Approval rates are often treated as a simple balance between growth and risk. Declines are accepted as the cost of protection, with fraud controls positioned as the necessary barrier that keeps bad actors out. In reality, many of the customers being declined today are not fraudulent at all.

As payment behaviour has become more complex, legitimate transactions increasingly resemble patterns once associated with fraud. Customers move across devices, channels, and locations, while traditional controls still rely on fixed assumptions. This has led to a rise in false positives, where good customers are rejected because the system lacks confidence, not because risk is present.

Advanced fraud models have emerged in response to this shift. Their role is not to relax controls, but to improve how risk is interpreted. By reducing uncertainty rather than increasing tolerance, they allow merchants to approve more legitimate customers without expanding their exposure.

This reframes fraud systems from defensive tools into part of the approval infrastructure itself, shaping who is trusted as behaviour continues to evolve.

- Why Good Customers Are Still Being Declined

- How Fraud Models Have Evolved Beyond Rules and Thresholds

- Precision Over Permissiveness: What Advanced Actually Means

- Reducing False Positives Without Increasing Fraud Exposure

- How Fraud Decisions Influence Issuer Behaviour Over Time

- When Better Fraud Modelling Backfires

- Conclusion

- FAQs

Why Good Customers Are Still Being Declined

False declines are often described as edge cases, but in practice they are structural. As payment environments become more complex, many legitimate transactions no longer fit the narrow patterns that traditional fraud controls were designed to recognise. When behaviour falls outside those expectations, systems default to caution.

This is particularly visible where controls rely on rigid rules or binary thresholds. Signals are treated in isolation, stripped of context, and forced into yes-or-no decisions. The outcome is predictable: transactions that are unfamiliar rather than risky are blocked, even when there is no clear indication of fraud.

Over time, this approach creates collateral damage. Good customers encounter unnecessary friction, abandon purchases, and lose trust. From the merchant’s perspective, approval rates decline without a corresponding reduction in fraud. What appears to be stronger protection is often just a higher level of uncertainty being managed through rejection.

There is also a wider system effect. Issuers observe transaction streams shaped by these decisions. When legitimate activity is repeatedly interrupted or behaves erratically due to over-defensive controls, issuer confidence can be affected. Declines then reinforce themselves, not because fraud is increasing, but because the overall decision environment becomes less predictable.

Understanding why good customers are still being declined requires recognising this chain reaction. It is not simply a matter of tuning thresholds. It reflects how fraud decisions are made, how uncertainty is handled, and how those choices ripple through the approval ecosystem.

How Fraud Models Have Evolved Beyond Rules and Thresholds

Early fraud controls were built around certainty. Rules and thresholds worked well when behaviour was relatively stable and signals were easy to classify. Transactions either matched known risk patterns or they did not. As long as customer behaviour remained predictable, this approach was effective.

That stability has eroded. Legitimate behaviour now changes faster than static rules can be updated. Customers switch devices, locations, and payment methods as part of normal usage. When fraud controls are anchored to fixed assumptions, they struggle to interpret this variation. The result is not better protection, but more ambiguity being resolved through decline.

From static rules to behavioural interpretation

Modern fraud models place less emphasis on single signals and more on patterns over time. Instead of asking whether a transaction crosses a predefined line, they assess whether behaviour is consistent with what has been observed before. This shift allows systems to tolerate variation without treating it as inherently risky.

Why context matters more than isolated signals

Context changes how signals should be read. A location change, a new device, or an unusual purchase amount may be unremarkable when viewed alongside prior behaviour, but suspicious when seen in isolation. Advanced models focus on how signals relate to one another, rather than scoring each one independently.

Where threshold-based decisioning breaks down

Binary cut-offs force complex behaviour into simple outcomes. When confidence is low, thresholds tend to be tightened, increasing false positives. Over time, this creates a cycle where controls become more defensive without becoming more accurate.

In contrast, legacy approaches tend to struggle in environments where:

Behaviour shifts frequently without indicating fraud

Signals appear risky in isolation but benign in combination

Decision confidence matters more than absolute risk scores

Variation is normal rather than exceptional

This evolution does not make fraud decisions easier. It makes them more precise. By moving beyond rigid rules and thresholds, modern models aim to reduce uncertainty instead of reacting to it through blanket rejection.

Precision Over Permissiveness: What Advanced Actually Means

The idea that approving more good customers requires being more permissive is a common misunderstanding. In practice, permissiveness increases exposure without improving decision quality. What advanced fraud models change is not how much risk is accepted, but how clearly risk is understood.

Precision shifts the focus from rigid outcomes to confidence in interpretation. Instead of forcing uncertain behaviour into binary decisions, advanced models aim to recognise when behaviour is unfamiliar rather than fraudulent. This distinction matters because uncertainty and risk are not the same thing, even though they are often treated as such.

When decisions are made with greater confidence, controls do not need to be loosened to improve approvals. Legitimate customers pass because the system understands them better, not because it tolerates more risk. In this sense, “advanced” does not mean aggressive optimisation. It means fewer assumptions, clearer decisions, and less reliance on rejection as a substitute for understanding.

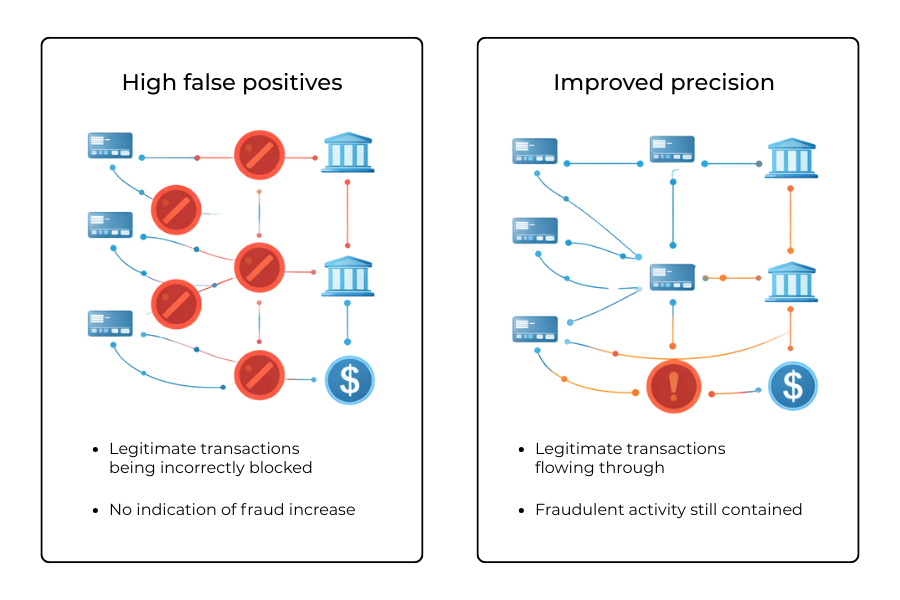

Reducing False Positives Without Increasing Fraud Exposure

False positives are often treated as an unavoidable side effect of fraud prevention. In reality, they are a sign that uncertainty is being managed through rejection rather than understanding. When systems cannot confidently interpret behaviour, declining the transaction becomes the safest option, even when there is no clear evidence of fraud.

Reducing false positives starts with separating uncertainty from actual risk. Many declines occur not because behaviour is dangerous, but because it is unfamiliar. Advanced fraud models are designed to recognise this difference. By learning how legitimate behaviour varies over time, they reduce the need to treat every deviation as a threat.

Misclassification carries costs beyond the immediate lost transaction. Customers who are declined without clear reason are less likely to return, and repeated friction can erode trust in the payment experience. Over time, this also affects approval performance more broadly, as transaction patterns become less consistent and harder for issuers to interpret.

Improved precision changes this dynamic. When fraud decisions are more accurate, legitimate traffic flows more smoothly, and the overall decision environment becomes more stable. This stability allows controls to remain firm where risk is real, while avoiding unnecessary rejection where it is not.

In practice, reducing false positives without increasing exposure tends to result in:

- Fewer legitimate customers being blocked due to ambiguous signals

- More consistent transaction behaviour reaching issuers

- Lower reliance on blanket controls to manage uncertainty

The outcome is not weaker protection, but better alignment between fraud decisions and actual risk. As false positives fall, approval quality improves, and merchants are able to grow without trading confidence for coverage.

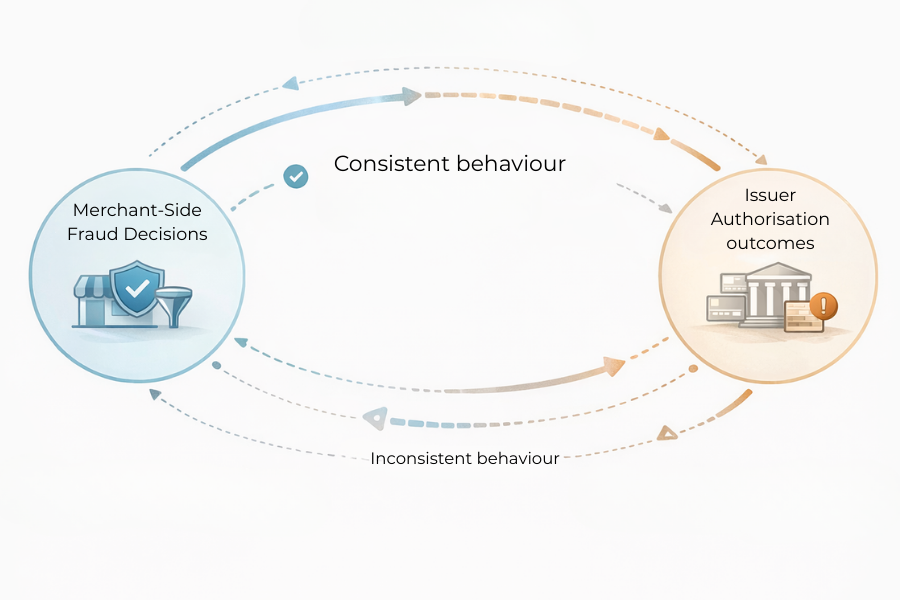

How Fraud Decisions Influence Issuer Behaviour Over Time

Fraud decisions made at the merchant level do not stop at the point of acceptance or decline. Over time, they shape the quality and consistency of the transaction streams that issuers see. This matters because issuers assess risk not only at the individual transaction level, but across patterns of behaviour that develop over repeated interactions.

Why issuers respond to decision consistency

Issuers are sensitive to predictability. When transactions from a merchant follow coherent patterns, authorisation systems are better able to distinguish normal variation from genuine risk. Over-defensive fraud controls disrupt this predictability. Legitimate transactions are blocked, retried, or rerouted in ways that create noisy behaviour upstream, making it harder for issuers to form stable expectations.

The feedback loop between fraud decisions and approvals

This creates a feedback loop. Conservative merchant-side decisions increase inconsistency in what reaches issuers, which can lead to more cautious issuer responses. In turn, merchants experience lower approval rates and may tighten controls further, reinforcing the cycle. What begins as an attempt to manage risk locally can end up degrading approval performance system-wide.

The approval signal merchants rarely measure

Advanced fraud models help break this loop by improving decision quality at the source. When fewer legitimate transactions are misclassified, traffic becomes more consistent and easier to interpret. Issuers respond to this clarity over time, often with higher confidence in authorisation decisions. The improvement is indirect, but meaningful: better fraud decisions lead to better approval environments, even when fraud exposure remains controlled.

Understanding this relationship reframes the value of advanced fraud modelling. Its impact is not limited to stopping bad transactions. It influences how the wider payments ecosystem interprets a merchant’s activity, shaping approval outcomes well beyond any single decision.

When Better Fraud Modelling Backfires

More sophisticated fraud models do not automatically lead to better outcomes. In some cases, they introduce new risks when precision is pursued without sufficient oversight or context. One common failure mode is overfitting. Models that learn too narrowly from historical behaviour can perform well in stable conditions, but struggle when customer behaviour shifts. What once improved accuracy can quickly become brittle.

Another risk emerges when decision logic becomes difficult to interpret. As models grow more complex, it can become harder for teams to understand why decisions are being made. This loss of interpretability complicates governance and makes it harder to respond when outcomes change unexpectedly. Instead of reducing uncertainty, complexity can obscure it.

There is also the danger of optimising for short-term approval gains at the expense of longer-term stability. If models are tuned aggressively to minimise declines without regard for behavioural drift, fraud exposure can rise quietly. The impact is often delayed, surfacing later through issuer responses or downstream controls rather than immediate losses.

These risks do not negate the value of advanced fraud models, but they highlight the need for balance. Precision improves approvals only when it is supported by continuous monitoring, clear accountability, and an understanding of how behaviour evolves. Without that discipline, even advanced models can undermine the confidence they are meant to build.

Conclusion

Approving more good customers has become less about relaxing controls and more about improving how decisions are made. As payment behaviour grows more complex, the cost of misclassification increases, and blunt fraud controls struggle to distinguish uncertainty from genuine risk.

Advanced fraud models address this by improving precision rather than permissiveness. By interpreting behaviour in context and reducing false positives, they allow legitimate customers to pass without increasing exposure. This shift improves not only immediate approval outcomes, but also the consistency of transaction behaviour that issuers rely on over time.

The result is a more stable approval environment built on confidence rather than caution. When fraud decisions are clearer and more accurate, merchants are better positioned to grow without trading trust for protection.

FAQs

1. Why are good customers still being declined despite strong fraud controls?

Because many fraud controls manage uncertainty through rejection. When behaviour does not fit expected patterns, legitimate customers can be declined even when there is no clear indication of fraud.

2. What does approving more good customers actually mean in a fraud context?

It refers to reducing false positives by improving decision precision, not by relaxing risk standards. The goal is clearer interpretation of behaviour, not higher tolerance for fraud.

3. How do advanced fraud models differ from traditional rule-based controls?

Advanced models focus on behavioural patterns and context over time, rather than isolated signals and fixed thresholds. This allows them to distinguish unfamiliar behaviour from genuinely risky activity.

4. Do advanced fraud models increase fraud exposure?

Not when applied correctly. By reducing misclassification and improving confidence in decisions, they can maintain or even improve fraud outcomes while allowing more legitimate transactions through.

5. Why are false positives considered a structural problem rather than an edge case?

Because modern payment behaviour frequently deviates from historical norms. Systems built around rigid assumptions struggle in this environment, leading to consistent misclassification rather than occasional error.

6. How do fraud decisions at the merchant level affect issuer approvals?

Merchant-side decisions shape the consistency of transaction streams that issuers see. Clearer, more predictable behaviour tends to build issuer confidence over time, supporting higher approval rates.

7. What role does uncertainty play in fraud decisioning?

Uncertainty arises when behaviour cannot be confidently interpreted. Traditional systems often respond by declining transactions, while more advanced models aim to reduce uncertainty through better context.

8. Can advanced fraud models fail or create new risks?

Yes. Overfitting, loss of interpretability, or aggressive optimisation can undermine decision quality if not properly governed. Precision must be balanced with oversight and adaptability.

9. Why doesn’t tightening fraud controls always reduce risk?

Because tighter controls often increase false positives without improving accuracy. This can degrade transaction consistency and indirectly harm approval performance.

10. Is improving approval rates primarily a fraud problem or a growth problem?

It is increasingly a decision-quality problem. Approval outcomes depend on how well systems distinguish between risk and ambiguity, not just on how aggressively fraud is blocked.

11. How do advanced fraud models change the role of fraud systems?

They shift fraud systems from being purely defensive layers to becoming part of the approval infrastructure, influencing which customers are trusted and how consistently behaviour is interpreted.

12. Why is precision more valuable than permissiveness in fraud decisioning?

Because permissiveness increases exposure, while precision improves confidence. Better decisions allow legitimate customers through without weakening protection.