Checkout performance in 2026 is no longer defined by how many payment methods a merchant can offer. For global businesses, it is increasingly shaped by whether the right methods appear at the right moment, in the right markets, and behave predictably once a customer commits to pay. As Alternative Payment Methods (APMs) have become mainstream and in many markets, their impact on conversion, trust, and post-checkout confidence has grown significantly.

Many merchants have responded to this shift by expanding coverage aggressively, adding digital wallets, bank-based payments (A2A), and local methods market by market. In practice, this more is better approach often creates the opposite effect. Overloaded checkouts reduce visual clarity, inconsistent refund behaviour introduces customer uncertainty, and operational complexity grows faster than the performance gains. What looks like hyper-localisation on paper often feels like friction to the customer.This is why leading global merchants are rethinking their approach. Instead of treating APMs as a growing list of integrations, they are designing Balanced Portfolios that prioritise relevance, sequencing, and governance. In 2026, checkout performance improves not when more options are shown, but when payment choice feels familiar, controlled, and reliable across the entire purchase journey.

- Why Alternative Payment Methods Have Become a Checkout Performance Lever

- What a Balanced APM Strategy Actually Means in 2026

- Where Global APM Rollouts Typically Go Wrong

- Designing the Balanced APM Portfolio

- Checkout Design and Method Surfacing: Why Presentation Matters

- The Operational Layer Merchants Underestimate

- Governing an APM Strategy as You Scale Globally

- Conclusion

- FAQs

Why Alternative Payment Methods Have Become a Checkout Performance Lever

For a long time, alternative payment methods were treated as a localisation feature rather than a core performance driver. Cards were assumed to be the global default, with APMs added primarily to meet niche regional expectations or to support edge cases (like unbanked populations). In 2026, that hierarchy has fundamentally shifted. In major markets from Brazil’s Pix to the Netherlands’ iDEAL and India’s UPI APMs now shape how customers judge trust, control, and effort at the point of payment.

This change is rooted in consumer behaviour rather than just technology. Customers increasingly arrive at the checkout with an existing, hardened preference, whether that is a familiar biometric wallet, a direct bank-based flow, or a regulated deferred payment option. When that preference is visible and works as expected, the checkout feels intuitive. When it is missing or buried behind a More Options dropdown, the experience feels unfamiliar, even if card rails are technically available. The result is hesitation rather than rejection, which often shows up in analytics as abandonment rather than declines.

APMs also influence performance because they change how risk and confidence are perceived. Wallets and bank-based payments shift authentication, credential management, and confirmation away from the merchant interface and onto the customer’s own device. In cross-border contexts, this perceived control matters as much as price or delivery speed. A customer in Germany buying from a US merchant feels safer paying via PayPal or a local bank transfer than entering raw card details.

As APM usage grows, their role in checkout performance becomes structural. They no longer act as a fallback for cards but as primary routes to completion. Merchants that recognise this shift design checkouts around customer expectation, not payment hierarchy, and that design choice increasingly determines conversion outcomes.

What a Balanced APM Strategy Actually Means in 2026

A balanced APM strategy in 2026 is not about maximising coverage to hit a vanity metric. It is about designing a payment mix that improves completion without introducing new points of confusion, failure, or operational strain. Balance is achieved when payment choice feels natural to the customer and manageable for the business, rather than impressive on a feature list.

The distinction matters because APMs behave very differently once a transaction moves beyond the Pay button. Some methods confirm instantly (Instant Payment rails), while others remain pending for hours. Some support partial refunds cleanly, others require full reversals. Some shift authentication and liability away from the merchant (like Open Banking), while others introduce additional reconciliation and support complexity. Treating all APMs as interchangeable options ignores these operational realities and often leads to performance gains at checkout being offset by massive friction later in the journey.

In practice, balance is about portfolio design rather than method accumulation. Merchants that perform well globally define which methods are genuinely relevant in each market and how they should be presented. They also understand how those methods interact with risk controls, refunds, settlement timing, and customer expectations. The goal is not to offer every possible way to pay, but to ensure that the methods offered behave predictably and support confidence from selection through to post-purchase resolution.

A balanced APM strategy typically considers the following factors together, rather than in isolation:

- Market relevance: Is this method a top-three preference for my specific demographic?

- Sequencing: How are methods surfaced? (e.g., Apple Pay on iOS, Google Pay on Android).

- Risk profile: How does this method handle disputes and fraud liability?

- Refund characteristics: Can I automate returns, or will this create a support ticket?

- Operational visibility: Does this method integrate cleanly with my central reconciliation ledger?

When these elements are aligned, APMs enhance checkout performance without creating hidden costs. When they are not, performance gains tend to be short-lived.

Where Global APM Rollouts Typically Go Wrong

Many global APM initiatives struggle not because the methods themselves are flawed, but because they are introduced without enough consideration for how customers actually choose, interpret, and trust payment options. The most common failures tend to surface quietly, through lower completion rates or higher post-checkout friction, rather than through obvious technical errors.

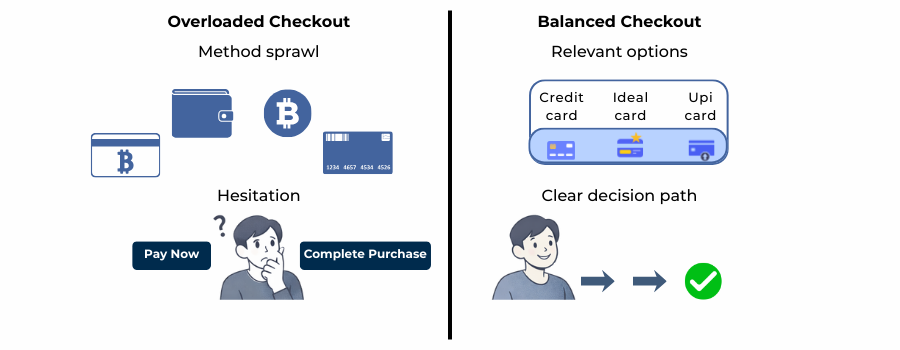

Method sprawl without relevance

A frequent mistake is assuming that more choice automatically leads to better performance. In reality, an overcrowded checkout often called the NASCAR effect due to the clutter of logos forces customers to stop and evaluate, breaking momentum at the most sensitive point of the journey. When unfamiliar or rarely used methods are presented alongside dominant local options, visual clarity is lost. Customers hesitate, second-guess their decision, or abandon entirely, even though a suitable method was technically available.

Identical checkout design across markets

Another issue arises when merchants deploy the same checkout structure everywhere. Payment preferences are highly local, shaped by habit and trust rather than logic. A layout that performs well in the UK (heavy on cards and wallets) may feel unintuitive in the Netherlands (heavy on iDEAL) or Brazil (heavy on Pix). When local methods are hidden behind generic labels or secondary flows, customers perceive the checkout as foreign or unreliable, particularly in cross-border scenarios.

Hidden operational and trust debt

Problems also emerge after payment. Some APMs introduce delayed confirmations, complex refund paths, or fragmented settlement reporting. If these behaviours are not clearly understood and communicated, customer confidence erodes once something changes or goes wrong. Over time, what appeared to be a conversion win at checkout becomes a source of disputes, support tickets, and internal friction. In each case, the issue is not the presence of APMs, but the absence of deliberate design around how they are chosen, presented, and managed.

Designing the Balanced APM Portfolio

A balanced APM portfolio recognises that different payment methods solve different problems, and that no single option performs equally well across markets, basket sizes, or customer segments. The objective is not to elevate one method over others, but to understand where each one contributes to checkout performance and where it introduces trade-offs that must be managed.

Cards as the universal baseline

Cards remain the most universally accepted payment method and continue to perform strongly in familiar, domestic contexts. They offer flexibility, clear confirmation, and established refund processes. However, in cross-border scenarios, cards are more sensitive to issuer caution, authentication challenges (3DS), and currency perception. For global merchants, cards are essential, but they are no longer sufficient on their own to deliver consistent performance everywhere.

Wallets for speed and familiarity

Digital wallets (Apple Pay, Google Pay, Click to Pay) have become powerful performance drivers because they reduce effort and reinforce trust. Customers recognise the interface, credentials are already stored, and authentication often happens via biometrics (Passkeys) outside the merchant’s environment. This can significantly reduce friction at checkout. The trade-off is dependency. Wallets introduce platform-specific rules around disputes, refunds, and visibility, which merchants must factor into their overall payment strategy.

Bank-based payments for certainty and cost control

Account-to-account (A2A) and bank-based payment methods offer predictability that cards and wallets sometimes cannot. They reduce chargeback exposure and often provide faster settlement via rails like SEPA Instant or Faster Payments. In markets where these methods are well understood, particularly in parts of Europe, they can materially improve confidence. Their limitation is familiarity. Where customers do not expect them, adoption remains low, regardless of technical advantages.

BNPL as a selective performance lever

Buy Now, Pay Later (BNPL) options can lift conversion in higher-value baskets by reducing upfront friction. Used selectively, they improve accessibility without overwhelming the checkout. Used indiscriminately, they complicate refunds, returns, and customer expectations, especially as 2026 regulations require stricter affordability checks. In a balanced portfolio, BNPL is positioned as a strategic option, not a default.

Checkout Design and Method Surfacing: Why Presentation Matters

Even a well-chosen APM mix can underperform if it is presented poorly. In global checkouts, performance is often shaped less by which methods are enabled and more by how those methods are surfaced to the customer at the moment of decision. Presentation influences confidence, speed, and perceived effort, all of which directly affect completion rates.

A common mistake is treating the checkout as a catalogue. Showing every available method at once forces customers to evaluate options rather than act on instinct. In markets where payment preferences are strong, this hesitation is enough to break momentum. High-performing merchants instead design for relevance. The most likely methods (based on IP address, device, and currency) appear first, while secondary options remain accessible without dominating the experience.

Surfacing also needs to adapt to context. Device type, customer history, basket value, and geography all influence which payment route is most appropriate. Static checkouts ignore these signals and leave performance on the table. Dynamic sequencing often driven by AI orchestration layers allows familiar methods to feel native rather than imposed. For example, an iPhone user in France should see Apple Pay and Cartes Bancaires immediately, while an Android user in Poland sees Google Pay and BLIK.

Clarity does not end at selection. Customers need to understand what will happen next: whether confirmation is instant, whether redirection will occur, and how payment status will be communicated. When fallback paths are unclear or hidden, trust erodes quickly. In 2026, effective checkout design treats method presentation as a behavioural system, not a visual preference.

The Operational Layer Merchants Underestimate

For many global merchants, checkout performance is still measured at the point of authorisation. What happens after payment is often treated as a downstream operational concern, owned by finance or support teams rather than by the checkout team itself. In practice, this separation is artificial. Customers judge payment reliability over the full lifecycle, especially when something changes.

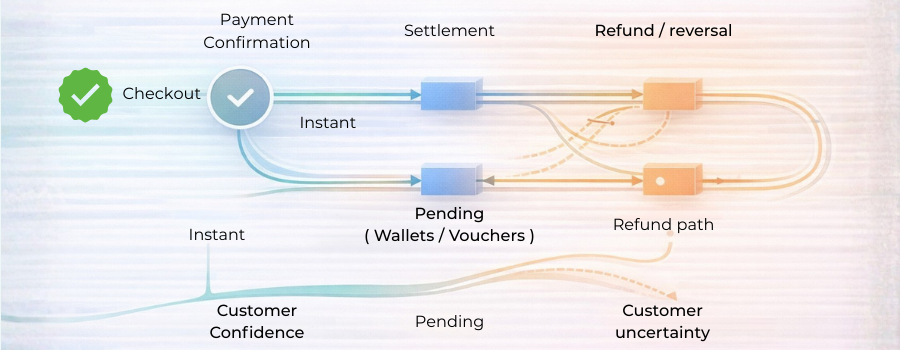

APMs behave very differently once a transaction moves beyond confirmation. Some methods settle instantly (A2A), others remain pending (traditional vouchers or asynchronous wallets). Some support partial refunds cleanly, while others require full reversals or manual intervention via IBAN collection. When these differences are not anticipated, merchants struggle to explain outcomes clearly, and customers are left uncertain about where their money is and when it will return.

Refund handling is where this tension becomes most visible. Delays are not always the issue; unpredictability is. When customers do not understand the timing, route, or conditions of a refund, confidence breaks and disputes follow. This is particularly damaging in cross-border scenarios, where expectations already vary.

Settlement and reconciliation add another layer of complexity. As APMs scale across regions, reporting becomes fragmented, making it harder to maintain a single view of performance and risk. Merchants that improve checkout outcomes sustainably are those that design APM strategies with operational behaviour in mind from the outset, recognising that post-checkout clarity is inseparable from checkout performance itself.

Governing an APM Strategy as You Scale Globally

As alternative payment methods mature from tactical additions into core checkout infrastructure, governance becomes the difference between sustained performance and gradual degradation. Without clear ownership and discipline, even well-designed APM strategies tend to drift as markets expand, teams change, and new methods are introduced opportunistically.

Effective governance starts with portfolio intent. High-performing merchants are explicit about why each method exists, which customer behaviour it serves, and what conditions would justify expanding, deprioritising, or removing it. This prevents the gradual accumulation of low-impact methods that add complexity without improving outcomes. This is often managed through a Keep/Kill Quarterly Review, where methods that fail to meet volume or conversion thresholds are deprecated.

Ongoing performance review is equally important. Conversion lift alone is no longer a sufficient success metric. Merchants increasingly evaluate APMs across a broader set of signals: refund rates, dispute patterns, settlement predictability, and support impact. Reviewing these factors together ensures that short-term checkout gains do not mask longer-term operational costs.

Finally, change control matters. Checkout layouts, routing logic, and method sequencing often evolve incrementally, sometimes without clear visibility. Governance frameworks that require structured review before changes are made help preserve consistency and prevent accidental regressions. In 2026, global merchants that treat APM strategy as a governed system rather than a collection of integrations are far better positioned to scale without sacrificing checkout performance.

Conclusion

In 2026, checkout performance for global merchants will no longer improve by simply expanding payment choice. It is shaped by how well alternative payment methods are selected, presented, and governed as part of a single system. When APMs are added without clear intent, performance gains tend to be short-lived, offset by confusion, operational strain, and declining trust.

Merchants that see sustained improvement approach APMs as a Balanced Portfolio. They prioritise relevance over volume, design checkout flows around customer expectation, and account for how each method behaves beyond the moment of payment. This discipline reduces friction not only at checkout, but across refunds, settlement, and support interactions that influence long-term confidence.

As global commerce becomes more fragmented in terms of markets, methods, and customer behaviour, the role of payment strategy becomes more central. A balanced APM strategy does not eliminate complexity, but it manages it deliberately. In doing so, it allows checkout performance to improve in ways that are predictable, scalable, and resilient as merchants grow across regions.

FAQs

1. What does a balanced APM strategy actually mean for global merchants?

A balanced APM strategy means offering the right payment methods for each market, rather than the maximum number possible. It focuses on relevance, checkout sequencing, and predictable post-payment behaviour, so conversion improves without adding operational or trust issues later.

2. Why does adding more payment methods sometimes reduce checkout performance?

Because too many options create hesitation. Overcrowded checkouts reduce visual clarity and force customers to evaluate rather than act. This often leads to abandonment, even when a suitable payment method is available.

3. How do APMs influence customer trust at checkout?

APMs signal familiarity and control. When customers see a method they already use and trust, such as a local bank payment or wallet, they feel safer completing the transaction, especially in cross-border purchases.

4. Are alternative payment methods replacing cards globally?

No. Cards remain a universal baseline, but they are no longer sufficient on their own. In many markets, wallets and bank-based payments have become primary routes to completion, particularly where customers expect them by default.

5. Why do APMs behave so differently after checkout?

Each APM has its own confirmation, settlement, and refund mechanics. Some confirm instantly, others remain pending. Some support partial refunds easily, while others require full reversals or manual processes. These differences directly affect customer confidence after payment.

6. How do refunds impact checkout performance?

Refund behaviour shapes trust. Customers are more likely to dispute payments when refund timing or method is unclear, even if the refund is technically allowed. Predictability matters more than speed in most cases.

7. What is the biggest mistake merchants make when rolling out APMs globally?

Treating all markets the same. Payment preferences are highly local. A checkout design that works in one country can feel confusing or unreliable in another if dominant local methods are hidden or deprioritised.

8. Why does checkout presentation matter as much as method selection?

Because customers choose instinctively. How methods are surfaced, ordered, and contextualised influences confidence and speed. Showing everything at once often hurts performance, while sequencing by likelihood improves completion.

9. How does a balanced APM strategy reduce operational complexity?

By limiting methods to those that genuinely add value and by understanding their downstream behaviour. This reduces fragmented reporting, reconciliation issues, and support overhead caused by low-volume or poorly understood methods.

10. Why is governance critical as APMs scale?

Without governance, payment portfolios drift. New methods get added opportunistically, checkout layouts change incrementally, and performance degrades quietly. Governance ensures that APM decisions remain intentional and aligned with business outcomes.

11. How should merchants evaluate APM performance beyond conversion rates?

By looking at refund rates, dispute patterns, settlement predictability, and support impact alongside conversion. A method that boosts checkout completion but creates operational friction may reduce overall performance over time.

12. Can a balanced APM strategy eliminate complexity altogether?

No. Global payments are inherently complex. A balanced strategy does not remove that complexity, but it manages it deliberately, ensuring checkout performance improves in a way that is predictable, scalable, and resilient.