In the fast-evolving world of payments, high-risk merchants face a financial challenge beyond simple transaction approvals: the true cost of processing each payment. Behind every authorised sale lies a complex stack of fees, interchange, scheme costs, acquirer mark-ups, and often, hidden operational charges.

In 2026, these costs are more visible than ever. The new EU Payment Services Regulation (PSR) and upcoming PSD3 framework are reshaping how acquiring banks and processors structure their pricing. Meanwhile, acquirers across regions such as the UK, LATAM, the Middle East, and Africa have tightened their risk models. The result? High-risk businesses are paying anywhere from 2.5% to 6.5% per transaction, compared to 1-2% for low-risk merchants.

For industries like iGaming, adult content, CBD, forex, and digital subscriptions, these pricing uplifts can directly hit profit margins. But the truth is, not every cost is fixed.

Up to 40% of a high-risk Merchant Discount Rate (MDR) is negotiable if you understand where the leverage lies.

This guide by the Payment Mentors team breaks down every layer of high-risk pricing, from interchange and basis points to scheme fees and rolling reserves. We’ll uncover:

- Which pricing components are truly negotiable?

- Practical, region-specific strategies to reduce your effective MDR in 2026 without harming approval rates.

At Payment Mentors, we specialise in helping regulated and high-risk merchants navigate these complexities. Whether you operate across Europe, the UAE, or LATAM, understanding your pricing anatomy is the first step toward cutting costs and staying fully compliant.

- The Anatomy of the Merchant Discount Rate (MDR): What You’re Really Paying For

- Understanding Interchange in a High-Risk Context

- Why Geography Matters in High-Risk Payment Pricing

- The Hidden Cost Layer Most High-Risk Merchants Miss

- The 2026 Playbook: Cutting Costs Without Cutting Corners

- From Audit to Action: Turning Insights into Savings

- Making Sense of the Cost Maze

- Final Words

- FAQs

The Anatomy of the Merchant Discount Rate (MDR): What You’re Really Paying For

For most high-risk businesses, the Merchant Discount Rate (MDR) appears on the invoice as a single line item, perhaps 3.9% + 25p per transaction.

However, this number hides an entire ecosystem of participants, rules, and risk premiums. Each percentage point is split between several entities, including the card issuer, card network, and acquiring bank, as well as technology and compliance providers.

To gain control over processing costs, merchants need to understand exactly how that number is built, and more importantly, which parts are fixed by regulation and which can be optimized.

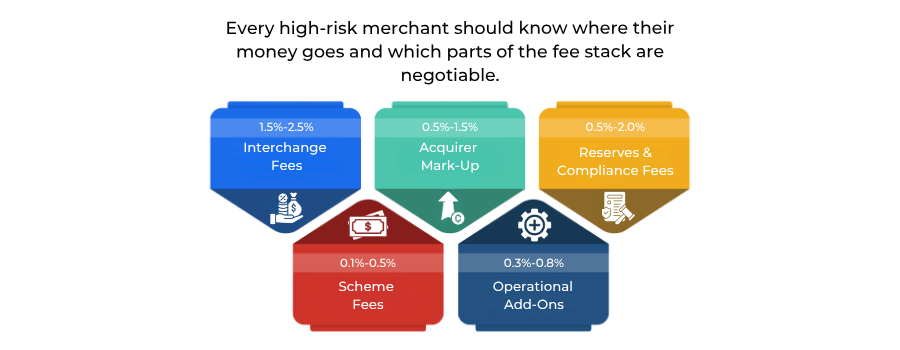

At Payment Mentors, we refer to this as the Payment Pricing Stack. It’s made up of five layers:

- Interchange Fees: paid to the issuing bank

- Scheme Fees: paid to the card network (Visa, Mastercard, etc.)

- Acquirer Mark-Up: paid to your acquiring or processing partner

- Reserves & Liquidity Costs: cash flow withheld as risk cover

Understanding this anatomy allows businesses to know where the negotiation levers exist and where regulation fixes the price floor.

1. Interchange Fees: The Core Cost Set by Card Issuers

What it is: The interchange fee is the amount the acquiring bank must pay to the issuing bank for every transaction. It covers costs like liquidity, fraud protection, and cardholder benefits (such as cashback or rewards).

Regulation in 2026:

Under the EU Interchange Fee Regulation (Regulation (EU) 2015/751), consumer card interchange is capped at:

- 0.2% for debit cards

- 0.3% for credit cards

These caps apply across the EU and UK, but there are critical exceptions:

- Commercial and corporate cards are not capped.

- Cross-border transactions (e.g. a UK merchant processing a German card) may attract higher interchange, often 1.6%-2.2%

- High-risk MCCs (Merchant Category Codes), such as 7995 (iGaming) or 5967 (Adult Services), are priced above standard consumer segments due to elevated chargeback rates and compliance oversight.

Why it matters:

While you cannot negotiate interchange directly (it’s set by network rules and regulators), you can influence which rate applies through:

- Improved authentication (SCA, 3D Secure 2.2)

- Reducing fraud and chargeback ratios

- Routing to domestic acquirers where caps apply.

2. Scheme Fees: The Network’s Infrastructure Charge

What they are:

Scheme fees are the costs charged by the card networks, such as Visa, Mastercard, or American Express, for using their infrastructure. These fees help fund the global authorisation network, fraud detection systems, and brand management.

Typical components include:

- Assessment or brand fees (percentage-based)

- Cross-border or currency-conversion fees

- Compliance and data integrity charges.

These fees typically range from 0.05% to 0.15%, plus a small fixed fee (usually £0.02-£0.10 per transaction).

Are they negotiable?

No, scheme fees are fixed by the card networks and passed directly to the acquirer. However, merchants can lower exposure by:

- Routing transactions through domestic instead of international networks

- Using network tokenization (reduces per-transaction security costs)

3. Acquirer Mark-Up: The Negotiable Profit Layer

This is the acquirer or processor’s margin, often expressed in basis points (bps) plus a per-transaction charge.

Example: If your contract reads 280 bps + £0.15 per transaction, then on a £100 sale, you pay £2.80 + £0.15 = £2.95 to your acquiring partner.

Why it varies:

- Merchant Category Code (MCC) and industry risk rating

- Transaction volume and average ticket size

- Jurisdiction of merchant incorporation (e.g. EU vs offshore)

- Historical chargeback and dispute ratios

- Settlement currency and preferred payout terms.

High-risk acquirer mark-ups can vary from 1.5% to 3.5%, sometimes even higher for industries such as crypto or adult content.

Negotiation strategy:

At Payment Mentors, we advise reviewing your pricing every 6-9 months. Once your operational KPIs improve (chargebacks under 0.9%, 3D Secure adoption, compliance certifications), you can request a mark-up reclassification. Many acquirers offer step-down tiers for proven risk improvements.

4. Operational Add-Ons: The Silent Cost Multipliers

Beyond the primary three layers, many merchants face additional charges that are technically outside the MDR but still inflate the total cost of acceptance. These include:

| Fee Type | Description | Typical Range (2026) | How to Manage |

|---|---|---|---|

| FX Conversion Fee | Applied when payout or settlement occurs in a different currency | 0.25%-1.00% | Use local settlement accounts or multi-currency wallets |

| Gateway/Orchestration Fee | Paid to the technology provider for transaction routing | £0.03-£0.10 | Bundle under one PSP or move to usage-based pricing |

| Rolling Reserve | 5-10% of volume held for 180 days as risk collateral | Variable | Negotiate release schedule (e.g., 90/120/180-day stagger) |

| Chargeback Handling Fee | Flat fee per dispute | £15-£30 | Deploy alert systems like Ethoca or Verifi to prevent disputes |

Each of these components can add 0.3%-0.7% to your effective rate, often unnoticed because they appear under separate billing categories.

5. Compliance & Monitoring Fees: The Overlooked Category

Many acquirers and PSPs now include compliance-related surcharges for high-risk merchants. Examples include:

- PCI DSS Non-Validation Fee: charged if you fail to file annual security questionnaires.

- Chargeback Monitoring Fee: applied if the monthly ratio exceeds card network thresholds

- AML/KYC Review Fees: levied for additional screening during onboarding renewals.

These are avoidable with proactive compliance. Maintaining PCI DSS validation, implementing 3D Secure 2.2, and meeting chargeback targets not only prevent penalties, they also improve your acquirer risk score, leading to potential fee discounts in future reviews.

6. What’s Fixed vs What’s Flexible

| Fee Component | Who Controls It | Payment Mentors Recommendation |

| Interchange | Card issuer (regulated) | Optimise authentication and card mix |

| Scheme Fees | Card network (Visa, Mastercard, etc.) | Focus on domestic routing and data accuracy |

| Acquirer Mark-Up | PSP / Acquirer | Negotiate quarterly, based on KPIs |

| Gateway / Tech Fees | Vendor | Bundle or rebid annually |

| Rolling Reserve | Acquirer | Step-down based on dispute ratios |

| Compliance Fees | Acquirer / Regulator | Stay audit-ready and maintain certifications |

The reality is that only one-third of your MDR is truly fixed by regulation or network policy. The rest, acquirer margins, reserves, gateway costs, and compliance fees, are negotiable or performance-dependent.

Businesses that analyse their fee statements monthly and benchmark against market rates typically achieve 15-25% lower total processing costs over 12 months.

At Payment Mentors, we help clients translate technical pricing reports into actionable strategy, giving CFOs clear visibility into their true cost of acceptance and where savings can be achieved without jeopardising approval rates.

Understanding Interchange in a High-Risk Context

Every time a card transaction is authorised, the card-issuing bank collects an interchange fee from the acquirer. For high-risk businesses, online casinos, adult platforms, forex brokers, nutraceuticals, or CBD retailers, this fee is usually higher than for ordinary e-commerce merchants.

That difference arises because issuers factor in fraud probability, dispute frequency, and brand sensitivity when classifying merchant category codes (MCCs). High-risk MCCs such as 7995 (iGaming) or 5967 (Adult Content) almost always sit outside the EU’s regulated interchange caps.

In 2026, a typical EU consumer card may carry an interchange of 0.2 % (debit)/ 0.3 % (credit), but the same transaction processed under a high-risk MCC or across borders can climb to 1.8-2.4 %. Multiply that by thousands of payments a day, and the cost impact becomes enormous.

The good news: although you cannot negotiate interchange directly, you can influence the tier your transactions qualify for. This is where optimisation begins.

What Determines Your Interchange Rate

- Card Type: Consumer cards are capped; commercial or corporate cards are not.

- Transaction Channel: Card-present (lower risk) vs card-not-present / online (higher).

- Cross-Border Routing: Transactions routed via non-domestic acquirers attract inter-regional interchange.

- Authentication Strength: Transactions verified with Strong Customer Authentication (SCA) or 3-D Secure 2.2 generally qualify for lower interchange.

- Data Completeness: Supplying additional fields (known as Level 2 / Level 3 data) signals legitimacy and can downgrade fees.

- Risk Profile / MCC: Issuers assign MCC-specific risk coefficients; these are periodically updated by the networks.

Five Proven Ways to Lower Interchange Costs

- Enhance Authentication and SCA Adoption

Implementing 3-D Secure 2.2 and risk-based SCA reduces non-authenticated flags that trigger higher interchange brackets.

- Use frictionless flows where possible to preserve conversion.

- Maintain accurate customer IP and device data so issuers approve frictionless SCA exemptions confidently.

Result: up to 0.2-0.4 % reduction in average interchange for CNP transactions.

Source: European Banking Authority SCA Guidelines 2024.

- Submit Level 2 and Level 3 Transaction Data

Level 2 and Level 3 data include tax ID, invoice number, product code, and merchant postcode. In the UK and the US, this richer dataset enables qualified interchange categories for corporate cards.

Example: a UK B2B merchant adding L3 data can see interchange drop from 1.9% to 1.2%.

Tools such as Visa Commercial Data Portal and Mastercard Smart Data automate this process.

- Reduce Chargebacks and Fraud Ratios

Issuers penalise merchants with high dispute rates through downgraded interchange codes or additional scheme fees.

Maintain chargebacks below 0.9 % of monthly transactions by:

- Enabling real-time dispute alerts (Ethoca / Verifi)

- Using pre-chargeback resolution workflows

- Offering fast refunds through Open Banking payouts or SEPA Instant.

- Use Domestic Acquiring and Smart Routing

Cross-border transactions often cost 50 – 100 basis points more due to inter-regional interchange.

Establish local acquiring relationships in your major customer markets (e.g., Germany, Brazil, UAE) to keep transactions domestic in network terms.

Advanced payment orchestration platforms (Primer, Bridge, Paydock) can automatically route traffic to the cheapest acquirer per BIN range. This technique, known as least-cost routing, can cut effective fees by 10 – 20 %.

- Leverage Open Banking and Alternative Rails

Account-to-Account (A2A) payments, now widely available across the UK and EU under the new Payment Services Regulation (PSR), bypass card networks entirely. They carry no interchange and no chargebacks.

Use them for:

- Deposits and top-ups in iGaming

- Subscription renewals

- High-value B2B transactions.

By migrating even 20 % of volume to A2A, a high-risk merchant can lower blended acceptance costs by 0.4 – 0.8 %.

Worked Example: Before and After Optimisation

| Scenario | Channel | Interchange Rate Before | Optimisation Applied | New Rate | Saving |

| UK Consumer Debit | Domestic CNP | 0.50 % | 3-DS + SCA exemption approved | 0.20 % | -0.30 % |

| EU Commercial Card | Cross-border | 1.90 % | Level 3 data + local acquiring | 1.20 % | -0.70 % |

| iGaming Commercial Card | Offshore Routing | 2.30 % | BIN-level routing to EU acquirer | 1.60 % | -0.70 % |

Even modest adjustments compound quickly: a merchant processing £5 million monthly could save £ 25,000 – £ 35,000 per month.

Source: Reserve Bank of Australia Merchant Fees Report 2024, Bank of England Payments Dashboard 2025

Technology Partners and Tools

- Network Portals: Visa Risk Manager, Mastercard Ethoca.

- Orchestration Platforms: Primer, Bridge, Apexx.

- Open Banking APIs: TrueLayer, Token.io, and GoCardless.

- Data Enrichment for L3: FIS Access PaySuite, ACI Worldwide.

These tools enable real-time risk scoring, domestic routing, and data submission, all essential to high-risk fee control.

Regional Regulatory Snapshots (2026)

| Region | Interchange Regime | High-Risk Notes |

| EU / EEA | IFR caps 0.2 % debit / 0.3 % credit | Commercial and cross-border remain uncapped |

| UK | Retained EU caps + PSD2 rules | Surcharging is banned on consumer cards |

| Australia / NZ | RBA cost of acceptance framework | Least-cost routing reduces MDR for debit cards |

| Canada / US | Market-driven rates; surcharging allowed (with limits) | High-risk verticals are subject to reserve requirements |

| MENA / Africa | No interchange caps | Offshore acquiring adds FX spread of 0.4-1 % |

- Interchange makes up 40-60 % of a high-risk merchant’s total processing cost.

- While you cannot rewrite network rules, you can qualify for lower tiers through compliance, data quality and routing.

- Each 0.1 % reduction in effective interchange equals roughly £ 1,000 per £1 million processed.

A well-structured optimisation plan can recover 15-25 % of annual processing costs within one year.

Why Geography Matters in High-Risk Payment Pricing

In 2026, payment pricing is no longer just about the risk category; it’s also about where a transaction takes place. The same business model may attract a 1.5 % fee in Germany but 4.5 % in the Middle East.

Regional regulation, acquirer appetite, taxation, and local clearing systems all influence cost. For high-risk sectors, where acquirers often route through offshore or third-party processors, geography can double or triple the effective Merchant Discount Rate (MDR).

At Payment Mentors, we analyse each jurisdiction using three variables:

- Regulatory environment: level of consumer and AML control.

- Acquirer competition: the number of banks willing to board high-risk merchants.

- Currency & settlement infrastructure: presence of SEPA, Faster Payments, PIX, or instant-payment equivalents.

Europe (UK & EEA)

Typical MDR (High-Risk): 2.5 – 3.5 %

Europe remains the most transparent market for high-risk merchants.

The Interchange Fee Regulation (EU 2015/751) caps consumer interchange at 0.2 % / 0.3 %, creating predictable baseline costs.

However, many iGaming and CBD operators process with Maltese (MGA) or Gibraltar licences, where acquirer availability is limited and rolling-reserve requirements are higher (5-10 %).

Optimisation levers:

- Maintain EU-based acquiring to stay under IFR caps.

- Implement SCA/3-DS 2.2 to prevent downgrades.

- Integrate Open Banking payments for low-risk deposits and refunds.

United Kingdom

Typical MDR (High-Risk): 2.8 – 3.8 %

Post-Brexit, the UK retains the EU interchange caps but no longer enforces them cross-border with the EEA. A UK merchant taking a French card now pays inter-regional interchange (~1.5 %).

High-risk onboarding is governed by FCA consumer-credit and AML standards. Banks de-risk aggressively, pushing many firms to fintech acquirers.

Optimisation levers:

- Use domestic UK acquiring for local transactions.

- Offer Faster Payments / Open Banking for account-to-account payouts.

- Stay within a chargeback ratio of < 0.9 % to retain Tier A pricing.

LATAM (Brazil & Mexico Focus)

Typical MDR (High-Risk): 3.5 – 4.2 %

Latin America offers rapid consumer growth but limited acquirer competition.

Brazil’s PIX instant-payment system, introduced by the Banco Central do Brasil, has lowered domestic processing costs dramatically. Yet international acquirers still charge elevated risk premiums for card transactions in gaming, forex and digital-goods sectors.

Mexico enforces its own interchange caps (0.65 % debit / 1.45 % credit), but few banks will board cross-border high-risk clients without local incorporation.

Optimisation levers:

- Integrate PIX or SPEI rails for local users.

- Use hybrid routing – cards for first payment, PIX for reloads.

- Partner with regional PSPs experienced in iGaming licences (e.g., Betsson Brasil, Codere).

Middle East (UAE & GCC Region)

Typical MDR (High-Risk): 4.0 – 5.5 %

The GCC region is one of the most expensive for high-risk acquiring.

The Central Bank of the UAE and Saudi SAMA closely monitor cross-border iGaming, crypto, and remittance flows. Only a handful of banks (often partnered with offshore acquirers in Cyprus or Malta) offer settlement.

FX conversion (USD → AED) adds another 0.4 – 1 %.

Optimisation levers:

- Structure offshore entities in friendly jurisdictions (Malta, Isle of Man) with regional IBANs.

- Use multi-acquirer set-ups to split domestic vs international traffic.

- Explore mobile-wallet rails (STC Pay, Payit) for local users.

Africa (South Africa & Kenya Focus)

Typical MDR (High-Risk): 4.2 – 5.0 %

African markets are mobile-first. M-Pesa, Airtel Money, and Orange Money dominate consumer payments, carrying lower interchange but higher KYC friction. Card acquisition is limited, so offshore processors fill the gap.

South Africa’s FSCA is tightening AML rules for gambling and forex, increasing onboarding time but improving legitimacy.

Optimisation levers:

- Combine mobile money acceptance with card back-up.

- Use local settlement banks to avoid cross-border uplifts.

- Deploy tiered fraud controls to meet FSCA monitoring requirements.

Australia & New Zealand

Typical MDR (High-Risk): 2.2 – 2.8 %

Both markets benefit from transparent regulation by the Reserve Bank of Australia (RBA) and the Commerce Commission NZ (ComCom). Merchants can legally surcharge up to the cost of acceptance, a limit calculated from their average MDR.

The RBA’s push for Least-Cost Routing (LCR) has lowered debit-card fees substantially, making these regions among the most competitive outside Europe.

Optimisation levers:

- Implement LCR for domestic debit cards.

- Offer PayTo (Australia’s new A2A rail) to reduce chargebacks.

- Ensure compliance with ComCom’s surcharge transparency rules.

North America (US & Canada)

Typical MDR (High-Risk): 3.0 – 4.5 %

The US and Canada lack interchange caps; rates are set by the card networks. Visa and Mastercard allow credit-card surcharging within limits (usually ≤ 3 % or the merchant’s MDR, whichever is lower).

Canada legalised surcharging in October 2022, but debit cards remain excluded. High-risk sectors face strict reserve requirements and annual compliance audits.

Canada legalised surcharging in October 2022, but debit cards remain excluded. High-risk sectors face strict reserve requirements and annual compliance audits.

Optimisation levers:

- Pass compliant surcharges where permitted.

- Provide Level 3 data for corporate cards to gain lower interchange tiers.

- Maintain chargeback ratios below Visa 0.9 % / Mastercard 1.5 % thresholds.

Comparative MDR Table (2026 Estimates)

| Region | Low-Risk MDR | High-Risk MDR | Key Drivers |

| Germany (EU) | 1.4 % | 2.8 % | IFR caps + strong local acquiring |

| UK | 1.5 % | 3.0 % | PSD2 residual rules + surcharge ban |

| UAE / GCC | 2.2 % | 4.5 % | Offshore acquiring + FX spread |

| Brazil (LATAM) | 2.0 % | 3.8 % | Tax complexity + limited acquirers |

| Kenya / South Africa | 2.5 % | 4.2 % | High fraud + mobile money fees |

| Australia | 1.3 % | 2.6 % | LCR + regulated surcharging |

| Canada | 1.6 % | 3.1 % | Market-driven pricing |

(All estimates based on Visa / Mastercard public interchange tables and central-bank merchant-fee reports 2024-2025.)

- Geography is now a primary pricing variable for high-risk merchants.

- Regions with strong regulation (EU, UK, AU/NZ) offer stability and lower fees.

- Emerging markets (MENA, Africa, LATAM) carry higher margins but higher fraud and FX risk.

The best global strategy is multi-acquirer optimisation, combining onshore and offshore processing to balance approval rates and cost.

The Hidden Cost Layer Most High-Risk Merchants Miss

Many merchants believe their Merchant Discount Rate (MDR) represents their total processing cost. In reality, that’s only the visible tip of the iceberg. Beneath the headline percentage lies a collection of administrative, compliance, and technical fees that can raise the effective cost of acceptance by 0.5 – 1.5 percentage points.

These charges often appear under vague invoice terms such as non-compliance fee, monitoring charge, or service adjustment. For high-risk industries, iGaming, adult, CBD, travel, remittance, the likelihood of incurring them is far greater because acquirers allocate additional resources for risk oversight.

At Payment Mentors, we categorise hidden fees into four groups:

- Non-Compliance Penalties

- Set-up & Monthly Maintenance Costs

- Gateway & Statement Add-Ons

- Cross-Border & FX Surcharges

- Non-Compliance and Monitoring Penalties

These are applied when a merchant fails to meet contractual or regulatory standards.

| Fee Type | Typical Range (2026) | Trigger | How to Avoid It |

| PCI DSS Non-Validation Fee | £250 – £500 p.a. | Failure to file the annual SAQ and vulnerability scan | Maintain PCI validation and submit on time |

| Chargeback Monitoring Fee | £10 – £25 / month | Ratio > 0.9 % (Visa) or 1.5 % (Mastercard) | Deploy Ethoca/Verifi alerts; issue refunds early |

| AML/KYC Review Fee | £50 – £200 per review | Extra screening during re-onboarding | Keep KYB/KYC records updated |

| Regulatory Cost Adjustment | Variable (0.05 – 0.2 %) | Scheme or legislative changes | Review contracts quarterly |

Why they matter:

Each penalty increases your risk profile, which can raise acquirer mark-ups at renewal. Avoidance demonstrates compliance maturity, something that Payment Mentors highlights when negotiating lower reserves.

- Set-Up and Maintenance Costs

Acquirers recover administrative overheads by charging for onboarding, system access, or low monthly volume.

| Fee Type | Typical Range | Notes |

| Underwriting / Onboarding Fee | £200 – £1 000 | One-off for high-risk application reviews |

| Monthly Minimum Fee | £25 – £100 | Charged if MDR revenue < threshold |

| Account Maintenance Fee | £10 – £30 per month | Covers statement generation and support |

| Early Termination Fee | Variable (£250 – £500) | Applied if the contract ends before the term |

Best practice: Bundle these into your mark-up negotiation. High-volume merchants can request waivers or credit offsets.

- Gateway and Statement Add-Ons

Many merchants use third-party gateways or orchestration layers. Each adds a marginal cost that’s easy to overlook.

| Fee Type | Description | Typical Cost | Control Measure |

| Gateway Access Fee | Monthly API connectivity charge | £10 – £50 | Consolidate gateways |

| Per-Transaction Gateway Fee | Technical processing fee | £0.03 – £0.10 | Volume-based pricing |

| Batch Settlement Fee | Per payout batch | £1 – £5 | Use weekly settlement instead of daily |

| Statement Fee | For paper reports | £5 – £10 | Switch to digital-only |

Tip from Payment Mentors

Always request a complete line-item statement. If your PSP refuses, it’s usually a sign of blended pricing hiding micro-fees.

- Cross-Border and FX Surcharges

High-risk merchants often serve global customers, meaning frequent currency conversions and inter-regional routing. Each adds a cost layer.

| Fee Type | Typical Range | Description |

| Cross-Border Interchange Uplift | +0.40 – 1.20 % | Applied when the issuer & acquirer are in different regions |

| FX Conversion Spread | 0.25 – 0.80 % | Exchange margin on settlement |

| International Authorisation Fee | £0.03 – £0.08 per txn | Network cost for foreign cards |

How to control them:

- Open multi-currency accounts (GBP, EUR, USD).

- Use local acquisition where customer concentration is high.

- Avoid converting currencies multiple times in the settlement chain.

How to Audit and Eliminate Hidden Fees

- Demand Line-Item Transparency: Request statements showing interchange, scheme, and markup separately.

- Benchmark Quarterly: Compare effective MDR against published scheme data.

- Use FinOps Dashboards: Integrate reporting tools (e.g., Gr4vy, FIS Access PaySuite).

- Negotiate Gateway Bundles: Merge tech fees under a single vendor.

- Engage Specialist Consultancy: Firms like Payment Mentors audit high-risk pricing contracts to recover overcharges.

For high-risk merchants, the majority of overpayment doesn’t stem from regulation; it comes from opaque pricing structures.Removing or renegotiating just three hidden items can reduce total costs by 15 – 20 % without altering acquirer relationships.

The 2026 Playbook: Cutting Costs Without Cutting Corners

Reducing payment processing costs in high-risk industries is not about finding shortcuts; it’s about building resilient infrastructure. At Payment Mentors, we view cost optimisation as a blend of five disciplines: data, technology, geography, compliance, and negotiation.

The key principle: you can’t control what you can’t measure.

Once you know your full pricing anatomy (as explained in earlier sections), the next step is to apply structured, measurable changes.

- Move the Mix: Add Lower-Cost Payment Rails

Credit card fees will always remain high in risk-weighted sectors. However, today’s alternative payment options are safe, fast, and regulator-approved, and they carry zero interchange.

Open Banking & Account-to-Account (A2A) Payments

- Fee model: flat £0.20-£0.50 per transaction (vs 2-4 % card MDR).

- No chargebacks, since payments are customer-authenticated via bank.

- Instant settlement through UK Faster Payments, EU SEPA Instant, and Australia’s PayTo.

Best use cases:

- iGaming deposits and withdrawals, subscription renewals, and high-value B2B purchases.

- Pair with card rails for initial acquisition, then nudge returning customers toward A2A (Pay by Bank).

Mobile Money & Local Wallets

In Africa and LATAM, mobile money options such as M-Pesa, Airtel Money, and PIX offer dramatic cost advantages:

- MDR is often below 1 %.

- Instant settlement and built-in KYC;

- Compatible with digital wallets for recurring payments.

These should complement, not replace, card acceptance. Payment Mentors often design multi-rail acceptance flows that automatically route customers to the most cost-effective local method.

- Route Smarter: Use Multi-Acquirer & Least-Cost Routing

Multi-acquirer architecture allows a merchant to connect to multiple acquiring banks through a payment orchestration platform. Each transaction can be automatically directed to the acquirer offering the lowest cost or highest authorisation rate for that card type and region.

Benefits:

- Avoids cross-border uplifts by routing domestically.

- Enables benchmarking of acquirer performance over time.

Tools to use: Primer, Gr4vy, Bridge, or in-house API routing.

Least-Cost Routing (LCR)

In card-present environments (Australia, New Zealand, Canada), LCR sends debit transactions through the cheapest domestic network rather than the international Visa/Mastercard rails.

Result: 10-20 % savings on debit transactions.

Every time a transaction is downgraded, for example, because it lacks SCA, L3 data, or a full customer address, it’s reclassified into a higher interchange tier.

For high-risk merchants processing tens of thousands of transactions, this can inflate costs by 0.3-0.6 %.

Quick fixes that work:

- Implement 3-D Secure 2.2 with frictionless SCA.

- Enrich every transaction with tax amount, merchant postcode, and customer reference (for L3 eligibility).

- Avoid manual reattempts of declined transactions; use automated retry logic instead.

The data maturity model Payment Mentors deploys shows that after three months of L3 data submission, average interchange costs drop by 8-12 %.

- Negotiate the Parts You Can Control

While interchange and scheme fees are fixed, the acquirer markup, reserve structure, and tech fees are fully negotiable. Merchants rarely revisit their pricing, yet Payment Mentors’ data shows that even strong accounts often overpay by 20 %.

How to approach negotiation effectively:

- Prepare Evidence: Gather 3-6 months of transaction data with dispute ratios and approval rates.

- Prove Performance: Demonstrate stable chargebacks (<0.8 %) and full PCI DSS compliance.

- Request Step-Down Reserves: Many acquirers will move from 10 % to 5 % reserves after consistent clean processing.

- Reprice Tech Fees: Bundle gateway and orchestration into one integrated cost.

- Benchmark: Compare competing acquirers quarterly; Payment Mentors provides clients with region-by-region pricing benchmarks.

Real-world result

A UK-based forex brokerage reduced its effective MDR from 4.2 % to 3.1 % after a two-round negotiation supported by data evidence.

5. Align Compliance with Cost Reduction

Compliance is not just a legal necessity; it’s a pricing advantage.

Every acquirer grades merchants on a risk scorecard. Maintaining strong scores directly translates into lower mark-ups and faster settlements.

Areas where compliance lowers cost:

- PCI DSS Level 1 Validation: eliminates non-compliance surcharges.

- AML Reporting Accuracy: fewer manual reviews, lower due diligence fees.

- KYC Automation: speeds up new customer verification, improving cash flow.

Pro Tip: Maintain a compliance scorecard showing audit dates, SCA success rates, and dispute levels. Acquirers treat this as proof of maturity when reviewing pricing.

Bonus: Leverage Payment Mentors’ Data Audit Framework

At Payment Mentors, our consultants implement a proprietary Payment Efficiency Framework designed for high-risk merchants.

It includes:

- Data diagnostics: Detecting downgrade triggers and fee leakage.

- Market comparison matrix: Identifying cheaper onshore or offshore acquirers.

- Reserve optimisation plan: Tying release schedules to KPI milestones.

- Governance support: Aligning fee strategy with upcoming PSD3 and global AML rules.

On average, clients achieve a 15-25 % reduction in total processing costs within 6-12 months.

- Cost reduction is achieved through strategy, not shortcuts.

- Moving 20 % of volume to A2A or Open Banking can reduce blended MDR by 0.4-0.8 %.

- Least-cost routing and multi-acquirer setups are now mainstream.

- Clean data, strong compliance, and KPI-driven negotiations unlock lower pricing tiers.

- High-risk doesn’t have to mean high-cost, but it does require precision.

From Audit to Action: Turning Insights into Savings

By this stage, you know how your fees are structured, what can be negotiated, and which regions cost more.

But knowledge is only powerful when it’s applied.

At Payment Mentors, we’ve distilled the process into a simple 30-day plan that transforms discovery into measurable savings, without disrupting live operations.

Week 1: Map Your True Cost of Acceptance

Objective: build transparency.

- Collect 3-6 months of statements from each PSP or acquirer.

- Reconcile total fees paid vs. transaction volume to calculate your effective MDR (all-in cost).

- Categorise every fee: interchange, scheme, markup, gateway, reserve, compliance.

- Highlight anomalies such as variable FX or regulatory adjustment items.

- Use Payment Mentors’ Fee-Stack Template to visualise costs per payment rail (cards, open-banking, mobile money).

Week 2: Benchmark and Identify Leverage Points

Objective: know what good looks like.

- Compare each component with industry averages from:

- Visa UK Interchange Tables

- Mastercard UK Fee Schedule

- Reserve Bank of Australia Merchant Fees Report 2024

- Note where your numbers exceed benchmarks by > 0.3 %.

- Identify negotiables: acquirer mark-up, reserve rate, gateway access, chargeback fees.

- Flag non-negotiables: interchange caps, scheme fees, taxes, focus effort elsewhere.

Week 3: Implement Quick Wins

Objective: secure visible savings fast.

- Optimise routing: Enable domestic acquirer paths wherever possible.

- Activate Open Banking / A2A options for deposits or large transfers.

- Review reserve policy: Request partial releases for clean chargeback months.

- Enable 3-D Secure 2.2 across all card flows to prevent downgrades.

- Eliminate paper statements and duplicate gateway accounts.

These steps alone often trim 0.3-0.6 % from total MDR within the first month.

Week 4: Negotiate and Formalise Changes

Objective: lock in sustainable savings.

- Prepare a data-driven pitch: Show improved KPIs (chargeback < 0.8 %, SCA success > 97 %).

- Contact your acquirer for a quarterly pricing review; request step-down mark-ups or reserve reductions.

- Bundle fees (gateway + processing + settlement) into one transparent rate.

- Document compliance readiness (PCI DSS v4.0 certificate, AML audit results).

- Sign revised addenda and set reminders for next review in 90 days.

Maintenance Loop (Beyond 30 Days)

- Semi-annually: review compliance documents (PCI DSS, AML certifications).

- Annually: renegotiate mark-ups if volume or risk profile improves.

Payment Mentors recommends creating an internal Payment Steering Committee, including finance, compliance, and tech leads, meeting monthly to ensure optimisation remains ongoing.

Case Study Snapshot

A European iGaming operator followed this 30-day roadmap with Payment Mentors’ guidance:

| Metric | Before | After | Change |

| Effective MDR | 4.2 % | 3.3 % | -0.9 pp (-21 %) |

| Chargeback Ratio | 1.2 % | 0.7 % | -0.5 pp |

| Rolling Reserve | 10 % | 5 % | -50 % |

Result: annual savings ≈ of £ 180,000 on a £20 million turnover.

- A structured 30-day plan can reclaim 15-25 % of total fees.

- Cost reduction begins with data transparency, not new providers.

- Negotiations succeed when backed by evidence and compliance.

- Treat payments as a living cost centre, and monitor continuously.

Making Sense of the Cost Maze

Every high-risk merchant, from a regulated betting platform in Malta to a CBD retailer in the UK, pays more for the privilege of processing payments. But as we’ve shown, high-risk doesn’t have to mean high-cost.

Most of the additional expense comes not from what you sell, but from how your payments are structured:

- Outdated routing,

- Poor authentication data

- Limited acquirer visibility

- Hidden operational fees.

With data transparency, compliant practices, and the right mix of payment rails, high-risk operators can achieve cost structures that rival low-risk merchants, while staying fully compliant with regulators and schemes.

Core Lessons from the High-Risk Pricing Deep Dive

| Theme | Key Lesson | Practical Impact |

| 1. MDR Anatomy | Understand every fee layer, interchange, scheme, markup, and add-ons. | Identifies where 40 % of the cost is negotiable. |

| 2. Interchange Optimisation | Adopt 3-D Secure 2.2, Level 3 data, and domestic routing. | Reduces effective interchange by 0.3-0.7 %. |

| 3. Regional Comparison | Costs vary 2× across markets; balance onshore/offshore wisely. | Cuts cross-border uplifts by 0.5-1 %. |

| 4. Hidden Fees | Non-compliance and gateway extras inflate costs invisibly. | Recover 10-20 % by auditing contracts. |

| 5. Strategic Optimisation | Combine A2A, least-cost routing, and compliance scorecards. | Creates lasting, risk-adjusted efficiency. |

| 6. 30-Day Action Plan | Audit → Benchmark → Implement → Negotiate. | Converts theory into measurable savings. |

A Changing Landscape, and a Call to Act

The year 2026 will be transformative for high-risk payment processing:

- The EU PSD3 and UK Payment Services Regulation (PSR) will modernise consumer protection.

- AI-based risk scoring will reshape acquirer decision-making.

- Open Banking adoption is expected to surpass 80 % of UK adults, according to OBIE forecasts.

These changes mean merchants who adapt early will not only save money but also secure their position with acquirers long-term.

At Payment Mentors, we’ve observed a consistent pattern:

Merchants who treat payments as a data-driven discipline, not a background cost, outperform competitors by 15-30 % in net profit margin within a year.

Final Words

Payment costs are one of the few controllable expenses in a high-risk business.

By applying the principles outlined in this guide and partnering with specialists who understand every acquirer nuance, your business can process more profitably, remain fully compliant, and scale globally with confidence.

At Payment Mentors, our mission is simple: to make high-risk payments predictable, affordable, and sustainable, no matter where you operate.

FAQs

1. What makes a business high-risk for payment processing?

A business is classified as high-risk when acquirers or banks consider it more likely to experience chargebacks, fraud, or regulatory scrutiny. Common examples include iGaming, adult content, forex, CBD, nutraceuticals, and travel. These sectors face higher merchant fees, reserve requirements, and stricter compliance checks.

2. Why are high-risk payment processing fees higher than normal?

High-risk merchants face elevated fraud exposure, dispute ratios, and regulatory compliance costs. To offset these, acquirers apply risk-adjusted mark-ups and hold rolling reserves. While interchange and scheme fees are fixed, the acquirer’s markup and reserve policy are negotiable, areas where Payment Mentors helps clients cut costs.

3. What is the Merchant Discount Rate (MDR)?

The MDR is the total percentage charged per transaction by all parties in the processing chain, including interchange, scheme fees, acquirer markup, and technology fees. For high-risk sectors, MDRs can range between 2.5 % and 6.5 %, depending on jurisdiction and industry.

4. Can I reduce my MDR as a high-risk merchant?

Yes. By improving chargeback ratios, maintaining PCI DSS compliance, submitting Level 2/3 data, and negotiating mark-ups, you can reduce your effective MDR by 0.5-1.5 %. Payment Mentors conducts audits that typically save clients 15-25 % of total annual processing costs.

5. What is the difference between interchange, scheme, and acquirer fees?

- Interchange: Paid to the card-issuing bank.

- Scheme Fees: Paid to the card network (Visa, Mastercard).

- Acquirer Mark-Up: The processor’s margin for handling transactions.

Understanding these distinctions helps merchants identify which parts of their pricing are negotiable.

6. What are rolling reserves, and why do acquirers hold them?

A rolling reserve is a percentage (usually 5-10 %) of daily transaction value held back by the acquirer for a set period (often 180 days) to cover potential chargebacks or disputes. It’s standard for high-risk merchants, but can be reduced through consistent performance and strong dispute management.

7. What are the hidden fees in high-risk payment processing?

Hidden costs often include non-compliance penalties, gateway access charges, FX spreads, and cross-border uplifts. Individually small, these can inflate the effective MDR by up to 1.5 %. Regular auditing ensures you pay only what’s contractually justified.

8. How does geography affect high-risk payment costs?

Fees differ sharply by region. For example, a high-risk merchant may pay 2.8 % in Germany, 4.5 % in the UAE, or 3.8 % in Brazil. Local regulation, FX exposure, and acquirer availability all drive variation. Working with global consultants like Payment Mentors helps merchants balance onshore and offshore acquiring to reduce costs.

9. Can open banking help lower payment processing fees?

Yes. Open Banking and Account-to-Account (A2A) payments bypass card networks, eliminating interchange and chargebacks. In the UK and EU, they now offer near-instant settlement and cost up to 80 % less than credit card transactions.

10. What is least-cost routing (LCR)?

LCR automatically directs debit-card transactions through the cheapest domestic network rather than expensive international rails. Common in Australia and New Zealand, it can save merchants 10-20 % on debit-card costs without affecting the customer experience.

11. How do chargebacks affect my processing fees?

Exceeding chargeback thresholds (0.9 % for Visa, 1.5 % for Mastercard) can trigger monitoring fees, reserve increases, and mark-up hikes. Maintaining clean transaction data, quick refund policies, and early-warning tools prevents those penalties.

12. Can I negotiate with my payment processor?

Absolutely. Acquirer mark-ups, reserves, gateway charges, and statement fees are all negotiable. Once you can present strong performance metrics (chargebacks, SCA success, and fraud rates), you’re in a solid position to request revised pricing tiers.

13. Are there government regulations affecting high-risk payment fees?

Yes. Key ones include:

- Interchange Fee Regulation (EU 2015/751): caps consumer card interchange in the EU/UK.

- Payment Services Regulation (UK): sets Open Banking and SCA standards.

- Reserve Bank of Australia LCR Policy: enforces domestic debit routing.

Payment Mentors ensures all client strategies comply with these frameworks.

14. What’s the role of PCI DSS in reducing fees?

PCI DSS (Payment Card Industry Data Security Standard) compliance demonstrates data protection maturity. Acquirers reward compliant merchants with lower monitoring fees and faster onboarding. Non-compliance can lead to surcharges of £250-£500 per year.

15. How can Payment Mentors help my business?

- Fee audits and MDR analysis.

- Multi-acquirer cost benchmarking.

- Reserve and mark-up negotiation.

- Regulatory alignment (FCA, MGA, EU).

- Implementation of A2A and Open Banking solutions.

Our goal is to transform complex payment environments into predictable, optimised, and compliant cost structures.