International expansion changes what payments represent inside a business. What begins as a contained function in one market becomes an operational system spanning regions, regulations, currencies, and customer behaviour. At that point, payments are no longer something that can be set up once and left to run.

Expansion is often approached as an enablement task: adding local payment methods, meeting new regulatory requirements, or connecting to additional providers. While necessary, these steps do not address how payments are actually managed once multiple markets are live. As complexity grows, the challenge shifts from capability to coordination, visibility, and control.

Without a clear operational structure, differences between markets start to compound. Settlement timelines diverge, reconciliation effort increases, and performance issues become harder to interpret. Payments may still function, but with rising friction and cost.

Merchants that expand successfully recognise this early. They treat payments not just as a technology stack, but as an operational discipline that must be deliberately structured as the business grows internationally.

- International Expansion Turns Payments Into an Operational System

- What Payment Operations Actually Means in a Multi-Market Context

- Centralised vs Localised Payment Ownership

- How Merchants Coordinate Payment Behaviour Across Markets

- Settlement, Liquidity and Reconciliation as Expansion Stress Points

- Preventing Fragmentation as Markets Multiply

- Merchant Readiness Check: Are Your Payment Operations Structured for Expansion?

- Conclusion

- FAQs

International Expansion Turns Payments Into an Operational System

In a single market, payment activity often behaves like a linear flow. Transactions are authorised, settled, and reconciled through a familiar set of paths. Exceptions exist, but they are manageable because patterns are relatively stable. Expansion disrupts that stability. Each new market introduces different issuer behaviour, regulatory expectations, settlement mechanics, and customer payment habits, all interacting with the same underlying system.

As this variation accumulates, payments stop behaving like a single process and start behaving like a set of interdependent operations. Decisions made in one area, such as authentication handling or settlement configuration, begin to affect outcomes elsewhere. Issues no longer present as isolated incidents. They appear as patterns that span markets and time, often without a single, obvious cause.

This is the point at which informal handling breaks down. Relying on individual teams to respond to issues as they arise becomes inefficient, and sometimes risky. Without structure, merchants struggle to distinguish between market-specific anomalies and systemic problems. The result is slower diagnosis, inconsistent responses, and increasing operational effort just to maintain baseline performance.

Treating payments as an operational system means acknowledging that expansion creates ongoing coordination work. Responsibilities need to be clear, information needs to flow reliably, and behaviour across markets needs to be interpretable as part of a whole.

What Payment Operations Actually Means in a Multi-Market Context

As merchants expand internationally, the term payment operations starts to mean something very different from simply running transactions. It moves beyond processing and into the day-to-day work required to keep payments predictable across markets that behave differently.

In practice, payment operations cover how authorisation outcomes are monitored when issuer behaviour varies by region, how authentication challenges are applied in regulated and non-regulated environments, how settlement timelines are tracked across different clearing cycles, and how disputes and refunds are handled when customer expectations and legal frameworks differ.

Each of these elements may work acceptably in isolation. Together, however, they form a system that requires coordination to remain manageable.

The challenge is that these operational components rarely scale evenly. Some markets generate more authentication friction, others introduce settlement delays or reconciliation complexity. Without a clear operational view, these differences are easy to misread as local issues rather than symptoms of a broader structural problem.

Payment operations, in this sense, are about maintaining coherence. They provide the mechanisms through which behaviour can be observed, compared, and understood across regions. When this layer is missing or underdeveloped, merchants often find themselves reacting to problems without knowing whether they are market-specific or systemic.

Centralised vs Localised Payment Ownership

As payment operations grow across markets, one of the earliest structural decisions merchants face is where ownership sits. This is not a tooling question, but an organisational one. The way responsibility is distributed has a direct impact on how consistently payments behave and how quickly issues can be addressed.

Central Control Models

In a centralised model, payment decisions are owned by a single team or function. This approach prioritises consistency. Transaction behaviour, authentication rules, and reporting standards are aligned across markets, making it easier to compare performance and spot emerging issues. Central ownership also reduces the risk of duplicated effort or conflicting configurations developing in parallel.

The limitation of central control is sensitivity to local nuance. Market-specific issuer behaviour or regulatory interpretation may not be immediately visible to a central team. If feedback loops are weak, decisions can lag behind local reality, creating friction that feels avoidable to regional teams.

Local or Regional Ownership Models

Localised ownership places more decision-making closer to individual markets. This can improve responsiveness to regional differences and allow adjustments to be made quickly when behaviour shifts. For markets with distinct payment norms, local input can be essential.

The risk, however, is fragmentation. Without strong coordination, local changes accumulate in ways that make the overall system harder to understand. Reporting becomes inconsistent, operational practices diverge, and knowledge is siloed within regions. Over time, the payments operation can feel less like a single system and more like a collection of loosely connected setups.

In practice, successful merchants tend to balance these models. Central ownership establishes operating principles and guardrails, while local teams provide market-specific insight. How this balance is structured determines whether payment operations remain coherent as expansion continues.

How Merchants Coordinate Payment Behaviour Across Markets

Once multiple markets are live, coordination becomes more important than configuration. The challenge is no longer enabling payments in a new region, but ensuring that payment behaviour remains understandable when the same transaction profile produces different outcomes across markets.

Coordination starts with interpretation. Issuer responses, authentication challenges, and decline patterns need to be reviewed in a way that allows differences to be compared rather than treated as isolated events. Without a shared view, teams often respond locally to symptoms, adjusting processes to resolve immediate issues. While this can restore short-term performance, it also increases divergence between markets.

Over time, these local adjustments create complexity that is hard to track. Payment behaviour begins to depend on historical decisions rather than current intent. When conditions change, it becomes difficult to predict how the system as a whole will respond.

Merchants that manage this well focus on consistency in decision-making, even when outcomes differ by market. Market-specific behaviour is expected, but it is surfaced and reviewed within a shared operational context rather than managed in isolation. Coordination becomes the mechanism that keeps payment operations cohesive as expansion continues.

Settlement, Liquidity and Reconciliation as Expansion Stress Points

Settlement is often where the operational impact of expansion becomes most visible. As new markets are added, payment flows that once settled along a single, predictable timeline begin to split into multiple paths. Different currencies, clearing cycles, and local practices introduce variation in when funds move and when they become usable.

Liquidity pressure tends to follow. Even when overall revenue grows, funds may be held longer in certain markets or released unevenly across regions. Timing gaps complicate planning, particularly when growth is uneven. These effects are rarely dramatic in isolation, but together they reduce confidence in forecasts and increase the effort required to manage working capital.

Reconciliation compounds this strain. Expansion increases the number of entities, accounts, and reporting formats involved in the payment lifecycle. Differences in settlement timing and data structure make it harder to align transactions, fees, refunds, and chargebacks into a single, coherent view. Teams often spend more time resolving discrepancies than analysing performance or risk.

Without structure, these issues are treated as local inconveniences rather than signals of systemic complexity. Merchants that organise payment operations deliberately are better able to anticipate these pressures and prevent routine expansion from turning into persistent operational drag.

Preventing Fragmentation as Markets Multiply

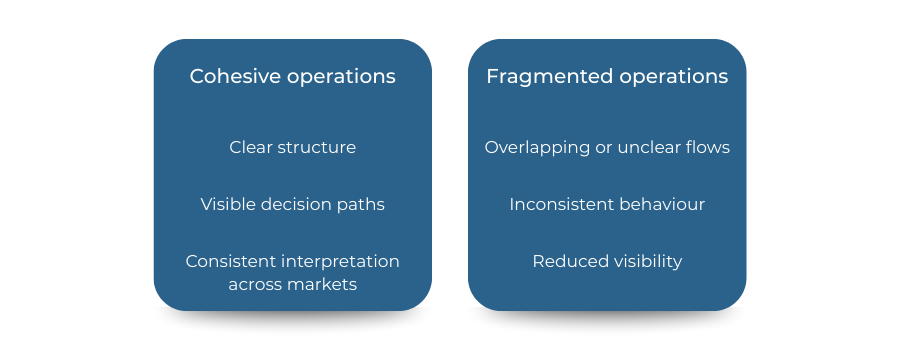

Fragmentation rarely arrives all at once. It develops quietly as market-specific decisions accumulate over time. Small adjustments are made to accommodate local requirements or issuer behaviour, often with good intent. Without a unifying operational structure, those adjustments begin to pull payment behaviour in different directions.

The early signs are subtle. Reporting no longer aligns cleanly across regions. Similar transactions produce different outcomes without an obvious explanation. Some markets require disproportionate manual attention, while others appear stable.

Fragmentation becomes a problem when it limits understanding. Once payment behaviour can no longer be interpreted as part of a single system, it becomes harder to decide whether performance changes are market-specific or systemic. Operational effort increases, not because payments are failing, but because they are behaving inconsistently.

Preventing this does not mean forcing uniformity. Variation is inevitable. The objective is to ensure that differences are intentional, visible, and governed. When divergence is tracked centrally, it remains manageable.

Merchant Readiness Check: Are Your Payment Operations Structured for Expansion?

By the time multiple markets are live, payment operations are already carrying the weight of earlier decisions. Readiness at this stage is not about ambition, but about whether the existing structure allows behaviour to be understood and managed as variation increases.

A useful sense check is whether payment behaviour can be reviewed across markets without relying on local interpretation alone. Responsibility for payment outcomes should be clear between central and regional teams, and settlement timing should remain visible as currencies and regions increase. When issues arise, it should be possible to determine whether they are market-specific or systemic without extensive manual investigation.

If these questions are difficult to answer, expansion may still continue, but operational strain is likely to increase. In most cases, the friction that appears later is not caused by growth itself, but by the absence of structure to absorb it.

Conclusion

International expansion places a different kind of demand on payment systems. What begins as a set of integrations becomes an operational network that must absorb variation across markets, regulations, and customer behaviour.

Merchants that struggle during expansion are rarely limited by capability. More often, they are constrained by operating models that were never designed to coordinate payment behaviour across regions. Without clear ownership, visibility, and governance, differences accumulate until they are difficult to interpret or control.

Structuring payment operations deliberately allows merchants to treat variation as an expected condition rather than a disruption. The success of international expansion in payments is less about reaching new markets quickly, and more about sustaining clarity as the business grows across borders.

FAQs

1. Why do payment operations become more complex during international expansion?

Because expansion introduces variation rather than just volume. Different issuer behaviour, settlement timelines, regulatory expectations, and customer habits interact with the same payment system, increasing coordination and oversight requirements.

2. At what point do merchants typically need formal payment operations?

Payment operations usually become necessary once merchants operate across multiple markets. At that stage, informal handling breaks down and payments start behaving as an interconnected operational system rather than a single flow.

3. Is international payment expansion mainly a technical challenge?

No. While technical enablement is required, the greater challenge is operational. Structure, ownership, and visibility determine whether payment behaviour remains understandable as markets multiply.

4. What is meant by payment operations in a multi-market context?

Payment operations refer to the ongoing management of authorisation outcomes, authentication behaviour, settlement timing, reconciliation, and dispute handling across markets that behave differently.

5. Why do settlement and liquidity issues increase during expansion?

Different markets introduce multiple clearing cycles, currencies, and release timings. Without structure, these variations reduce predictability and make cash flow harder to manage as complexity grows.

6. How does payment ownership affect international operations?

Ownership determines how consistently decisions are made and how quickly issues are resolved. Centralised ownership improves coherence, while local ownership improves responsiveness. Most merchants require a balance of both.

7. What causes payment operations to fragment over time?

Fragmentation usually develops from small, market-specific adjustments made without central oversight. Over time, these decisions accumulate and make payment behaviour harder to interpret as a single system.

8. Why is coordination more important than configuration once markets are live?

After enablement, the challenge shifts to understanding why outcomes differ across regions. Coordination ensures differences are reviewed collectively rather than managed in isolation.

9. How can merchants tell whether payment issues are local or systemic?

This depends on structure and visibility. When payment behaviour can be compared across markets within a shared operational view, patterns become easier to identify and diagnose.

10. Does successful international expansion require uniform payment behaviour across markets?

No. Variation is inevitable. The goal is not uniformity, but ensuring differences are intentional, visible, and governed rather than emerging accidentally.

11. What is the biggest operational risk merchants underestimate during expansion?

The gradual loss of clarity. Payments may continue to work, but without structure, understanding why performance changes becomes increasingly difficult.

12. When should merchants reassess how their payment operations are structured?

Reassessment is most valuable before entering new markets or significantly increasing regional complexity. Waiting until operational strain is visible often means reacting rather than designing deliberately.