By 2026, merchants and PSPs will be operating in a very different payment environment from the one shaped by card rails alone. Card schemes still dominate consumer spending, but rising scheme fees, stricter issuer risk models, Strong Customer Authentication (SCA) friction and cross-border volatility are forcing payment teams to reassess their dependency on cards as the default option for every use case.

At the same time, account-to-account (A2A) payments have moved from “experimental” to strategic. Open banking payment initiation, variable recurring payments and domestic instant payment schemes are maturing across Europe, the UK, APAC and LATAM. In the EU, the combination of PSD3, the new Payment Services Regulation (PSR) and the Instant Payments Regulation (IPR) is pushing banks and PSPs to make instant euro credit transfers the norm rather than the exception, with strict expectations on speed, availability and screening.For merchants, this creates both opportunity and complexity. A2A rails can reduce costs, accelerate settlement and simplify fraud exposure, but they also change how disputes, refunds, UX and liability work. The 2026 A2A playbook is therefore not “cards versus A2A”, but a framework for deciding which rail to use for which journey: when cards remain optimal, when open banking or instant payments should be prioritised, and how PSPs and gateways should orchestrate all three within one coherent payment strategy.

- The 2026 Payments Landscape: Cards, A2A & Instant Rails Converge

- Cards in 2026: Strengths, Weaknesses & Strategic Role

- Open Banking A2A: PIS, VRP & Bank API Infrastructure (2026 Upgrade)

- Instant Payment Rails: FPS, SEPA Instant, RTP, PIX, UPI, PayTo & PayNow/PromptPay

- Decision Matrix: Cards vs A2A vs Instant Payments

- Fraud, Disputes & Liability Across Each Rail

- Customer Experience (UX) Comparison: Behaviour & Friction by Rail

- PSP / Gateway Roadmaps: Supporting A2A in 2026

- Merchant Use Case Scenarios: Choosing the Right Rail per Vertical

- Corridor-Level Strategy: How Rail Performance Varies Across Regions

- Merchant A2A Strategy Playbook (2026)

- KPI Framework (A2A Adoption %, Refund Time, Dispute Rate, Net Cost)

- Conclusion

- FAQs

The 2026 Payments Landscape: Cards, A2A & Instant Rails Converge

For most of the past decade, digital commerce has been built on a familiar foundation: card networks as the default method of payment, supported by acquirers, gateways and fraud systems that all evolved around the same rails. That model still accounts for the majority of European and UK eCommerce volume in 2026 but the structural forces shaping merchant payment decisions have shifted dramatically.

Why Cards Are Under Pressure

Card rails remain the most universal option for cross-border commerce, but their economics and reliability are increasingly strained. Issuers have tightened risk controls, introducing more behavioural scoring, stricter velocity checks and more aggressive SCA requirements. Scheme fees and cross-border interchange continue to rise. And as chargeback volumes grow in high-risk sectors, merchants are questioning the long-standing assumption that cards should be the default option for every customer journey.

The Rise of A2A Payments

In contrast, account-to-account (A2A) payments, both via open banking payment initiation and domestic instant payment schemes, are becoming operationally viable alternatives. Over the past two years, API uptime has improved, authentication journeys have simplified, and settlement times have shifted from next-day to real-time across major European markets.

The EU’s new Instant Payments Regulation (IPR) requires banks to offer mandatory instant euro credit transfers at the same price as standard transfers and to execute them within 10 seconds. When combined with the broader reforms under PSD3 and the Payment Services Regulation (PSR), A2A begins to compete structurally with cards not only on price, but on speed, reliability and transparency.

Emergence of Instant Payment Rails as Global Standards

Beyond Europe, regional schemes such as India’s UPI, Brazil’s PIX, Thailand’s PromptPay, Singapore’s FAST and the UK’s Faster Payments System (FPS) are expanding both domestically and cross-border. Settlement speeds of under 5 seconds, consumer familiarity with bank-to-bank transfers and low transaction fees are reshaping payment preferences, especially in mobile-first regions.

As these systems gain traction, they create a new expectation: that money should move instantly, with no intermediaries adding cost or friction.

A Converging Multi-Rail Environment

By 2026, the result is a payment landscape where no single rail is universally dominant. Instead:

- Cards remain strong for high-value, cross-border and dispute-sensitive categories.

- Open banking A2A excels in domestic eCommerce, bill payments and recurring use cases.

- Instant payment rails dominate in emerging markets and high-velocity, low-margin sectors.

For merchants and PSPs, this convergence requires a more deliberate strategy. Rail selection can no longer be reactive. It must be engineered, every corridor, product type and risk profile demands a specific decision.

Cards in 2026: Strengths, Weaknesses & Strategic Role

Despite the rise of A2A and instant payment schemes, cards remain the most established and commercially mature payment rail for global merchants in 2026. Their ubiquity, dispute rights, established fraud infrastructure and broad issuer acceptance mean that businesses cannot simply abandon cards, even as regulatory pressure and scheme economics evolve. Understanding the role cards play in a multi-rail environment is therefore essential to building the 2026 payment strategy.

The Strengths That Keep Cards Relevant

Cards continue to dominate for one fundamental reason: they work almost everywhere. The combination of near-universal consumer adoption, deep issuer trust and decades of risk-management optimisation makes cards uniquely resilient across corridors.

The strongest advantages include:

1. Consumer familiarity and ease of use

Cards still deliver one of the smoothest checkout flows, especially when exemptions remove SCA friction. Stored card credentials underpin low-friction repeat purchases and subscription lifecycles.

2. High global acceptance coverage

No other rail matches the cross-border reach of card networks. For travel, digital goods, marketplaces and cross-border commerce, cards remain unparalleled.

3. Structured dispute and refund mechanisms

Chargeback rights, although costly, offer consumer protection frameworks that many A2A rails lack. For sectors where disputes are frequent, this structure reduces friction and operational confusion.

4. Mature fraud detection and issuer risk systems

Card issuers rely on decades of historical behavioural data, enabling more predictable scoring, clearer velocity controls and refined fraud decisioning. This reliability stabilises approval rates in established markets.

Where Cards Are Losing Ground

The challenges are becoming harder to ignore. Many merchants are reassessing their card dependency due to:

1. Rising scheme and cross-border fees

Interchange caps differ regionally, scheme fees continue to increase, and FX markups in cross-border transactions remain materially higher than A2A alternatives.

2. Increasing issuer-driven friction

Tighter risk controls, more behavioural analytics and stricter SCA logic result in soft declines and increased challenge rates, particularly in high-risk sectors.

3. Complex authentication flows

Even with 3DS improvements, authentication continues to cause drop-offs. A2A and instant payments using bank biometrics offer more predictable authentication in some markets.

4. High operational burden from chargebacks

While disputes are structured, they are expensive and resource-intensive. High-risk verticals face escalating fraud-related chargebacks and scheme monitoring pressures.

Where Cards Still Outperform A2A and Instant Payments

Despite the pressures, cards retain clear superiority in several commercial areas:

- Travel and airlines: Because of dispute rights, multi-leg journeys and high-value ticketing.

- High-risk sectors: Where issuers have robust fraud models compared to early-stage A2A fraud controls.

- Cross-border transactions: Where A2A availability is limited or fragmented.

- Subscription initiation: Where card-on-file is simple, recognised and trusted.

- Refund-heavy journeys: Where structured dispute frameworks reduce friction.

The Strategic Role of Cards in a Multi-Rail 2026 Payment Mix

Cards are no longer the default rail for every customer journey, but they are still a core component of a merchant’s multi-rail strategy. In 2026, their role shifts from “one-size-fits-all” to:

- Primary rail for cross-border and high-dispute environments

- Value anchor for recurring lifecycle payments

The key is not whether cards will remain; they will. The question for merchants is how to rebalance volume across cards, A2A and instant payments to stabilise costs, reduce friction and align with the behaviour of 2026 issuers and consumers.

Open Banking A2A: PIS, VRP & Bank API Infrastructure (2026 Upgrade)

Open banking A2A payments have moved from niche adoption to mainstream consideration in 2026. What began under PSD2 as an experimental, API-driven alternative has matured into a viable payment rail for eCommerce, recurring billing, and high-velocity domestic transactions.

The combination of better API performance, stronger regulatory obligations and improved user experience means merchants now view A2A as a core strategic rail rather than a secondary option.

Payment Initiation Services (PIS): The Core of Open Banking A2A

Payment Initiation Services allow a customer to pay a merchant directly from their bank account through a regulated API. Unlike cards, which rely on issuer risk scoring, PIS payments initiate a direct bank-to-bank credit transfer.

The 2026 version of PIS is significantly stronger than the early PSD2 phase because:

- Bank API uptime has improved across the UK and EU.

- Authentication journeys are cleaner, using biometrics through banking apps.

- PSPs support more stable redirection flows, reducing user drop-offs.

- Settlement times align with domestic instant rails in many corridors.

Under the upcoming PSD3 and Payment Services Regulation (PSR), banks must provide more consistent APIs and clearer dispute-handling reporting for PIS. The European Commission outlines its reform package here:

https://finance.ec.europa.eu/consumer-finance-and-payments/payment-services/payment-services_en

These upgrades materially improve commercial viability.

Variable Recurring Payments (VRP): A2A for Subscriptions and Billing

VRP extends A2A beyond one-off payments by enabling regulated, pre-consented recurring transactions directly from bank accounts. After a customer approves a consent mandate, future charges can occur without repeated authentication, similar to card-on-file.

By 2026:

- Non-sweeping VRP is expanding through bank mandates and regulatory pressure.

- Merchant-initiated payments (MIT-equivalent) become realistic for utilities, subscriptions, and financial services.

- Refund workflows are improving, though still less structured than card chargebacks.

- PSPs are beginning to integrate VRP directly into routing logic, placing it alongside cards and instant rails.

VRP is still maturing, but its potential to replace card-on-file in domestic markets is becoming clearer.

Bank API Infrastructure: Reliability Moves to Production-Grade

Early open banking suffered from inconsistent bank APIs, outages, latency issues and unpredictable user journeys. That era is ending.

2026 improvements include:

- Stronger regulatory uptime requirements

- Standardised API payload formats

- Better SCA delegation flows

- More consistent consent-handling mechanisms

- Reduced variance in authentication screens between banks

These changes reduce one of the biggest historical UX pain points.

Why Open Banking A2A Works Better in 2026

From the merchant perspective, the 2026 upgrades deliver tangible benefits:

- Lower processing cost compared to card interchange and scheme fees

- No chargebacks, eliminating operational overhead

- Cleaner authentication through mobile biometrics

- Predictable settlement when paired with instant payment rails

- Reduced issuer-driven declines, as no card issuer risk scoring is applied

However, A2A does not replace cards universally. Its limitations remain:

- Bank login friction (compared to card-on-file)

- Weaker dispute frameworks

- Fragmented adoption across corridors

- Complex refunds compared to card rails

The Strategic Role of Open Banking A2A in 2026

In most European and UK use cases, A2A is evolving into:

- A cost-saving rail for domestic eCommerce

- A reliable settlement rail when paired with instant schemes

- A future-ready alternative for subscriptions via VRP

- A risk-reduced option with no chargeback exposure

- A gateway optimisation tool when issuer friction rises on cards

A2A is no longer positioned as a replacement rail but as a core component of a multi-rail strategy where merchants can choose the optimal payment rail for each journey.

Instant Payment Rails: FPS, SEPA Instant, RTP, PIX, UPI, PayTo & PayNow/PromptPay

Instant payment systems have become the backbone of domestic and regional A2A strategies. By 2026, they represent far more than “faster bank transfers”; they form a universal expectation that funds should move immediately, with no intermediaries adding friction or cost. Each region has built its own rail, and while they differ in governance, settlement models and refund mechanics, they share one defining principle: real-time, irrevocable payments.

UK: Faster Payments System (FPS)

FPS is one of the earliest instant payment rails, and in 2026, it remains central to retail banking and open banking PIS flows. FPS supports 24/7 settlement, with payments typically completing within seconds.

For merchants, FPS underpins open banking A2A reliability, enabling faster settlement cycles and predictable cash flow.

However, refund processes remain slower than card chargebacks and require operational coordination through PSPs and merchant support teams.

EU: SEPA Instant (SCT Inst)

The EU’s SEPA Instant scheme has evolved significantly since its initial adoption. From 2025 onward, the EU Instant Payments Regulation (IPR) obliges banks to deliver instant euro credit transfers within 10 seconds, at the same price as standard transfers.

For merchants, SCT Inst aligns open banking PIS with true real-time settlement, turning A2A into a viable alternative to cards for domestic euro payments. Refunds are manual, but the speed and predictability of settlement reduce liquidity gaps.

US: Real-Time Payments (RTP) & FedNow

The United States operates two real-time rails: RTP (The Clearing House) and FedNow (Federal Reserve). Both offer near-instant settlement, with RTP supporting request-to-pay flows useful for billing and marketplaces. Adoption is growing, but coverage is not yet universal across all issuing banks. Refund frameworks remain bank-driven and less structured than card disputes.

Brazil: PIX (Global Benchmark)

PIX has become the world’s most successful instant payment system, accounting for a majority of digital transactions in Brazil.

Key strengths include:

- Sub-five-second settlement

- QR-code interoperability

- Nearly universal consumer adoption

- Extremely low transaction cost

PIX sets the global benchmark for instant payment adoption speed and consumer behavioural familiarity. Many international PSPs now design A2A UX around PIX-style flows.

India: UPI (National + Emerging Cross-Border)

UPI is the most scalable A2A rail globally, processing tens of billions of transactions monthly.

Its strengths include:

- Mobile-first authentication

- Merchant QR readiness

- Low interchange-like fees

- Strong issuing-bank support

- Rapid expansion into cross-border corridors

UPI’s user experience, simple, biometric, mobile-native, sets a UX standard that other regions attempt to replicate.

Australia: PayTo (Mandated A2A for Recurring Payments)

PayTo is Australia’s next-generation A2A framework, enabling authenticated, pre-approved payments that behave similarly to VRP. Mandates are visible and managed in the customer’s banking app, improving transparency and dispute prevention. PayTo is particularly relevant for subscriptions and billing flows where recurring A2A is required.

Singapore & Thailand: PayNow / PromptPay Cross-Border Link

The PayNow-PromptPay cross-border system allows consumers and merchants to send money instantly between Singapore and Thailand using phone-number-based identifiers. This marks the beginning of regional instant payment interoperability, a trend expected to expand across ASEAN. For merchants, this creates a blueprint for low-cost, real-time cross-border settlement without card schemes.

The Strategic Role of Instant Payment Rails in 2026

In a multi-rail world, instant payments perform a distinct function:

- As a settlement rail for open banking PIS, giving A2A true commercial viability

- As a standalone payment rail in APAC and LATAM, where consumer adoption is extremely high

- As a liquidity stabiliser, it improves merchant cash flow compared to card T+1/T+2 cycles

- As a cost reducer, often priced significantly below card interchange fees

- As a foundation for recurrent A2A, enabling VRP- or PayTo-style consented billing

Instant rails are not universally mature, nor do they replace cards in high-dispute verticals. But in domestic markets, especially APAC and LATAM, they are becoming the backbone of merchant payment strategies.

Decision Matrix: Cards vs A2A vs Instant Payments

Selecting the right payment rail in 2026 requires a structured assessment of cost, conversion, settlement timing, chargeback exposure and refund complexity. Cards, open banking A2A and instant payment rails perform very differently across these dimensions. The matrix below provides a practical benchmark for merchants and PSPs evaluating which rail best aligns with their operational and commercial models.

Decision Matrix: Cards vs A2A vs Instant Payments (2026)

| Criteria | Cards | Open Banking A2A (PIS/VRP) | Instant Payment Rails (FPS, SCT Inst, PIX, UPI, PayTo) |

| Conversion Rate | High familiarity; friction depends on SCA exemptions | Strong when biometrics are used; drop-offs are possible during bank login | Very high in markets with rail familiarity (PIX, UPI); varies globally |

| Processing Cost | Highest (interchange, scheme fees, acquirer markups) | Low; typically fixed-fee or low variable pricing | Low; in many markets, near-zero transaction costs |

| Chargebacks / Disputes | Strong consumer protection but high merchant cost | No chargebacks; only complaints/PSR dispute routes | No formal chargebacks; refunds handled manually or via bank request |

| Refund Mechanics | Structured, standardised, predictable | Refunds possible but not standardised; PSP-driven | Refund mechanisms vary; they can be slower or manual |

| Settlement Speed | T+1–T+3, depending on acquirer and corridor | Immediate or near-instant when paired with instant rails | Real-time 24/7 settlement |

| Fraud Exposure | Strong issuer fraud models; high false decline risk | Lower fraud exposure; transaction initiated by the customer | Lower fraud; finality reduces misuse but raises irreversibility risk |

| Cross-Border Capability | Strongest global coverage | Limited to domestic/regional markets | Primarily domestic; select cross-border corridors are emerging |

| UX Friction | Familiar, fast; friction varies by SCA | Bank login can add steps, though, improving | Very fast in regions where instant payments are widely adopted |

| Recurring Payments | Mature card-on-file; widely supported | VRP is still evolving; non-sweeping is gaining traction | PayTo/UPI mandates show potential; not universal |

How Merchants Should Apply This Matrix

The decision matrix is not intended to declare a single “winning” rail. Instead, it highlights the trade-offs that matter when building a multi-rail payment strategy.

Cards excel when:

- Disputes matter

- Cross-border acceptance is essential

- Ticket values are high

- Regulatory expectations demand strong consumer protections

Open Banking A2A excels when:

- Cost reduction is a priority

- Domestic transactions dominate

- Authentication via mobile banking apps is reliable

- Chargeback exposure is problematic

Instant Payments excel when:

- Real-time settlement is commercially valuable

- The market has high adoption (PIX, UPI, FPS)

- Low-margin sectors require minimal processing cost

- Merchants want to avoid scheme pricing volatility

Why 2026 Requires Multi-Rail Decisions

Merchants can no longer optimise payments by relying on a single rail. Multiple forces, regulatory reform, issuer risk tightening, API improvements, consumer familiarity with bank apps and domestic instant payment adoption mean that the “best” rail depends entirely on context:

- Corridor

- Product type

- Refund expectations

- Dispute frequency

- Operational readiness

- Customer behaviour

- Cost sensitivity

The decision matrix allows merchants and PSPs to map these variables and engineer a rail selection strategy that aligns with performance, compliance and economics.

Fraud, Disputes & Liability Across Each Rail

Fraud management and liability allocation differ fundamentally across cards, open banking A2A, and instant payment rails. For merchants, these differences are not simply operational; they shape revenue protection, customer support models, dispute handling and overall payment strategy. By 2026, understanding how each rail handles liability is one of the most important considerations when deciding which payment method to prioritise.

1. Fraud Dynamics on Card Rails

Card networks have the most established fraud and dispute frameworks. Issuers apply behavioural analytics, device scoring, velocity controls and sector-level risk models. This maturity reduces the risk of unauthorised transactions but increases false declines, particularly for cross-border or high-risk categories.

For merchants, the key exposures include:

- Dispute fees from schemes and acquirers

- Operational workload from managing evidence packs and representments

- Scheme monitoring pressures for excessive fraud or disputes

Cards provide consumer protection but create heavy merchant liability and operational costs.

2. Fraud & Liability in Open Banking A2A (PIS & VRP)

Open banking payments are customer-initiated, which fundamentally changes the fraud model. Because the payer authenticates directly with their bank:

- Issuer-driven fraud scoring does not apply

- False declines are significantly lower

- Fraud exposure shifts away from the merchant

However, the absence of card-style chargebacks means merchants face a different structure:

- No formal chargeback rights

- Bank-initiated reversals only in narrow cases (e.g., technical error, regulatory breach)

- Consumer complaints follow banking dispute routes, not merchant-led chargebacks

- Refunds depend on merchant policy and PSP workflows

This reduces fraudulent disputes but introduces complexity when consumers expect “card-like” resolution pathways.

For VRP:

- Mandate transparency reduces misuse

- Dispute handling remains less structured than card rails

Open banking reduces fraud losses but requires strong refund and customer care processes.

3. Fraud & Liability in Instant Payment Rails

Instant payment systems, FPS, SCT Inst, UPI, PIX, PayTo, PayNow/PromptPay, share a common characteristic: finality. Once the payment is executed, it cannot be reversed through a consumer-initiated dispute like a chargeback.

This finality fundamentally changes liability:

- Fraud losses are typically borne by the payer, not the merchant

- Banks may support recall requests, but these are discretionary

- Refunds must be handled directly through merchant support systems

- Regulatory frameworks vary greatly by region

The absence of chargebacks is highly attractive to merchants, but it increases the need for:

- Strong upfront authentication

- Transparent refund policies

- Clear customer communication

- Operational readiness for complaint management

Fraud volumes are often lower on instant payment rails due to strong biometric authentication and bank-grade risk controls. However, the irreversibility risk can increase customer anxiety in unfamiliar markets.

4. What Liability Means for Merchants in 2026

When comparing all three rails, the liability landscape can be summarised as follows:

- Cards: High consumer protection → High merchant liability → Heavy operational workload.

- Open Banking A2A: Strong authentication → No chargebacks → Merchant-led refund processes.

- Instant Payments: Irreversible → Minimal fraud disputes → Merchant-managed resolution pathways.

Choosing the right rail is therefore not just a cost or conversion decision, but a liability strategy. Sectors with high dispute potential may still rely on cards; sectors with predictable customer relationships and low refund friction benefit from A2A and instant rails.

In 2026, the most resilient merchants blend all three rails, aligning liability with the risk profile of each product, corridor and consumer journey.

Customer Experience (UX) Comparison: Behaviour & Friction by Rail

Choosing the right payment rail isn’t only about cost or liability. In 2026, the biggest driver of rail adoption is customer experience, how quickly, confidently and predictably a user can complete a transaction. Cards, open banking A2A and instant payment rails all deliver very different levels of friction, familiarity and trust. These UX differences have a direct impact on conversion, repeat usage and the overall revenue curve for merchants.

1. UX on Card Rails: Familiar, Fast, but Dependent on SCA Outcomes

Cards continue to provide one of the strongest UX experiences for consumers, mainly due to decades of behavioural conditioning. Customers instinctively understand the card flow, recognise stored credentials, and feel reassured by chargeback rights.

What works well:

- Familiarity: Customers trust card payments by default.

- Speed: Minimal cognitive load for checkout.

- Stored details: Reduces friction for returning users.

- Exemptions: When SCA exemptions apply, friction is close to zero.

What creates friction:

- 3DS challenges: Extra steps reduce completion rates.

- Issuer-controlled risk scoring: False declines interrupt UX.

- Cross-border behaviour: Higher challenge rates and SCA friction.

Cards deliver strong performance where trust and habit matter most, but SCA-driven unpredictability can damage conversion, especially for high-risk merchants or in specific corridors.

2. UX on Open Banking A2A: Improving Rapidly, Driven by Mobile Banking Behaviour

Open banking A2A (PIS) relies on bank app authentication, which has become significantly smoother as banks adopt biometrics and streamline consent flows. UX is now aligned with everyday mobile banking habits.

What works well:

- Strong biometric authentication: Fast and intuitive.

- No card details needed: Reduces data-entry friction.

- Increasing consumer familiarity: Particularly in the UK and parts of the EU.

What creates friction:

- Mandatory bank login: Adds cognitive effort compared to card-on-file.

- UI inconsistency between banks: Some flows remain slower or more fragmented.

- Limited cross-border acceptance: Users may encounter unfamiliar flows.

A2A UX is strongest for mobile-first customers who regularly use banking apps. However, it still lags behind cards for impulse purchases or older demographics unfamiliar with bank-driven authentication prompts.

3. UX on Instant Payment Rails: Fastest Experience Where Adoption Is High

Instant payment systems like PIX, UPI, PayNow, PromptPay and even Faster Payments offer the fastest path to transaction completion, provided that consumers are accustomed to the rail.

What works well:

- True real-time payment completion.

- Simple QR or app-based flows: Especially in APAC and LATAM.

- Strong consumer confidence: Built on mobile-first banking ecosystems.

- No multi-step authentication: Native biometric approval in most markets.

Where friction appears:

- Irreversible payments: Some consumers hesitate if unfamiliar with the rail.

- Regional fragmentation: UX consistency varies widely between countries.

- Limited refund expectations: Customers accustomed to card chargebacks may worry.

In regions like Brazil, India, Thailand and Singapore, instant payment UX significantly outperforms cards, especially for low-ticket or high-frequency purchases. In Europe, UX strength depends on corridor maturity and consumer habit formation.

4. Behavioural Impact: What the Data Trends Suggest for 2026

Across markets, three behavioural trends emerge:

Trend 1: Mobile-first authentication is normalising friction

Consumers now trust biometrics more than passwords or OTPs. This benefits A2A and instant payments, closing the UX gap with stored cards.

Trend 2: Irreversibility affects consumer confidence

While instant payments are fast and clean, consumers still expect card-like dispute routes in unfamiliar sectors. Merchant communication becomes essential.

Trend 3: UX expectations are diverging by region

- APAC + LATAM: Instant payments dominate due to mobile-pay familiarity.

- UK + EU: A2A adoption is increasing as bank UX improves and IPR mandates real-time capability.

- US: Card familiarity remains strong; adoption curves lag.

5. How UX Should Influence Rail Selection

UX is not the same across customer segments:

- Impulse purchases → Cards

- High-frequency, mobile-first → Instant payments

- Trusted merchant relationships → A2A (PIS/VRP)

- Subscription lifecycle → Cards for initiation, VRP for repeat billing

- High-ticket travel → Cards due to dispute protection

The merchants that perform best in 2026 are not the ones choosing a single “best” UX, they are those creating rail-personalised journeys, giving customers a payment method that aligns with expectation, trust and behavioural flow.

PSP / Gateway Roadmaps: Supporting A2A in 2026

For PSPs, acquirers and gateways, the rise of A2A and instant payment rails is not simply a product expansion; it represents a structural rewiring of their entire payment architecture. Cards remain central to merchant revenue, but PSPs now face a dual obligation: maintaining high card approval performance while building robust connectivity to open banking PIS/VRP and domestic instant rail networks. This shift defines the 2026 roadmap for most European, UK and APAC PSPs.

1. API Connectivity: From Card Rails to Multi-Rail Gateways

Legacy gateway infrastructure was designed for card tokenisation, 3DS flows, and acquirer switching.

A2A requires a fundamentally different base layer:

- Direct PIS connections to banks (or via regulated TPP aggregators)

- VRP mandate setup + consent lifecycle management

- Instant payment initiation + confirmation APIs

- Unified API surface for merchants across all rails

PSPs moving into A2A must operate as multi-rail API providers, not card-centric gateways.

2. Integrating A2A Into Routing Logic

PSPs in 2026 are evolving from “card-first” routing engines into rail-agnostic decision engines.

Key routing layers expanding include:

- Rail selection logic: card → A2A → instant

- Fallback mapping: When A2A fails, route to card; when card soft-declines, prompt A2A

- Risk/consent profile routing: use VRP for trusted customers, cards for first-time users

- Corridor-based routing: PIX in Brazil, UPI in India, SCT Inst for euro payments

The orchestration logic that once applied only to acquirer choice must now apply across payment rails themselves.

3. Reconciliation & Settlement: The Biggest Technical Upgrade

A2A settlement is fundamentally different from card settlement:

- Cards: batch-based, T+1/T+2, scheme-based reporting

- A2A: bank-driven, immediate/near-instant, no scheme intermediary

- Instant rails: real-time posting, 24/7 availability

PSPs must modernise reconciliation systems to handle:

- Mixed settlement cycles

- Instant payment confirmations

- Multiple refund flows

- PSP vs bank-led exception handling

This has become a primary investment theme for PSPs in 2026.

4. Refunds & Disputes: Merchant Support Needs a New Structure

Cards have structured chargebacks; A2A and instant payments do not.

PSPs are building new merchant tools for:

- A2A refunds (merchant-driven, not bank-driven)

- Complaint management dashboards

- VRP mandate cancellation flows

- Instant payment recall requests (where supported)

- Bank-API error transparency

Merchants expect “card-like clarity”, even though A2A has no card-style chargebacks. PSPs must close that experience gap.

5. Authentication & Consent Management

A2A flows depend on:

- Biometric authentication

- Bank app redirection

- Consent screens and mandate storage

In 2026, PSPs must support:

- Mandate dashboards for VRP and PayTo

- Consent expiry notifications

- SCA alignment across all rails

- Pre-authentication logic for multi-step A2A journeys

This is a significant shift from traditional 3DS models.

6. Data & Risk Modelling: A2A Requires New Signals

Cards have decades of issuer fraud data behind them. A2A does not, so PSPs are investing in new risk layers:

- Bank API behavioural signals

- Device intelligence during A2A initiation

- Consent-level risk analytics (VRP/PayTo)

- Instant payment fraud typology mapping

PSPs must develop a new risk engine to balance A2A’s low chargeback exposure with its irreversible payment finality.

7. PSP Commercial Models: New Pricing Paradigms

PSPs traditionally monetised card processing through:

- % fees

- Scheme routing markups

- FX spreads

- Acquirer fees

A2A changes everything. New commercial models include:

- Fixed-fee PIS pricing

- VRP mandate-based pricing

- Per-rail pricing (PIX, UPI, FPS, SCT Inst)

- Instant confirmation APIs

PSPs in 2026 must design commercial structures that reflect a multi-rail environment rather than card-centric economics.

8. The PSP Roadmap Summary

To compete in 2026, PSPs and gateways must deliver:

- Rail-agnostic APIs

- Real-time settlement support

- Hybrid routing (cards + A2A + instant rails)

- VRP/PayTo consent lifecycle capabilities

- A2A refund frameworks

- Multi-rail reconciliation

- Advanced data + risk modelling

- Regional instant rail integration (PIX, UPI, PayNow, SCT Inst, FPS)

PSPs that fail to modernise will become bottlenecks as merchants shift toward low-cost, low-latency payment methods.

Merchant Use Case Scenarios: Choosing the Right Rail per Vertical

A2A and instant payment adoption cannot be evaluated in isolation. Different industries operate with different refund behaviours, dispute expectations, fraud patterns, customer journeys and corridor exposures. The optimal payment rail in 2026 varies significantly from one vertical to another. Below are structured, real-world merchant scenarios showing which rail works best, when, and why.

1. Retail eCommerce (Low–Mid Value, High Volume)

Retail flows are dominated by convenience, impulse behaviour and repeat purchases.

Best Rail Mix:

- Cards → best for impulse purchases, stored credentials, and low-friction repeat cycles.

- A2A (PIS) → strong for cost reduction in domestic markets with strong bank-app adoption.

- Instant Payments → competitive when mobile-first customers expect immediate processing (e.g., UPI, PIX).

Why this mix works:

Card familiarity preserves conversion, while A2A reduces costs for predictable customers. Instant payments unlock low-margin viability in APAC/LATAM.

2. iGaming & High-Risk Verticals

High dispute environments with aggressive issuer risk scoring and strict compliance.

Best Rail Mix:

- Cards → still essential for high-value deposits and established trust flows.

- Instant Payments → strong adoption in markets like India/Brazil (UPI/PIX), offering real-time account funding.

- A2A → useful for domestic corridors where reliability is high, but refund complexity must be managed.

Why this mix works: Instant rails deliver fast deposits; cards manage high-value stakes; A2A supports regulated markets with stable bank flows.

3. Travel & Airlines

High basket sizes + multi-leg journeys + refund-heavy flows = high dispute complexity.

Best Rail Mix:

- Cards → primary rail due to structured chargebacks and strong consumer protection.

- A2A → secondary rail only in domestic markets where refunds are predictable.

- Instant Payments → limited due to irreversibility concerns for high-ticket purchases.

Why this mix works:

In travel, disputes are common, and consumers expect chargeback rights. Cards anchor trust and reduce operational disputes.

4. Subscriptions & Recurring Billing (SaaS, Membership, OTT)

Recurring payments depend on seamless re-authentication and mandate stability.

Best Rail Mix:

- Cards → remain the easiest method for subscription initiation.

- VRP (A2A Recurring) → strong for stable domestic relationships; reduces churn and failed renewals.

- Instant Rails → relevant only where VRP-like mandate systems exist (e.g., PayTo, UPI AutoPay).

Why this mix works: Cards for onboarding → VRP/PayTo for ongoing billing → hybrid model reduces lifecycle friction.

5. Marketplaces & Platforms

Complex split-pay flows with multi-sided settlement.

Best Rail Mix:

- A2A → strong for pay-ins to minimise cost.

- Instant Rails → ideal for pay-outs (creator payments, same-day settlement).

- Cards → maintain optionality for cross-border buyers.

Why this mix works: Marketplaces prioritise settlement speed and low fees. Instant rails drastically improve liquidity for sellers.

6. Digital Goods & Microtransactions

High volume, low margin; conversion and speed are crucial.

Best Rail Mix:

- Instant Payments → fastest experience; extremely low cost; strong adoption in mobile-first markets.

- A2A → good for domestic flows with strong mobile banking habits.

- Cards → valuable for global reach and frictionless stored credentials.

Why this mix works: Instant payments eliminate cost barriers; cards protect reach; A2A balances domestic economics.

7. Financial Services, Lending & Wealth Apps

Settlement speed and regulatory alignment matter most.

Best Rail Mix:

- Instant Payments → ideal for disbursements, withdrawals and top-ups.

- A2A → strong for secure pay-ins (loan repayments, savings transfers).

- Cards → used sparingly for customer acquisition flows.

Why this mix works: Instant rails deliver immediacy; A2A improves repayment reliability; cards remain optional.

How Merchants Should Use These Scenarios

These sector profiles show that no single rail is optimal across all industries.

Merchants must map:

- Dispute exposure

- Refund behaviour

- Consumer familiarity

- Basket size

- Settlement requirements

- Corridor coverage

- Operational bandwidth

This forms the foundation for the 2026 A2A Playbook, rail selection based on behaviour, risk and commercial logic rather than convenience or legacy assumptions.

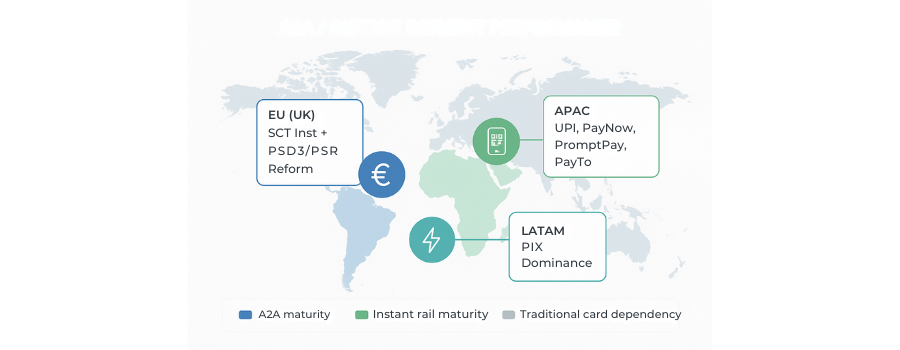

Corridor-Level Strategy: How Rail Performance Varies Across Regions

Payments are no longer global in a uniform sense. In 2026, payment behaviour, infrastructure maturity, regulatory expectations and real-time settlement capabilities vary dramatically by region. A merchant’s A2A strategy must therefore be corridor-specific, not globally standardised.

This section outlines how cards, A2A and instant payments behave across the UK, EU, APAC, LATAM and emerging Middle Eastern/African markets and how merchants should adapt rail selection accordingly.

United Kingdom: The Most Mature Open Banking Market in Europe

The UK is the most advanced A2A corridor due to:

- High mobile banking adoption

- Well-established PIS flows

- VRP (non-sweeping) expansion

- Faster Payments (FPS) reliability

Best performing rails in 2026

- A2A (PIS): very strong for domestic eCommerce

- VRP: excellent for recurring billing and utilities

- Cards: still essential for cross-border, travel and high-friction journeys

Strategic recommendations

- Offer A2A as a primary low-cost rail for UK customers.

- Use cards as a fallback or for high-value purchases requiring dispute comfort.

- Implement VRP for subscription renewal flows to reduce involuntary churn.

European Union: IPR Obligations + PSD3/PSR Interaction

The EU is undergoing the most significant regulatory shift of all corridors. Three frameworks are reshaping A2A adoption:

1. Instant Payments Regulation (IPR)

Requires banks to execute euro instant payments within 10 seconds and at no surcharge over standard transfer pricing.

2. PSD3

Modernises PSD2 with stronger rules on authentication, fraud reporting and API reliability.

3. Payment Services Regulation (PSR)

Brings open banking elements into a directly applicable regulation, improving:

- API standardisation

- Data access

- Dispute transparency

- Availability requirements

Best performing rails in 2026

- A2A (PIS) + SCT Inst: strong for domestic payments

- Cards: critical for cross-border and dispute-heavy segments

Strategic recommendations

- Prioritise SCT Inst for eurozone domestic flows.

- Leverage PIS to reduce cost where bank adoption is strong.

- Maintain cards for cross-border and high-dispute categories (travel, digital goods).

APAC: UPI, PayTo, PayNow, PromptPay and Regional Instant Payment Growth

APAC is the most dynamic instant payment region globally.

India: UPI

- The world’s most scaled A2A system

- Biometric approval + mobile-first UX

- Growing global acceptance (UAE, Singapore, France corridors)

Australia: PayTo

- Mandated bank-to-bank consented payments

- Designed for recurring billing, similar to VRP, but more mature in mandate flow

- Ideal for subscriptions and predictable billing cycles

Singapore–Thailand: PayNow/PromptPay Cross-Border

- Phone-number-based cross-border instant transfers

- Structurally significant for future ASEAN interoperability

- Excellent model for low-cost cross-border settlement

Best performing rails in APAC

- Instant payments (UPI, FAST, PayNow/PromptPay) dominate consumer behaviour

- A2A works extremely well for pay-ins

- Cards retain importance for travel, international shoppers, and high-ticket purchases

Strategic recommendations

- Lead with instant payment rails for domestic APAC users.

- Use A2A as the default for bill payments, subscriptions, and financial services.

- Ensure cards are available for cross-border and travel bookings.

LATAM: PIX Sets the Global Standard

Brazil’s PIX system has become the global benchmark for A2A success:

- Instant settlement

- Near-zero transaction cost

- Universal adoption

- Strong consumer trust

- QR interoperability

In LATAM:

- PIX is the dominant rail for both pay-ins and payouts.

- Cards remain important for international purchases and refund-heavy journeys.

Strategic recommendations

- Prioritise PIX for domestic Brazil volumes.

- Maintain cards for cross-border flows and travel.

- Use A2A where PIX infrastructure expands regionally (e.g., Chile, Colombia initiatives).

Middle East & Africa: Emerging Instant Rails

A2A and real-time payment adoption is accelerating with rails such as:

- UAE Instant Payments Platform (IPP)

- Saudi Arabia’s SARIE instant rail upgrade

- South Africa’s Rapid Payments Programme (RPP)

These systems are still early-stage but represent the beginning of regional instant payment modernisation.

Strategic recommendations

- Offer cards as the primary payment method for now.

- Introduce instant rails where adoption is meaningful (UAE, KSA, South Africa).

- Monitor regulatory mandates closely as open banking frameworks evolve.

Corridor Strategy Summary

2026 requires rail-by-rail, corridor-by-corridor decision engineering:

- UK: A2A + VRP strongest in Europe

- EU: SCT Inst + PSD3/PSR driving structural reform

- APAC: Instant payment rails dominate (UPI, PayNow, PromptPay, PayTo)

- LATAM: PIX becomes the commercial default

- Middle East/Africa: Instant rails emerging, cards remain central

No single rail wins globally. Merchants must design regionalised, multi-rail stacks aligned with regulation, consumer behaviour and settlement infrastructure.

Merchant A2A Strategy Playbook (2026)

By 2026, rail selection is no longer an abstract conceptual exercise. Merchants must design multi-rail strategies that align with regional adoption, customer expectations, fraud/loss frameworks, cost structure and API availability. The A2A playbook below provides a structured approach to making rail decisions, preparing operations, and measuring performance in a multi-rail world.

Rail Selection Model: When to Use Cards, A2A, and Instant Payments

A2A is not a universal replacement for cards; instant rails are not universally mature; and cards remain essential in dispute-heavy and cross-border environments. The selection model below helps merchants determine which rail to prioritise per scenario.

1. Use Cards When:

- Disputes or refunds are frequent

- Basket values are high

- The purchase is cross-border

- Customer is a first-time or one-off payer

- Stored credentials improve conversion

2. Use A2A (PIS/VRP) When:

- Domestic purchases dominate

- Reducing processing cost is a priority

- The customer uses mobile banking frequently

- Subscription renewals or bill payments are involved

- Chargeback exposure is problematic

- Reliability of bank APIs is high in the corridor

3. Use Instant Payments When:

- Settlement speed is commercially valuable

- Customers are mobile-first (APAC/LATAM)

- Payouts or withdrawals are part of the user journey

- Merchant operates in low-margin or high-frequency flows

- The local market has high adoption (PIX, UPI, PayNow/PromptPay)

This model ensures rail decisions are grounded in behavioural, commercial and operational realities, not defaulting to what’s familiar.

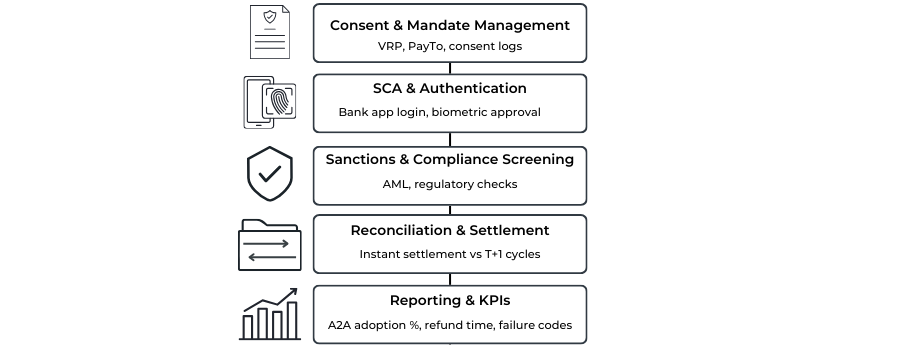

Operational Readiness Checklist (Consent, SCA, Sanctions, Reconciliation, Reporting)

A2A and instant payments succeed only when merchants prepare their operational stack correctly.

The checklist below covers the essential operational requirements for a 2026-ready A2A environment.

Consent & Mandate Management

- Store customer consent (VRP/PayTo) with clear visibility.

- Support mandate revocation and renewal workflows.

- Ensure customer notifications for consent updates or expiries.

- Maintain audit logs for compliance.

Strong Customer Authentication (SCA) Alignment

- Align routing with bank-driven biometric flows.

- Monitor bank-specific authentication drop-off patterns.

- Implement SCA fallback logic for inconsistent API behaviours.

- Prepare transparent messaging for customers during re-authentication.

Sanction Screening & Regulatory Compliance

- Align A2A flows with transaction-monitoring expectations.

- Introduce screening for VRP/PayTo recurring instructions.

- Integrate bank-level sanctions responses into payment status reporting.

- Ensure PSP-level compliance logs meet PSD3/PSR auditing expectations.

Reconciliation & Settlement Processes

- Support mixed settlement cycles (real-time, T+1, batch).

- Ensure reconciliation files differentiate rails clearly.

- Prepare workflows for A2A refund processing (merchant-initiated).

- Track failed or delayed instant payments at the bank API layer.

Reporting & Analytics

- Build dashboards separating A2A, instant, and card performance.

- Monitor success/failure codes from banks to understand root causes.

- Log API reliability, authentication steps and consent events.

- Provide financial reporting aligned with regulatory formats.

A2A is operationally different from cards, and this checklist helps merchants build the necessary backbone.

KPI Framework (A2A Adoption %, Refund Time, Dispute Rate, Net Cost)

Payment strategy must be measurable. The KPI framework below ensures merchants monitor the right metrics across A2A, instant payments and cards.

Primary A2A KPIs

- A2A Adoption Rate (%)

% of customers selecting A2A vs cards. - A2A Conversion Rate

Completion rate from initiation → bank authentication → final settlement. - Instant Refund Completion Time

Speed at which funds return to consumers (where the process exists). - Dispute / Complaint Rate

Bank-directed complaint volume vs overall transactions. - Net Processing Cost Per Rail

Consolidated cost including PSP fees, refunds, and operational overhead.

Instant Rail KPIs

- Real-time settlement success rate

- API failure incidence by bank

- Authentication pass rate

- Retry request success (where supported)

Card KPIs (for comparison)

- SCA challenge success rate

- Soft-decline recovery

- Chargeback ratio

- Approval rate by BIN/corridor

The KPI framework ensures payment teams make data-led decisions about which rail to surface prominently in each journey.

Integration & Rollout Blueprint: Phased A2A Deployment

A2A and instant payments should not be launched globally in one step. A phased rollout avoids UX shocks, operational friction and unexpected cost exposure.

Phase 1: Corridor Prioritisation

- Identify top domestic markets with strong bank APIs.

- Select instant rails where consumer adoption already exists (PIX, UPI).

- Assess regulatory readiness (IPR in the EU, VRP in the UK, PayTo in Australia).

Phase 2: Merchant & PSP Integration

- Develop a unified payment API supporting cards + A2A, + instant rails.

- Integrate PIS flows; enable VRP where available.

- Align routing logic with customer value segments.

- Implement consent dashboards and reconciliation files.

Phase 3: Controlled Rollout

- Make A2A the default for domestic users where conversion supports it.

- Retain cards as a fallback and for cross-border payments.

- Use instant rails for deposits, withdrawals or payouts.

- Monitor authentication failures, API errors and settlement reliability.

Phase 4: Optimisation

- Refine routing based on KPIs.

- Introduce smart nudges for cost-optimal rails.

- Add instant refunds if supported by PSP.

- Improve VRP usage for recurring flows.

Phase 5: Scale & Automation

- Expand rails regionally (APAC, LATAM, EU corridors).

- Automate settlement reports and reconciliation.

- Use KPI outputs to dynamically feature preferred rails at checkout.

- Introduce orchestration logic between payment rails, not just acquirers.

This blueprint ensures merchants transition into A2A through controlled, measurable steps rather than high-risk operational leaps.

Conclusion

The 2026 payments environment demands that merchants and PSPs move beyond single-rail thinking. Cards remain foundational, but rising issuer friction, scheme fees and dispute costs mean they can no longer anchor every customer journey. Open banking A2A has matured into a commercially viable alternative for domestic eCommerce, while instant payment rails have become the fastest and most cost-efficient route in mobile-first markets across APAC and LATAM.

The structural reforms introduced through the EU’s Instant Payments Regulation, PSD3 and the PSR are reshaping the economics and reliability of bank-to-bank payments. At the same time, regional instant rails such as UPI, PIX, PayNow/PromptPay and PayTo are setting new expectations around settlement speed and authentication experience. These shifts mean that choosing the right rail in 2026 is no longer about preference; it is an operational, regulatory and commercial requirement.

The merchants that perform best are those who treat rail selection as a strategic design problem. They align cards, A2A and instant payments with corridor realities, risk exposure, UX patterns and refund frameworks. They deploy consent-driven recurring models where appropriate, route pay-ins and pay-outs intelligently, and measure performance through a disciplined KPI framework. PSPs that support this shift, with multi-rail routing, strong reconciliation, clear refund tooling and mandate lifecycle management, will define the next generation of payment infrastructure.In 2026, the winning payment strategy is a multi-rail strategy: one that recognises that no single rail is universally optimal, but the right combination can deliver lower cost, higher conversion, faster settlement and more predictable performance across global markets. Cards, A2A and instant payments each have a role, and the merchants that master their interplay will set the commercial benchmark for the next phase of digital payments.

FAQs

1. What is the main difference between cards and A2A payments in 2026?

Cards use issuer-controlled risk scoring, allow chargebacks and support global acceptance, making them ideal for high-ticket and cross-border journeys. A2A payments route money directly from a customer’s bank account using PIS/VRP, offering lower cost, fewer false declines and real-time settlement in supported corridors. However, A2A does not offer chargeback rights, so refunds and dispute processes work differently.

2. Are A2A and instant payments the same thing?

No. A2A refers to bank-to-bank transfers initiated via open banking APIs (PIS/VRP). Instant payments are a settlement speed, not a method; rails like FPS, SCT Inst, UPI or PIX push funds in real time. A2A can run over instant rails, but the two are not interchangeable.

3. Why do merchants adopt A2A if cards already work globally?

A2A reduces processing cost, lowers false declines and offers predictable authentication via mobile banking apps. In domestic markets with high bank-app adoption (UK, EU, India, Singapore, Brazil), A2A often outperforms cards for cost, reliability and UX. Merchants still keep cards for cross-border traffic and refund-heavy sectors like travel.

4. Do A2A payments support refunds and recurring billing?

Yes. Refunds are merchant-initiated rather than controlled by banks or schemes. For recurring billing, VRP (UK), PayTo (Australia), and UPI AutoPay (India) allow consented bank withdrawals similar to card-on-file, but with more control for the customer and lower risk of payment failures.

5. Are instant payments safe for customers if they cannot be reversed?

Instant rails rely on strong biometric authentication, bank-driven risk models and real-time fraud detection, making them highly secure. The lack of chargebacks increases payment finality, but customers can still raise complaints with their bank, and merchants must offer clear refund routes.

6. Will instant payments replace cards globally?

No. Instant payments dominate in APAC and LATAM, but cards remain essential for global travel, large purchases, subscription onboarding and cross-border acceptance. The 2026 trend is multi-rail stacks, not replacement.

7. Which rail provides the best conversion rate in 2026?

It depends on the corridor. Cards remain strong globally, but instant payment rails outperform cards in UPI-, PIX- and PayNow-dominant markets. In Europe and the UK, A2A conversion improves significantly where biometric authentication shortens the flow.

8. How does PSD3 impact A2A adoption?

PSD3 strengthens bank API availability, improves authentication standards and clarifies fraud reporting. Combined with the PSR and IPR requirements, PSD3 makes A2A payments more reliable, regulated and commercially viable for merchants and PSPs.

9. Can merchants use A2A for cross-border payments?

Mostly no, A2A works best domestically because banks operate in-country. Some early cross-border initiatives (PayNow–PromptPay, UPI overseas expansion, PIX partnerships) exist, but cards remain the most scalable cross-border rail.

10. Why are refunds more complex on A2A and instant payment rails?

These rails do not include chargebacks or scheme-led dispute processes. Refunds must be initiated by merchants and handled through their PSP. This requires clear operational processes but reduces fraud-driven disputes significantly.

11. What KPIs should merchants track when adopting A2A?

Key metrics include A2A adoption %, bank authentication completion rates, instant refund speed, API failure incidence, dispute volume, and net processing cost per rail. These KPIs help merchants optimise routing and determine when to surface A2A over cards.

12. Do instant payments reduce fraud?

Yes, in most markets they do. Biometric authentication and bank-controlled risk models lower fraud attempts. Fraud does not disappear, but the exposure is different because transactions are pushed by the customer and validated in real-time.

13. Should merchants promote A2A as the primary payment method?

Only in markets where A2A is mature (UK, NL, DE, SE, BR, IN, SG). A2A should not fully replace cards, but can safely be surfaced first for returning users, domestic buyers or high-frequency purchases where consent and authentication are predictable.

14. What does a strong multi-rail strategy look like in 2026?

Cards for cross-border and disputes, A2A for domestic cost optimisation, and instant payments for real-time settlements in mobile-first regions. Merchants that build rail-personalised journeys see higher approval rates, lower processing costs and more predictable conversions.