted promotions, or unapproved branding.

- Traffic Source Verification: Use analytics and tagging tools to confirm that affiliate traffic originates from approved jurisdictions (no grey-market targeting).

- Negative Media Screening: Monitor affiliates in international databases and news sources for fraud, insolvency, or data-breach incidents.

Payment Mentors recommends maintaining a Reputation Risk Register for affiliates, ranking each from Low to Critical risk with justification and audit notes.

3. Transaction-Level EDD on Payouts

Every affiliate commission should pass through transaction-specific EDD filters before approval:

- Threshold Alerts: Flag payouts above £10 000 or 10 % above historical average for manual review.

- Jurisdictional Cross-Checks: If the affiliate’s payout destination changes (from a UK account to one in Belize), freeze the transaction until documentation is re-verified.

This approach ensures each payment is linked to demonstrable economic activity, satisfying Proceeds of Crime Act (POCA 2002) expectations.

4. Ongoing Monitoring and Relationship Reviews

EDD isn’t a one-time process, it’s continuous. The MGA and UKGC expect periodic affiliate reviews at least annually, or sooner if risk factors change.

Operators should establish:

- Quarterly risk scoring based on chargeback ratios, player quality, and flagged AML alerts.

- Re-verification every 12 months of corporate registration and bank data.

- Affiliate off-boarding criteria (e.g., exceeding defined fraud thresholds or refusal to update KYB).

Automated compliance systems can integrate with CRM or affiliate-tracking tools to trigger review reminders and generate audit logs for regulators.

5. Cooperation with Financial Intelligence Units (FIUs)

Under AML regulations, gambling operators are reporting entities. If suspicious affiliate behaviour arises, unusual commission patterns, unexplained jurisdiction shifts, or inconsistent invoicing, operators must file Suspicious Activity Reports (SARs) to their local FIU:

- UK → National Crime Agency (NCA) under POCA.

- Malta → Financial Intelligence Analysis Unit (FIAU).

- LATAM → COAF (Brazil) or UIAF (Colombia) depending on the jurisdiction.

Failing to report such anomalies can trigger severe penalties, including personal accountability for MLROs and directors.

Tax and Jurisdictional Issues: Managing Global Compliance for Affiliate Payouts

As affiliate marketing in iGaming becomes more globalised, operators now face a new class of regulatory complexity, cross-border tax exposure and jurisdictional compliance.

When an operator in the UK or Malta pays an affiliate in another jurisdiction, such as Cyprus, Curacao, Brazil, or the UAE, that payout becomes a reportable financial transaction under multiple regulatory frameworks:

- AML/CFT laws (to trace illicit fund movement)

- tax transparency rules (under OECD CRS and FATCA)

This section explains how operators can structure affiliate payouts to remain compliant across tax zones, without triggering red flags from auditors, acquirers, or regulators.

1. The Core Challenge: Cross-Border Payout Visibility

Affiliate payments are often treated as marketing expenses, yet in the eyes of regulators, they represent cross-border financial transfers.

If not properly documented, these can appear as suspicious fund flows, especially when:

- The affiliate is based in an offshore jurisdiction

- The payment destination is different from the registered business country

- The amount exceeds local tax-reporting thresholds.

In 2025, the OECD Common Reporting Standard (CRS) and the EU’s DAC6 directive made it mandatory for financial institutions and payment service providers to report cross-border payments above specific thresholds, even for marketing or commission transactions.

For example:

- In the UK, HMRC requires operators to maintain affiliate payout ledgers for all non-resident partners, with documented UBO verification.

- In Malta, the FIAU’s Implementing Procedures Part II (Remote Gaming) classifies affiliate payments as business relationships subject to ongoing monitoring.

2. Regional Tax Compliance Differences

Understanding jurisdictional differences is crucial when paying affiliates globally.

| Region | Key Regulator / Tax Authority | Compliance Focus | Payout Implications |

| United Kingdom | HMRC / UKGC | VAT, AML under POCA, FATF alignment | Non-UK affiliates must submit W-8BEN-like declarations or face withholding tax. |

| Malta (EU) | MGA / FIAU / CFR | Corporate transparency, AML CFT | Requires proof of affiliate’s fiscal residence and VAT registration for cross-border payments. |

| Brazil (LATAM) | COAF / Receita Federal | FX reporting, AML under Law 9.613/98 | Payouts via PIX or SWIFT must include full beneficiary data; crypto payments scrutinised under COAF Circular 4.978. |

| UAE / Curacao (Offshore) | FSRA / CBA | AML source of funds | Offshore accounts trigger enhanced due diligence by European acquirers. |

| Australia / NZ | AUSTRAC / IRD | AML CTF Act, GST | Affiliate payouts above AUD 10,000 must be reported to AUSTRAC as cross-border transfers. |

| Canada | FINTRAC / CRA | Beneficial ownership reporting | Requires record-keeping of all affiliate payments exceeding CAD 10,000. |

| South Africa | FSCA / SARS / FIC | Cross-border reporting | All marketing-related payments abroad must include compliance justification. |

This demonstrates that affiliate payment obligations extend beyond gaming law, they now intersect tax reporting, AML tracing, and cross-border financial compliance.

3. Structuring Affiliate Payments for Tax Transparency

To ensure compliance while maintaining operational efficiency, operators should build a tax-transparent payout structure:

a. Declare All Affiliates as Service Providers

All affiliates should be treated as business-to-business (B2B) contractors.

This means collecting:

- Tax Identification Numbers (TINs) or equivalent (VAT ID, EIN).

- Country of Tax Residence Declaration.

- Signed affiliate agreements including payment jurisdiction clauses.

This approach aligns with OECD BEPS Action 13 and prevents affiliates from being misclassified as unregistered marketing agents.

b. Recordkeeping Under OECD CRS

Ensure your finance department reports affiliate payments to your PSP or bank with complete details:

- Affiliate’s legal name and jurisdiction.

- Bank name, SWIFT/BIC, and account country.

- Amount, currency, and nature of transaction (e.g., marketing commission).

Banks and PSPs will forward this data under CRS to local tax authorities, preventing non-disclosure risk during audits.

c. Avoid Tax Haven Triangulation

Regulators increasingly monitor payouts routed through tax-neutral hubs such as Cyprus, Mauritius, or the Isle of Man.

To reduce red flags:

- Match payout jurisdiction to the affiliate’s incorporation country.

- Prohibit inter-affiliate transfers unless justified with invoices and contracts.

- Maintain signed declarations confirming no tax evasion or UBO concealment.

4. Managing Crypto and Alternative Payment Risks

The rise of cryptocurrency affiliate payouts, especially in markets like LATAM and Eastern Europe, has drawn significant scrutiny from FIUs and banking partners.

Why Crypto Payments Raise Red Flags

- Anonymous UBOs: Many crypto wallets lack verified ownership.

- Cross-border volatility: Tokens can be easily converted offshore, complicating AML tracing.

- Regulatory inconsistency: While Malta and the UK have VASP licensing, other regions (e.g., Curacao) lack clear frameworks.

If affiliates request payments via stablecoins or crypto, operators should:

- Process through regulated VASPs only.

- Require on-chain KYT (Know Your Transaction) reports from the VASP.

- Apply transactional risk scoring (chain analytics, wallet clustering, and sanctions screening).

- Log and retain all blockchain transaction hashes for AML audit trails.

This mirrors the FATF Travel Rule standard implemented in the EU’s MiCA Regulation (effective 2024).

5. Reporting & Withholding Obligations

Depending on the affiliate’s jurisdiction, operators may have withholding tax duties.

For example:

- UK-based operators paying non-resident affiliates must withhold tax unless a double-tax treaty applies.

- Malta’s Cooperation with Other Jurisdictions on Tax Matters Act (2011) requires all cross-border B2B payments to include fiscal identification.

- Brazil’s COAF and Receita Federal mandate declaration of international service payments in the SISBACEN system.

Operators should coordinate with their tax advisors to determine:

- Applicable withholding rates.

- Exemption certificates (if a treaty applies).

- FX reporting or invoicing requirements.

6. Jurisdictional Payment Routing: Best-Practice Flow

To align with both AML and tax compliance, a recommended affiliate payout flow is:

- Affiliate Invoice Submitted → includes tax ID and jurisdiction declaration.

- Internal EDD Verification → finance + compliance approval based on KYB and AML results.

- Banking Review → payout made via SWIFT, SEPA, or PIX (no peer-to-peer or third-party accounts).

- Transaction Logging → PSP reports to CRS/FIU as applicable.

- Archive and Audit Trail → stored in affiliate compliance file for five years.

This ensures every payout is defensible in audits from regulators such as HMRC, FIAU, or COAF.

Cross-border affiliate payments in the iGaming sector are no longer simple marketing transactions, they are regulated financial transfers that require full tax transparency and AML alignment. Operators that align their payout structures with OECD CRS, UK HMRC, and local FIU requirements can safeguard both their revenue and their regulatory standing.

At Payment Mentors, we help iGaming operators design affiliate payout frameworks that satisfy compliance obligations across the UK, EU, LATAM, and offshore markets, ensuring transparency, traceability, and trust in every transaction.

Anatomy of Fraud in Affiliate Payouts

Affiliate marketing was once the backbone of player acquisition, but in today’s regulated environment, it has also become one of the most exploited financial channels for fraud and money laundering in iGaming. The UK Gambling Commission (UKGC), Malta Gaming Authority (MGA), and Financial Conduct Authority (FCA) now classify unverified or opaque affiliate payments as potential AML red flags, on par with suspicious player withdrawals or bonus abuse patterns.

In this section, we’ll unpack the most common fraud schemes that occur within affiliate payout ecosystems, the payment rails and data loopholes that enable them, and how regulators are responding with enforcement actions.

Classic Patterns of Affiliate Fraud

Affiliate fraud isn’t always about fake traffic or bot clicks, it often involves structurally sophisticated patterns designed to manipulate commission models, launder money, or distort revenue attribution. Below are the most common typologies seen by compliance teams across Europe and the UK.

1. CPA Abuse (Bot or Farmed Sign-Ups)

Under Cost-Per-Acquisition (CPA) models, fraudsters generate fake player accounts using bots, identity farms, or synthetic IDs to trigger CPA payouts.

- Typical signs: High signup volumes from a single IP range, minimal player engagement, or zero deposits after registration.

- Regulatory view: The UKGC classifies this as a false economic event, if an operator pays for it, it can be treated as a breach of AML due diligence and marketing integrity rules.

- Control: Introduce velocity filters, device fingerprinting, and mandatory deposit verification before CPA release.

2. RevShare Gaming (Bonus Abuse Cohorts)

Fraudsters use revenue-share schemes to funnel manipulated player losses or orchestrate fake activity within closed groups.

- Pattern: The affiliate collaborates with players to cycle deposits and withdrawals, generating artificial revenue flow.

- AML risk: This mimics layering, disguising illicit funds as legitimate gaming revenue.

- Control: Apply negative carryover and clawbacks for suspicious retention metrics (e.g., extremely high win/loss ratios or recycled transactions).

3. Hybrid Arbitrage and Sub-Affiliate Laundering

Many affiliate networks introduce multi-tier sub-affiliate structures, where each level can obfuscate fund origin.

- Tactic: Fraudsters insert shell sub-affiliates to split commissions, making tracing difficult.

- Example: £10,000 commission split across five sub-affiliates registered in different jurisdictions (Cyprus, Serbia, Curacao, etc.).

- Control: Maintain a Sub-Affiliate Register with verified KYB and tax data for every downstream partner.

4. Straw Affiliates and Shell Companies

Some operators unknowingly onboard affiliates that are fronts for insiders, former employees, blacklisted entities, or even previously banned partners.

- Risk: Enables internal collusion and misuse of player data.

- Control: Implement background screening for beneficial ownership and UBO linkage checks against internal HR and vendor databases.

Payment-Rail Risks: When Fraud Hides in Payout Channels

Affiliate fraud doesn’t stop at traffic; it extends to how commissions are paid out. Unscrutinised payment rails are fertile ground for AML and fraud breaches.

1. Faster Payments and Open Banking Payouts

Faster Payments and Open Banking APIs enable near-instant affiliate payments, but when used without proper confirmation of payee or account-matching verification, they become vectors for:

- Payouts to mismatched beneficiaries.

- Transfers to mule or synthetic accounts.

- Rapid pass-through transactions for laundering.

Control tip:

Use Open Banking verification or Pay.UK Confirmation of Payee system to validate every affiliate’s bank account holder name against the registered entity.

2. E-Wallet Daisy-Chains

Some affiliates request payment to digital wallets or alternative payment providers. Fraudsters use these layers to conceal true ownership or reroute funds offshore.

- Example: Operator pays to Skrill → immediately withdrawn to crypto wallet → converted to stablecoins.

- Regulatory context: FCA and UKGC expect operators to apply equivalent KYC/KYB obligations for all payment rails.

- Control: Prohibit payouts to unverified wallets or third-party processors not registered under FCA’s E-Money Regulations 2011.

3. Invoice Factoring of Commissions

An emerging AML risk involves affiliates selling their commission invoices to third-party financiers or factoring services.

- Impact: The affiliate’s payment now goes to an unknown counterparty.

- Control: Only approve invoice factoring if the financier passes full KYB/EDD checks and is disclosed contractually.

Data Manipulation & Attribution Fraud

Affiliate systems rely heavily on tracking data, cookies, UTMs, SDKs, and clickstreams, which can be falsified to hijack attribution.

1. Cookie Stuffing & Last-Click Hijacking

Fraudsters exploit tracking cookies to claim players they didn’t actually refer to.

- Outcome: Inflated commission payouts, data misalignment, and potential breach of GDPR data accuracy principles.

2. SDK Spoofing

Mobile app fraudsters spoof Software Development Kits (SDKs) to simulate genuine installs and conversions.

- Common in affiliate networks targeting UK and LATAM markets.

- Control: Use device fingerprinting and server-side conversion validation.

3. Player Value Manipulation

Affiliates may intentionally inflate lifetime value (LTV) data to prolong their RevShare eligibility.

- By recycling players through multiple accounts, they simulate ongoing engagement.

- Detection: Employ anomaly detection tools that cross-check deposits, logins, and session IPs.

Payout Governance & Controls (Finance + Risk)

While marketing teams often own affiliate relationships, it is the finance and risk departments that carry the real compliance liability. The UKGC, FCA, and HMRC have made it clear: if affiliate commissions become a vehicle for money laundering, it’s the licensee, not the affiliate, who faces regulatory consequences.

This section explains how operators can establish robust payout governance and financial controls, ensuring every commission payment is defensible under audit, traceable through banking logs, and compliant with both AML and data integrity regulations.

Payment Policy: Setting the Right Cadence and Control Points

One of the biggest weaknesses in affiliate programmes is undisciplined payout timing. Instant or same-day commissions create a high-risk environment where AML red flags may be missed.

Best-Practice Policy:

- Adopt Net-30 or Net-45 cycles: A 30-45 day cool-off period gives finance teams time to review player quality, chargeback ratios, and fraud alerts before releasing funds.

- Introduce a quality review window: Payouts should only be triggered after validating player activity, deposit legitimacy, and KYC completion.

- Reject same-day or first-cycle payouts: The UKGC advises that new affiliates be treated as probationary accounts for at least one full payout cycle before eligibility.

- Volume caps for new partners: Restrict total commissions (e.g., £5,000 cap) during the first 60 days of partnership. This aligns with proportional risk controls under POCA’s reasonable steps principle.

Segregated Payment Lanes: Keeping Affiliate Funds Firewalled

To reduce contamination risk, affiliate payments should never pass through general player wallet accounts or operational expense accounts.

Controls:

- Dedicated Affiliate Payout Account:

- Open a separate business bank account solely for affiliate payments.

- Enables full traceability for AML and POCA audits.

- Approval Matrix (Two-Person Rule):

- Minimum of two approvers (Finance + Risk/Compliance) required for every payout release.

- This ensures dual accountability for all commission disbursements.

- Geo-Specific Routing:

- Avoid cross-border transfers without verified tax documentation.

- For UK affiliates, use SEPA/Faster Payments; for EU partners, SEPA or IBAN transfers only.

- LATAM affiliates should receive payouts via regulated intermediaries with KYC controls (e.g., EBANX, PayRetailers).

Red-Flag Rules: When to Freeze or Delay Affiliate Payouts

An affiliate payout is not just a marketing transaction, it’s a potential STR (Suspicious Transaction Report) event. Operators should implement automated red-flag triggers that halt or escalate payments when anomalies appear.

Example Red-Flag Triggers:

| Red Flag | Possible Risk Type | Recommended Action |

| Affiliate requests payout >£10,000 in first month | Money Laundering / Front Company | Delay & escalate to MLRO |

| Payout account name ≠ Affiliate registered entity | Straw or third-party payout | Freeze payment; verify KYB |

| Sudden 300% traffic spike pre-payday | CPA Bot/Fraud Traffic | Manual review of attribution logs |

| Repeated failed payouts or bank rejections | Account substitution / sanctions | Cross-check via Open Banking |

| Affiliates with same IP as operator staff | Internal collusion | Escalate to Compliance Committee |

Every red flag should automatically create an internal alert record, logged within the affiliate management system and mirrored to the compliance audit trail.

Evidence Pack for SARs & Audit Defence

If an affiliate payout triggers suspicion, under the POCA and MLR regimes, operators are obligated to report a Suspicious Activity Report (SAR) to the UK Financial Intelligence Unit (FIU). To defend the business during an audit or enforcement case, every payout must be supported by a clear evidence trail.

Affiliate Payout Evidence Pack Checklist

- Attribution Logs: Player registration and deposit timestamps linked to affiliate ID.

- Traffic Quality Reports: Evidence of legitimate referral patterns and geo-source analysis.

- Communication Logs: Email chains, chat history, or CRM notes verifying affiliate discussions.

- Creative Approvals: Screenshots or signed confirmations that ad creatives were pre-approved under CAP/BCAP rules.

- KYB & Banking Verification: Copies of company certificates, UBO verification, and bank account proof.

- Transaction Ledger: Payout date, method, approver names, and compliance sign-off.

The Finance Department should work with the MLRO (Money Laundering Reporting Officer) to ensure SARs are filed before payout release if suspicion cannot be cleared.

Integrating AML Monitoring Tools

Leading iGaming operators now deploy payout-integrated monitoring tools that link affiliate systems with AML analytics.

Recommended Integrations:

- Transaction Screening APIs → Sanctions and PEP screening per payout (Dow Jones, ComplyAdvantage).

- Payment Verification Tools → Name match via Open Banking Confirmation of Payee.

- Fraud Analytics Platforms → Detect high-risk payout clusters or repeat beneficiaries.

- Case Management Systems → Automatically tag flagged payouts to compliance dashboards for investigation.

Outcome: These integrations convert affiliate management systems into auditable, regulated financial environments, aligning with the UKGC’s 2025 compliance focus on supply-chain payment transparency.

Record Retention & Audit Trail

Under both LCCP 15.2.1 (Reporting Requirements) and POCA Section 330, affiliate payment data must be retained for at least five years after termination of the partnership.

Operators should maintain:

- KYB and tax records.

- Invoices and payment confirmations.

- SAR or internal escalation logs.

- Annual reconciliation summaries.

These records must be readily accessible to auditors, regulators, and acquirers, particularly during periodic AML audits or licence renewals.

Creative & Media Compliance: What Must Be in the Contract

Affiliate marketing isn’t just about referral traffic, it’s a compliance liability. The UK Gambling Commission (UKGC), Advertising Standards Authority (ASA), and Committees of Advertising Practice (CAP/BCAP) hold licensed operators jointly responsible for all third-party advertising, even if the affiliate acts independently.

Under LCCP SR Code 1.1.2, every affiliate or third-party marketing partner must be treated as if bound by the operator’s own licence conditions. That means every claim, creative, or social media promotion is effectively a regulated communication, and a single misleading ad can trigger operator fines or licence suspension.

This section defines what affiliate contracts must include, how operators can design media-compliance workflows, and how to stay audit-ready under ASA and UKGC oversight.

CAP/BCAP Must-Haves: Non-Negotiable Advertising Rules

1. Age Targeting & Protection of Vulnerable Audiences

Advertising for gambling must not be directed at individuals under 18, or anyone self-excluded or identified as at-risk.

- Rule: Ads must not appear on youth-oriented platforms (e.g., TikTok, Snapchat) or next to underage content.

- Mandatory Safeguards:

- Content keyword exclusions (e.g., school, student, teen).

- Verified influencer lists only.

Example: ASA upheld a complaint in 2024 against an iGaming affiliate for promoting free spins in a YouTube stream where >20% of viewers were under 18. The operator, not the affiliate, was fined £145,000 for failure to control targeting.

2. Misleading or Exaggerated Claims

Affiliates often use sensational copy, risk-free bets, guaranteed wins, no losses.

Under CAP Code rules 3.1-3.3, such language constitutes misrepresentation unless backed by verifiable data.

Contractual Clause:

Affiliates must not use statements suggesting certainty of financial gain or risk-free play. All bonus offers must clearly display wagering and withdrawal conditions.

Best Practice:

- Require pre-approval of all bonus creatives.

- Maintain an internal Bonus Disclosure Register linking ad creatives to live terms.

3. Mandatory Disclaimers & Transparency

All affiliate creatives must include:

- Age warning: 18+ | BeGambleAware.org.

- Financial responsibility notice: Please play responsibly.

Failure to include these disclosures in all placements (web, app, or influencer post) breaches BCAP 17.4.5 and ASA CAP 16.3.14.

Example: A 2023 ASA investigation found an operator’s banner ad omitted 18+ on mobile view; the affiliate’s contract did not require responsive design testing, resulting in shared liability.

4. No Financial Distress or Misleading Value Claims

CAP Code 16.3.6 bans ads that exploit financial pressure or imply gambling is a solution to debt.

Forbidden Phrases:

- Boost your income.

- Pay your bills by betting smarter.

- Turn your luck into cash.

Operators must monitor affiliate sites and influencers regularly for non-compliant content.

Control Tip:

Implement a creative crawler (automated web scanner) to flag such phrases across live campaigns.

Platform-Specific Clauses: Tailoring Rules to the Medium

Each platform introduces unique compliance risks: your affiliate contract should address all.

1. Search & Display (Google Ads, Bing, etc.)

- Restrict brand bidding on operator trademarks.

- Prohibit paid search ads that mimic operator domains.

- Require negative keyword lists to exclude underage or vulnerable demographics.

2. Social Media (Meta, X, TikTok)

- Enforce influencer compliance: each post must include #ad or #sponsored per ASA influencer guidelines.

- Require influencer age verification and audience demographic proof before campaign approval.

3. Streaming & Podcast Platforms (Twitch, YouTube, Spotify)

- Prohibit co-promotion of gambling with alcohol or crypto speculation on the same stream.

- Require 30-second minimum responsible gambling disclaimer in every video description.

- Maintain time-stamped proof of inclusion for audits.

Audit & Whistleblowing Mechanisms

1. Randomised Creative Sampling

Operators should conduct quarterly creative sampling, reviewing at least 10% of all affiliate ad placements.

This audit ensures compliance with:

- CAP/BCAP content rules.

- UKGC LCCP SR 1.1.2 accountability clauses.

2. Breach Escalation Ladder

A structured process must exist for handling non-compliance:

- Stage 1: Warning notice and 48-hour takedown requirement.

- Stage 2: Temporary suspension of commissions.

- Stage 3: Termination and report to regulator (if breach suggests AML/POCA link).

3. Whistleblower Reporting

Affiliate managers and marketing staff should have a protected disclosure route to report suspected manipulation, fake traffic, or prohibited creatives. This aligns with the UKGC’s expectation of internal transparency and accountability under Licence Condition 15.2.1.

Creative compliance is not marketing hygiene, it’s a legal obligation.

Operators that fail to control affiliate creatives face:

- Regulatory fines (under CAP/BCAP).

- Licence suspension (under LCCP 1.1.2).

- Brand damage through media exposure.

Embedding these advertising standards directly into affiliate contracts and workflows is the only way to maintain compliance integrity and build regulator trust.

Template Clauses (Operator-Affiliate Agreement)

Once the creative and payout controls are defined, the next layer of defence lies in the affiliate contract itself.

The UK Gambling Commission (UKGC), Malta Gaming Authority (MGA), and EU AML directives expect operators to have legally binding contracts that explicitly extend compliance, AML, and advertising obligations to every affiliate and sub-affiliate.

This section provides model clauses that can be adapted by in-house legal teams or inserted into affiliate T&Cs to strengthen governance and withstand regulator audits or enforcement.

1. Responsibility for Third Parties (LCCP Mirror Clause)

Purpose: To comply with LCCP SR Code 1.1.2, which makes the operator accountable for the actions of its affiliates as if they were bound by licence conditions.

Clause Example: The Affiliate acknowledges and agrees that it shall conduct all marketing and promotional activity in full compliance with the Licence Conditions and Codes of Practice (LCCP) issued by the UK Gambling Commission, as if the Affiliate itself were a licensed operator.

The Operator shall have the right to audit, suspend, or terminate this Agreement immediately if the Affiliate fails to comply with the LCCP, the UK Code of Non-broadcast Advertising (CAP Code), or any applicable anti-money laundering (AML) regulation.

2. Data & Reporting (Transparency and Auditability)

Purpose: To establish data-sharing standards between the operator and the affiliate for AML, player attribution, and payment verification.

Clause Example: The Affiliate shall maintain accurate, time-stamped records of all referred traffic, player registrations, and associated marketing activity.

Upon written request, the Affiliate shall provide the Operator with raw data logs including IP addresses, referral timestamps, clickstream data, and device identifiers for compliance audit purposes.

The Affiliate agrees that failure to supply data or provide audit access within 10 business days of request constitutes a material breach.

3. Payment Terms (Holds, Reserves, and Clawbacks)

Purpose: To ensure all commission payments align with AML and fraud risk controls.

Clause Example: Affiliate commission payments shall be made on a Net-45 basis, subject to satisfactory fraud and player quality reviews.

The Operator may apply a rolling reserve of up to 10% of commission value for up to 180 days to mitigate the risk of fraud, chargebacks, or regulatory fines.

The Operator reserves the right to withhold or claw back payments if referred players are later found to have engaged in bonus abuse, money laundering, or responsible gaming violations.

4. Prohibited Conduct (Marketing & Operational Restrictions)

Purpose: To define clear boundaries for affiliate behaviour in advertising, targeting, and communications.

Clause Example:

The Affiliate shall not:

- Target individuals under 18 years of age or self-excluded persons.

- Use misleading language such as risk-free, guaranteed wins, or easy profit.

- Conduct paid search using the Operator’s trademark or domain name.

- Offer bonuses, free spins, or incentives not pre-approved by the Operator.

- Promote gambling content alongside alcohol, financial trading, or crypto-investment promotions.

Control Mechanism: Include a takedown SLA (Service Level Agreement) requiring removal of infringing materials within 24 hours of written notice.

5. Sanctions & AML Warranties

Purpose: To protect the operator from indirect exposure to sanctioned entities or illicit flows.

Clause Example: The Affiliate warrants that neither it, its directors, nor its Ultimate Beneficial Owners (UBOs) are listed on any UK, EU, or OFAC sanctions list.

The Affiliate agrees to undergo periodic AML and sanctions screening conducted by the Operator or its authorised third parties.

The Operator reserves the right to immediately suspend payments and terminate this Agreement upon detection of a sanctions or AML breach.

6. Inspection, Audit Rights & Record Retention

Purpose: To ensure the operator’s right to inspect records and meet AML audit standards.

Clause Example: The Operator shall have the right to conduct audits, inspections, and compliance reviews of the Affiliate’s operations, systems, and records upon reasonable notice.

The Affiliate agrees to maintain all relevant marketing, payment, and KYC/KYB documentation for a minimum of five (5) years following the termination of this Agreement.

Failure to comply with an audit request or to provide accurate information shall constitute a material breach, subject to termination and regulatory disclosure.

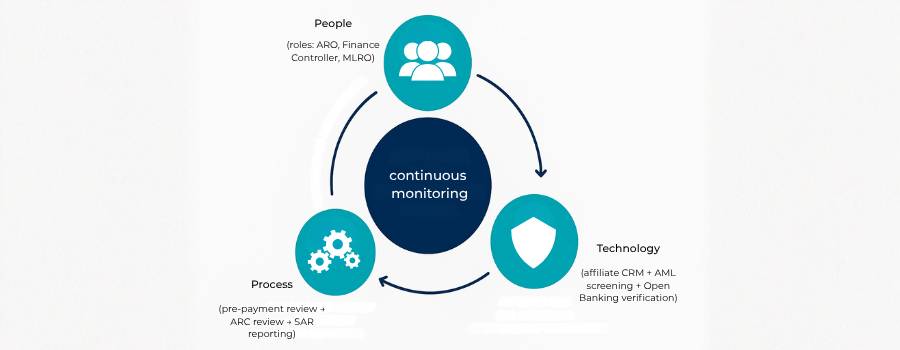

Building the Operating Model: People, Process, and Technology

Having the right clauses and controls on paper is not enough, regulators like the UKGC, FCA, and HMRC now expect licensees to operationalise their risk management. In practice, this means having clearly defined roles, documented workflows, and auditable systems for tracking every affiliate, creative, and payout.

This section explains how to design a functional Affiliate Risk Governance Model, showing how people, processes, and technology must integrate to prevent AML failures, fraud, and reputational damage.

People: Assigning Accountability and Oversight

Affiliate oversight isn’t just a marketing function, it’s a cross-departmental compliance task. Under the UKGC’s Licence Condition 12 (Prevention of Money Laundering and Terrorist Financing) and POCA 2002, each affiliate payment could be a transaction subject to financial crime scrutiny.

To meet these standards, operators must define clear RACI (Responsible, Accountable, Consulted, Informed) roles:

| Role | Core Responsibilities | Reports To |

| Affiliate Risk Owner (ARO) | Manages onboarding, due diligence (KYB), affiliate audits, and red-flag reviews. | MLRO / Compliance Director |

| Finance Controller | Executes payouts, maintains reserve holds, validates bank details, and logs transaction approvals. | CFO |

| Marketing Manager | Ensures creatives meet CAP/BCAP standards, approves campaigns, and coordinates pre-approval workflows. | Head of Marketing |

| Legal & Compliance Officer | Reviews contracts, ensures AML clauses are enforceable, and manages data-sharing compliance. | Chief Legal Officer |

| MLRO (Money Laundering Reporting Officer) | Reviews suspicious affiliate payouts, escalates SARs, liaises with NCA/FIU. | Board / UKGC Key Contact |

| Audit & Internal Controls Lead | Conducts quarterly affiliate compliance audits and ensures LCCP reporting alignment. | Audit Committee |

Best Practice: Establish a dedicated Affiliate Risk Committee (ARC) that meets monthly to review high-risk affiliate relationships, suspicious payout alerts, and audit results.

Process: Embedding Compliance into Daily Operations

To build resilience, affiliate governance must be process-driven, not ad hoc. Each payout, partnership, or creative approval should pass through a standardised compliance workflow.

1. Pre-Payment Review Checklist

Before every payout, Finance and Risk teams must confirm:

- KYB and UBO details verified in the last 90 days.

- Affiliate’s domain, traffic sources, and creatives remain approved.

- No red flags from monitoring tools (traffic spikes, mismatched bank names).

- Payment account matches the verified entity (Open Banking confirmation).

- Tax information is current (VAT/TIN number validated).

- Payout amount aligns with historical commission averages (variance threshold ±20%).

2. Monthly Affiliate Risk Committee Workflow

- Review new affiliates onboarded in the last 30 days.

- Examine risk-scored payouts (those flagged by transaction monitoring).

- Check AML compliance logs (SARs filed, reviews pending).

- Summarise compliance findings for internal reporting to the MLRO and board.

- Recommend sanctions or offboarding of non-compliant affiliates.

3. Incident Runbook for Red Flags

If suspicious activity arises, e.g., affiliate requests payout to a new beneficiary, the workflow must follow a documented escalation protocol:

- Step 1: Freeze payout.

- Step 2: Alert Affiliate Risk Owner & MLRO.

- Step 3: Conduct immediate document re-verification.

- Step 4: File internal Suspicious Activity Note (SAN).

- Step 5: If suspicion remains, submit SAR to the NCA before releasing funds.

This structure ensures that affiliate payout compliance mirrors AML escalation procedures applied to player transactions.

Technology: Integrating Risk Detection and Audit Automation

The affiliate ecosystem produces thousands of data points, clicks, conversions, payouts, invoices. Without automation, these signals become impossible to track manually.

A tech-driven compliance model integrates data monitoring, document management, and AML tools directly into the affiliate management platform.

1. Core Technology Stack for Affiliate Governance

| Function | Tool Type | Examples / Features |

| Affiliate CRM / Platform | Central hub for tracking traffic, commissions, and creatives. | Income Access, MyAffiliates, Impact.com |

| KYB / Sanctions Screening | Automates identity and UBO verification. | ComplyAdvantage, SumSub, Dow Jones Risk & Compliance |

| Payment Verification | Confirms beneficiary legitimacy. | Open Banking APIs, Confirmation of Payee |

| Fraud & Traffic Analytics | Detects fake sign-ups, bot clicks, CPA manipulation. | SEON, TrafficGuard, FraudScore |

| Creative Monitoring | Auto-scans web and social content for CAP/BCAP breaches. | AdVerif.ai, BrandVerity |

| Case Management / SAR Filing | Tracks investigations and regulator reports. | Lucinity, Salv, AMLHub |

Tech Compliance Tip: Integrate your affiliate CRM with transaction monitoring tools used for player AML review. That way, suspicious player traffic from affiliates can be traced upstream, connecting fraud patterns directly to payout risk.

2. Audit Logs & Data Retention

- Maintain a central repository of all affiliate data (contracts, KYB records, payment logs).

- Enable immutable audit trails to track when data was accessed, changed, or approved.

- Store audit logs securely for a minimum five years, per POCA 2002 and UKGC LCCP 15.2.1.

Cross-Department Coordination: Eliminating Silos

Affiliate risk cannot live in isolation. Finance, Marketing, and Compliance must operate as a single governance chain.

To formalise collaboration:

- Implement a joint sign-off policy for high-value payouts.

- Schedule quarterly joint training for affiliate managers on AML and advertising rules.

This integrated model creates what regulators call a culture of compliance.

Conclusion

In today’s UK-regulated iGaming environment, affiliate marketing is both a growth engine and a compliance trap. The Affiliate Payout Crisis has shown that when operators chase volume without oversight, they risk not only losing profits to fraud but also breaching AML and regulatory obligations under LCCP, POCA, and UK sanctions law.However, the case studies and controls outlined throughout this guide prove one thing clearly: payout integrity can be your competitive advantage.

1. What is the affiliate payout crisis in UK iGaming?

The affiliate payout crisis refers to rising incidents of fraud and AML breaches linked to unverified or fake affiliate partners in the UK gambling sector. Unchecked commission structures and weak KYB processes have allowed bad actors to launder funds or manipulate traffic metrics, leading to UKGC investigations and heavy operator fines.

2. Why are affiliate payments considered high-risk from an AML perspective?

Affiliate payouts are treated as third-party financial transfers. If an affiliate’s identity or bank account isn’t verified, these payments could be used to disguise illicit funds, similar to layering in money laundering schemes. Under POCA 2002, operators are legally responsible for identifying and reporting such risks.

3. What is LCCP SR Code 1.1.2, and why does it matter for affiliate programmes?

The Licence Conditions and Codes of Practice (LCCP) SR Code 1.1.2 makes operators responsible for all third-party partners, including affiliates , as if bound by the LCCP. This means any affiliate breach (e.g., non-compliant ad or fraudulent payout) is treated as the operator’s failure under UKGC rules.

4. What are the most common types of affiliate fraud in iGaming?

- CPA abuse: fake or bot sign-ups created to trigger commissions.

- RevShare manipulation: inflated player activity or bonus abuse cohorts.

- Hybrid arbitrage: combining CPA and RevShare to exploit payout timing.

- Sub-affiliate laundering: hidden affiliate layers masking the real payee.

5. How do AML and POCA regulations apply to affiliate payments?

Under POCA (Proceeds of Crime Act 2002), any financial transaction that could involve illicit funds must be monitored and, if suspicious, reported through a Suspicious Activity Report (SAR) to the National Crime Agency (NCA). This includes affiliate commissions that appear inconsistent, unverifiable, or unusually large.

6. What are KYB and KYC in affiliate vetting?

KYB (Know Your Business) verifies the affiliate company’s legal registration, ownership (UBO), and business model. KYC (Know Your Customer) applies to individuals receiving payments, ensuring they’re legitimate and not on sanctions lists. Operators must apply both processes to affiliates to prevent fraud and AML exposure.

7. How should iGaming operators structure affiliate commissions safely?

Safe commission design involves:

- Tiered verification: higher commissions only for fully verified affiliates.

- Rolling reserves: holding 10-15% of payouts for 30-60 days to detect fraud.

- Quality gates: release commissions only after player activity meets AML and responsible gaming thresholds.

8. What tools can help detect affiliate payout fraud?

Operators use technologies such as:

- ComplyAdvantage / SumSub for KYB & sanctions screening.

- SEON or FraudScore for device fingerprinting and traffic validation.

- Open Banking APIs for beneficiary verification.

These tools reduce manual review time and ensure audit-proof compliance.

9. How does the UKGC view affiliate programme responsibility?

The UKGC holds licensees fully responsible for all affiliate activities under third-party accountability. Even if the affiliate operates independently, the operator is liable for their conduct, including advertising, payouts, and AML breaches.

10. What red flags should trigger an affiliate payout freeze?

- Affiliate requesting payouts to a new or mismatched account.

- Rapid increase in CPA conversions from a new domain.

- Affiliates unwilling to share UBO details.

- Player traffic showing identical device or IP patterns.

- Payout request immediately after large bonus campaigns.

11. How do affiliate contracts support AML compliance?

Affiliate contracts should include clauses for:

- Right to audit affiliate traffic and data.

- Immediate termination for AML or ad breaches.

- Rolling reserves and clawbacks for fraudulent commissions.

- Data retention and recordkeeping aligned with POCA and LCCP.

12. What’s the difference between CPA and RevShare models from a risk perspective?

- CPA (Cost Per Acquisition): high front-loaded risk, fraudsters can trigger payouts without sustainable player activity.

- RevShare: lower immediate fraud risk but vulnerable to data manipulation and bonus abuse.

- Hybrid models blend both and require strict monitoring to balance incentive and fraud control.

13. How often should affiliates be re-screened for compliance?

Best practice is quarterly re-screening (every 90 days) of all affiliates and their payment accounts. This ensures ongoing compliance with UK sanctions, FATF updates, and POCA obligations. Automated monitoring tools should flag affiliates with changing ownership or domain details.

14. What are the consequences of non-compliance in affiliate payouts?

Penalties include:

- Regulatory fines from the UKGC (ranging from £200k-£10m).

- Licence suspension or revocation.

- Banking relationship termination.

- Reputational loss among affiliates, investors, and players.

Example: In 2023, a UK iGaming operator was fined £350,000 for failing to verify affiliate beneficiaries and report suspicious payouts.

15. How can affiliate payout integrity become a business advantage?

When operators implement robust compliance, KYB, reserves, AML screening, and clear payment policies, they gain trust from banks, regulators, and reputable affiliates. This creates a transparent ecosystem that attracts higher-quality partners, cleaner traffic, and long-term revenue stability.