Regulation has become a defining feature of how payments operate in Europe. What was once experienced as a set of compliance obligations has increasingly shaped the way payment operations are structured, governed, and managed on a day-to-day basis. For many European merchants, regulation is no longer something to prepare for periodically; it is a constant operating condition.

This has changed the role payments play inside organisations. Decisions that were previously informal or optimised locally now carry wider consequences across risk, approvals, reconciliation, and reporting. As regulatory expectations have tightened across multiple areas, tolerance for inconsistency has fallen. Payments that behave unpredictably, even if technically compliant, introduce operational strain that is difficult to absorb.

In response, European merchants are restructuring how payment operations function. The focus has shifted from enabling individual capabilities to building stable, interpretable systems that can operate reliably under sustained regulatory pressure. This adaptation is less about meeting specific rules and more about redesigning operating models to support consistency, visibility, and control as the baseline for doing business in Europe.

- Why Europe Feels Operationally Different for Merchants

- Regulation as an Operating Environment, Not a Rulebook

- How Payment Operations Are Being Restructured in Practice

- Governance Replacing Experimentation

- The Trade-Offs European Merchants Are Accepting

- Why These Changes Persist Beyond Individual Regulations

- Conclusion

- FAQs

Why Europe Feels Operationally Different for Merchants

For merchants operating in Europe, payments are shaped by a level of regulatory presence that influences day-to-day decisions rather than sitting in the background. Regulation is not experienced as a single change or event, but as a steady constraint that affects how payment flows are designed, monitored, and adjusted over time.

This environment places a premium on predictability. Payment behaviour that varies widely between channels, markets, or customer segments is harder to justify and more difficult to manage when scrutiny is constant. As a result, European merchants tend to favour consistency over rapid experimentation, even when alternative approaches might appear commercially attractive in the short term.

The operational impact is cumulative. Small variations in authentication handling, approval logic, or settlement processes can quickly create complexity that is difficult to explain or defend. Over time, this makes informal decision-making less viable. Payment operations begin to feel heavier, not because systems are inefficient, but because they are designed to withstand ongoing oversight.

This is why Europe often feels operationally different from other regions. The emphasis is not simply on meeting regulatory requirements, but on building payment operations that behave in a controlled and interpretable way. For merchants, adapting to this environment means accepting that stability and structure are not optional, but central to how payments function in a regulated market.

Regulation as an Operating Environment, Not a Rulebook

European regulation is often described in terms of rules and requirements, but for merchants its real impact is operational. Once multiple regulatory obligations interact, they stop behaving like a checklist and start shaping how payment operations function on a daily basis. Decisions around approvals, authentication, and reporting are no longer isolated choices; they sit within a wider environment where consistency and traceability matter.

From compliance tasks to operational discipline

In regulated markets, compliance does not live at the edge of the organisation. Regulatory expectations influence how payment processes are designed, how exceptions are handled, and how changes are introduced. Activities that might once have been treated as configuration choices become operational disciplines, governed by documented rationale and repeatable behaviour. Over time, this shifts payments from a flexible function to a structured one.

Why variation is harder to absorb in Europe

Variation carries a higher operational cost in Europe. When payment behaviour differs across markets or channels, it becomes harder to explain outcomes and demonstrate control. Even small inconsistencies can trigger additional review, internal escalation, or rework. As a result, European merchants are more cautious about allowing divergence in how payments are handled, preferring models that behave consistently even if they are less optimised locally.

How regulation reshapes merchant behaviour indirectly

The influence of regulation extends beyond explicit requirements. It affects how merchants approach risk, how they interpret approval performance, and how they design customer journeys. Decisions are made with an awareness of how they might be scrutinised later, not just how they perform today. In this way, regulation reshapes behaviour indirectly, encouraging operating models that prioritise clarity and control over experimentation.

Taken together, these dynamics explain why regulation in Europe feels less like a rulebook and more like an operating environment. Merchants are not simply complying with individual mandates; they are adapting their payment operations to function reliably within a system where oversight is continuous and expectations are enduring.

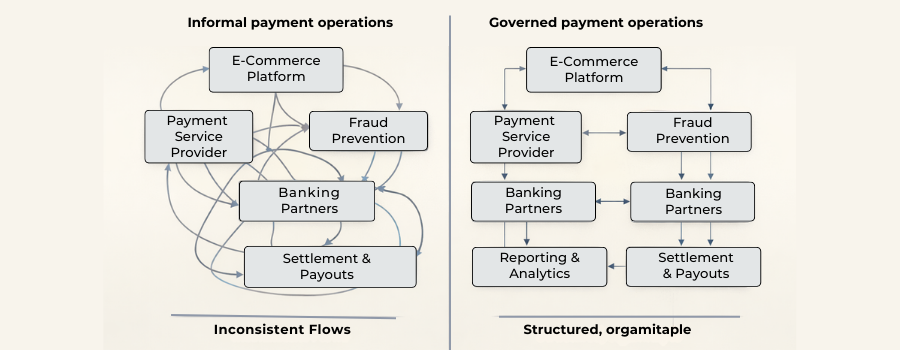

How Payment Operations Are Being Restructured in Practice

As regulation has become a permanent feature of the European payments landscape, merchants have been forced to rethink how payment operations are organised and controlled. The changes are less about adding new capabilities and more about reshaping existing processes so that they behave predictably under sustained oversight.

Authentication as a managed process, not an exception

Authentication is no longer treated as a fallback triggered only when risk spikes. In regulated environments, inconsistent application creates noise that is difficult to justify or explain. European merchants increasingly manage authentication as a defined process, with clear rules about when it is applied and how outcomes are handled. The goal is not to maximise pass-through rates, but to ensure that authentication behaviour remains stable and defensible over time.

Approval behaviour under regulated flows

Approval optimisation in Europe tends to be conservative by design. Rather than experimenting frequently with routing or retries, merchants prioritise predictable approval behaviour that aligns with regulatory expectations. Changes are introduced deliberately, assessed over longer periods, and documented carefully. This reduces short-term volatility, even if it limits the pace at which performance can be tuned.

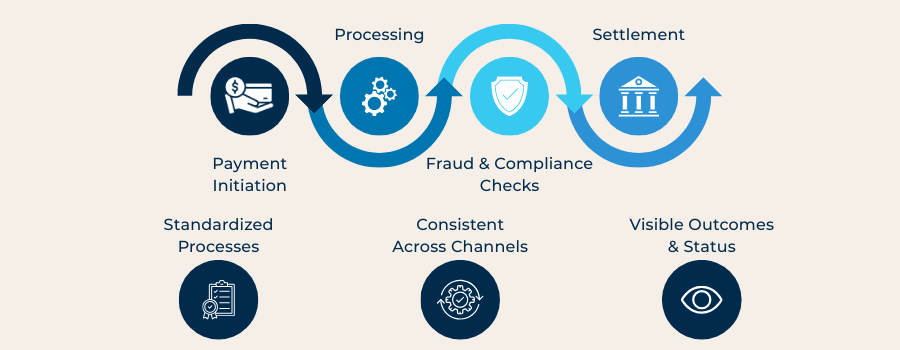

Reconciliation and reporting as first-class functions

Regulation has also elevated reconciliation and reporting from back-office tasks to core operational functions. European merchants invest more effort in ensuring that payment data can be traced cleanly from transaction to settlement. Visibility across flows, fees, and outcomes is treated as essential, not optional, because it underpins both internal control and external accountability.

Across these areas, the restructuring is consistent in its intent. Payment operations are designed to behave in ways that can be understood, explained, and reviewed without excessive interpretation. This does not eliminate complexity, but it contains it, allowing merchants to operate within a regulated environment without constant friction.

Governance Replacing Experimentation

As regulatory pressure has increased, informal experimentation in payment operations has become harder to sustain. Decisions that were once made locally or adjusted quickly in response to performance now carry broader implications for risk, compliance, and internal accountability. In this environment, governance has moved from being a supporting function to a central organising principle.

European merchants are increasingly centralising ownership of payment decisions. Responsibility for how payments behave is defined more clearly, with fewer ad-hoc changes made at the edges of the organisation. This reduces the risk of conflicting configurations developing in parallel and makes it easier to explain why systems behave the way they do when questioned internally or externally.

Documentation and auditability have followed the same trajectory. Changes to payment flows, approval logic, or authentication handling are more likely to be recorded, reviewed, and justified before they are implemented. While this slows the pace of change, it also reduces the likelihood of unintended consequences emerging later. Governance, in this sense, is not about control for its own sake, but about maintaining coherence as complexity grows.

The shift away from experimentation is often misunderstood as conservatism. In practice, it reflects a recognition that regulated payment environments reward clarity over agility. By embedding governance into payment operations, European merchants create systems that can evolve deliberately rather than reactively, within the constraints of ongoing oversight.

The Trade-Offs European Merchants Are Accepting

Restructuring payment operations for a regulated environment comes with deliberate trade-offs. The most visible is speed. Change cycles in Europe tend to be slower, as adjustments to payment behaviour are introduced cautiously and reviewed over longer periods. While this can feel restrictive, it reduces volatility and lowers the risk of decisions having unintended regulatory or operational consequences.

Flexibility is another area where compromise is common. European merchants are often less willing to support highly divergent payment behaviours across markets or channels, even when local optimisation might improve short-term performance. Uniformity makes systems easier to understand and defend, particularly when outcomes need to be explained to internal stakeholders or external reviewers.

These trade-offs are not accidental. They reflect an operating reality in which predictability and control are valued more highly than rapid experimentation. For many merchants, the stability gained outweighs the loss of agility. Payments may evolve more slowly, but they do so within a structure that supports confidence, accountability, and long-term sustainability in a regulated market.

Why These Changes Persist Beyond Individual Regulations

Many of the operational changes European merchants have made were triggered by specific regulatory developments, but they tend to persist long after individual requirements settle or evolve. Once payment operations have been restructured to support consistency, visibility, and governance, reverting to less controlled models offers little practical benefit.

This persistence reflects how regulation reshapes expectations internally. Teams become accustomed to operating within clearer boundaries, with defined ownership and documented decision-making. The discipline required to meet regulatory scrutiny also improves coordination between payments, risk, finance, and compliance functions, making loosely structured approaches harder to justify even when rules change.

Over time, these operating models establish a new baseline. Payments are expected to behave predictably, to be explainable without excessive interpretation, and to withstand ongoing oversight. Regulation may act as the catalyst, but the resulting operational maturity often becomes a permanent feature of how European merchants run payments, rather than a temporary response to external pressure.

Conclusion

Regulation has reshaped how payments operate in Europe in ways that extend far beyond compliance. For merchants, adapting has meant restructuring payment operations so they can function predictably under sustained oversight, rather than responding to regulatory change as a series of isolated events.

This shift has driven a move towards greater consistency, clearer ownership, and stronger governance. While these changes often reduce flexibility and slow the pace of experimentation, they also create operating models that are easier to understand, explain, and defend. In a regulated environment, that stability becomes a practical advantage rather than a constraint.

As European markets continue to evolve, the operational discipline built in response to regulation is likely to persist. Payments that are structured for clarity and control are better equipped to absorb future change, making regulation less of a hurdle and more of a defining condition of how payment operations are run.

FAQs

1. Why does regulation affect payment operations beyond compliance requirements?

Because regulatory expectations influence how payments behave day to day. Consistency, traceability, and explainability become operational necessities, not just compliance outcomes.

2. Why do European payment operations feel heavier than in other regions?

They are designed to withstand continuous oversight. Predictability and control are prioritised over flexibility, which adds structure but also operational weight.

3. Is restructuring payment operations mainly about meeting new rules?

No. While rules often act as the trigger, restructuring is about building operating models that remain stable and interpretable under ongoing regulatory pressure.

4. Why is consistency valued more than optimisation in European payments?

In regulated environments, inconsistent behaviour is harder to explain and defend. Stability reduces operational risk even if it limits short-term performance gains.

5. How has regulation changed approval and authentication handling?

Authentication and approval decisions are managed as defined processes rather than reactive tools. This reduces variability and makes outcomes easier to justify over time.

6. Why have reconciliation and reporting become core operational functions?

Because visibility into payment flows underpins both internal control and external accountability. Clean traceability is essential in a regulated market.

7. What does governance replace in European payment operations?

It replaces informal experimentation. Decision-making becomes more centralised, documented, and deliberate to avoid conflicting behaviour and unintended consequences.

8. Are European merchants becoming more conservative in how they run payments?

They are becoming more structured rather than more conservative. The focus shifts from speed and flexibility to clarity and operational coherence.

9. Do these operational changes slow down innovation?

They slow the pace of change, but they also reduce volatility. Innovation tends to happen within clearer boundaries rather than through rapid experimentation.

10. Why do these operational models persist even when regulations change?

Once structure, ownership, and discipline are embedded, reverting to less controlled approaches offers little benefit. Operational maturity becomes the new baseline.

11. Is regulation the main driver of these changes, or just a catalyst?

Regulation is the catalyst. The resulting changes persist because they improve coordination, accountability, and system stability beyond compliance needs.

12. What defines a well-adapted payment operation in a regulated European market?

Predictable behaviour, clear ownership, consistent processes, and the ability to explain outcomes without excessive interpretation.